NACAS Of Companies Act 1956 Vis-à-vis NFRA Of Companies Act 2013

(National Advisory Committee on Accounting Standard vis-à-vis National Financial Reporting Authority)

As a corporate professional one should be equipped with the knowledge of the bodies set up under the company law to advice the central government and regulate the issues in regard to the standards of accounting and auditing which a company or a particular class of company must have to adopt.

NACAS set up under Companies act 1956 and NFRA set up under Companies act 2013 are the bodies for the purpose of advisory and regulation of compliances with the standards notified in relation to accounting and auditing. The NACAS will no longer be in action after applicability of section 132 of the Companies act 2013, which deals with NFRA. Following information about the above-mentioned bodies can be the basis of distinction between the aforesaid two statutory bodies.

A brief about NACAS set up under Companies Act 1956

The Companies (Amendment) Act, 1999, new sub-sections (3A), (3B) and (3C) were inserted in section 211, which required that the every balance sheet and profit & loss account of the Company shall comply with the accounting standards, as may be prescribed by the Central Government in consultation with the National Advisory Committee on Accounting Standards (NACAS). Therefore, Section 210A was enacted to constitute an Advisory Committee to be called “National Advisory Committee on Accounting Standards”.

Main Objective of NACAS

To advise the Central Government on the formulation and lying down of accounting policies and accounting standards for adoption by companies or class of companies under this Act but at the same time NACAS did not have any regulatory powers to regulate the above issues. In simple words the role of NACAS was only restricted to the advisory.

Constitution of NACAS set up under Companies Act 1956

A brief about NFRA set up under Companies Act 2013

The concept of having a body such as National Financial Reporting Authority is a modified concept the bare of which was extracted from Companies act 1956.

In Companies Act, 2013, the new authority is set up named National Financial Reporting Authority (NFRA). It is an advisory body which will also function as the regulatory authority for the accounting policies for same purposes for which NACAS was set up under Companies act 1956.

Main Objectives of NFRA

Main Objectives of NFRA

(a) The first objective is similar to the objective of NACAS i.e. advice the Central Government on the formulation and laying down of accounting and auditing policies and standards for adoption by companies or class of companies or their auditors.

(b)The second objective is of regulatory nature which aims at monitoring and enforcing the compliance with accounting standards and auditing standards along with the quality of service provided by professionals, ensuring compliance with standards, and suggest measures required for improvement in quality of service of the professionals.

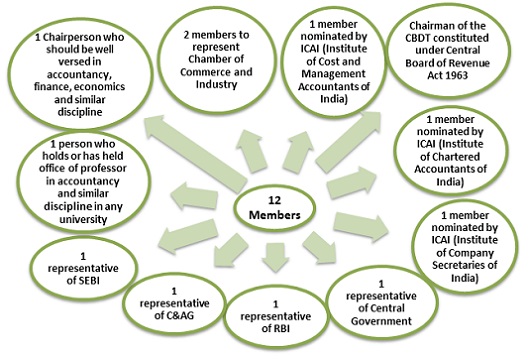

Constitution of NFRA

Other Regulatory Powers given to NFRA which was not there with NACAS

Other Regulatory Powers given to NFRA which was not there with NACAS

(a) NFRA has the power to investigate, either suo moto or on a reference made to it by the Central Government, for bodies corporate or persons, into the matters of professional or other misconduct committed by any member or firm of chartered accountants.

(b) NFRA has the same powers as are vested in a civil court under the Code of Civil Procedure, 1908, while trying a suit

- discovery and production of books of account and other documents

- Power to Summon the attendance of persons and examining them on oath

- Power of inspection of any books, registers and other documents of any person

(c) Power to impose penalty if misconduct proved

(d) NFRA has also the power of debarring the member or the firm from engaging himself or itself from practice as member of the Institute of Chartered Accountant of India for a minimum period of six months or for such higher period not exceeding ten years.

There is also a provision for appellate authority where aggrieved person can appeal against the order of NFRA. The head office of NFRA shall be at New Delhi and it may, meet at such other places in India, as it deems fit. Its accounts shall be audited by Comptroller and Auditor General of India (CAG) and such accounts as certified by CAG, together with audit report, shall be forwarded annually to the Central Government

The intention of the legislatures to bring NFRA to weed out the shortcomings of the NACAS is laudable yet it may be construed to undermine the powers and authority of the Institute of Chartered Accountants of India with respect to the matter of professional misconduct and other allied matters.

CA Hemant Sharma – Membership No. 535518

CA Hemant Sharma – Membership No. 535518

For feedback and queries please feel free to mail @ hemant.sharma53@outlook.com