Summary: A DRC-01 is a formal notice issued by a GST officer for cases of unpaid or short-paid tax, erroneous refunds, or incorrect use of input tax credit. It is a notice, not a demand order, and is issued under various sections, including Section 73 (non-fraud cases) and Section 74 (fraud cases), which apply until the financial year 2023-24. For the financial year 2024-25 and onwards, a new Section 74A is used for both fraud and non-fraud cases. Upon receiving a DRC-01, a taxpayer must submit a reply in Form DRC-06 within the specified period. If the officer is satisfied with the response, they issue a closure order in DRC-05. However, if the reply is not satisfactory, or if no reply is submitted, the officer proceeds by issuing a demand order in DRC-07. The time limits for issuing a DRC-01 and passing a final order vary depending on the section, with distinct timelines for fraud and non-fraudulent cases.

Notice in DRC-01 us 73, 74, 74A of GST:-

1.Officer can issued notice in number of cases:

- Tax not paid

- Tax short paid

- Erroneously refund

- Input tax credit wrongly availed

- Input tax credit wrongly utilised

2. Full form of DRC:

Full form of DRC is Demand & Recovery Certificate.

3. DRC-01:

A notice will be issued by the GST officer for the above mentioned cases. It is a notice not a demand order.

4. Applicability of Sections:

DRC-01 is issued by the officer u/s Sec 73(1) or 74(1) or 74A(1) and in some other sections for the above mentioned cases.

| S. No. | Nature | Applicability of Section |

| 1 | DRC-01 | Non fraud cases: Section 73(1) |

| 2 | DRC-01 | Fraud cases: Section 74(1) |

| 3 | DRC-01 | Non fraud cases: Section 74A(1) |

| 3 | DRC-01 | Fraud cases: Section 74A(1) |

a. Section 73 & 74 are applicable till FY 23-24. Officer can-not issue notice under these both sections for the FY 24-25 or onwards.

b. Section 74A is applicable from FY 24-25. Officer can issue notice under this section for the FY 24-25 or onwards.

This means that if officer wants to issue a notice for FY 24-25 or onwards then officer will use the Section 74A instead of Sections 73 & 74.

5. DRC-06:

The registered person will submit the reply in Form DRC-06 within the prescribed period by explaining the each & every ground raised by the officer.

a. If registered person is aggrieved by the officer then he will file the reply in DRC-06. There is no requirement to pay the taxes through DRC-03.

b. If registered person is partially aggrieved by the officer then he will file the reply in DRC-06 along with the payment through DRC-03.

6. DRC-05:

a. If officer is satisfied with the reply furnished by the person then he will issue the closure order in Form DRC-05 & no further action will be taken by the officer.

b. If officer is not satisfied with the reply furnished by the person then he will take the further action by issuing a demand order in DRC-07 & he will not pass the closure order in DRC-05.

7. Further actions by the officer:

Further action will be taken by the officer if he is not satisfied with the reply furnished by the registered person in DRC-06 by issuing a demand order in DRC-07.

8. Time limit for issuing of DRC-01:

- Intimation can be issued before issuing of notice in Form DRC-01.

| S No | Sections | Time limit for issuing of notice |

| 1 | U/s 73 | At least 3 months prior to the time limit for issuance of order |

| 2 | U/s 74 | At least 6 months prior to the time limit for issuance of order |

| 3 | U/s 74A | Within 42 months from the due date of annual return |

9. Time limit for passing the order:

| S No | Sections | Time limit for passing the order |

| 1 | U/s 73 | Within 3 years from the due date of annual return |

| 2 | U/s 74 | Within 5 years from the due date of annual return |

| 3 | U/s 74A | Within 12 months from the date of issuance of notice |

10. Example 1:

The officer wants to issue notice for the year 23-24. The due date of annual return was 31-12-2024.

| S No | Sections | Time limit for passing the order | Time limit for issuing of notice |

| 1 | U/s 73 | Order must be passed by 31-12-2027. | The notice must be issued by 30-09-2027. |

| 2 | U/s 74 | Order must be passed by 31-12-2029. | The notice must be issued by 30-06-2029. |

| 3 | U/s 74A | N.A. | N.A. |

** Sec 74A is applicable for the FY 24-25 or onward.

11. Example 2:

The officer wants to issue notice for the year 24-25. The due date of annual return will be 31-12-2025, if not extended.

| S No | Sections | Time limit for passing the order | Time limit for issuing of notice |

| 1 | U/s 73 | N.A. | N.A. |

| 2 | U/s 74 | N.A. | N.A. |

| 3 | U/s 74A | Order must be passed by 30-06-2030. | The notice must be issued by 30-06-2029. |

Note: In case of erroneous refund, the time limit for passing the order will be considered from the date of refund order.

** Sec 73 & 74 will not be applicable for the FY 2024-25.

12. Rule 142:

| S. No. | Form No. | Rule 142 |

| 1 | DRC-01 | Notice is issued u/r 142(1)(A) |

| 2 | DRC-06 | Reply will be filed u/r 142(4) |

| 3 | DRC-05 | Closure order will be passed u/r 142(3) |

| 4 | DRC-07 | Demand order will be passed u/r 142(5) |

13. Officer actions against reply:

| S. No. | Reply | Action by the officer |

| 1 | If officer is satisfied with the reply | He will pass the closure order in DRC-05 |

| 2 | If officer is not satisfied with the reply | He will issue the demand order in DRC-07 |

| 3 | If no reply furnished | He will issue the demand order in DRC-07 |

14. Applicability of sections based on the year:

| S No | Sections | Purpose | Applicability |

| 1 | U/s 73 | Non fraud cases | Till FY 23-24 |

| 2 | U/s 74 | Fraud cases | Till FY 23-24 |

| 3 | U/s 74A | Fraud & non fraud cases | From FY 24-25 |

15. Time petition:

1.A person can file an application of extension of time to submit a reply to the notice.

2. There is no separate form prescribed for this.

3. It will be filed in form DRC-06.

16. Expiry of time:

If the time period for filing a reply to the notice has expired, the reply can still be submitted on the GST portal. In such cases, there is no need to submit it physically at the GST office or send it via email to the concerned GST officer.

17. Note:

a. DRC-01 cannot be issued again for the same grounds for the same financial year.

b. DRC-01 can be issued again for different grounds for the same financial year.

c. DRC-01 can be issued for one year. For different years, separate notice will be issued by department.

–

Acknowledgement of acceptance of payment made voluntarily

23. Refer to the article: ASMT-10 Notice u/s 61 of GST:-

24 .Refer to the article: DRC-01A of GST:-

https://taxguru.in/goods-and-service-tax/gst-drc-01a-intimations-sections-73-74-74a.html

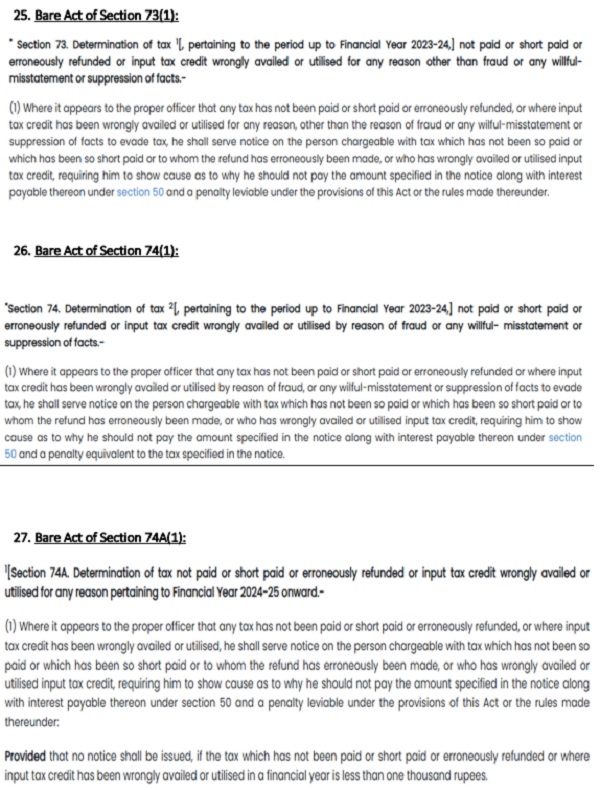

25. Bare Act of Section 73(1):

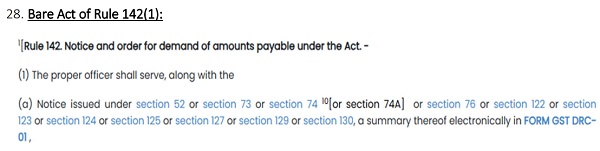

28. Bare Act of Rule 142(1):

Steps against summary order DRC-07:

If the officer issues DRC-07 against the reply furnished by the taxpayer in Form DRC-06, then taxpayer can file an appeal against such order.

*****

If you have any queries, you can reach the author by email at caashishsingla878@gmail.com or by phone at 9896478194.

Disclaimer: The views and opinions expressed in this article are those of the author. This article is intended for general information purposes only and does not constitute professional advice. Readers are strongly advised to consult a qualified professional for guidance specific to their individual situation before making any financial, legal, or tax-related decisions. The author shall not be held liable for any loss or damage of any kind incurred as a result of the use of this information or for any actions taken based on the content of this article.

Author Bio