The National Financial Reporting Authority (NFRA) has issued its fourth series of guidance on Auditor-Audit Committee Interactions, focusing on the audit of accounting estimates and judgments, specifically concerning the impairment of non-financial assets under Ind AS 36 and SA 540. Driven by the need to improve audit quality and reinforce communication, the document addresses key requirements of the Companies Act, 2013 and SEBI LODR, which mandate the Board and Audit Committee to review accounting estimates. The guidance details the technical requirements for impairment testing, defining concepts like recoverable amount (the higher of fair value less costs of disposal and value in use) and Cash Generating Units (CGUs). It outlines numerous external and internal impairment indicators and specifies the complex steps involved in estimating future cash flows and appropriate discount rates, particularly for assets like goodwill and intangible assets with indefinite useful lives. The document concludes by providing a comprehensive list of potential questions the Audit Committee should pose to the statutory auditors, covering areas such as the evaluation of internal controls, management’s impairment process, reliance on expert opinions, calculation of terminal values and the transparency of disclosures.

National Financial Reporting Authority

NFRA releases Auditor-Audit Committee Interaction Series 4 titled: Audit of Accounting Estimates and Judgments-Impairment of Non-financial Assets

Initiative Strengthens Communication between Auditors and Audit Committees to Enhance Audit Quality; Protects Public Interest and Safeguards Investor Protection

Posted On: 30 SEP 2025

The National Financial Reporting Authority (NFRA) has released the Auditor-Audit Committee Interactions Series 4, titled: Audit of Accounting Estimates and Judgements-Impairment of Non-financial Assets- Ind AS 36, SA 540 etc.

In the course of NFRA’s enforcement, review and monitoring activities, the auditor’s communication with those charged with Governance (TCWG) (including the Audit Committees) has been highlighted. A need has been felt through these activities towards reinforcing the ways and means of communication between the Statutory Auditors and the Audit Committees in particular drawing upon the requirements in the Companies Act 2013 (CA 2013), the two relevant Standards on Auditing (SA 260 (R) and 265), other related SAs and the Standard on Quality Control (SQC).

NFRA has obligations to suggest measures for improvement in overall audit quality and to promote awareness and significance of accounting- auditing standards, auditor’s responsibilities and audit quality. Therefore keeping in view NFRA’s objectives of protecting public interest and investor protection, NFRA continues with its series of Auditor-Audit Committee Interactions, which are being issued on significant areas of accounting and auditing, from time to time.

This Auditor-Audit Committee Interactions Series 4 draws the attention of the auditors to the potential questions the Audit Committees/Board of Directors may ask them in respect of impairment of non-financial assets. Within that, this communication includes aspects pertaining to the audit of impairment of non-financial assets as required by Ind AS 36, Impairment of Assets and SA 540, Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures.

****

National Financial Reporting Authority (NFRA)

Audit Committee* – Auditor Interactions Series 4 Audit of Accounting Estimates and Judgements Impairment of Non-financial Assets- Ind AS 36, SA 540 etc.

*NFRA does not set standards and codes for Corporate Governance, Board of Directors and Audit Committees.

Introduction

1. In course of NFRA’s enforcement, review and monitoring activities, auditor’s communication with Those Charged with Governance (TCWG) (including the Audit Committees) has been variously highlighted. A need has been felt through these activities towards reinforcing the ways and means of communication between the Statutory Auditors and the Audit Committees in particular drawing upon the requirements in the Companies Act 2013 (CA 2013), the two relevant Standards on Auditing (SA 260 (R) and 265), other related SAs and the Standard on Quality Control (SQC 1).

2. Therefore, in accordance with NFRA’s obligations to suggest measures for improvement in overall audit quality and to promote awareness and significance of accounting and auditing standards, auditor’s responsibilities, audit quality, and keeping in view NFRA’s objectives of protecting public interest and investor protection, NFRA has commenced with this series of Auditor-Audit Committee Interactions, which will be issued on significant areas of accounting and auditing, from time to time.

3. The preparation and presentation of financial statements involve judgments and estimates, especially in complex areas including impairment of non-financial assets. This Auditor-Audit Committee Interactions Series 4 draws the attention of the auditors to the potential questions the Audit Committees/Board of Directors may ask them in respect of impairment of non-financial assets as required by Ind AS 36, Impairment of Assets and SA 540, Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures.

4. Impairment is different from depreciation. Depreci-ation1 is systematic allocation of the depreciable amount of an asset over its useful life, where depreciable amount is the cost of an asset, or other amount substituted for cost, less its residual value. Whereas, Impairment loss2 is the amount by which the carrying amount of an asset or a cash-generating unit exceeds its recoverable amount.

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

Companies Act 2013 (CA 2013) and SEBI (LODR) requirements relating to Audit Committee/Board of Directors on review of accounting estimates and judgments

5. As per Section 134 (5) of CA 2013, the Board of Di- rectors (BOD) are required to state in the Directors’ Responsibility Statement in the Board’s Report, which is part of Annual Report, that they had selected such accounting policies and applied them consistently and made judgements and estimates that are reasonable and prudent to give a true and fair view of the state of the affairs of the company.

6. SEBI LODR specifically mandates the Audit Committee to review major accounting entries involving estimates based on the exercise of judgment by management.

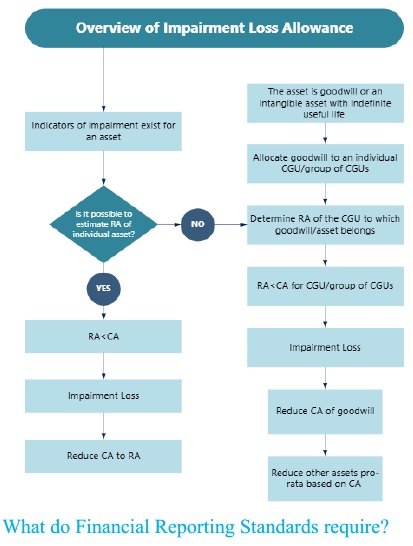

What do Financial Reporting Standards require?

(RA: Recoverable amount, CA: Carrying amount, CGU: Cash generating unit)

7. Preparation and Presentation (including Disclosures) of financial statements requires the Management to make estimates and judgements in the recognition/measurement of assets, liabilities, income and expenses. Such areas could be impairment of non-financial assets, expected credit loss (ECL) for financial assets, provisions for liabilities, recognition/measurement of deferred tax assets and so on. Some of these could be complex requiring special attention by the Preparers, Audit Committees and the Auditors.

8. Schedule III to CA 2013 enumerates various types of assets to be presented in the balance sheet of an entity e.g.,

- Property, plant and equipment (PPE);

- Capital work-in-progress;

- Investment property;

- Goodwill;

- Intangible assets;

- Biological assets;

- Inventories;

- Financial Assets;

√ Investments

√ Trade receivables

√ Loans

These assets are further classified Current vs Non-current based on Ind AS 1.

9. Ind AS 36 applies in accounting for the impair- ment of all assets, except certain specified types of assets3 e.g.,

- inventories,

- assets arising from construction contracts,

- deferred tax assets,

- assets arising from employee benefits,

- or assets classified as held for sale (or included in a disposal group that is classified as held for sale), etc., because separate Indian Accounting Standards dealing with these assets contain guidance for accounting of such assets.

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

10. Ind AS 36 prescribe the procedures that an entity applies to ensure that its assets are carried at no more than their recoverable amount. Para 6 of Ind AS 36 defines recoverable amount as the higher of an asset’s or cash-generating unit’s fair value less costs of disposal and its value in use.

11. Major terms defined in this Standards are –

- A cash-generating unit (CGU) is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets. Refer Para 67 & 68 of Ind AS 36 for guidance to determine CGUs.

- Carrying amount is the amount at which an asset is recognised after deducting any accumulated depreciation (amortisation) and accumulated impairment losses thereon.

- The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs of disposal and its value in use.

- An impairment loss is the amount by which the carrying amount of an asset or a cash-generating unit exceeds its recoverable amount.

12. The Standard describes some indications that an impairment loss may have occurred. If any of those indications is present, an entity is required to make a formal estimate of recoverable amount. Irrespective of whether there is any indication of impairment, an entity shall also (a) test an intangible asset with an indefinite useful life or an intangible asset not yet available for use for impairment annually by comparing its carrying amount with its recoverable amount; and (b) test goodwill acquired in a business combination for impairment annually.

Impairment indicators

External sources of information

(a) there are observable indications that the asset’s value has declined during the period significantly more than would be expected as a result of the passage of time or normal use.

(b) significant changes with an adverse effect on the entity have taken place during the period, or will take place in the near future, in the technological, market, economic or legal environment in which the entity operates or in the market to which an asset is dedicated.

(c) market interest rates or other market rates of return on investments have increased during the period, and those increases are likely to affect the discount rate used in calculating an asset’s value in use and decrease the asset’s recoverable amount materially.

(d) the carrying amount of the net assets of the entity is more than its market capitalisation.

Internal sources of information

(e) evidence is available of obsolescence or physical damage of an asset.

(f) significant changes with an adverse effect on the entity have taken place during the period, or are expected to take place in the near future, in the extent to which, or manner in which, an asset is used or is expected to be used.

(g) evidence is available from internal reporting that indicates that the economic performance of an asset is, or will be, worse than expected.

Dividend from a subsidiary, joint venture or associate

(h) for an investment in a subsidiary, joint venture or associate, the investor recognises a dividend from the investment and evidence is available that:

i) the carrying amount of the investment in the separate financial statements exceeds the carrying amounts in the consolidated financial statements of the investee’s net assets, including associated goodwill; or

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

ii) the dividend exceeds the total comprehensive income of the subsidiary, joint venture or associate in the period the dividend is declared.

Measuring recoverable amount

13. Para 18 of Ind AS 36 defines the recoverable amount of an asset or a cash-generating unit as the higher of its fair value less costs of disposal and its value in use.

- Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

- Value in use is the present value of the future cash flows expected to be derived from an asset or cash-generating unit.

14. It is not always necessary to determine both an as-set’s fair value less costs of disposal and its value in use. If either of these amounts exceeds the as-set’s carrying amount, the asset is not impaired, and it is not necessary to estimate the other amount.

15. Recoverable amount is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. If this is the case, recoverable amount is determined for the cash-generating unit to which the asset belongs unless either: (a) the asset’s fair value less costs of disposal is higher than its carrying amount; or (b) the asset’s value in use can be estimated to be close to its fair value less costs of disposal and fair value less costs of disposal can be measured.

16. An intangible asset with an indefinite useful life is to be tested for impairment annually by comparing its carrying amount with its recoverable amount, irrespective of whether there is any indication that it may be impaired. However, the most recent detailed calculation of such an asset’s recoverable amount made in a preceding period may be used in the impairment test for that asset in the current period, provided all of the prescribed criteria are met.

17. If there is any indication that an asset may be impaired, recoverable amount shall be estimated for the individual asset. If it is not possible to estimate the recoverable amount of the individual asset, an entity shall determine the recoverable amount of the cash-generating unit to which the asset belongs (the asset’s cash-generating unit).

Fair value less cost of disposal

18. A fair value measurement of a non-financial asset takes into account a market participant’s ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use. (paragraphs 27 to 33 of Ind AS 113, Fair Value Measurement).

19. Costs of disposal, other than those that have been recognised as liabilities, are deducted in measuring fair value less costs of disposal. Examples of such costs are legal costs, stamp duty and similar transaction taxes, costs of removing the asset, and direct incremental costs to bring an asset into condition for its sale. However, termination benefits (as defined in Ind AS 19, Employee Benefits) and costs associated with reducing or reorganising a business following the disposal of an asset are not direct incremental costs to dispose of the asset.

Value in Use

20. The following elements shall be reflected in the calculation of an asset’s value in use:

(a) an estimate of the future cash flows the entity expects to derive from the asset;

(b) expectations about possible variations in the amount or timing of those future cash flows;

(c) the time value of money, represented by the current market risk-free rate of interest;

(d) the price for bearing the uncertainty inherent in the asset; and

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

(e) other factors, such as illiquidity, that market participants would reflect in pricing the future cash flows the entity expects to derive from the asset.

21. Estimating the value in use of an asset involves two steps:

(a) estimating the future cash inflows and outflows to be derived from continuing use of the asset and from its ultimate disposal; and

(b) applying the appropriate discount rate to those future cash flows.

22. In measuring value in use an entity shall:

(a) base cash flow projections on reasonable and supportable assumptions that represent management’s best estimate of the range of economic conditions that will exist over the remaining useful life of the asset. Greater weight shall be given to external evidence.

(b) base cash flow projections on the most recent financial budgets/forecasts approved by management but shall exclude any estimated future cash inflows or outflows expected to arise from future restructurings or from improving or enhancing the asset’s performance. Projections based on these budgets/forecasts shall cover a maximum period of five years, unless a longer period can be justified.

(c) estimate cash flow projections beyond the period covered by the most recent budgets/forecasts by extrapolating the projections based on the budgets/forecasts using a steady or declining growth rate for subsequent years, unless an increasing rate can be justified. This growth rate shall not exceed the long-term average growth rate for the products, industries, or country or countries in which the entity operates, or for the market in which the asset is used, unless a higher rate can be justified.

23. Estimates of future cash flows shall include:

(a) projections of cash inflows from the continuing use of the asset;

(b) projections of cash outflows that are necessarily incurred to generate the cash inflows from continuing use of the asset (including cash outflows to prepare the asset for use) and can be directly attributed, or allocated on a reasonable and consistent basis, to the asset; and

(c) net cash flows, if any, to be received (or paid) for the disposal of the asset at the end of its useful life.

24. Future cash flows shall be estimated for the asset in its current condition. Estimates of future cash flows shall not include estimated future cash inflows or outflows that are expected to arise from:

(a) a future restructuring to which an entity is not yet committed; or

(b) improving or enhancing the asset’s performance.

25. Estimates of future cash flows shall not include (a) cash inflows or outflows from financing activities; or (b) income tax receipts or payments.

26. The estimate of net cash flows to be received (or paid) for the disposal of an asset at the end of its useful life shall be the amount that an entity expects to obtain from the disposal of the asset in an arm’s length transaction between knowledgeable, willing parties, after deducting the estimated costs of disposal.

27. The discount rate (rates) shall be a pre-tax rate (rates) that reflect(s) current market assessments of (a) the time value of money; and (b) the risks specific to the asset for which the future cash flow estimates have not been adjusted.

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

Recognising and measuring an impairment loss

28. If the recoverable amount of an asset is less than its carrying amount, the carrying amount of the asset shall be reduced to its recoverable amount. That reduction is an impairment loss.

29. An impairment loss shall be recognised immediately in profit or loss, unless the asset is carried at revalued amount in accordance with another Standard (for example, in accordance with the revaluation model in Ind AS 16, Property, Plant and Equipment). Any impairment loss of a revalued asset shall be treated as a revaluation decrease in accordance with that other Standard.

30. When the amount estimated for an impairment loss is greater than the carrying amount of the asset to which it relates, an entity shall recognise a liability if, and only if, that is required by another Standard.

31. After the recognition of an impairment loss, the depreciation (amortisation) charge for the asset shall be adjusted in future periods to allocate the asset’s revised carrying amount, less its residual value (if any), on a systematic basis over its remaining useful life.

Goodwill

32. For the purpose of impairment testing, goodwill acquired in a business combination shall, from the acquisition date, be allocated to each of the acquirer’s cash-generating units, or groups of cash-generating units, that is expected to benefit from the synergies of the combination, irrespective of whether other assets or liabilities of the acquire are assigned to those units or groups of units. Each unit or group of units to which the goodwill is so allocated shall:

(a) represent the lowest level within the entity at which the goodwill is monitored for internal management purposes; and

(b) not be larger than an operating segment as defined by paragraph 5 of Ind AS 108, Operating Segments, before aggregation.

33. A cash-generating unit to which goodwill has been allocated shall be tested for impairment annually, and whenever there is an indication that the unit may be impaired, by comparing the carrying amount of the unit, including the goodwill, with the recoverable amount of the unit.

34. The impairment loss of a cash generating unit shall be allocated to reduce the carrying amount of the assets of the unit (group of units) in the following order: (a) first, to reduce the carrying amount of any goodwill allocated to the cash-generating unit (group of units); and (b) then, to the other assets of the unit (group of units) pro rata on the basis of the carrying amount of each asset in the unit (group of units).

Reversing an impairment loss

35. An entity shall assess at the end of each reporting period whether there is any indication that an impairment loss recognised in prior periods for an asset other than goodwill may no longer exist or may have decreased. If any such indication exists, the entity shall estimate the recoverable amount of that asset.

36. Indications of a potential decrease in an impairment loss mainly mirror the indications of a potential impairment loss.

37. An impairment loss recognised in prior periods for an asset other than goodwill shall be reversed if, and only if, there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss was recognised. If this is the case, the carrying amount of the asset shall be increased to its recoverable amount. That increase is a reversal of an impairment loss.

38. The increased carrying amount of an asset other than goodwill attributable to a reversal of an impairment loss shall not exceed the carrying amount that would have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior years.

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

39. An impairment loss recognised for goodwill shall not be reversed in a subsequent period.

Disclosure

40. An entity shall disclose the following for each class of assets:

- the amount of impairment losses/reversals of impairment losses recognised in profit or loss during the period and the line item(s) of the statement of profit and loss in which those impairment losses are included.

- the amount of impairment losses/ reversals of impairment losses on revalued assets recognised in other comprehensive income during the period.

41. Similar information is required to be disclosed for each reportable segment.

- the discount rate(s) used in the current measurement and previous measurement if fair value less costs of disposal is measured using a present value technique.

- the discount rate(s) used in the current estimate and previous estimate (if any) of value in use.

42. In some cases, entity is required to disclose the main classes of assets affected by impairment losses/reversals of impairment losses; and the main events and circumstances that led to the recognition of these impairment losses/ reversals of impairment losses.

43. The amount of the unallocated goodwill to be disclosed together with the reasons why that amount remains unallocated.

44. Prescribed information for each cash-generating unit (group of units) for which the carrying amount of goodwill or intangible assets with indefinite useful lives allocated to that unit (group of units) is significant in comparison with the entity’s total carrying amount of goodwill or intangible assets with indefinite useful lives.

What Do Standards on Auditing (SAs) Require?

45. There are several areas that involve accounting estimates and management judgements4. Following key SAs would be of interest to Auditors and Audit Committees.

- SA 5405 which lays down audit requirements of risk assessment procedures and guidance on nature of accounting estimates, indicators of possible management bias and audit work paper documentation. This SA expands on how requirements of SA 3156 and SA 3307 have to be applied in the audit of accounting estimates.

- SA 7018 deals with the auditor’s responsibility to communicate key audit matters (KAM) in the auditor’s report. One of the three items included as a KAM in this standard relates to areas that involved significant management judgement, including accounting estimates that have been identified as having high estimation uncertainty. The auditor is required to report the reason and rationale for considering it as a KAM and how the matter was addressed during the course of the audit.

- SA 2609 Stipulates that auditors communicate with those charged with governance about the qualitative aspects of accounting policies, practices, and estimates, aiding the Audit Committee in its oversight responsibilities.

Potential Questions the Audit Committee May Pose to Auditors

Fundamental areas

46.1 Has the auditor evaluated and tested internal controls over following critical areas?

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

♦ Identification of cash-generating units (CGUs) and the allocation of assets, in particular, good- will.

♦ Identification of indicators of impairment.

♦ Models and data used, and management assumptions made in estimation of forecast cashflows, fair value and value in use.10

♦ Sensitivity testing and scenario analysis.

♦ Management information system over Budget versus Actual performance.

♦ Changes in the above from one period to another.

♦ Use of Management Experts.

♦ Disclosures

Recoverable Amount

46.8 In respect of estimation of value in use and fair value less cost of disposal, has the auditor obtained SAAE to ensure that the management estimates meet the key requirements of the applicable financial reporting framework i.e., Ind AS 36 and Ind AS 113 and the applicable Standards on Auditing?

46.9 How did the auditor evaluate that the models/methods, used by management for fair value and value in use, are appropriate?

46.2 Has the auditor identified impairment of nonfinancial assets as significant risk of material misstatement? If not, why not?

46.3 Has the auditor evaluated whether there is a need for professional(s) with specialised skills or knowledge?11

46.4 How did the auditor evaluate competence, capability and independence of management experts and auditor’s experts employed, if any?

Impairment Indicators

46.5 How did the auditor verify the appropriateness of management’s process of identification of impairment indicators for non-financial assets? Has he obtained sufficient appropriate audit evidence (SAAE) in this regard?

46.6 Did the auditor identify any indicator which was not identified by the management? If so, did the auditor discuss this issue with the management and details thereof?

46.7 In case of entities having Goodwill and Intangible assets with indefinite useful life, whether auditor has ensured annual impairment test by the entity by comparing the carrying value and recoverable amount?

Estimation of future cash flows

46.10 How has the auditor tested the following aspects?

♦ Whether estimation of future cash flows from the assets reflect time value of money, price for bearing the uncertainty in the cash flows and other factors such as illiquidity which the market participants would factor in.12

♦ Whether base cash flow estimations are supported by reasonable and supportable assumptions. Has the auditor tested the reasonableness and reliability of future growth projections, profit margins etc., by evaluating the following:

> Historical trend of actual performance versus budget.

> Entity’s economic and operating environment keeping in mind the evolving trends of competition, customer behavior and regulatory scenario.

> Are the growth rates higher than the market trends justified?

♦ Has the auditor ensured the cash flow estimates exclude the following:

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

> cash inflows and outflows and related cost savings from future business, future restructurings or from improving or enhancing the asset’s performance except those permitted under Ind AS 3613.

> Cash flows from assets and liabilities that are largely independent of the cash inflows from the asset under review (e.g., financial assets such as receivables and recognised liabilities such as payables, pensions or provisions).14

> Cash flows from financial activities and income tax receipts and payments.15

♦ How did the auditor evaluate justification for cash flow projections for more than five years, if any?

♦ Has the auditor tested reasonableness of weight-ages given to internal and external data?

♦ Has the auditor evaluated the period for which the cash flows considered are appropriate ?

Discount rates

46.11 How has auditor evaluated the following?

♦ Estimates of future cash flows and the discount rate reflect consistent assumptions about price increases attributable to general inflation.

♦ Discount rates are pre-tax rates.

♦ Reasonableness of discount rates within the range of discount rates estimates by the management.

♦ Has the auditor challenged the management determined discount rates versus those by the Auditor’s expert, if any.

♦ Approach used does not result into double-counting of assumptions used16.

46.12 How did the auditor evaluate the reliability and accuracy of data and inputs used for estimation of future cash flows, discount rates, growth projections etc.?

46.13 Has the auditor obtained SAAE regarding computation of terminal value and growth rates for that period?

46.14 Did the auditor review sensitivity analysis to identify the impact of changes in key assumptions?

46.15 Has the auditor tested reasonableness of weight-ages given to different scenarios?

46.16 How has the auditor tested the management estimation of fair value and/or value in use to avoid management bias?17

46.17 Did the auditor develop a point estimate or a range to evaluate management’s point esti-mate?18

46.18 Has the auditor challenged reasonableness of value in use estimate if it is higher than the market capitalisation of the entity or the group?19

Fair value

46.19 How has the auditor tested the reasonableness and appropriateness of fair value?

46.20 Has the auditor evaluated whether the management determined fair value truly represents the fair value required under Ind AS 113 i.e. it is not affected by conditions20 like transaction with a related party, transaction under duress or forced sale or the unit of account is different from the unit of account used for fair value measurement?

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

Recognising and measuring impairment loss Cash-generating units (CGUs) and goodwill

46.21 Has the auditor ensured consistency in the identification of CGUs and the related assets, including allocation of corporate assets, from one period to another?21 If there is a change has the auditor checked the rationale and its reasonableness?

46.22 Has the auditor tested whether the basis of carrying amount of CGUs is consistent with the basis of determination of recoverable amount of CGUs?22

46.23 If the entity has goodwill, has the auditor tested its allocation or reallocation when there is reorganisation of entity’s reporting structure, to CGU or group of CGUs in accordance with the criteria laid down in Ind AS 36?23

46.24 If the entity uses calculation made in a preceding period, has the auditor tested its reasonableness and acceptability bearing in mind the conditions stipulated in Ind AS 36?24

Impairment loss recognition and reversal

46.25 Has the auditor checked correctness of order and the basis of allocation of impairment loss to goodwill, if any, and other assets of the CGU?

46.26 How did the auditor evaluate appropriateness of reversal of impairment losses? Has the auditor tested the reasonableness of external and internal sources of information supporting the reversal of impairment loss of assets?

46.27 Has the auditor checked that impairment loss recognised for goodwill is not reversed in subsequent period?25

46.28 Has the auditor checked the correctness of recognition and reversal of impairment loss for an asset carried at revalued amount in accordance with another Ind AS?26

46.29 Has the impairment loss (other than on revalued assets) been properly recognised in the Statement of Profit and loss?

Disclosures and Transparency

46.30 Do the financial statements include adequate disclosures about the assumptions, judgements, and uncertainties related to impairment testing consistent with the requirements of Ind AS 36, Companies Act, and SEBI (LODR)?

Key Audit Matters

46.31 Has the auditor identified impairment of non-financial assets as a key audit matter? If not, why?

46.32 How has the auditor addressed the matter during audit? What were the types of audit tests performed? Has he performed and adequately documented the audit tests performed as described by him/her in the audit report?

Auditor-Audit Committee Interaction Series 4 Audit of Accounting Estimates and Judgments: Impairment of Nonfinancial Assets-Ind AS 36, SA 540 etc.

Acknowledgments

NFRA acknowledges the contributions of subject matter experts Shri R. Anand, Shri D Sundaram, Shri Nawshir Mirza, and Shri P R Ramesh in developing this publication.

Disclaimer: This publication by NFRA Staff is intended purely towards promotion of awareness of auditing and accounting standards and audit quality as part of NFRA’s education, training, seminar and advocacy initiatives. NFRA and the subject matter experts do not accept any responsibility or liability for any loss caused to any person or any entity, howsoever arising from the use of or refraining from the use of the contents of this document. This document is not a policy/standard/recommendation/statement of Executive Body of NFRA, the Authority or the Government and is not issued as a substitute for any obligations of Auditors, Management, TCWG including Audit Committees, as are provided in law, rules, and regulations.

Notes:-

1 As per Para 6 of Ind AS 16

2 As per Para 6 of Ind AS 36

3 Refer Para 2 of Ind AS 36

4 Also refer para A6 and A7 of Standard on Auditing (SA) 540, Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures.

5 Standard on Auditing (SA) 540, Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures.

6 Standard on Auditing (SA) 315, Identifying and Assessing Risk of Material Misstatement Through Understanding the Entity and its Environment.

7 Standard on Auditing (SA) 330, The Auditors’ Responses to Assessed Risks.

8 Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor’s Report.

9 Standard on Auditing (SA) 260, Communication with Those Charged with Governance

10 Para A28 of SA 540

11 Para 14 of SA 540

13 Para 33(b) read with paras 44-47 of Ind AS 36

14 Para 43 of Ind AS 36

15 Para 50 of Ind AS 36

16 Para A15-A21 of Ind AS 36

17 Para A9 of SA 540

18 Para 13(d) of SA 540

19 Para 5.21.4 of Final Decision Settlement Notice for EY and Mr. Richard Wilson, FRC UK.

20 Para B4 of Ind AS 113

12 Para 303 of Ind AS 36