Introduction:

The Place of Supply (POS) and Location of Supplier are crucial for determining the nature of supply viz. Inter State supply or Intra State supply. GST is destination/ consumption based tax. The Place of Supply provisions determine the place, i.e., Taxable Jurisdiction where tax should reach. The improper determination of place of supply lead to paying IGST instead of SGST & CGST or vice versa.

Provisions dealing with Place of Supply:

Chapter V of IGST Act, 2017– Sections 10 to 13 prescribes the provisions relating to Place of Supply of Goods and Services. There are simply shown in below chart.

Relevant Definitions:

- Continuous Journey- [section-2(3) of IGST Act]

- means a journey for which a single or more than one ticket or invoice is issued at the same time,

- either by a single supplier of service or through an agent acting on behalf of more than one supplier of service,

- and which

- involves no stopover between any of the legs of the journey for which one or more separate tickets or invoices are issued.

Explanation- For the purposes of this clause, the term “stopover” means a place where a passenger can disembark either to transfer to another conveyance or break his journey for a certain period in order to resume it at a later point of time;

- Export of Goods- [section-2(5) of IGST Act]

- with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India

- Export of Services– [section-2(6) of IGST Act]

- means the supply of any service when,––

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange or in Indian Rupees wherever permitted by Reserve Bank of India; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8;

Explanation 1 to Section 8.––For the purposes of this Act, where a person has,––

(i) an establishment in India and any other establishment outside India;

(ii) an establishment in a State or Union territory and any other establishment outside that State or Union territory; or

(iii) an establishment in a State or Union territory and any other establishment being a business vertical registered within that State or Union territory, then such establishments shall be treated as establishments of distinct persons.

- Fixed Establishment- [section-2(7) of IGST Act]

- means a place (other than the registered place of business) which is characterised by a sufficient degree of permanence and suitable structure in terms of human and technical resources to supply services or to receive and use services for its own needs

- Import of Goods- [section-2(10) of IGST Act]

- with its grammatical variations and cognate expressions, means bringing goods into India from a place outside India;

- Import of Services- [section-2(11) of IGST Act]

- means the supply of any service, where––

(i) the supplier of service is located outside India;

(ii) the recipient of service is located in India; and

(iii) the place of supply of service is in India;

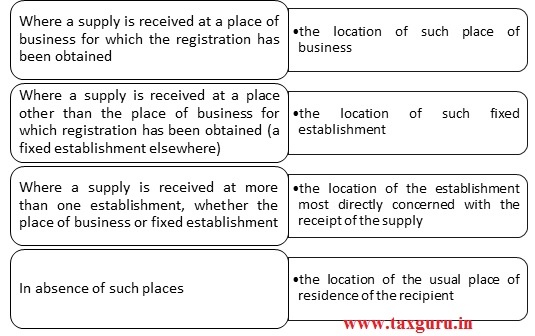

- Location of The Recipient of Services- [section-2(14) of IGST Act]

- Location of the Supplier of Services- [section-2(15) of IGST Act]

Tips to Remember Provisions:

Most of us make special efforts to remember the provisions of Place of Supply (POS). We don’t need to make such efforts, and it is easy to remember with general logic. GST is destination/ consumption based tax. So apply the logic where the supply is consumed/ terminated/ utilised/ made available. For Supply of Services in B2B transactions it will be usually the location of such person (viz. Recipient)

Now, let us understand the provisions in summarized and general manner.

Place of supply of goods other than supply of goods imported into, or exported from India. [section-10]

It deals with Supply of Goods within India i.e., Domestic Transactions.

| Section | Issue | Place of Supply |

| 10(1)(a) | Where the supply involves movement of goods | Location of the goods at the time at which the movement of goods terminates (ends) for delivery to the recipient E.g.: Mr. X of Delhi sends goods to Mr.Y of Karnataka. POS will be where movement terminates (viz. Karnataka) |

| 10(1)(b) | Bill to Ship to Sale-Where the goods are delivered by the supplier to a recipient or any other person on the direction of a third person (agent or on his own) (before or during the movement of goods) | It shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such third person

E.g.: Mr. Y instructs Mr. X to deliver goods to Mr. Z and Mr.X delivers to Mr.Z- it shall be deemed that Mr. Y has received the goods and POS will be place of Mr. Y |

| 10(1)(c) | Where the supply does not involve movement of goods | Location of such goods at the time of the delivery to the recipient E.g.: Mr. A sells fully furnished building in Goa to Mr. B and POS for Furniture will be where furniture is located at time of delivery to Mr. B (viz. Goa) |

| 10(1)(d) | Where the goods are assembled or installed at site | Place of such installation or assembly |

| 10(1)(e) | Where the goods are supplied on board a conveyance, including a vessel, an aircraft, a train or a motor vehicle | Location at which such goods are taken on boardE.g.: Mr. A takes goods on board at Andhra Pradesh on a Delhi-Tamil Nadu Train and sells them in Tamil Nadu. POS will be where goods are taken on Board (viz. Andhra Pradesh) and not the place of sale. |

| 10(2) | Where the place of supply of goods cannot be determined | Shall be determined in such manner as may be prescribed |

Place of supply of goods imported into, or exported from India. [ section-11]

It deals with Supply of Goods involving Cross Border transactions.

| Section | Issue | Place of Supply |

| 11(a) | Goods imported into India | Location of such Importer E.g.: Mr. A of Assam imports goods from Mr. B of China. POS will be location of such importer (viz. Assam) |

| 11(b) | Goods exported from India | Location outside India E.g.: Mr. K of Assam exports goods to Japan. POS will be Japan. |

Place of supply of services where location of supplier and recipient is in India.[section-12]

The provisions of this section shall apply to determine the place of supply of services where the location of supplier of services and the location of the recipient of services is in India. [section-12(1)]

| Section | Issue | Place of Supply | |

| 12(2) | Except for services specified in sub-sections (3) to (14) | Made to a registered person | Location of such registered person |

| Made to any person other than a registered person | The location of the recipient where the address on record exists | ||

| The location of the supplier of services in other cases. | |||

| This is default presumption and apply this sub-section where supply of services does not fall in any of below mentioned cases. | |||

| 12(3) | Supply of Services-(a) directly in relation to an

Any service provided by way of grant of rights to use immovable property or for carrying out or co-ordination of construction work; or |

Location at which the immovable property or boat or vessel, as the case may be, is located or intended to be located | |

| (b) by way of lodging accommodation by a hotel, inn, guest house, home stay, club or campsite, by whatever name called, and including a house boat or any other vessel; or | |||

| (c) by way of accommodation in any immovable property for organising any marriage or reception or matters related thereto, official, social, cultural, religious or business function including services provided in relation to such function at such property; or | |||

| (d) any services ancillary to the services referred to in clauses (a), (b) and (c), | |||

| If the location of the immovable property or boat or vessel is located or intended to be located outside India | Place of supply shall be the location of the recipient | ||

| Where the immovable property or boat or vessel is located in more than one State or Union territory | In proportion to value of services separately collected or determined as per terms of contract or agreement entered into. | ||

| In the absence of such contract or agreement | Service of providing accommodation where such single property is situated other than in 2 or more contagious States or UT or both | Based on no of nights stayed in each such property | |

| Where such property is situated in 2 or more contagious States or UT or both,Services ancillary to above also | Area of immovable property lying in each State/UT | ||

| Services by way of lodging accommodation in house boat or vessel and its ancillary services | Time spent by such boat or vessel in each state or UT based on declaration made by service provider | ||

| 12(4) | Supply of

|

Location where the services are actually performed. | |

| 12(5) | Supply of services in relation to training and performance appraisal | To a Registered Person (RP) | Location of such RP |

| To other than a RP | Location where such services are actually performed | ||

| 12(6) | Supply of services provided by way of admission to a

|

Place where the event is actually held or where the park or such other place is located | |

| 12(7) | Services by way of organisation of a

|

To a Registered Person (RP) | Location of such person |

| To a person other than a RP | Place where the event is actually held | ||

| If the event is held outside India, the place of supply shall be the location of the recipient. | |||

| Where the event is held in more than one State or Union territory and a consolidated amount is charged for supply of services relating to such event | In proportion to the value for services separately collected or determined in terms of the contract or agreement entered into | ||

| In the absence of such agreement | Computed by the application of generally accepted accounting principles | ||

| 12(8) | Supply of services by way of transportation of goods, including by mail or couriers | To a RP | Location of such RP |

| To other than RP | Location at which such goods are handed over for their transportation | ||

| If goods are transported outside India | Destination of such goods | ||

| 12(9) | Supply of passenger transportation service (The return journey shall be treated as a separate journey, even if the right to passage for onward and return journey is issued at the same time.) | To a RP | Location of such RP |

| To other than RP | Place where the passenger embarks on the conveyance for a continuous journey | ||

| Where the right to passage is given for future use and the point of embarkation is not known at the time of issue of right to passage | Determined in accordance with provisions of sub-section (2)

E.g.: Location of Recipient if address available on records or location of Supplier |

||

| 12(10) | Supply of services on board a conveyance, including a vessel, anaircraft, a train or a motor vehicle | Location of the first scheduled point of departure of that conveyance for the journey. E.g.: POS of services on train at Vijayawada in a Delhi-Tamil Nadu going train will be at Delhi | |

| 12(11) | Supply of telecommunication services including data transfer, broadcasting, cable and direct to home television services to any person shall | ||

| (a) In case of services by way of fixed telecommunication line, leased circuits, internet leased circuit, cable or dish antenna | Location where the telecommunication line, leased circuit or cable connection or dish antenna is installed for receipt of services | ||

| (b) in case of mobile connection for telecommunication and internet services provided on post-paid basis | Location of billing address of the recipient of services on the record of the supplier of services | ||

| (c) in cases where mobile connection for telecommunication, internet service and direct to home television services are provided on pre-payment basis through a voucher or any other means | Through a selling agent or a re-seller or a distributor | Address of the selling agent or re-seller or distributor as per the record of the supplier at the time of supply | |

| By any person to the final subscriber | Location where such prepayment is received or such vouchers are sold | ||

| (d) in other cases | Address of the recipient as per the records of the supplier of services | ||

| Where such address is not available, the location of supplier of services | |||

| If the address of the recipient as per the records of the supplier of services is not available | The place of supply shall be location of the supplier of services | ||

| If such pre-paid service is availed or the recharge is made through internet banking or other electronic mode of payment | Location of the recipient of services on the record of the supplier of services | ||

| Where the leased circuit is installed in more than one State or Union territory and a consolidated amount is charged for supply of services | In proportion to the value for services separately collected or determined in terms of the contract or agreement entered into. | ||

| In the absence of such agreement | Based on the number of points lying in each such state or UT | ||

| In case of circuit between 2 points | The starting and ending point will constitute 2 points | ||

| Any intermediate point or place of circuit, benefit of leased circuit is also available at that point | Such point is also considered as a point. | ||

| 12(12) | Supply of banking and other financial services, including stock broking services to any person | Location of the recipient of services on the records of the supplier of services | |

| If the location of recipient of services is not on the records then-location of the supplier of services. | |||

| 12(13) | Supply of insurance services | To a RP | Location of such person |

| To a person other than RP | Location of the recipient of services on the records of the supplier of services | ||

| 12(14) | Supply of advertisement services to the Central Government, a State Government, a statutory body or a local authority meant for the States or Union territories | In proportion to the value of service as per contract or agreement | |

| In the absence of such agreement or contract | Advertisements in Newspapers or Publications | Amount payable for publication in each such state or UT | |

| Printed Material, pamphlets, leaflets, T-shirts etc. | Amount payable for distribution of copies in each state or UT | ||

| Advertisements in Hoardings | Amount payable for hoardings located in each state or UT | ||

| Advertisements on Trains | Amount attributable to ration of length of railway track for that train in each state or UT | ||

| On Utility bills or Gas bills | Bills pertaining to billing address of consumers in each state or UT | ||

| On Railway Tickets | Ratio of Railway tickets in each state or UT | ||

| On Radio Stations | Amount payable to such radio station by virtue of its name | ||

| On television channels | Based on viewership in each state or UT | ||

| In Cinema halls | Amount payable to cinema halls or screens in each state or UT | ||

| On Internet | It is deemed service is provided to all over India. Calculated on basis of internet subscribers in each state or UT | ||

| Through SMS | Based on telecom subscribers in each state or UT | ||

Place of supply of services where location of supplier or location of recipient is outside India. [section-13]

When either of location of supplier or location of recipient is outside India the provisions of this section are attracted. [section-13(1)]

| Section | Issue | Place of Supply | ||

| 13(2) | Except for services specified in sub-sections (3) to (13) | Location of the recipient of services: | ||

| Where the location of the recipient of services is not available | Location of the supplier of services. | |||

| This is default presumption and apply this sub-section where supply of services does not fall in any of below mentioned cases. | ||||

| 13(3) | Services supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services | Location where the services are actually performed | ||

| When such services are provided from a remote location by way of electronic means

(It won’t apply in the case of services supplied in respect of goods which are temporarily imported into India for repairs or any other treatment and are exported after repairs or other treatment without being put to any other use in India, other than that which is required for such repairs or any other treatment) |

Location where goods are situated at the time of supply of services | |||

| Services supplied to an individual, which require the physical presence of the recipient or the person acting on his behalf | Location where the services are actually performed | |||

| 13(4) | Supply of services supplied directly in relation to an·

|

Place where the immovable property is located or intended to be located. | ||

| 13(5) | Supply of services supplied by way of admission to, or organisation of a

|

Place where the event is actually held. | ||

| 13(6) | Any services referred to in sub-section (3) or sub-section (4) or sub-section (5) is supplied at more than one location, including a location in the taxable territory | Location in the taxable territory. | ||

| 13(7) | Where the services referred to in sub-section (3) or sub-section (4) or sub-section (5) are supplied in more than one State or Union territory | As per Agreement or contract basis | ||

| In the absence of such agreement or contract | Services supplied on the same goods | Equally dividing the value in each state or UT where service is performed | ||

| Services supplied on different goods | On the ratio of invoice value of service in each state or UT | |||

| Services supplied to individuals | Applying generally accepted accounting principles | |||

| 13(8) | (a) services supplied by a

(b) intermediary services (c) services consisting of hiring of means of transport, including yachts but excluding air crafts and vessels, up to a period of one month |

location of the supplier of services ( The place of supply for hiring of transport, including yacht beyond one month will be dealt by the provisions of sub-section (3)) | ||

| 13(9) | Supply of services of transportation of goods, other than by way of mail or courier | Place of destination of such goods.( If by mail or courier then will be dealt by provisions of sub-section (3)) | ||

| 13(10) | Supply in respect of passenger transportation services | Place where the passenger embarks on the conveyance for a continuous journey. | ||

| 13(11) | Supply of services provided on board a conveyance during the course of a passenger transport operation, including services intended to be wholly or substantially consumed while on board | First scheduled point of departure of that conveyance for the journey. | ||

| 13(12) | Supply of online information and database access or retrieval services For the purposes of this sub-section, person receiving such services shall be deemed to be located in the taxable territory, if any two of the following non-contradictory conditions are satisfied, namely:

(a) the location of address presented by the recipient of services through internet is in the taxable territory; (b) the credit card or debit card or store value card or charge card or smart card or any other card by which the recipient of services settles payment has been issued in the taxable territory; (c) the billing address of the recipient of services is in the taxable territory; (d) the internet protocol address of the device used by the recipient of services is in the taxable territory; (e) the bank of the recipient of services in which the account used for payment is maintained is in the taxable territory; (f) the country code of the subscriber identity module card used by the recipient of services is of taxable territory; (g) the location of the fixed land line through which the service is received by the recipient is in the taxable territory. |

Location of the recipient of services. | ||

| 13(13) | In order to prevent double taxation or non-taxation of the supply of a service, or for the uniform application of rules | The Government shall have the power to notify any description of services or circumstances in which the place of supply shall be the place of effective use and enjoyment of a service. | ||

Author Bio

Thanks for the very informative posting.

Please clarify the below query:

Suppose a company is having GST registrtaion in one state & incurring hotel accommodation expenses at a different state. Can the company claim Input Credit (CGST & SGST) charged by the hotel?

Excellent work