Case Law Details

Vitthal Sahakari Sakhar Karkhana Ltd Vs ACIT (ITAT Pune)

Mere Additions Do Not Establish Concealment- Pune ITAT Deletes Penalty under Section 271(1)(c) on VSI Contribution & Omitted Section 244A Interest

Summary: The Pune ITAT allowed the assessee’s appeal and deleted the penalty of Rs.4,14,259 levied under Section 271(1)(c) of the Income-tax Act, 1961 in respect of additions relating to VSI contribution and interest received under Section 244A. The assessee, a co-operative society, had originally declared a loss, and during assessment the Assessing Officer made various additions, of which the CIT(A) sustained only the addition of VSI contribution of Rs.13,15,926 and interest under Section 244A of Rs.34,716. The Tribunal noted that the issue of VSI contribution had already been decided in favour of the assessee in earlier judicial decisions, including a coordinate bench ruling, and held that merely because the assessee did not challenge the quantum addition, penalty under Section 271(1)(c) could not be levied. Regarding the omitted Section 244A interest, the Tribunal accepted the assessee’s explanation that the omission occurred due to non-availability of the refund break-up and was a human error without any deliberate attempt to conceal income or furnish inaccurate particulars. Accordingly, it directed cancellation of the penalty on both additions and allowed the appeal.

The Pune Bench of the Income Tax Appellate Tribunal deleted the penalty levied under section 271(1)(c) on additions relating to Vasantdada Sugar Institute (VSI) contribution and interest received under section 244A, holding that the facts did not establish either concealment of income or furnishing of inaccurate particulars. The Tribunal reiterated that mere confirmation of a quantum addition does not automatically justify imposition of penalty.

The assessee, a co-operative sugar factory, had filed its return declaring a loss. During scrutiny, the Assessing Officer made various disallowances, including VSI contribution of ₹13.16 lakh and interest on income-tax refund of ₹34,716. While the CIT(A) deleted certain additions, these two additions were sustained, following which the Assessing Officer levied a penalty of ₹4.14 lakh under section 271(1)(c), which was also confirmed by the CIT(A).

Before the Tribunal, the assessee submitted that the allowability of VSI contribution was already covered in its favour by the Bombay High Court in CIT v. Jai Ambika Sahakari Sakhar Karkhana Ltd. and by the Tribunal’s own earlier decision in the assessee’s case. Therefore, merely because the assessee had not challenged the quantum addition further, penalty could not be levied on a claim that was otherwise legally debatable and supported by judicial precedents.

Accepting the contention, the Tribunal held that penalty is not leviable merely because the quantum addition has attained finality. Since the claim for VSI contribution was supported by binding judicial precedents, it could not be treated as a case of concealment or furnishing of inaccurate particulars. Accordingly, the penalty relating to the VSI contribution was deleted.

With regard to the omission to disclose interest under section 244A, the Tribunal accepted the explanation that the refund had been directly credited by the Department without separately indicating the interest component and that the omission occurred due to the absence of a detailed break-up. Considering the small amount involved and the plausible explanation offered, the Tribunal held that the lapse amounted to a bona fide human error and not a deliberate attempt to conceal income. While the addition could be sustained, the ingredients necessary for levy of penalty under section 271(1)(c) were absent. The Tribunal therefore directed cancellation of the penalty on this addition as well.

Accordingly, the Tribunal set aside the order of the CIT(A), cancelled the entire penalty under section 271(1)(c), and allowed the assessee’s appeal.

Author’s Comments:

The decision reiterates an important principle that penalty proceedings are distinct from quantum proceedings. Even where an addition is sustained, penalty cannot follow automatically unless there is clear evidence of concealment or furnishing of inaccurate particulars. The ruling is particularly significant in holding that a claim supported by judicial precedents remains a bona fide claim, and that inadvertent omission of a small amount of section 244A interest due to lack of proper details constitutes a human error rather than concealment, thereby not warranting penalty under section 271(1)(c).

Cases Discussed

1. Shri Vithal Sahakari Sakhar Karkhana Ltd. vs. ITO, ITA No.163/PUN/2018, order dated 15.07.2022

2. CIT vs. Jai Ambika Sahakari Sakhar Karkhana Ltd., Tax Appeal No.17 of 2008, order dated 07.02.2012

3. Bhima S.S.K. Ltd., ITA No.1414/PUN/2000

FULL TEXT OF THE ORDER OF ITAT PUNE

This appeal filed by the assessee is directed against the order dated 06.11.2025 of the Ld. CIT(A) / NFAC, Delhi relating to assessment year 2016-17.

2. Although a number of grounds have been raised by the assessee, however, these all relate to the order of the Ld. CIT(A) / NFAC in confirming the penalty of Rs.4,14,259/- levied by the Assessing Officer u/s 271(1)(c) of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’).

3. Facts of the case, in brief, are that the assessee is a co-operative society and filed its return of income on 29.09.2016 declaring total loss of Rs.4,50,38,687/-. The case was selected for scrutiny under CASS and thereafter the Assessing Officer completed the assessment u/s 143(3) of the Act on 26.12.2018 determining the total loss at Rs.3,85,79,520/-. In the said order the Assessing Officer made the following disallowances / additions:

| 1. | Disallowance u/s 37 | Rs.37,43,837/- |

| 2. | Addition of VSI contribution | Rs.13,15,926/- |

| 3. | Disallowance of expenses | Rs.13,64,693/- |

| 4. | Addition of interest received u/s 244A | Rs.34,716/- |

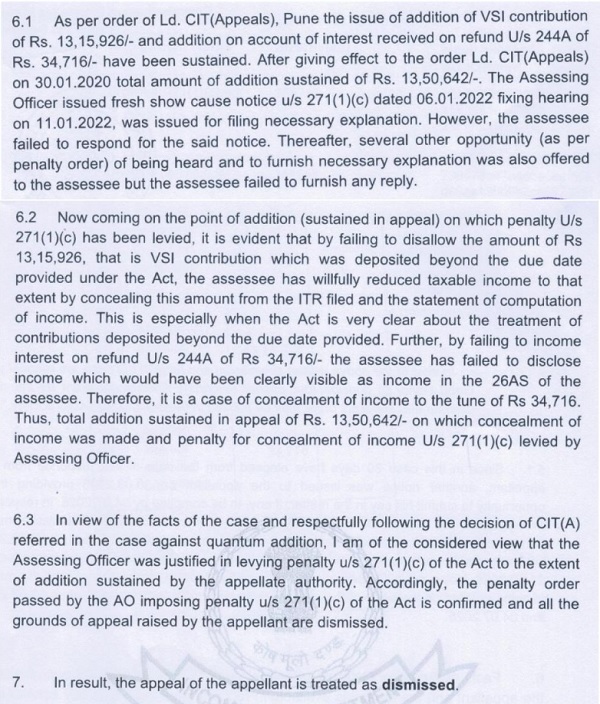

4. In appeal the Ld. CIT(A) / NFAC deleted the disallowance u/s 37 of Rs.37,43,837/- and expenses of Rs.13,64,693/-. However, he confirmed the addition of VSI contribution of Rs.13,15,926/- and interest received u/s 244A of Rs.34,716/-. The Assessing Officer thereafter initiated penalty proceedings u/s 271(1)(c) of the Act. However, there was no response from the side of the assessee to the various notices issued. The Assessing Officer therefore, levied penalty of Rs.4,14,259/- u/s 271(1)(c) being 100% of tax sought to be evaded on account of the above two additions.

5. In appeal the Ld. CIT(A) / NFAC upheld the penalty so levied by the Assessing Officer by observing as under:

6. Aggrieved with such order of the Ld. CIT(A) / NFAC the assessee is in appeal before the Tribunal.

7. So far as the disallowance / addition of VSI contribution of 13,15,926/- is concerned, the Ld. Counsel for the assessee at the outset submitted that the issue stands decided in favour of the assessee by the decision of the Hon’ble Bombay High Court in the case of CIT vs. Jai Ambika Sahakari Sakhar Karkhana Ltd. vide Tax Appeal No.17 of 2008 order dated 07.02.2012 where the Hon’ble High Court in a detailed order has allowed the contribution to Vasant Dada Sugar Institute (VSI) as an allowable deduction u/s 35(1) of the Act.

8. Referring to the decision of the Co-ordinate Bench of the Tribunal in the case of Shri Vithal Sahakari Sakhar Karkhana Ltd vs. ITO vide ITA No.163/PUN/2018 order dated 15.07.2022 for assessment year 2014-15, he submitted that the Tribunal has decided the issue in favour of the assessee allowing the claim of provision for VSI contribution. Relying on various other decisions filed in the paper book, he submitted that similar view has been taken.

9. So far as the second issue i.e. interest on IT refund is concerned, the Ld. Counsel for the assessee submitted that in absence of breakup of refund and interest paid by the department u/s 244A on refund the assessee could not show the interest income separately in the credit side of Profit and Loss Account. Further, the amount is very negligible. He accordingly submitted that no penalty should be levied on non-disclosure of the interest on IT refund of Rs.34,716/-.

10. The Ld. DR on the other hand heavily relied on the orders of the Assessing Officer and the Ld. CIT(A) / NFAC.

11. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and the Ld. CIT(A) / NFAC and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. We find the Assessing Officer in the instant case levied penalty of Rs.4,14,259/- u/s 271(1)(c) of the Act on account of two additions i.e. addition of Rs.13,15,926/- on account of VSI contribution and addition of Rs.34,716/- being the interest received on IT refund. We find the Ld. CIT(A) / NFAC sustained the penalty levied by the Assessing Officer, the reasons of which have already been reproduced in the preceding paragraphs. So far as the first addition is concerned, we find the Pune Bench of the Tribunal in the case of Shri Vithal Sahakari Sakhar Karkhana Ltd vs. ITO (supra) while deciding an identical issue has allowed the claim of VSI contribution by observing as under:

“(ii) VSI Contribution

7. The ld. AR submitted that the issue of provision for VSI contribution has been decided by the Co-ordinate Bench in favour of the assessee by following the order of Tribunal in the case of Bhima S.S.K. Ltd. in ITA No. 1414/PUN/2000. The ld. DR fairly admitted that this issue has been considered by the Co-ordinate Bench. The Co-ordinate Bench while deciding this issue in favour of assessee has observed as under :

“18. We have heard both the sides and gone through the relevant material on record. It is found that the ld. CIT(A) has determined this issue in favour of the assessee by following the order passed by the Pune Benches of the Tribunal in the case of Bhima S.S.K. Ltd. (supra). No material has been placed on record to show that this order of the Tribunal has been reversed or modified in any manner by the Hon’ble High Court. Respectfully following the precedent, we decide this issue in favour of the assessee.”

8. Thus, in view of the above findings of the Tribunal and submissions of both the sides, the issue is decided in favour of the assessee.”

12. We, therefore, are of the considered opinion that the penalty is not leviable on account of addition of Rs.13,15,926/- towards VSI contribution. Merely because the assessee has not preferred any appeal against the order of the Ld. CIT(A) / NFAC sustaining the quantum addition, the same, in our opinion, cannot be a ground to levy penalty u/s 271(1)(c) of the I T Act, 1961. We, therefore, set aside the order of the Ld. CIT(A) / NFAC sustaining the penalty u/s 271(1)(c) of the Act on addition of VSI contribution.

13. So far as the penalty levied u/s 271(1)(c) on the amount of Rs.34,716/- being the interest received on IT refund u/s 244A is concerned, we find force in the arguments of the Ld. Counsel for the assessee that due to non-availability of break-up of such refund along with interest u/s 244A of the Act since the amount has been credited to the account of the assessee directly, the assessee missed to show separately the amount of interest received u/s 244A which is a human error and there is no deliberate attempt to conceal the particulars of income or furnish inaccurate particulars. In our opinion, the same is justified for making addition but levy of penalty u/s 271(1)(c) of the Act is not justified. We, therefore, direct the Assessing Officer to cancel the penalty levied on the amount of IT refund received u/s 244A. Accordingly, the order of the Ld. CIT(A) / NFAC is set aside and the grounds raised by the assessee are allowed.

14. In the result, the appeal filed by the assessee is allowed.

Order pronounced in the open Court on 6thJuly, 2026.

Author Bio