Introduction

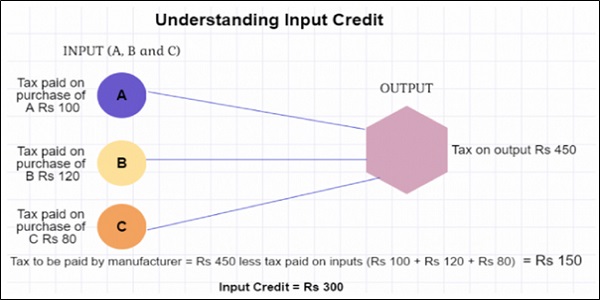

One of the highlights of the GST regime, the Input Tax Credit (ITC) is a fundamental benefit brought forward to prevent the cascading effect of taxation.[1] In simple words, the idea of ITC is to permit companies/businesses to deduct the tax they owe on sales from the tax they pay on business purchases. At the time of the voluntary winding up of businesses or in cases of liquidations as per the Insolvency and Bankruptcy Code of 2016, the business may have some amount of ITC in excess of what is actually availed by the company.[2] This is particularly relevant as the question is whether such an amount of ITC is refundable to the company in question. This is where the thesis statement lies in this analytical essay, addressing both the practical and judicial aspects.

Shama Banu, Sana Ara, Shambhavi S M and Kavitha J, ‘Research on the GST’s Input Tax Credit (ITC)’ (International Journal of Novel Research and Development (IJNRD) 2024) Vol 9 Issue 6 https://www.ijnrd.org/papers/IJNRD2406133.pdf accessed 15 January 2026.[3]

Companies believe that the taxes they have paid through ITC cannot simply vanish and should be claimed by creditors and liquidators as part of the assets qualifying for the liquidation pool. However, the revenue authorities resist such claims by terming the sections of the law too restrictive in allowing such refunds.[4] After the GST was implemented in 2017, this issue remained mostly theoretical for about 7 years and was resolved only at the tax authority level. However, the Sikkim High Court’s recent ruling in “SICPA India Private Limited v. Union of India,”[5] has brought this issue into judicial scrutiny and raised many interpretational questions, necessitating the need to evaluate this issue from a legal standpoint.

Page Contents

- Contemporary Relevance and Practical Implications of the ITC–IBC Interface

- Statutory Framework Governing Refund of Unutilised Input Tax Credit

- Interaction Between the CGST Act and the Insolvency and Bankruptcy Code

- Judicial Interpretation in SICPA India Pvt. Ltd. v. Union of India: Divergent Approaches

- Judicial Precedents on the Primacy of the IBC Over Tax Statutes

- Practical Challenges in Settlement of Input Tax Credit During and After Insolvency

- Comparative Jurisdiction

- Conclusion

Contemporary Relevance and Practical Implications of the ITC–IBC Interface

The issue becomes important in light of the reversal by the Sikkim High Court’ and the general practical anomalies that lie. There lies a clear tussle between the law laid down and the insolvency priorities. ITC refunds can help creditors during recovery under Insolvency. Still, the counter to this lies in the fact that if refunds are given, then this reduces Government revenue and tax intake.[6] This article explores the relationship between insolvency law and GST refund legislation. It will do so by also looking at the judicial approach through various cases. Additionally, there would be a comparison with the international standards on the same issue to understand what could be the best practices that could be implemented within the Indian framework.

Statutory Framework Governing Refund of Unutilised Input Tax Credit

Section 49(6)[7] states that “the proper officer shall refund any balance in the electronic cash ledger and the electronic credit ledger in accordance with the provisions of Section 54.” This language implies a refund mechanism that would apply to any credit ledger amount that isn’t used. On the other hand, Section 54(3)[8] provides that “a registered person may claim refund of unutilised input tax credit at the end of any tax period, only in such cases as may be prescribed and in the manner as may be prescribed by the Board.”

The first proviso to Section 54(3) then specifies that refund shall be allowed “in such manner and subject to such conditions as may be prescribed in the cases mentioned in clauses (i) and (ii) of sub-section (3),” with these clauses being: “(i) zero-rated supplies made without payment of tax; and (ii) the cases where the credit has accumulated on account of the rate of tax on the inputs being higher than the rate of tax on output supplies.”

While Section 54(3) appears to limit refunds to just two situations, Section 49(6) provides a broad clause for repaying any sum that may be left. Whether Section 54(3) restricts the application of Section 49(6) or whether it serves only as an example while Section 49(6) retains a broader scope is open to interpretation.

Interaction Between the CGST Act and the Insolvency and Bankruptcy Code

A liquidator must notify the tax commissioner as soon as they are hired with the intention of winding up a business, according to Section 88 of the CGST Act.[9] The maximum time frame for the tax commissioner to declare a quantity of money that might cover all taxes, penalties, and interest owed by that business is three months. The goal is to safeguard dues during the bankruptcy process. All company directors may be held jointly and severally liable if the business is unable to pay taxes (Section 88(3)) unless they can prove that they were not negligent.[10] Section 88 makes it extremely clear that taxes play a significant role in this insolvency process and that the government must make a first claim on firm assets for any amount owed in taxes.[11] No tax credit refunds are mentioned in this section, nor is it made clear that any money left over from insolvency payments should come before any amount from taxes that are deemed to be required for repayment as a result of insolvency.[12]

When a company is on the verge of bankruptcy, whether through CIRP or liquidation, the insolvency professional’s duties are clear as they get. If the company isn’t already registered for GST, it should be, and output tax payments and returns should be kept up to date.[13] Sales of the assets may occur even if the company goes into liquidation, and the liquidator must be registered for GST in order to engage in such transactions. All of this shows that the company continues to pay taxes and is registered for GST as an entity through the liquidator until the winding-up procedure is completed.[14]

Under the IBC’s Section 53 waterfall mechanism, taxes owed to the government are classified as “operational debts.”[15] Financial creditors have priority over these and are satisfied after them. When it comes to liquidations, the remaining funds would only be transferred to the government’s account once the liquidators settle as per hierarchy. An excess might end up in the company’s liquidation estate and be allocated in accordance with the waterfall’s rules. But according to Section 49(6) of the existing GST system, the remaining amount in the input tax credit account must be returned to the government. Given that the government has no claim to the excess funds that end up in the company’s account, this appears to conflict with the principles outlined in the IBC.[16]

Judicial Interpretation in SICPA India Pvt. Ltd. v. Union of India: Divergent Approaches

In the SICPA case, the petitioner contended that the government should not be allowed to retain the unavailed credit unless specifically authorised by law, and that a refund should be permissible when business ceases operations. The petitioner relied on several judgments [“Shabnam Petrofils Pvt. Ltd. v. Union of India[17]; Union of India v. Slovak India Trading Company Pvt. Ltd.[18] and Eicher Motors Ltd. v. Union of India[19]“] in support of its contention.

The court noted that while Section 49(6) of the CGST Act permits the refund of any balance in the ECrL after the payment of all dues, such refund must comply with Section 54. Section 54(3) restricts the grant of a refund of unutilised ITC to two scenarios: zero-rated supplies or cases of an inverted duty structure. However, there is no express statutory prohibition against refunding the ITC upon business closure.

The court placed reliance on the judgement in case of Slovak India Trading Company Pvt Ltd.[20] Ratio of Slovak was that CENVAT credit cannot be denied only on the ground that business was liquidated. The court drew analogy with this judgement to support its decision.

The SICPA case makes it clear that the judiciary itself has expressed conflicting views on how legislation should be interpreted. The Division Bench believed that the law is strict and interprets it in accordance with the strict rule of interpretation, while the Single Judge believed that the law is ambiguous in favour of the taxpayer and thus rests on the maxim “contra fiscum.”

Ultimately, the opinions of both benches stand for two basic methods of interpreting statutes and constitutions. The fairness of the Single Judge’s approach rules out undue enrichment; therefore, it is unlawful to keep taxes where the laws do not expressly allow for retention. According to the Division Bench’s “fiscal conservatism” approach, a refund would be granted only in accordance with the law; otherwise, there would be no refund at all.[21]

Judicial Precedents on the Primacy of the IBC Over Tax Statutes

The Indian judiciary has made significant contributions in addressing the conflict between GST and IBC.

In the case of STO v. Rainbow Papers Ltd.,[22] it was held that tax authorities are operational creditors, which led to tax authorities’ claims being settled in pursuance of the approved resolution plan, emphasising the overriding effect of the IBC framework.

In the case of Ghanashyam Mishra & Sons (P) Ltd. v. Edelweiss Asset Reconstruction Co. Ltd.[23], the court held that once a resolution plan is approved, all the claims, including those of tax authorities, are to be settled in accordance with the plan. This further fortifies the sanctity of the approved resolution plan and is in furtherance of IBC’s intent of time-bound resolution, since it prevents disputes with tax authorities.

Hence, the discrepancies between GST and IBC are resolved to the extent of liability of the insolvent-assesee towards the department, but the aforesaid Sikkim High Court judgement is a rare ruling that helps decide reconciling ITC claim during or post insolvency.[24]

There are bipolar adjudications in the domain of ITC lapse after CIRP begins. Some judgements establish that ITC cannot be reversed by virtue of insolvency, but some consider it to be affected by peculiarities of the CIRP and IBC claims.[25]

Practical Challenges in Settlement of Input Tax Credit During and After Insolvency

1. Valid Invoices and Receipt of Goods/Services: During the insolvency process, business operations experience a disruption, and records may be lost, making it difficult for the assessee to obtain original invoices. This may affect the ability to claim ITC under Section 16 of the CGST Act.

2. Timely Filing of Returns: The disruption noted above may cause unintended delay in filing returns, which may lead to a penalty or affect the entitlement to credit, further aggravating the financial distress.

3. Reconciliation of Records: All the records and books of accounts must match with each other for the assessee to easily claim ICT. If there is any mismatch in the previous records, for example, owing to a clerical error, the task of claiming ITC would become a herculean task, more so when there is a mismatch in GSTR 2A and 3B, which may lead to a dispute.

4. Resolution Plan Constraints: The Resolution plan may further complicate the extent to which ITC can be claimed. ITC may not be allowed for the debts written off. If the approved resolution plan requires some debts to be written off, the corresponding ITC may be denied.

5. Delay in responding to the Department: During CIRP, it is difficult for the liquidator-represented assessee to respond to notices issued by the Department, which invariably require a response within a short time. This may further cause disputes.

Thus, while mounting challenges in computation, claim and settlement of ITC during or post CIRP exist, these challenges are aggravated by the current regime, which allows ITC only in exceptional circumstances to an already financially burdened assessee. Further, it is also contradictory to the very purpose of rejuvenating the corporate debtor, as also rightfully opined by the Bankruptcy Law Reform Committee.[26]

Circular No. 134/04/2020-GST provides as to how ITC can be claimed with respect to first returns filed; however, it does not provide for claims of ITC accumulated on subsequent returns. This essentially means that the insolvent-assessee would not be eligible for claiming ITC on subsequent returns, which would constitute a major chunk of the ITC that the insolvent-assessee should be entitled to. Hence, while the circular is a partial relief, it is definitely very inadequate. [27]

While that is the position of law, in some foreign countries, a liberal and a pro-insolvent approach is taken to catalyse the resolution process. In the next section, the authors undertake an overview of the law in some foreign countries.[28]

Comparative Jurisdiction

1. Australia: In Australia, the representative of the debtor is entitled to claim the ITC that the debtor himself would have been lawfully entitled to, but for the initiation of the insolvency for a creditable acquisition or import.[29]

2. EU: Through its rulings, the EU has emphasised that only that portion of ITC claimed for goods that would not be used for the economic activity for which they are intended (due to liquidation) will be disallowed. This essentially implies that the tax paid on the acquisition of goods that are already used for economic activities will be eligible as a credit.[30]

3. UK: English law is even more progressive. It allows that after the cancellation of registration with the relevant tax authorities, if any goods are acquired, the tax paid on those acquisitions can be claimed as ITC by filling Form VAT426. This facility is available exclusively for those who are undergoing insolvency. Liquidators, official receivers, or trustees in bankruptcy may use this form.[31]

While Australia and the United Kingdom adopt a more pro-insolvent approach that protects the ITC of the corporate debtor, the model rule underlying the EU emphasises the prevention of undue claims arising from unused inputs. India can take guidance from these models to prepare a regime that strikes a balance in the interests of creditors, liquidators, and the Revenue. Moving to a more flexible threshold and pro-rescue orientation may facilitate smoother insolvency resolutions and prevent the efflux of legitimate ITC in liquidation.

Conclusion

The GST and Insolvency and Bankruptcy Code (IBC)-related issue is complex, and the issue of unutilized Input Tax Credit (ITC) in cases of company insolvency or liquidation is one such issue. The Input Tax Credit, aimed at avoiding the cascading effect of tax, is a substantial asset for companies facing insolvency. The SICPA India Pvt. Ltd vs. Union of India judgment shows the conflict between Sections 49(6) and 54(3) of the CGST Act, where one section allows for a refund of unutilized credit and the other restricts it. Previous judgments such as Shabnam Petrofils, Slovak India Trading Co., and Eicher Motors hold that since it’s not banned, one can claim unutilized credits.

“Practical issues such as reconciliation of records, filing of returns, and limitations under resolution plans” are obstacles in making claims under the Input Tax Credit (ITC). However, Circular No. 134/04/2020-GST gives some respite, though it doesn’t account for the aggregate ITC earned after initial returns. Best practices in countries like Australia, the EU, and the UK show that there are some “more pro-insolvent models that enable liquidators/trustees in insolvency cases to offset claims under ITC.”

Making India’s GST refund system consistent with the principles of IBC while protecting tax revenues will therefore benefit insolvency resolutions, justice, and disputes. It is a realistic and justifiable approach.

Reference

[1] Directorate General of Taxpayer Services, Central Board of Indirect Taxes & Customs, “Input Tax Credit Mechanism” (GST Council, 5 August 2019) https://www.gstcouncil.gov.in/sites/default/files/e-version-gst-flyers/Input%20Tax%20Credit%20Mechanism-050819.pdf accessed 15 January 2026.

[2] The Insolvency and Bankruptcy Code 2016.

[3] Shama Banu, Sana Ara, Shambhavi S M and Kavitha J, ‘Research on the GST’s Input Tax Credit (ITC)’ (International Journal of Novel Research and Development (IJNRD) 2024) Vol 9 Issue 6 https://www.ijnrd.org/papers/IJNRD2406133.pdf accessed 15 January 2026.

[4] Soham Agrawal and Himansh Soni, “Residual Credit Rift: Navigating the ITC Closure Conundrum” The Competition & Commercial Law Review (1 September 2025, updated 4 September 2025) https://www.tcclr.com/post/residual-credit-rift-navigating-the-itc-closure-conundrum accessed 15 January 2026.

[5] SICPA India Pvt. Ltd. v. Union of India 2025 (6) TMI 834

[6] Directorate General of Taxpayer Services, Central Board of Indirect Taxes & Customs, Input Tax Credit Mechanism (Goods and Services Tax Council, 5 August 2019) https://www.gstcouncil.gov.in/sites/default/files/e-version-gst-flyers/Input%20Tax%20Credit%20Mechanism-050819.pdf accessed 15 January 2026.

[7] Central Goods and Services Tax Act 2017, s 49(6).

[8] Central Goods and Services Tax Act 2017, s 54(3).

[9] Central Goods and Services Tax Act 2017 (India), s 88.

[10] Central Goods and Services Tax Act 2017 (India), s 88(3).

[11] Central Goods and Services Tax Act 2017, s 88.

[12] Ms Priya, ‘A Study on Input Tax Credit (ITC) under GST’ (International Journal for Research Trends and Innovation (IJRTI) 2022) Vol 7 Issue 8 https://www.ijrti.org/papers/IJRTI2208146.pdf accessed 15 January 2026.

[13] Dr Mariappan Govindarajan, ‘Liquidator is liable to register under GST laws’ (TaxTMI, 19 July 2019) https://www.taxtmi.com/article/detailed?id=9355 accessed 15 January 2026.

[14] Mani Shanker Lal Dwivedi and Dr Nancy Gupta, ‘A Study of Input Tax Credit and Problem Faced by Taxpayer to Avail Input Tax Credit’ (International Journal of Current Science (IJCSPUB) 2024) Vol 14 Issue 4 https://rjpn.org/ijcspub/papers/IJCSP24D1068.pdf accessed 15 January 2026.

[15] Insolvency and Bankruptcy Code 2016, s 53.

[16] Grant Thornton Bharat LLP, ‘Sikkim HC allows refund of unutilised input tax credit upon closure of business’ (12 June 2025) https://www.grantthornton.in/globalassets/1.-member-firms/india/assets/pdfs/alerts/sikkim_hc_allows_refund_of_unutilised_input_tax_credit_upon_closure_of_business.pdf accessed 15 January 2026.

[17] Shabnam Petrofils Pvt. Ltd v Union of India [2019] GSTPanacea 89 (Guj HC) (R/Special Civil Application No. 16213 of 2018, 17 July 2019).

[18] Union of India v Slovak India Trading Company Pvt Ltd [2006] 201 ELT 559

[19] Eicher Motors Ltd and Another v Union of India and Others [1999] 2 SCC 361 (SC).

[20] Union of India v. Slovak India Trading Co. Pvt. Ltd., 2006 SCC OnLine Kar 854.

[21] Arbind Modi and Ajay Shah, Input Tax Credit and refunds under GST in India: Conceptual and legal framework (Working Paper 44, xKDR Forum 2025) https://ideas.repec.org/p/anf/wpaper/44.html accessed 15 January 2026.

[22] State Tax Officer v Rainbow Papers Ltd [2023] 9 SCC 545 (SC).

[23] Ghanashyam Mishra & Sons (P) Ltd v Edelweiss Asset Reconstruction Co Ltd [2021] 9 SCC 657 (SC).

[24] Sumit K Batra and Manish Khurana, ‘Navigating the GST maze in insolvency: Decoding ITC challenges under IBC’ (2024) 10(5) International Journal of Law 34–39 https://www.lawjournals.org/assets/archives/2024/vol10issue5/10223.pdf accessed 15 January 2026.

[25] Atishay Jain, ‘ITC Conundrum GST Law vs Insolvency & Bankruptcy Code’ (Tranzission, 13 November 2025) https://tranzission.in/itc-conundrum-gst-law-vs-insolvency-bankruptcy-code/ accessed 15 January 2026.

[26] Bankruptcy Law Reforms Committee, Report of the Bankruptcy Law Reforms Committee, Volume I: Rationale and Design (Insolvency and Bankruptcy Board of India, November 2015) https://ibbi.gov.in/BLRCReportVol1_04112015.pdf accessed 15 January 2026.

[27] Circular No 134/04/2020‑GST, CBEC‑20/16/12/2020‑GST: Clarification regarding GST issues for companies under the Insolvency and Bankruptcy Code, 2016 (Government of India, Ministry of Finance, Department of Revenue, Central Board of Indirect Taxes and Customs, 23 March 2020) https://gstcouncil.gov.in/sites/default/files/2024-06/circular-cgst-134h.pdf accessed 15 January 2026.

[28] Anubhav Pandey, ‘Input Tax Credit and Its Role in Preventing Tax Cascading under GST’ (2025) 5 Indian Journal of Integrated Research in Law Volume V Issue III https://ijirl.com/wp-content/uploads/2025/05/INPUT-TAX-CREDIT-AND-ITS-ROLE-IN-PREVENTING-TAX-CASCADING-UNDER-GST.pdf accessed 15 January 2026.

[29] A New Tax System (Goods and Services Tax) Act 1999 (Cth) C2004A00446 ‘latest’ https://www.legislation.gov.au/C2004A00446/latest/text accessed 15 January 2026

[30] UAB ‘Vittamed technologijos’ v Valstybinė mokesčių inspekcija (Case C‑293/21) EU:C:2022:763, Judgment of the Court (Tenth Chamber), 6 October 2022.

[31] HM Revenue & Customs, Insolvency (VAT Notice 700/56) (GOV.UK, 1 April 2014, last updated 23 October 2025) https://www.gov.uk/guidance/insolvency-and-vat-notice-70056#claims accessed 15 January 2026.

Author:-

| Tanmay Mehta Sector 19 Choupasni Housing Board, Jodhpur, (Rajasthan) |

|

| Lakshya Bansal Agrawal Marriage Home, Ganeshi Market, Bayana, Bharatpur (Rajasthan) |

|

| Samarth Parag Gosavi Flat No. B1, Runal Residency, Viveknagar, Akurdi, Pune, 411035 |

|

| Shubh Palvia Silver Oak Green Valley Wanawadi 411040 |

|