Accurate classification of materials and inventory is central to transparent financial reporting, particularly under the revised reporting structure mandated by the Companies Act, 2013. This article explores the practical treatment and regulatory backing for items such as cost of material consumed, stock-in-trade, and changes in inventory—essential components in the preparation of financial statements for manufacturing and trading entities.

1. Practical Explanation

Cost of Material Consumed (For Manufacturing Units)

This refers to the cost of raw materials used in the manufacturing process.

Applicable Material: Only Raw Material

Formula:

Opening Stock of Raw Material

+ Purchases of Raw Material

– Closing Stock of Raw Material

= Cost of Material Consumed

Purchase of Stock-in-Trade (For Trading or Hybrid Units)

This includes goods bought specifically for resale, without any manufacturing or processing.

– Applies mostly to Trading Units.

– May also appear in manufacturing units for goods sold without processing.

– Only the purchase amount is recorded (no opening or closing stock adjustments).

Changes in Inventories

Represents the net change in inventory levels across different stock types.

– Work-in-Progress (WIP)

– Finished Goods

– Stock-in-Trade

Formula:

(Opening Stock of WIP + Finished Goods + Stock-in-Trade)

– (Closing Stock of WIP + Finished Goods + Stock-in-Trade)

= Change in Inventories

Special Note on Trading Units

– Cost of Material Consumed: Not applicable (usually NIL).

– Purchase of Stock-in-Trade: Captures the value of goods purchased for resale.

– Change in Inventory: Opening Stock of Stock-in-Trade – Closing Stock of Stock-in-Trade

2. Regulatory and Accounting Standards Alignment

The treatment and terminology used in this article are consistent with the requirements of the Institute of Chartered Accountants of India (ICAI) and applicable accounting standards.

Revised Schedule III (Companies Act, 2013)

Under the Revised Schedule III to the Companies Act, 2013, the Profit & Loss Statement must separately disclose:

– Cost of Material Consumed

– Purchase of Stock-in-Trade

– Changes in Inventories of Finished Goods, Work-in-Progress, and Stock-in-Trade

These line items are standard across:

– Division I: For companies following Accounting Standards (AS)

– Division II: For companies complying with Indian Accounting Standards (Ind AS)

– Division III: For NBFCs under Ind AS

Accounting Standards (AS/Ind AS)

Relevant accounting standards such as AS 2 / Ind AS 2 (Valuation of Inventories) provide guidance on the classification and measurement of inventory:

– Inventories must be valued at the lower of cost and net realizable value (NRV)

– Disclosure of inventory types (raw materials, WIP, finished goods) is required

– Costs incurred in bringing inventory to its present condition must be recognized

3. Real-Life Illustration

| Stock Summary | |

| Particular | Amount (₹) |

| Opening Raw Material Stock | 1,953.05 |

| Purchases of Raw Material | 30,774.01 |

| Closing Raw Material Stock | 2,349.31 |

| Direct Labour & Overhead | 13,000.00 |

| Opening WIP | 115.58 |

| Closing WIP | 75.02 |

| Opening Finished Goods | 1,357.90 |

| Closing Finished Goods | 936.08 |

| Purchases of Stock-in-Trade (readymade fans) | 477.84 |

| Opening Stock-in-Trade5 | – |

| Closing Stock-in-Trade | – |

–

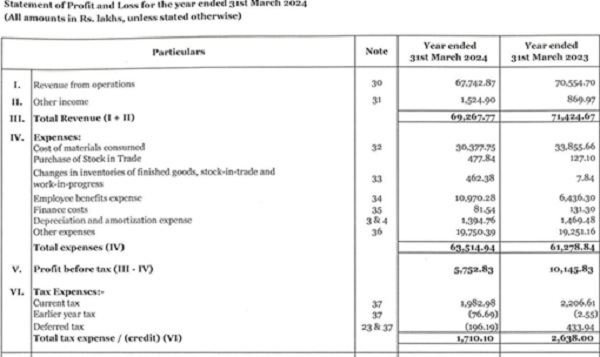

| Statement of Profit & Loss account | ||

| Particulars | Current FY | Previous FY |

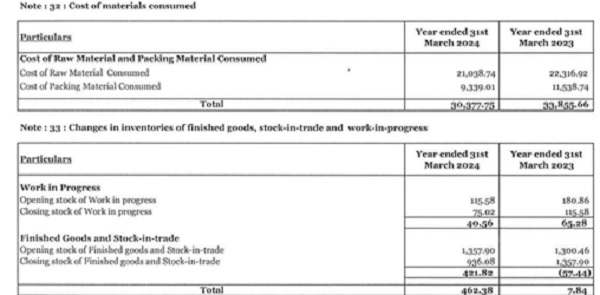

| Cost of material consumed (1953.05+30774.01-2349.31) | 30,377.75 | 33,855.66 |

| Purchase of Stock in trade | 477.84 | 127.10 |

| Changes in inventory (115.58+1357.90-75.02-936.08) | 462.38 | 7.84 |

| Balance sheet | ||

| Inventories | Current FY | Previous FY |

| – Raw Materials | 2,349.31 | 1,953.05 |

| – Work-in-Progress | 75.02 | 115.58 |

| – Finished Goods | 936.08 | 1,357.90 |

| – Stock-in-Trade | – | – |

| 3,360.41 | 3,426.53 |

4. Conclusion

Clarity in cost and inventory classification not only ensures statutory compliance but also enhances the quality of financial reporting.

Author Bio