Case Law Details

Flemingo Dutyfree Shop Private Limited Vs Commissioner of Customs (CESTAT Kolkata)

The appeal challenged an Order-in-Original dated 18.04.2024 confirming a demand of ₹1,36,77,319 along with interest towards Cost Recovery Charges (CRC) for customs supervision services provided between July 2016 and December 2018 at a special bonded warehouse operated at Netaji Subhas Chandra Bose International Airport, Kolkata. The warehouse licence required the licensee to avail customs supervision either on Merchant Over Time (MOT) basis or Cost Recovery Charges (CRC) basis.

The appellant contended that under Regulation 3(e) of the Special Warehouse Licensing Regulations, 2016 and paragraph 11 of CBEC Circular No. 32/2016-Cus dated 13.07.2016, MOT charges are applicable where customs officers are required once a day or once a week, whereas CRC applies only when officers are required for an entire day, the better part of a day because of distance or nature of work, more than once a day, or round-the-clock. The appellant submitted that customs officers were engaged only once a day for not more than two hours and that MOT payments had been regularly accepted for several years without objection. It also argued that no Superintendent of Customs had been specifically deputed and relied on an earlier Goa adjudication order dropping a similar CRC demand.

The Revenue supported the impugned order, arguing that customs officers had rendered services on most working days and that one or two officers were required for a major part of the day, making CRC applicable.

The Tribunal examined Regulation 3(e) and paragraph 11 of Circular No. 32/2016-Cus. It observed that the Circular permits recovery on MOT basis where warehouse operations require customs supervision once a week or once a day. CRC becomes applicable only where the officer remains absent from the customs office for the entire day or the better part of the day, where services are required more than once daily, or where round-the-clock supervision is sought.

After examining the records, the Tribunal found that the customs officers’ services had been utilized only for a limited period of about six hours or part of a day. It noted that there was no evidence showing that the officers worked throughout the day or for the better part of the day. Accordingly, it held that the appellant’s computation and payment of supervision charges on MOT basis were legally correct.

The Tribunal further held that the Revenue had not produced corroborative evidence establishing that customs officers had been engaged for the full day. It also found no evidence that Superintendents of Customs had been specifically posted or that their services had actually been utilized. The Tribunal observed that the show cause notice calculated charges based only on the number of days of supervision and not the actual hours of service, whereas the Circular makes the duration of supervision the relevant factor.

The Tribunal also noted that an identical dispute concerning the appellant’s operations at Dabolim International Airport, Goa, had earlier been decided by the Deputy Commissioner of Customs, who held that CRC could not be demanded in the absence of dedicated customs staff and that MOT charges alone were applicable for services availed on a need basis.

Holding that there was no evidence to justify recovery of supervision charges on CRC basis, the Tribunal concluded that the appellant was liable to pay charges only on Merchant Over Time basis. It therefore set aside the impugned order and allowed the appeal.

FULL TEXT OF THE CESTAT KOLKATA ORDER

The present appeal has been filed against the Order-in-Original No. KOL/CUS/A&A/ Pr. COMMISSIONER/ADJN/15/2024 dated 18.04.2024 passed by the Principal Commissioner of Customs (Airport & ACC), Custom House, 15/1, Strand Road, Kolkata – 700 001, West Bengal.

2. The facts of the case are that the M/s. Flemingo Dutyfree Shop Private Limited (hereinafter referred to as the “appellant”) is a private limited company incorporated under the provisions of the Indian Companies Act, 1956 and an existing company under the Companies Act, 2013, having its registered office at D-73/1, TTC Industrial Area, MIDC, Turbe, Navi Mumbai 400 703 and, inter alia, engaged in the business of running duty free shops at several airports and seaports in India.

3. By and under a Special License No.89/2016 dated 14.07.2016 issued by the Commissioner of Customs (Port), Kolkata, under section 58A(1) of the Customs Act, 1962 (“Customs Act”), the appellant was permitted to operate a special bonded warehouse at Netaji Subhas Chandra Bose International Airport (“NSCBI Airport”), Integrated Terminal Building, Kolkata, West Bengal, for storage of imported liquor, tobacco, perfumes, cosmetics, camera, watches, transistors, household items, food and confectionaries, accessories and such other items. As per condition 14 of the License, “The licensee shall take the services of Custom Officer either on Cost Recovery basis or MOT fees basis.”

4. As part of its normal business operations, the appellant is required to remove its products from its special bonded warehouse and bring them to its duty-free shops for sale. Being an operator of a special bonded warehouse, the appellant is required to comply with Regulation 3(e) of the Special Warehouse Licensing Regulations, 2016 (“Warehousing Regulations”), which requires a licensee to pay for the services of supervision of the warehouse by the customs officer and the services of supervision availed by the appellant are required to be paid in compliance with paragraph 11 of Circular No.32/2016-Cus dated 13.07.2016 issued by the Central Board of Excise and Customs (“CBEC”) (“Circular”) either on Merchant Over Time (“MOT”) basis or Cost Recovery Charges (“CRC”), as applicable.

5. Regulation 3 of the Warehousing Regulation and Paragraph 11 of the Circular states that where the licensee warrants operation of the warehouse once a week, or in cases, where the services of the customs officer is required once a day, an operator/licensee of a special bonded warehouse is required to pay costs of supervision on MOT basis. CRC is payable only in certain circumstances when the services of the customs officer is required for an entire day or for better part thereof.

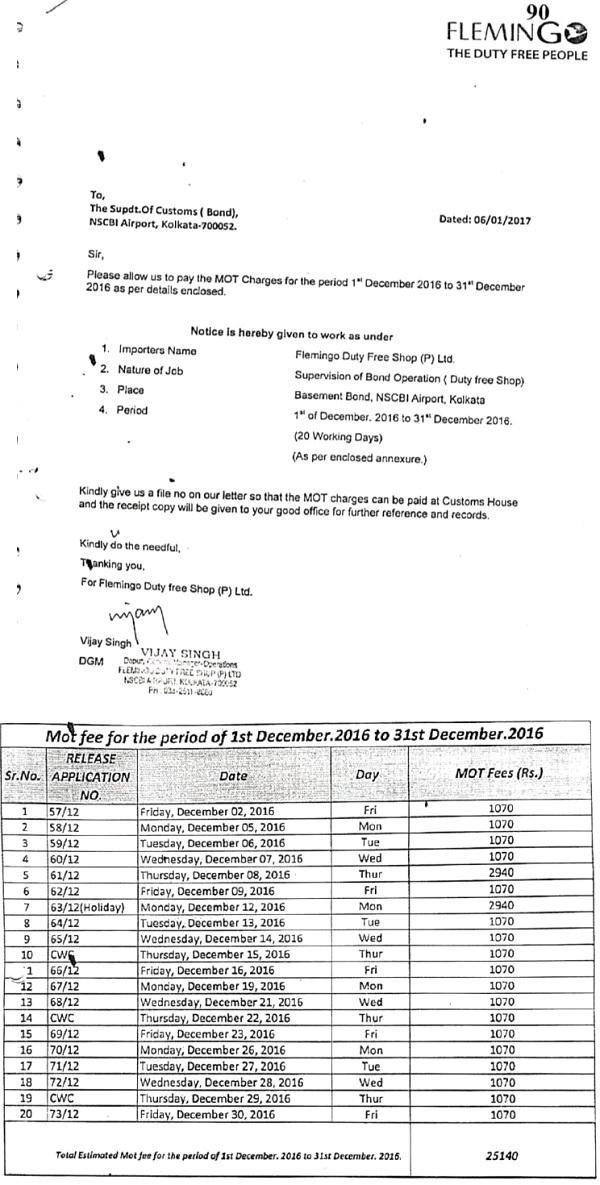

6. In compliance of Regulation 3(e) of the Warehousing Regulations read with Paragraph 11 of the Circular, the appellant made payment to the Superintendent of Customs (Bond), NSCBI Airport, for the services rendered by the Preventive Officer once per day for a period not exceeding two hours, on MOT basis for the period starting from July 2016 and ending on December 2018.

7. The appellant was issued a Show Cause Notice bearing No. F.No.S32(Audit)-38/2018 AP(Bond)/4178 dated 14.02.2019, demanding an amount of Rs.1,36,77,319/-, being the differential amount of Cost Recovery Charges (CRC) allegedly recoverable under Regulation 3(e) of the Warehousing Regulations read with Paragraph 11 of the said Circular for the period from July, 2016 to December, 2018, along with interest thereon.

7.1. The above said Notice was adjudicated and decided by the Ld. Principal Commissioner of Customs, Airport & Air Cargo Complex Commissionerate, Custom House, Kolkata, vide his Order-in-Original No. KOL/CUS/A&A/ Pr.COMMISSIONER/ADJN/15/2024 dated 18.04.2024 (hereinafter referred to as the “impugned order”) wherein the demand for recovery of Rs.1,36,77,319/-, along with applicable interest, in terms of Regulation 3(e) of the Special Warehouse Licensing Regulations, 2016 read with Paragraph 11 of the C.B.E.C. Circular No. 32/2016-Cus dated 13.07.2016 for the period from July, 2016 to December, 2018 has been confirmed.

7.2. Aggrieved by the impugned order, the appellant has filed the present appeal.

8. The Ld. Counsel appearing on behalf of the appellant submitted that the Ld. Principal Commissioner has failed to act in terms of Regulation 3(e) of the said Regulations read with Paragraph 11 of the Circular. It is submitted that as per Regulation 3 of the Regulations read with Paragraph 11 of the Circular, where the services of the Customs Officer is required once a day or once a week, the operator/licensee of the special bonded warehouse is required to pay costs of supervision on MOT basis; that recovery of costs on CRC basis is required only in certain circumstances when the services of the customs officer is required for an entire day or for better part thereof.

8.1. It is submitted that in the present case, the services of the Customs Officer were availed only once a day and that too for a period not exceeding 2 hours and as such, the recovery of costs on CRC basis is per se arbitrary, illegal and contrary to the provisions of Regulation 3 of the Warehousing Regulation read with Paragraph 11 of the Circular. Accordingly, the appellant contends that the impugned order is contrary both on law and facts.

8.2. He further submitted that the appellant had begun its operations at the NSCBI Airport since the year 2007 and pursuant to operationalization of the new terminal at NSCBI Airport, the appellant has been operating its warehouse located in the basement of the integrated Terminal Building of NSCBI Airport since the year 2014. It has also been submitted that even before operationalization of new terminal at NSCBI Airport i.e. in the year 2014, since the year 2010, the appellant has been making payment to the Superintendent of Customs (Bond), NSCBI Airport, on MOT basis for recovery of costs towards the services rendered by the Preventive Officer; these payments have been accepted by the Superintendent of Customs (Bond), NSCBI Airport, without any protest or demur. It is also mentioned that since the year 2010 and till date, there has been no change in the operations carried out by the appellant at NSCBI Airport; that as such, the sudden departure on the part of the Respondent qua recovery of costs towards the services rendered by the Preventive Officer on CRC basis instead of MOT basis, without any reason and justification, is brazen, arbitrary and a pure afterthought.

8.3. Without prejudice to the above, the Ld. Counsel for the appellant also inter alia made the following submissions: –

i. That vide the Show Cause Notice, the impugned Demand for recovery of costs towards the services rendered by the Preventive Officer on CRC basis has been raised only for the starting from July 2016 and ending in December 2018, though the appellant has been making payment of recovery of costs on MOT basis, as the Respondent is aware that the any demand for the period prior to the period starting from July 2016 and ending in December 2018 would be barred by the law of limitation. As such, it is clear that the impugned action on the part of the respondent in seeking the payment of recovery of costs on CRC basis qua the services rendered by the Preventive Officer is a pure afterthought to illegally and unjustly enrich itself at the cost of the appellant.

ii. That though the appellant in its Application for Renewal of Private Bonded Warehouse dated 04.06.2016 (“Renewal Application”) has averred that the distance of the warehouse of the Appellant from the Customs House is 30 kms approximately, the same is not a yardstick to apply to the present case for seeking payment of the impugned Demand on CRC basis, as the Customs House is only an administrative office of the Customs Authorities. No Customs Officers are deputed from the Customs House which is located at a distance of 30 kms approximately from the warehouse of the Appellant located at the basement of the integrated Terminal Building of NSCBI Airport. The Preventive Officer is deputed from the station at the upper ground floor of the integrated Terminal Building of NSCBI Airport. As such, the reliance of the Principal Commissioner of Customs upon the Renewal Application of the appellant is completely misplaced and a red herring.

iii. That the interpretation of Regulation 3(e) of the Warehousing Regulations by the Principal Commissioner of Customs is erroneous and perverse. Regulation 3(e) of the Warehousing Regulations does not require the Appellant to book the customs officer for a dedicated timeslot. As such, the Principal Commissioner of Customs is reading into the provisions of the Warehousing Regulations, which conduct on the part of the Principal Commissioner of Customs is contrary to the law and mandate of the Customs Act and the Rules and Regulation framed thereunder.

iv. That the purported finding of the Principal Commissioner of Customs “… Preventive Officer works under the direct supervision of the Superintendent of Customs, whose supervisory role was mandatory for performing various functions in the warehousing operation conducted through the Bond Section in the Airport Commissionerate” is simply devoid of logic. In the present case, no Superintendent of Customs was deputed/allotted by the Customs Authorities. As such, the impugned Demand qua recovery of costs on CRC basis towards Superintendent of Customs is not maintainable and ought to be set aside. The role of supervision by the Superintendent of Customs as sought to be established by the Principal Commissioner of Customs by way of the impugned Order is a general role of supervision performed by the Superintendent of Customs as part of its duties under the Customs Act and the Rules and Regulations framed thereunder. The role of supervision by the Superintendent of Customs as sought to be established by the Principal Commissioner of Customs by way of the impugned Order is not specific to the operations of the appellant at NSCBI I Airport. Airport.

8.4. Further, the Ld. Counsel for the appellant refers to the Order-in-Original No.05/2020-21- DC(CUS)/ADJ dated 27.02.2021 passed by the Deputy Commissioner of Customs, Goa, in the matter of the appellant with respect to its operations at Dabolim International Airport, Goa, wherein a similar demand for recovery of costs on CRC basis made was dropped. On this score, he argues that the principles of judicial propriety and judicial discipline warranted the Principal Commissioner of Customs to drop the impugned Demand in view of the Order-in-Original No.05/2020-21-DC(CUS)/ADJ dated 27.02.2021 passed by the Deputy Commissioner of Customs, Goa; the Principal Commissioner of Customs ought to have promoted and adhered to the principles of judicial propriety and judicial discipline.

8.5. In view of the above submissions, the Ld. Counsel for the appellant prayed that the impugned order be set aside by allowing the present appeal.

9. On the other hand, the Ld. Authorized Representative of the Revenue has reiterated the findings of the lower authority in the impugned order. Accordingly, he justified the impugned demand and prayed for rejection of the appeal.

10. Heard both sides and perused the documents presented before us.

11. We observe that in the present case, the appellant had been granted a Special Warehouse Licence by the Commissioner of Customs (Port), Kolkata vide Special License No.89/2016 dated 14.07.2016 under section 58A(1) of the Customs Act, 1962, to operate a special bonded warehouse at Netaji Subhas Chandra Bose International Airport (“NSCBI Airport”), Integrated Terminal Building, Kolkata, West Bengal, for storage of imported liquor, tobacco, perfumes, cosmetics, camera, watches, transistors, household items, food and confectionaries, accessories and various other items. As per condition 14 of the License, “The licensee shall take the services of Custom Officer either on Cost Recovery basis or MOT fees basis.”

12. Regulation 3(e) of the Special Warehouse Licensing Regulations, 2016 (“Warehousing Regulations”) requires a licensee to pay for the services of supervision of the warehouse by the officers of customs on recovery of costs, in compliance with paragraph 11 of Circular No.32/2016-Cus dated 13.07.2016 issued by the Central Board of Excise and Customs. For ease of reference, paragraph 11 of the C.B.E.C. Circular No. 32/2016-Cus. dated 13.07.2016 is reproduced below: –

“11. Recovery of costs:

Clause (e) of Regulation 3 of the Special Warehouse Regulations 2016 and circular no. 20/2016 Customs dated 20th May 2016 provide that the Licensee of a special warehouse shall undertake to bear costs of customs supervision on Merchant Over Time basis or on Cost Recovery. Now, the Board has approved the following guidelines:

a. The Licensee shall have to indicate the frequency with which the warehouse has to be operated per day / per week and the expected business hours of such operation.

b. The Principal Commissioner / Commissioner shall evaluate the projected requirement and the distance of the warehouse from the customs office to determine which of the modes of recovery of costs needs to be applied.

c. Illustratively, if the requirement of the licensee warrants the operation of the warehouse on a frequency which is, say, once in a week, the cost of supervision shall be charged on Merchant Over Time basis. Or, in cases, where the services of the Customs officer are required once a day, cost of supervision could also be based upon Merchant Over Time. However, if the warehouse is at such distance from the nearest customs office or the nature and duration of work is such that, the visit of the bond officer on every day basis, means his absence from his office for an entire day or better part thereof, the licensee shall have to undertake the services on cost recovery basis. Further, in cases where the licensee requires services of a customs officer for more than once in a day, he shall have to undertake supervision on cost recovery basis. Similarly, in case where round the clock services are requested, the licensee will have to bear charges on cost recovery basis for a suitable number of officers. Basically, this issue has to be examined on the above lines for deciding the recovery of costs from the licensee.”

12.1. From a perusal of the above Circular, it is clear that if the requirement of the licensee warrants the operation of the warehouse on a frequency which is once a week, then the supervision charges shall be payable on “Merchant Over Time” (MOT) basis. The supervision charges are required to be paid on Cost Recovery Charges (CRC) basis are required only in the following three situations:

i. where the warehouse is at a distance or nature of the work is such that the customs officer is required to be absent from his office for an entire day or for better part thereof, or

ii. where the services are required twice a day; or

iii. where the services are requested for the entire day.

13. In the present case, from the records, it is evident that the appellant have utilized the services of the officers only for six hours or part of a day. We find that the appellant themselves worked out the MOT charges payable by them for the services utilized. For ready reference, the charges worked out by the appellant for the period from 01st December, 2016 to 31st December, 2016, as submitted by the appellant vide its letter dated 06.01.2017 to the Superintendent of Customs (Bond), NSCBI Airport, Kolkata, is extracted below: –

14. It can be seen from the above that the officer’s services have been availed only for a limited period, of say six hours in a day, as submitted. There is no evidence available on record to indicate that the officer’s services have been utilized throughout the day. Thus, we hold that the determination of payment for the services as worked out by the appellant on MOT basis, for the period under dispute, is legally correct.

15. We have also taken note of the specific submission made by the Ld. Authorized Representative of the Revenue by referring the letter issued by the Deputy Commissioner of Customs, Import Bond Section, Custom House, Kolkata under F.No.S-41-216/07 IB (Pt.) dated 18.10.2016 addressed to M/s Flemingo DFS Pvt. Ltd. wherein M/s Flemingo DFS Pvt. Ltd. was specifically directed to comply with the procedure regarding Duty Free Shops contained in CBEC Circular No.32/2016 dated 13.07.2016. He drew our attention to the Details of the services rendered by Customs and MOT paid by Flemingo for the period from July 2016 (the month in which the said license was issued) to December 2018 (as available in pages 2 and 3 of the Show Cause Notice) to contend that the said table clearly indicates that M/s. Flemingo DFS Pvt. Ltd. has availed the services rendered by Customs for 558 (95%) days out of approximate 586 working days of the said period. Regarding duration of services provided by the Customs officers, it has been contended by the Revenue that one or two Customs officers are required for a major part of the day on a daily basis, which fact could be corroborated from the MOT calculation done by M/s Flemingo DFS Pvt. Ltd. By virtue of the above submissions, the Ld. Authorized Representative of the Revenue contended that the services rendered by the customs officers are chargeable on the basis of Cost Recovery in this case.

15.1. It is observed that in the case on hand, the claim of the Revenue is that the officers were posted from Customs House to attend the work relating to the Warehouse located in the Airport. However, we find that there is no evidence available on record to show that the said officers have actually worked for more than six hours. In the absence of any substantive evidence, it cannot be concluded that the services of the customs officers have been utilized for the full day. Therefore, the above contention of the Ld. Authorized Representative of the Revenue is devoid of merit.

16. From the details of the impugned demand, it is observed that the same has been raised in respect of services rendered by Superintendents of customs also. However, there is no evidence available on record to show that Superintendents of customs have been posted or that services of Superintendents have been utilized by the appellant.

17. It is relevant to note the said Circular requires the Principal Commissioner of Customs to determine the charges of the Officer of the Customs to be paid either on Cost Recovery Charges basis or Merchant Over Time basis, subject to the indication by the licensee, with respect to the business hours and frequency of operation of the warehouse. However, in the present case, despite, the fact that the appellant has availed the services of the Preventive Officer of the Customs for less than the better half of the day, it has been compelled to pay charges of the Preventive Officer for 8 hours payment slab, i.e. 10:00 a.m. to 06:00 p.m., as provided under the Customs (Fees for Rendering Services by the Customs Officer) Regulations, 1998, since there is no payment slab for less than 8 hours in a day.

17.1. The alleged calculation and/or computation, pertaining to the cost of supervision, as provided in the Show Cause Notice is not sustainable particularly in view of the fact that the computation provided under the Notice only enumerates the number of days spent for supervision by the Officers of the Customs and not the actual hours for which the services of the officers have been availed. On a bare perusal of the Circular, it can be seen that, while determining the cost of supervision, the hours spent by the Officer of the Customs in supervising the warehouse is the determinative factor and not the number of days spent by the Officer of Customs.

18. In fact, the appellant has specifically contended that it has been wrongly stated in the Show Cause Notice that the services rendered by customs for Flemingo was 558 days (95%) out of the 586 working days. Although the above is not material for the purpose of determining the cost of supervision, it has been stated by the appellant that the International Airports are 24*7 custom airport and the working hours of the customs officers stationed at these Airports are also 24*7, which makes it evident that the total number of working days from July, 2016 till November, 2018, were 883 days and the appellant have utilized the services of the officers only for 63% of the total period.

19. In view of the above, we find that there is no corroborative evidence on record to establish that the services of the officers of customs have been used for the entire day or for the better part thereof, as alleged by the Revenue, and therefore, in terms of Circular No.32/2016-Cus dated 13.07.2016, we hold that the appellant is liable to pay service charges for the services utilized by them only on Merchant Over Time (MOT) basis. Thus, the demand confirmed in the impugned order by demanding service charges as per Cost Recovery Charges (CRC) basis is not sustainable in the eyes of law.

20. We also take note of the fact that an identical matter, pertaining to the appellant’s operations at Dabolim International Airport, Goa, has already been decided by the Ld. Deputy Commissioner of Customs, Custom House, Marmagoa, Goa vide Order-in-Original No.05/2020-21-DC(CUS)/ADJ dated 27.02.2021, wherein a similar demand for recovery of costs on CRC basis made was dropped. The relevant observations as recorded by the Ld. Deputy Commissioner of Customs in the above Order-in-Original are reproduced below: –

“11. In terms of Board Circular No. 68/95 dated 15.06.1995 Private Bonded Warehouse operators are required to pay cost recovery charges if the services are required on continuous basis (09 AM to 06 PM or MOT/Supervisory charges as the case may be. On a bare perusal of the Board Circular, it is clear that cost recovery charges are to be recovered if the private bonded warehouse operator agrees to take the service on continuous basis and the officers are in fact posted for exclusive supervision.

Subsequent to implementation of Special Warehousing Regulations 2016, Circular 20/2016 has clarified that DFS being point of sale cannot be treated as warehouse and hence need not be licensed. Circular 32/2016 para 11 while dealing with recovery of costs for Special Warehousing Licensees spells out terms as to how to determine whether cost recovery charges or MOT are applicable.

12. I find that in SCN para 5 it has been brought out that the keys of the warehouse/shop is deposited with the Customs officer (SDO) and officer of the rank of Superintendent is permanently posted to supervise the functions of the DFS/warehouse.

However, M/s Flemingo Duty Free Shop Pvt. Ltd., in submissions dated 03/10/2019 and 25/08/2020 have claimed that no Customs officer was permanently posted and they have availed the services of the Customs officer on need basis to escort the bonded goods from warehouse to DFS

In this regard relied upon document no. 6 as mentioned in SCN at para 26, i.e. posting order of the officers was perused. It is evident from the said posting order that the officer posted in the Airport Baggage section was also given the charge of M/s Flemingo Duty Free Shop/warehouse. From this I come to a conclusion that exclusive officer to supervise only DFS/warehouse was not posted. When the exclusive officer is not posted, imposing cost recovery charges is not a judicious decision in terms of Circular 68/95 and Circular 32/2016.

14. However, I find that M/s Flemingo Duty Free Shop Pvt. Ltd has availed the services of the Customs officers for its warehouse functions and escorting the bonded goods from warehouse to Duty Free Shop on need basis. Hence MOT charges as applicable have to be paid. This is also in consonance with the Hon’ble High Court order dated 16/01/2012 pertaining to Writ Petition 467/2011.

15. Circular 20/2016 clearly acknowledges the fact that the DFS operators store goods in warehouses in and around the precinct of the airport which qualify to be licensed as bonded warehouses as they are capable of being under the lock of customs. Further clarification regarding recovery of costs through MOT or Cost recovery basis has been brought out in paragraph 11 of the Circular 32/2016

Reading both the circulars together I find that though it has been acknowledged that the warehouses are in or around precinct of airport, nowhere it exempts the licensee from payment towards MOT or cost recovery charges when warehouse is situated in the precinct of the airport which is in fact Customs station notified under Section 7 of the Customs Act, 1962.

16. Circulars issued by the Board are binding in law on the authorities under the respective statutes. Hence I find that though it is seen from the evidences produced that there is no basis for demand of cost recovery charges, MOT as prescribed under Customs (Fees for rendering services by Customs Officers) Regulations 1998, is clearly applicable.

17. Once I find that MOT is admissible in this case, amount of Rs. 2,95,460/- (Rupees Two Lakhs Ninety Five Thousand Four Hundred Sixty only) with interest accrued deposited by M/s Flemingo Duty Free Shop Pvt. Ltd. to the High Court Registry needs to be appropriated in terms Hon’ble High Court’s permission dated 03/03/2020.

18. Therefore, in the facts and circumstances of the instant case, demand of Cost Recovery Charges without posting a dedicated staff/officer as per the license condition is not sustainable. However, the payment of MOT charges being done by M/s Flemingo Duty Free Shop Pvt. Ltd. for costs of Customs Supervision in respect to the Special Warehouse is in accordance to Circular 68/95, Special Warehouse Regulations 2016 and Circular No. 32/2016 Customs dated 13th July, 2016 issued in F. No: 473/05/2015- LC 11 by Govt. of India, Ministry of Finance, Dept. of Revenue, Central Board of Excise and Customs.”

21. In view of the discussions hereinabove, we hold that the demand confirmed vide the impugned order is liable to be set aside.

22. In the result, the impugned order is set aside and the appeal filed by the appellant is allowed.

(Order pronounced in the open court on 24.06.2026)

Author Bio