Goods and Services Tax

Log in to FollowGoods and Services Tax India: Read all latest GST news, articles, notification, circulars, case laws news on, MVAT DVAT PVAT GST GSTN IGST CGST GST Council GST Rates SGST GST Forms GST Rules.

Movement of Capital goods between distinct person not supply

GST on Merchant Export

HC set-aside Cryptic, unreasoned & unpalatable GST Registration cancellation Order & SCN

Services rendered to holding company under an agreement does not make service provider an intermediary

Patna HC Sets Aside GST Registration Cancellation order – Directs reconsideration

HC allows Revocation of GST Registration under notification dated 31.03.2023

Utttar Pradesh Jal Nigam is not a Local authority; 18% GST applicable on works contract services

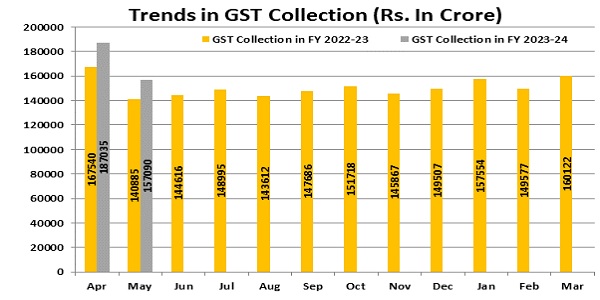

India’s GST Revenue for May 2023 Surpasses ₹1.57 Lakh Crore

Recent Updates In GST till 01st May 2023

Notice In Form ASMT-10 Invalid If Issued by Other Than Proper Officer Without Authorisation

Payment of mandatory pre-deposit directed against detention order

CBIC chairman Highlights Future-Ready Initiatives & Enforcement Successes

GST Implication on Goods sent for Exhibition

GST Registration Guidance for taxpayer wishing to register One Person Company

Goods and Services Tax India

The Goods and Services Tax or better known as GST is a Value added Tax and is a comprehensive indirect tax which is levied on the manufacture, consumption, and sale of goods and services. The Goods and Services Tax in India would replace all the indirect taxes which are levied today on goods and services by the Central and the State governments. GST is intended to be comprehensive for most of the goods and services. Goods and Services Tax is a single indirect tax for the entire nation, which would make India a unified market. It is proposed to be a single tax on supply of goods and services, from a manufacturer to the end consumer. The credit of all the input taxes which are paid at each and every stage would be allowed in the following stages of value addition that makes GST basically a tax on value addition only at every stage. The end consumer would have to bear only the Goods and Service Tax which is charged by the final dealer within the supply chain, together with all the set-off benefits availed at previous stages.

At Taxguru, we provide all the latest GST news to our viewers. Our group of expert keep a close check on all the latest developments and provide a comprehensive analysis on GST updates. We keep updating our portal with articles on GST for the enlightening our readers. Bookmark us for all the GST articles and much more on GST.