Case Law Details

Page Contents

Yashaswi Academy for Skills Vs PCIT (ITAT Pune)

Pune ITAT Restores U/s 12AA/12AB Registration – Skill Development Institution Held to be Engaged in ‘Education’ Despite Serious Allegations

Summary: The Pune ITAT partly allowed the assessee’s appeal by setting aside the Principal CIT (Central)’s order cancelling registration under Sections 12AA and 12AB of the Income-tax Act, 1961 and directing restoration of the registrations. The Revenue had cancelled the registration following a survey alleging sham transactions, diversion of charitable funds to trustees and related parties, commercial manpower supply, hotel and restaurant operations, unreasonable salaries, loans to related concerns, and that the assessee functioned merely as a facilitator under apprenticeship schemes rather than carrying out charitable educational activities. The Tribunal first upheld the jurisdiction of the Pr. CIT (Central) to exercise cancellation powers after transfer of jurisdiction under Section 127, relying on CBDT Notification No. 70/2014 and the CBDT clarification dated 19.01.2024. However, on merits, it held that the assessee’s dominant activity was imparting education through structured skill development and apprenticeship programmes, which falls within “education” under Section 2(15). It further held that acting as a facilitator in Government-recognised skill development programmes and receiving administrative fees did not convert the institution into a commercial enterprise. Accordingly, the Tribunal held that cancellation under Sections 12AA(3), 12AA(4) and 12AB(4) was not justified and restored the registrations.

The Pune ITAT has set aside the order of the Principal CIT (Central) cancelling the registration granted to Yashaswi Academy for Skills under sections 12AA and 12AB, holding that the cancellation was not legally sustainable on the facts of the case.

The Revenue had cancelled the registration after a survey, alleging that the assessee had indulged in sham transactions, diverted charitable funds for the benefit of trustees and related parties, provided manpower on a commercial basis, operated hotels and restaurants, paid unreasonable salaries, advanced loans to related concerns, and acted merely as a facilitator under apprenticeship schemes rather than carrying out charitable educational activities.

The Tribunal first upheld the jurisdiction of the Pr. CIT (Central) to exercise powers of cancellation after transfer of jurisdiction under section 127, distinguishing earlier Tribunal decisions on the basis of CBDT Notification No. 70/2014 and the CBDT clarification dated 19.01.2024.

However, on merits, the Tribunal held that the dominant activity of the assessee was imparting education through structured skill development and apprenticeship programmes, which squarely falls within the expression “education” under section 2(15). Merely acting as a facilitator in Government-recognised skill development programmes or receiving administrative fees from industry partners did not convert the institution into a commercial enterprise. Following the principles laid down by the Supreme Court in Ahmedabad Urban Development Authority, the Tribunal held that the assessee continued to pursue charitable educational objects and was entitled to exemption under sections 11 and 12. It also distinguished the decisions of the Kerala High Court in Mahatma Gandhi Charitable Society and Annadan Trust on facts.

Accordingly, the Tribunal held that the Pr. CIT (Central) was not justified in cancelling the registrations under sections 12AA(3), 12AA(4) and 12AB(4) and directed that the registrations be restored. The assessee’s appeal was partly allowed.

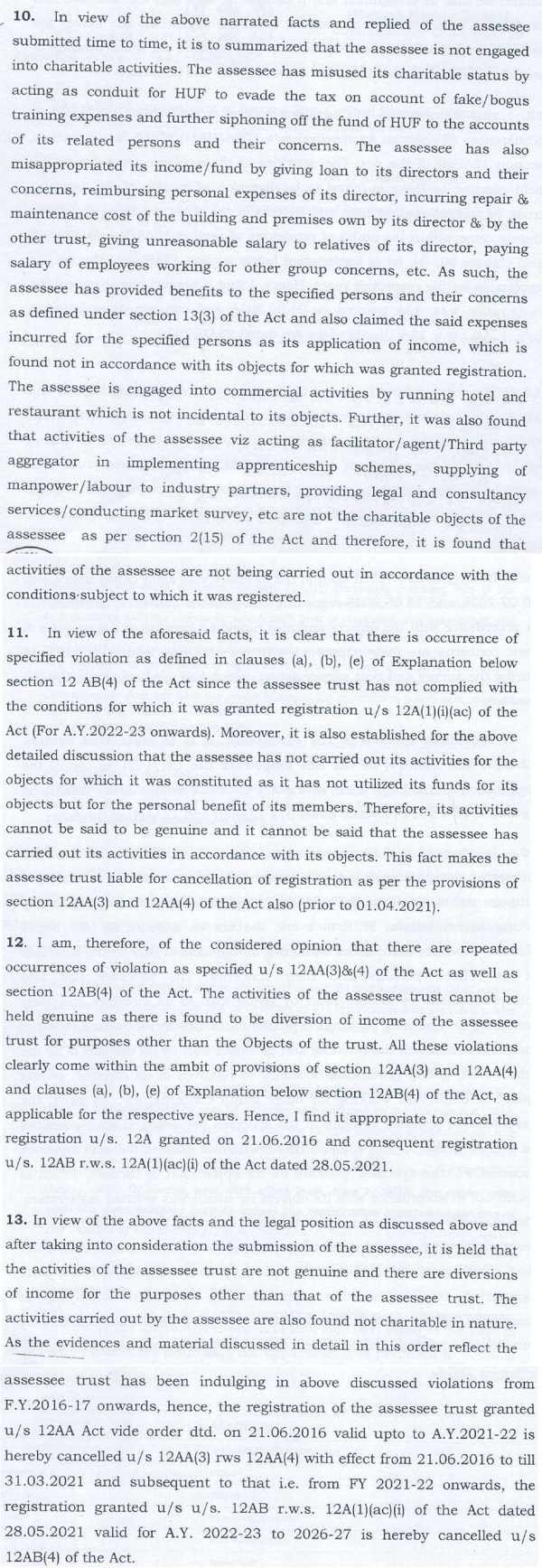

Cases Discussed

1. Yashaswi Academy for Skills Vs PCIT (ITAT Pune)

2. Ahmedabad Urban Development Authority (Supreme Court)

3. Mahatma Gandhi Charitable Society (Kerala High Court)

4. Annadan Trust (Kerala High Court

FULL TEXT OF THE ORDER OF ITAT PUNE

This appeal filed by the assessee is directed against the order dated 29.09.2025 passed by the Ld. Pr. CIT-(Central), Pune u/s 12AA(3) & 12AA(4) and 12AB(4) of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’).

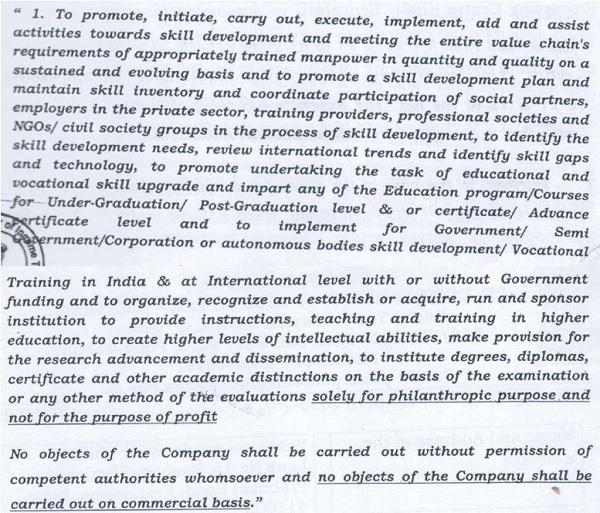

2. Facts of the case, in brief, are that the assessee Yashaswi Academy for Skills (in short ‘YAS’) was incorporated as a ‘Non-profit organization’ u/s 8 of the Companies Act, 2013 on 20.03.2014. The main object of YAS as per the Memorandum of Association (MOA) is to promote, execute and implement skill development. The relevant part of the MOA which has been reproduced by the Ld. PCIT(C) read as under:

3. In addition to the above object, the assessee has various ancillary objects in order to attain the main objects.

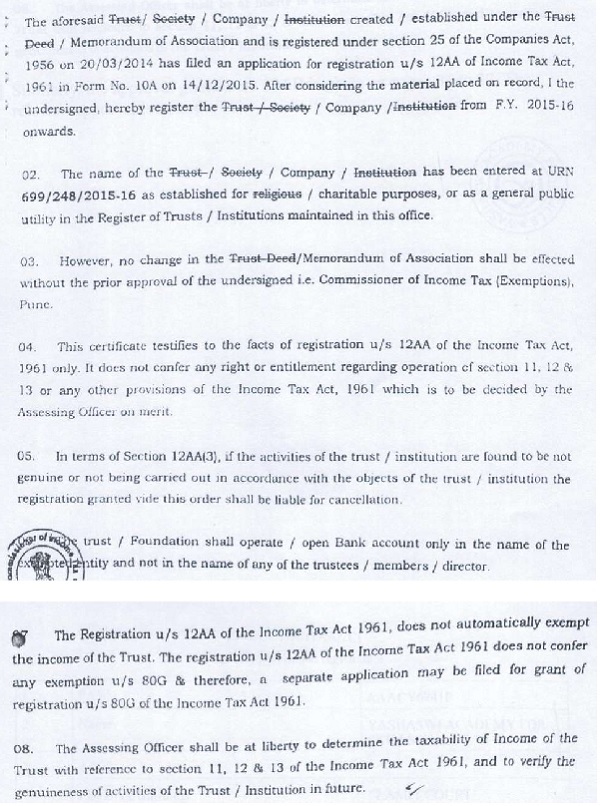

4. The assessee was granted registration u/s 12AA of the Act by the CIT(E), Pune on 21.06.2016 subject to the conditions namely “in terms of Section 12AA(3), if the activities of the trust/institution are found to be not genuine or not being carried out in accordance with the objects of the trust/institution, the registration granted vide this order shall be liable for cancellation.” The registration certificate issued u/s 12AA of the Act was valid till 31.03.2021 (Α.Υ.2021-22).

Further, due to change of registration related provisions and compliances due to introduction of section 12AB of the Act w.e.f. 01.04.2021 (relevant to A.Y.2022-23 and onwards), the assessee e-filed Form-10A for renewal of its registration as required under section 12AB r.w.s 12A(1)(ac)(i) of the Act. The registration was granted by the Central Processing Centre (CPC), Bengaluru in automated manner on 28.05.2021 which is valid from A.Y.2022-23 to AY 2026-27. The assessee has been filing its return of income showing total income at Rs.Nil after claiming exemption u/s 11 & 12 of the Act. The assessee has been claiming in the return of income that it is engaged into ‘Educational Activities’.

5. A survey action u/s 133A of the Act was conducted by ITO(Exemption), Ward-2, Pune on 06.03.2024. During the course of survey action, various incriminating documents and information were gathered. As a result of survey action and subsequent post-survey enquiries it was found that the activities carried out by the assessee are not genuine and / or are not being carried out in accordance with the objects of the trust for which it was granted the registration. It was also found that the assessee had been providing benefits to its trustees and related persons as per section 13(3) of the Act and concerns of the related persons by misappropriating its funds. The assessee was further found to be engaged in non-charitable activities which were admitted by the trustee/director of the assessee in his statement and also filed an affidavit reconfirming the same. Accordingly, it was noticed that the assessee had been consistently violating the provisions of the Income Tax Act as well as the conditions of the registration making itself liable for cancellation of its registrations granted u/s 12AA and 12A(1)(ac)(i) r.w.s 12AB of the Act as applicable to the respective years.

6. The Ld. Pr.CIT(C) noted that the Assessing Officer i.e. ITO(Exemption), Ward-2, Pune had submitted a proposal to the CIT(Exemption), Pune for cancellation of registration granted to the assessee which was duly endorsed by the Addl. CIT(Exemptions) Range, Pune vide letter no. Pn/Addl. CIT(Exemp)/12AA/630 dated 28.08.2024. Subsequently, upon centralization of the case to the charge of DCIT, Central Circle-2(2), Pune, a proposal for cancellation of the registration of the assessee was transferred to the Ld. Pr.CIT(C) vide letter no. Pn/CIT(E)/centralization/YAS/2024-25/3101, dated 31.12.2024 by the office of the CIT(E), Pune.

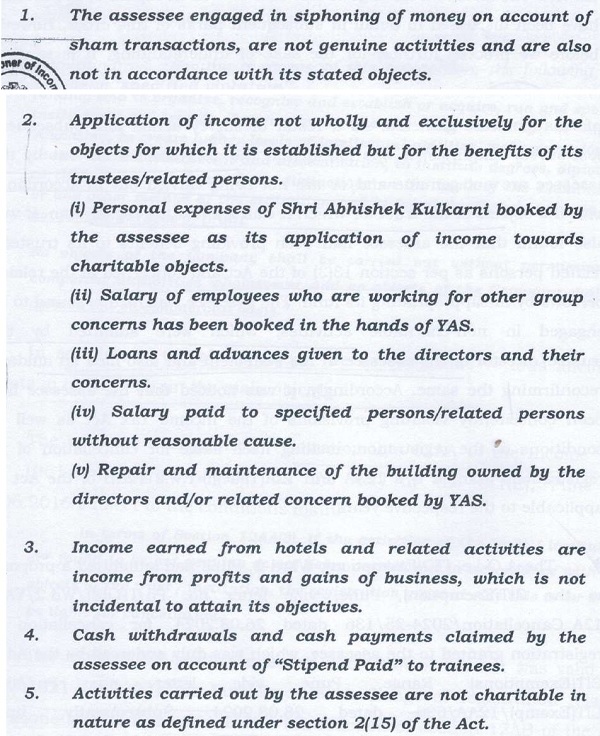

7. The Ld. Pr.CIT(C) on going through the same observed that there have been series of violations and repetitive violations in this case which can be broadly outlined as under:

8. He, therefore, issued a show cause notice asking the assessee to submit its explanation as to why the registration granted u/s 12AA of the Act dated 21.06.2016 should not be cancelled within the provisions of section 12AA(3) & 12AA(4) of the Act (applicable upto A.Y. 2021-22) and also the registration granted u/s 12A(1)(ac)(i) r.w.s 12AB of the Act (applicable for A.Y 2022-23 to 2026-27) should not be cancelled on account of specified violations u/s 12AB(4) of the Act. The assessee in response to the same filed detailed submission contending that it is a company incorporated as Non-Profit Organization engaged in charitable activities within the provisions of section 2(15) of the I.T. Act, 1961 and no income was diverted for the benefit of its trustees / settlers.

9. However, the Ld. Pr.CIT(C) was not satisfied with the explanation / submission given by the assessee and held that the activities of the assessee trust are not genuine and there are diversions of income for the purposes other than that of the assessee trust. Further, the activities carried out by the assessee are not found to be charitable in nature.

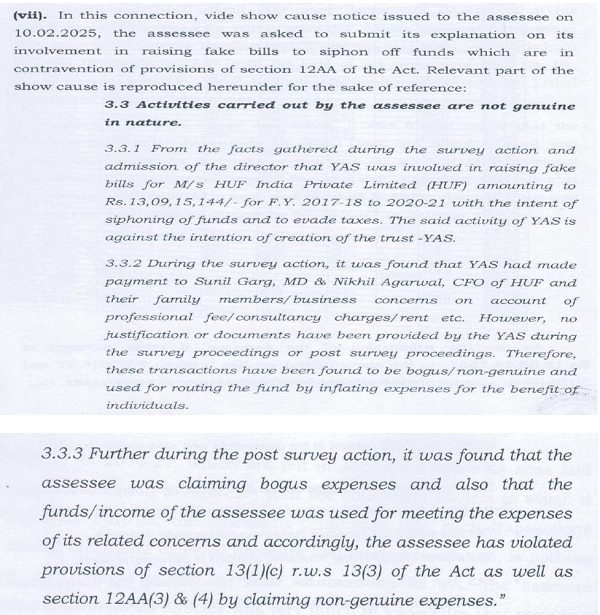

10. The first objection of the Ld. Pr.CIT(C) is that the assessee is engaged in siphoning of money on account of sham transactions which are not genuine activities and are also not in accordance with its stated objects. The Ld. Pr.CIT(C) noted that during the course of survey action, suspicious financial transactions for mobilizing manpower with M/s. HUF India Pvt. Ltd. (hereinafter may be referred as to HUF) had been found which is a subsidiary of Germany based company named HUF HULSBECK & FURST GMBH & CO. KG. The company-HUF is engaged in manufacturing of remote-controlled access and authentication of cars & automobiles. It has a manufacturing plant at Chakan, Pune. During the course of survey action, it was noticed that between F.Y. 2017-18 and 2020-21, the assessee had received substantial sums amounting to Rs.13.12 crore from HUF. However, the assessee had no such transactions with this party from December, 2020 onwards. Shri Vishwesh Kulkarni, Chairman and MD of the assessee was questioned about these transactions while recording his statement on oath. In reply, he stated that the assessee (YAS) had contract for supplying manpower & trainees to HUF. He further stated that on instructions of Shri Sunil Garg, MD of HUF, the assessee (YAS) raised additional invoices of trainees other than the regular invoices to generate cash for out-of-pocket expenses for HUF. For this purpose, Shri Sunil Garg had given names of some of the individuals and concerns to pay the amounts corresponding to the fake/additional invoices raised by YAS. Further, these amounts were debited by the assessee in its books as payments for professional fee / consultancy charges to the individuals and concerns named by Shri Sunil Garg. Shri Vishwesh Kulkarni also stated that after removal of Shri Sunil Garg from HUF, the assessee came to know that there was no such instruction given by the management of HUF to Shri Sunil Garg to generate cash. This led to discontinuation of business from HUF. He therefore held that during the course of survey action Shri Vishwesh Kulkarni has admitted that YAS was indulged in sham transactions by raising fake bills on account of manpower/trainee supply to HUF and subsequently siphoning off the funds in form of bogus professional fees/consultancy charges shown to be paid to certain individuals and concerns.

11. The Ld. Pr.CIT(C) noted that during the course of survey action the said facts were cross verified from the management of HUF. Statement of Shri Yogesh Ramdas Labade, CFO of HUF company was also recorded u/s 131 of the Act wherein he stated that HUF was engaged into business transactions with the assessee during the tenure of Mr. Sunil Kumar Garg as MD. HUF executed a contract with YAS to supply trainees, which was terminated by it after finding irregularities as mentioned in the FIR No.0380 dt. 14.03.2022 filed in Chakan Police Station. He provided a copy of the FIR to the survey team. He also stated that Shri Sunil Garg (then MD), Shri Nikhil Agrawal (then CFO) and Mr. Sandeep Wani (then Operation and administration Head) were involved in various irregular/fraudulent transactions in association with the assessee. He also confirmed that HUF had made payment of Rs.2,12,80,701/- to YAS towards actual supply of manpower/trainees, the year-wise details of which is as under:

| Year (F.Y) | Amount (Rs.) |

| 2016-17 | 29,88,518/- |

| 2017-18 | 33,39,669/- |

| 2018-19 | 79,78,184/- |

| 2019-20 | 54,75,462/- |

| 2020-21 | 14,98,868/- |

| Total | 2,12,80,701/- |

12. He noted that during the survey action it was found that the assessee had received total payment of Rs.13,12,20,437/- against which only Rs.2,12,80,701/-was towards supply of manpower/trainees during the F.Y. 2016-17 to 2020-21. This clearly establishes that payments received over and above of Rs.2,12,80,701/-were against bogus bills raised by the assessee. Shri Yogesh Ramdas Labade also submitted a copy of email dated 26.08.2020 informing discontinuation of business association with HUF. Further, during the course of survey action, statement of Shri Rajnikant Shivaji Khandebharat was also recorded u/s 131 of the Act. Shri Rajnikant Shivaji Khandebharat is an ex-employee of the assessee, who was caught by staff of HUF India Pvt. Ltd. with bogus invoices in the year 2020 which led to the expose of the scam and revealed the engagement of the assessee in raising fake invoices. Shri Rajnikant Shivaji Khandebharat was working as field officer who was removed by the assessee after exposure of the scam. Shri Rajnikant Shivaji Khandebharat explained the modus operandi of the assessee with HUF and submitted copy of fake bills raised by YAS as well as Maharashtra Industrial Services (Prop. Concern of Shri Vishwesh Kulkarni) with name of dummy trainees. He also submitted copy of a police complaint lodged and other documents in support of his statement. He confirmed to the survey team that names mentioned in the fake bills were never sent for training to HUF and the said scam was carried out by Shri Vishwesh Kulkarni with the help of key persons of HUF viz. Mr. Sunil Kumar Garg, Mr. Nikhil Agrawal, Mr. Sandeep Wani and Mr. Vishal Tamotia to siphon off the money. During the post survey verification, it was further found that the assessee had made payments to Mr. Sunil Garg, Mr. Nikhil Agarwal, and their family members & business concerns on account of professional fee/consultancy charges/rent etc. The assessee submitted the details of payments made to the said persons or their concerns during the F.Y.2016-17 to 2019-20 amounting to Rs.15,65,65,766/-. He, therefore held that the assessee was involved in malpractice of raising fake bills in addition to its regular bills to HUF with intent to further siphon off the funds on account of claiming bogus professional fees/consultancy charges/rental income, etc. Rejecting the explanation of the assessee that it was misled by Shri Sunil Garg for executing the transactions and took immediate corrective action by terminating all engagements with HUF, he noted that the activities of the assessee were against the intent of its creation as well as the charitable purposes defined under section 2(15) of the Act.

13. The Ld. Pr.CIT(C) noted that section 12AA(3) of the Act empowers the Commissioner to withdraw the registration granted u/s 12AA if he is satisfied that (a) the activities of the trust or institution are not genuine, and/or (b) are not being carried out in accordance with the objects of the trust or Institution. The instant case is covered within the both limbs of Section 12AA(3) i.e. activities of the trust are not genuine as well as not being carried out in accordance with its declared objects and therefore, in contravention of the provisions of section 12AA(3) of the Act and therefore, registration of the assessee u/s 12AA of the Act is liable for cancellation. For the above proposition he relied on the observation of the Hon’ble Apex Court in the case of Ananda Social & Educational Trust reported in CIT [2020] 114 com693/272 Taxman 7/426 ITR 340 (SC) where the Hon’ble Court held that:

“9. Section 12AA undoubtedly requires the Commissioner to satisfy himself about the objects of the trust or institution and genuineness of its activities and grant a registration only if he is so satisfied. The said section requires the Commissioner to be so satisfied in order to ensure that the object of the trust and its activities are charitable since the consequence of such registration is that the trust is entitled to claim benefits under sections 11 and 12 of the Act. In other words, if it appears that the objects of the trust and its activities are not genuine that is to say not charitable, the Commissioner is entitled to refuse and in fact, bound to refuse such registration”

14. He accordingly held that since the activities of the assessee are found to be not genuine and also not being carried out in accordance with the objects of the trust therefore it has violated the provisions of section 12AA(3) of the Act making itself liable for cancellation of registration granted u/s 12AA of the Act.

15. The next objection of the Ld. Pr.CIT(C) is that the assessee has not applied its income wholly and exclusively for the objects for which it is established but for the benefits of its trustees / related persons.

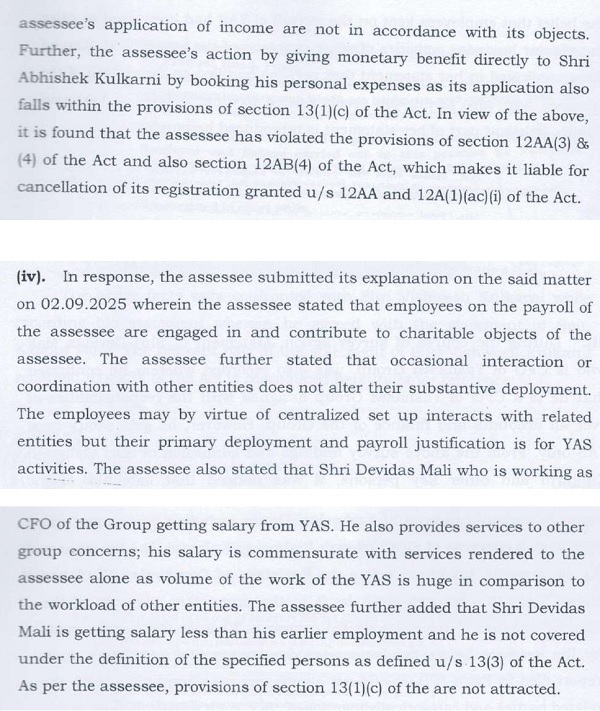

16. The Ld. Pr.CIT(C) noted that during the course of survey action it was found that the income of the assessee is being used for providing direct or indirect benefit to its settlors/trustees and their related concerns and the said benefits had been claimed by the assessee as its application of income. From the various details found during the course of survey he observed that the personal expenses of Shri Abhishek Kulkarni have been booked by the assessee as its application of income towards charitable objects. He gave certain examples of transactions which are personal and luxurious in nature and have no connection to the activities of the assessee. Rejecting the explanation given by the assessee that the payments made to credit card of Shri Abhisekh Kulkarni is reimbursement of expenses incurred by him on behalf of the company on cost to cost basis without any benefit derived by him, he held that the action of the assessee by giving monetary benefit directly to Shri Abhishek Kulkarni by booking his personal expenses as its application falls within the provisions of section 13(1)(c) of the Act. Therefore, the assessee has violated the provisions of section 12AA(3) & (4) of the Act and also section 12AB(4) of the Act which makes it liable for cancellation of its registration granted u/s 12AA and 12A(1)(ac) (i) of the Act.

17. The third objection of the Ld. Pr.CIT(C) is that the salary of employees who are working for other group concerns has been booked in the hands of YAS. He noted that although the various employees are getting salary from the assessee, however, they are working at the corporate office where 15 concerns are being run actively and the assessee used to take care of works of other concerns of group. Therefore, by bearing cost of salary and other expenses of the employees who are working for the other group concerns, the assessee provides benefit to its related concerns / persons specified u/s 13(3). He, therefore, was of the opinion that the assessee has violated the provisions of section 12AA(3) & (4) as well as 12AB(4) of the Act which make the assessee liable for cancellation of its registration granted u/s 12AA and 12A(1)(ac) r.w.s. 12AB of the Act.

18. The fourth objection of the Ld. Pr.CIT(C) is that the assessee society has given loans and advances to the directors and their concerns.

19. The Ld. Pr.CIT(C) observed from the financial statements of the assessee that it has advanced huge amount of loans to various concerns of Yashashwi Group including proprietary and partnership concerns of Shri Vishwesh Prabhakar Kulkarni. The assessee in its audit report submitted before the Registrar of Companies (ROC) has shown loans & advances given by it to the proprietary concerns of the director and also to the other related concerns. However, disclosures made by the assessee before the Income-tax department in its statutory audit report filed in Form-10B does not show any such transaction with the related parties and categorically mentioned “NO” such transaction. According to the Ld. Pr.CIT(C), providing loans and advances by the assessee to its related concerns/parties during financial year 2017-18 till the date of survey action which were either accumulated by claiming exemption u/s 11 of the IT Act, 1961 or borrowed by the assessee by taking loans shows that the assessee has diverted its funds to the specified persons and their concerns for their business activities which does not align with the stated objects of the assessee.

20. The next objection of the Ld. Pr.CIT(C) is that the salary has been paid to specified persons/related persons without reasonable cause.

21. He observed that during the course of survey action it was found that the assessee had paid salary to relatives of the directors and also other employees who are not on the payroll of the assessee-YAS. It was also found that the assessee has paid unreasonable amount of salary to Smt. Shobha Kulkarni who is wife of Shri Vishwesh Kulkarni & mother of Shri Abhishek Kulkarni. Mr. Vishwesh Kulkarni and Mr. Abhishek Kulkarni, both are the directors of the assessee. During the survey action, it was gathered that Smt. Shobha Kulkarni is one of the active partners in M/s. Reliable Industrial Services which is engaged into labour supply business. At the same time, she runs a beauty parlor as her proprietary concern under the name and style of “Femina Flaunts Studio Salon”. During survey, Smt. Shobha Kulkarni was questioned about her role and responsibility in YAS. She admitted in her statement recorded u/s 131 of the Act that she is not actively engaged in the activities of YAS and she only signs the documents as directed by her husband Shri Vishwesh Kulkarni.

22. He further noted that Miss Abhilasha Kulkarni, daughter of Shri Vishwesh Kulkarni had been getting salary whereas it was learned during the survey action that she was in United Kingdom for pursuing her studies. Furthermore, Shri Vishwesh Kulkarni failed to justify such excessive and unreasonable salary paid by YAS to his wife and daughter without actually rendering of services. Moreover, admission of Smt. Shobha Kulkarni that she does not have active participation in affairs of YAS and only signs as instructed by her husband, also revealed that related persons have been given direct benefits by the assessee by booking bogus/unreasonable salary expenses in its hand. In view of the above, he held that providing the benefits to the related persons and further claim of such benefits as application of its income are violation of the provisions of section 12AA(3) & (4) of the Act as well as clause (a) & (e) to Explanation of Section 12AB(4) of the Act of the Act which makes the assessee liable for cancellation of its registration u/s 12AA and 12A(1)(ac) r.w.s 12AB of the Act.

23. The next objection of the Ld. Pr.CIT(C) is that repair and maintenance of the building owned by the directors and/or related concern are booked by YAS. The Ld. Pr.CIT(C) observed that during the survey it was noticed that Yashaswi House, Lane No. 15, Prabhat Road, Pune-04 was being used as corporate office of Yashaswi Group to manage and control the business activities of all the concerns of the Group. However, renovation, repair & maintenance charges were booked in the hands of the assessee only. Shri Vishwesh Kulkarni in his statement recorded during the course of his survey had stated that Yashaswi House is owned by him and is being used for business activities of the assessee without charging any rent. Therefore, whatever recurring expenses of the building incurred had been booked in the hands of the assessee. The Ld. Pr.CIT(C) further noted that the assessee had also booked renovation expenses of building owned by a trust named Yashaswi Education Society at Pimpri Chinchwad, Pune which is registered under The Bombay Trust Act, 1950. Shri Vishwesh Kulkarni and his family members are the trustees/settlers of the trust Yashaswi Education Society, which is engaged into running and managing of a college under the name and title of International Institute Management Science (IIMS), Pimpri Chinchwad, Pune. He observed from the submission of Shri Vishwesh Kulkarni made during the survey action that the assessee had claimed expenses under head ‘Repair & Maintenance’ of building of Rs.67,94,795/- and Rs.7,37,38,213/- for F.Y.2022-23 and 2023-24, respectively. Similarly, it claimed expenses under the head ‘Repair & Maintenance – Others’ of Rs.1,20,07,183/- and Rs.1,05,73,368/ for F.Y.2022-23 and 2023-24, respectively. In addition, it was also found that many of the computers shown purchased in the hands of the assessee during F.Y.2021-22 have been delivered to one Mr. Pawan Sharma belonging to IIMS, Chinchwad, Pune for utilization of Yashaswi Education Trust. Shri Vishwesh Kulkarni in his statement recorded during the survey action had also admitted that all expenses for renovation work of Yashaswi Education Society had been borne by YAS. In view of the above he observed that the assessee diverted its income by showing such expenses as its application towards the objects to provide direct benefits to the specified persons/their concerns. Booking of those expenses in the hands of the assessee as its application of income, which are also not in accordance with objects of the trust, are violations of provisions of section 12AA(3) & (4) of the Act as well as under specified violation of 12AB(4) of the Act which makes the assessee liable for cancellation of its registration granted u/s 12AA and 12AB r.w.s 12A(1)(ac) of the Act.

24. The next objection of the Ld. Pr.CIT(C) is that the income earned from hotels and related activities are income from profits and gains of business, which is not incidental to attain its objectives. He noted that during the course of survey action, it was found that the assessee is running a restaurant named “Amit Garden Restaurant” in the premises of MSIHMCT at 412C, Shivaji Nagar, Deep Bangla Chowk, Senapati Bapat Road, Pune and extension part at 412/D, Shivaji Nagar, Pune named as Amit Garden Restaurant (also called Yashaswi Academy for Skill (Food Lab)) in collaboration with Maharashtra State Institute of Hotel Management and Catering Technology (MSIHMCT). The undertaken premises consist of 30 rooms hotel, a banquet hall, cafeteria, auditorium, etc. at Shivajinagar. The income generated from the hotel business was shown by the assessee in its books of account as part of its total income received from charitable activities. According to the tripartite agreement executed between Maharashtra State Institute of Hotel Management and Catering Technology (MSIHMCT) as first party, Maharashtra State Board of Technical Education (MSBTE) as second party and Yashaswi Academy for Skills (YAS) as third party, and they mutually agreed to impart on the job training to aspirants in the field of Hotel Management, Bakery & Food production, etc. wherein roles and responsibilities of the assessee were very much defined. He noted from the agreement that it was assessee’s responsibility to generate revenue from the infrastructure of the MSIHMCT by deciding competitive rates.

25. The Ld. Pr.CIT(C) noted that during the survey action, it was found that the rates charged by the assessee were at market rates and/or higher than the market rates. The said restaurant was run like any other restaurant of the market. No facility by way of discount/concession was offered by the assessee to students/trainees. The said restaurant was accessible to all. From the details of staff working at the restaurants gathered during the course of survey action, it was found that all of them were working on the payroll of the assessee and no one was found working as a trainee to get on-the-job training. Therefore, the income of the assessee from the above activity was found not incidental to attainment of its objects. According to the Ld. Pr.CIT(C) as per the provisions of section 2(15) of the Act, business of running a restaurant does not come within the purview of charitable activity. The role of the assessee as per the agreement was to implement various skill development programs in the areas of Food & Beverages, Housekeeping, Bakery, Cookery, Front Office etc. However, in the guise of skill development, the assessee was found running restaurants and hotel, which was neither the object of the assessee nor incidental to attain its objects. He, therefore, held that the assessee has focus on commercial activities rather than training/skill development for which infrastructure of MSIHMCT has mainly been given to the assessee to operate. The Ld. Pr.CIT(C) referred to the letter issued by Maharashtra State Board of Technical Education (MSBTE) on 01.03.2024 wherein the assessee was directed to stop running hotel/restaurant from the premises as the same had not been approved in the MOU. The MSBTE also clarified in the letter that the Board had conducted an inquiry and found that running a hotel and similar activities were not part of the MOU. He, therefore, held that the assessee runs hotel and similar activities in the guise of skill development and on the job training, which is not incidental to attainment of its objectives. The same is also not in accordance with the objects of the assessee. The Ld. Pr.CIT(C) therefore, held that the registration granted u/s 12AA & 12AB r.w.s 12A(1)(ac) of the Act to the assessee is liable for cancellation on account of violation of the provisions of section 12AA(3) of the Act (applicable for registration granted u/s 12AA of the Act valid by 31.03.2021) as well as 12AB(4) of the Act (applicable for registration granted u/s 12A(1)(ac)(i) of the Act from 01.04.2021 onwards).

26. The next objection of the Ld. Pr.CIT(C) is that cash withdrawals and cash payments have been claimed by the assessee on account of “Stipend Paid” to trainees.

27. The Ld. Pr.CIT(C) noted that during the course of survey action it was noticed from the cashbook that there were withdrawals of cash throughout the year and subsequent payments mainly with narration “Being Stipend paid”. During the survey action, Shri Vishwesh Kulkarni was asked while recording his statement to explain the utilization of the cash as the same was not the petty cash expenses. However, Shri Vishwesh Kulkarni didn’t give satisfactory explanation by just saying that it had been advised by the auditor to pass such entry. During the course of survey action, cash of Rs.84,96,900/- was also found physically in the cabin of Shri Vishwesh Kulkarni whereas as per the trial balance of the assessee, cash in hand position was of Rs.2,91,92,817/-. On being questioned, he stated in his statement that he would submit the reconciliation after going through the books of accounts. Further, during the post survey, the assessee submitted a reconciliation in respect of cash found physically and cash as per its books of accounts.

28. However no documentary evidence submitted by the assessee to prove the genuineness of such huge cash payments as stipend. He noted that under the NAPS, NATS and other such schemes, the apprentice’s stipend was payable by way of electronic mode directly to the apprentice’s verified bank account. Under, the National Apprenticeship Promotion Scheme (NAPS), it is a Direct Beneficiary Transfer (DBT) scheme with the Government of India (GoI) support going directly to the apprentices account instead of reimbursement to the establishment as earlier. If establishment chooses not to take the benefit of reimbursement, considered as a non-DBT contract, the stipend was payable to the account of the assessee electronically and not in cash. He noted that the assessee in its reply vide letter dated 27.03.2025 stated that it is providing structured training and skill development under government-approved apprenticeship programs like NEEM, NAPS etc under the Ministry of Skill Development. The assessee further stated that there has been no diversion of funds for non-charitable purposes and it has been incurred towards operational necessities such as stipend disbursements, local procurement, and emergency expenses. It has not misused for personal benefits of directors, or related parties. However, he noted that the above explanation of the assessee was not supported with any documentary evidences. He, therefore, issued a show cause notice asking the assessee to submit relevant documents to justify and prove genuineness of the cash payment made on account of stipend.

29. In reply, the assessee submitted documents for the payment of stipend out of cash withdrawals on 17.09.2025. The Ld. Pr.CIT(C) noticed from the details that the cash vouchers contain cash payments details till F.Y.2023-24. In addition to that no other documents to prove the genuineness of the apprentices worked with the respective establishments, copy of agreement with the apprentices and establishments, identity of apprentices, application forms of the apprentices, muster sheet and other documents to verify the terms and conditions of the agreement regarding payment of stipends, identity of the trainees as well as genuineness of the cash payments were furnished. The assessee has also not submitted any explanation on claim of cash payments, which are against guidelines of NAPS Scheme and other similar Schemes which give mandate the establishment to pay stipend through electronic mode and not in cash. Thus, the assessee failed to satisfactorily explain and justify such huge cash withdrawals and claim of subsequent payments as stipend to the trainees. According to the Ld. Pr.CIT(C) the said activities carried out by the assessee are no longer said to be genuine and in accordance with its objects. He, therefore, held that the assessee has made specified violation of the law as per section 12AB (4) of the Act and therefore, its registration u/s 12AB r.w.s 12A(1)(ac) is liable for cancellation.

30. The next objection of the Ld. Pr.CIT(C) is that the activities carried out by the assessee are not charitable in nature. He noted that the assessee is incorporated under the Companies Act 2013 on 20.03.2014 as ‘Not for Profit Organization”. The assessee-YAS holds registration under Sec 12AA/12AB of Income Tax Act 1961 and also having 80G registration. The company on the strength of its registration has regularly been claiming exemption u/s 11 & 12 of the IT Act in its ITR by showing that it is engaged into charitable activity i.e. Education. However, in result of the survey findings, it was noticed that the assessee is mainly working as manpower supplier as well as Facilitator/Third-Party-Aggregator (TPA)/Agent for industry partners to implement government sponsored skill development schemes mainly NEEM, NAPS, etc.

31. The Ld. Pr.CIT(C) noted that during the course of survey it was seen that no physical infrastructure like classroom, educational equipment, etc. were found at any of the premises. It was gathered that the assessee is only giving orientation to trainees/students about the industry before sending the fresher trainees to industry for on-the-job training. No skill development course is conducted for these students. On being enquired from the directors of the assessee regarding its activities, it was informed that the activities relating to apprenticeship, registration of students, submission of compliance on portal, training activities are being conducted only at branch office of the assessee at IIMS, S. No. 169/A, Chinchwad, Opp. Elpro International, Chinchwad, Pune. He referred to the statement of Smt. Jayashree Sandeep Sakpal working as Apprentice Compliance Head of the assessee at S. No.169/A, Chinchwad, Opp. Elpro International, Chinchwad, Pune wherein she explained the process of registration of apprentices / trainees. She stated that YAS approaches to the educational institutions for supply of apprentices. Thereafter, as per requirement, the students are being sent to the companies. The respective company completes the scrutiny process and sends the data of the selected students to YAS for further procedure. Subsequently, selected students come to Apprentice Compliance Department of YAS at Chinchwad office where their data is uploaded on the government portal and contract letters are given to the students with direction to join the companies/industry partners. In order to provide students/trainees to the industry, YAS charges service charge from the respective companies/Industry partners.

32. The Ld. Pr.CIT(C) noted that during the course of survey proceedings, Statement of Shri Vishwesh Kulkarni, Chairman and Director of YAS was also recorded wherein he stated that YAS is mostly working as a facilitator or intermediary for the Govt. to implement its various schemes. He further stated that YAS is mostly helping in implementing NEEM (National Employability Enhancement Mission), NAPS (Nation Apprenticeship Promotion Scheme) and NATS (National Training Scheme). For providing the services as Facilitator (for NEEM) or Third-Party Aggregator (for NATS & NAPS), the assessee charges administration fee from the concerned industries as per the agreement with them. Further, during the survey action, Shri Vishwesh Kulkarni was questioned to explain as to how the above role of the assessee comes under the domain of charitable activities. In reply, Shri Vishwesh Kulkarni admitted that activities of the assessee are similar to its other profit-making concerns viz. Reliable Industrial Services (Partnership Firm), Yashaswi Manpower Services (Prop. Concern), which are engaged in supplying of manpower, Shri Vishwesh Kulkarni also intended to surrender 12A/12AA registration certificate of the assessee in absence of any charitable activity.

33. In addition to the above, during the post-survey verification, it was further found from the incriminating impounded data back-up that there were folders in the name of “Business Associates”. In the said folders, there were various copies of agreements executed by the assessee for implementation of NEEM and NAPS Schemes with third parties.

34. The Ld. Pr.CIT(C) further noted that Shri Vishwesh Kulkarni submitted an affidavit voluntarily offering to surrender the registration granted to Yashaswi Academy for Skills u/s 124(1)(ac)(i) of the Income-tax Act, 1961 with immediate effect valid from A.Y.2022-23. Further, during the post-survey action, while analysing the facts gathered during the survey action, it was found that there was no change in the nature of activities carried out by the assessee prior to F.Y.2021-22. During the earlier years also, the assessee was mainly working as Third Part Aggregator/Facilitator/Agent in mobilization of the manpower for industry partners. Therefore, he was of the opinion that the activities carried out prior to F.Y.2021-22 by the assessee were also non charitable activities, hence, not eligible for claim of exemptions u/s 11 & 12 of the Act.

35. The next objection of the Ld. Pr.CIT(C) is regarding supply of contractual labour by the assessee. The Ld. Pr.CIT(C) observed that during the survey action it was noted that the assessee supplies contractual labour to its industry partners which is not in accordance with objects of the assessee. He referred to the statement of Shri Jitendra Polekar recorded during the survey action, wherein he stated that as on the date of survey action, YAS had provided 619 contractual labourers to various industry partners. Shri Jitendra Polekar was looking after payroll department of the Yashaswi Group. It was also found that the assessee is engaged in supply of contractual labour to the industry partners and such activity is not a charitable activity. The same is also not in accordance with the objects of the assessee for which it was granted registration u/s 12AA/12A of the Act.

36. The next objection of the Ld. PCIT is that the Salary Benchmarking Services and Other Services provided by the assessee to M/s. GKN Sinter Metal Pvt. Ltd is not charitable in nature and also not in accordance with its objects. He noted that during the course of survey action, statement of Shri Nikhil Darekar, Manager HR of M/s. GKN Sinter Metals Pvt Ltd., who is one of the industry partners of the assessee, was recorded on oath u/s 131 of the Act. It was found from the statement of Shri Nikhil Darekar that the assessee had conducted Salary Benchmark Survey and other services for M/s. GKN Sinter Metal Pvt. Ltd. which is not commensurating with the objects of the assessee. Further, on being cross examined Shri Vishwesh Kulkarni admitted in his statement recorded on oath on 11.06.2024 that the assessee had provided Salary Benchmarking Services to M/s. GKN Sinter Metals Pvt. Ltd. and other companies too. From the invoices of M/s. GKN Sinter Metal Pvt. Ltd. raised by the assessee, he noted that the assessee had raised various bills in the name of services provided to M/s. GKN Sinter Metal Pvt. Ltd. which are not in accordance with its approved objects. He therefore held that the activities carried out by the assessee are beyond its objects and commercial in nature. To maximize its profits the said activities are neither relating to the assessee’s objects nor being incidental to the attainment of its objects.

37. In view of the various violations and non-charitable activities carried on by the assessee, the Ld. Pr.CIT(C) issued a show cause notice asking the assessee to explain as to why the registration granted u/s 12AA should not be cancelled. Rejecting the various explanations given by the assessee and relying on various decisions the Ld. Pr.CIT(C) cancelled the registration granted u/s 12AA by observing as under:

38. Aggrieved with such order of the Ld. PCIT the assessee is in appeal before the Tribunal by raising the following grounds:

The following grounds are taken without prejudice to each other On facts and in law,

1) The order passed by the learned Pr. CIT(C), Pune dated 29.09.2025 u/s 12AA(3) and 12AA(4) and 12AB(4) is barred by limitation and hence, the same may be declared null and void.

2) The learned Pr. CIT(C), Pune erred in cancelling the registration granted to the assessee company u/s 12AA and section 12AB of the Act, without appreciating that the power to cancel registration under Section 12AB(4) is vested exclusively with the Principal Commissioner/Commissioner of Income Tax (Exemption) vide CBDT Notification and the exercise of such powers by the Ld. Pr. CIT(C) was without jurisdiction and hence, the order passed u/s 12AA(3) and 12AA(4) and u/s 12AB(4) may kindly be declared null and void.

3) The learned Pr. CIT(C), Pune failed to appreciate that the jurisdiction to cancel the registration u/s 12AA and 12AB could not be transferred from CIT(E) to the Pr. CIT(C) and hence, the order passed u/s 12AA(3) and 12AA(4) and 12AB(4) is invalid in law and hence, the same may be declared null and void.

4) The order passed by the learned Pr. CIT(C) u/s 12AA(3) and 12AA(4) and 12AB(4) is invalid in law since the same has been passed in violation by the provisions of section 12AA(5) and hence, the said order passed by the learned CIT(C) be declared null and void.

5) Without prejudice to the ground No.4, the assessee submits that the learned Pr. CIT(C) erred in cancelling the registration granted u/s 12AA vide order dated 21.06.2016 which was valid upto 31.03.2021 u/s 12AA(3) and 12AA(4) without appreciating that no order u/s 12AA(3) and 12AA(4) could be passed after 31.03.2021 and hence, the order passed by the learned CIT(C) is invalid in law and the same may be declared null and void.

6) The order passed by the learned Pr. CIT(C) dated 29.09.2025 be declared null and void since the show cause notices issued dated 10.02.2025 and 13.08.2025 were invalid in law.

7) The learned Pr. CIT(C) erred in holding that the assessee was not engaged in charitable activities and thus, the registration granted u/s 12AA and 12AB was required to be cancelled.

8) The learned Pr. CIT(C) erred in holding that-

a. The assesse company was mainly engaged as a Third Party Aggregator (TPA) / Facilitator / Agent for mobilizing the candidates and other procedural work w.r.t. implementation of the Apprenticeship Programs with a core intent to receive professional service charges and hence, such activities could not be said to be charitable in nature as laid down in section 2(15) of the Act.

b. The assessee was engaged in subcontracting of its work under NEEM, NAPS, etc. which resulted in violation of its agreements executed with the concerned Government Departments and also the conditions on which the assessee company was granted registration u/s 12AA/12AB of the Act.

c. The activities carried out by the assessee were not in accordance with its stated objects for which it was registered and hence, the assessee was not entitled to registered u/s 12AA/12A(1)(ac)(i) r.w.s. 12AB of the Act.

d. The assessee was supplying contractual labour to its industry partners which was not in accordance with the objects of the assessee and hence, the registration granted to the assessee was required to be cancelled.

e. The assessee had carried out salary benchmarking services and other services for GKN Sinter Metal Pvt. Ltd. which were beyond the objects of the assessee company and were commercial in nature.

f. The assessee was not engaged in the activities of providing education and was merely working as an agent for mobilizing manpower.

8) The learned Pr. CIT(C) erred in not appreciating that the assessee was engaged providing educational to the trainees and hence, there was no reason to hold that the assessee was not engaged in carrying out educational activities.

9) The learned Pr. CIT(C) erred in not appreciating that the assessee was appointed by Government authorities to provide theoretical training to the trainees and for which all the relevant evidences were submitted to him and therefore, there was no reason to hold that the assessee was not engaged in providing education.

10) The Ld. Pr. CIT(C) failed to appreciate that the activity of providing contractual labour or carrying out benchmarking and other services was incidental to the main objects of the assessee and hence, there was no reason to hold that the assessee had carried out commercial activities and therefore, the cancellation of registration on the said ground was not justified at all.

11) The Ld. Pr. CIT(C) erred in not appreciating that there was no prohibition on the assessee for engaging any third parties and the assessee had not violated provisions of any law or agreement entered into with Governmental Authorities and hence, the cancellation of the registration on this ground is not justified at all.

12) The Ld. Pr. CIT(C) erred in not appreciating the voluminous details provided by the assessee in the form of details of teaching faculties as well other details to prove that it was actively engaged in providing basic as well a theoretical training to the trainees and hence, it is not justified on his part to hold that the assessee was not engaged in providing education.

13) The learned CIT(C) erred in holding that the assessee had indulged in sham transaction by raising fake invoices in the name of HUF India Pvt. Ltd. with an intention to siphon off the funds by claiming bogus expenses and the said activity could not be said to be charitable in nature u/s 2(15) of the Act.

14) The learned Pr. CIT(C) further erred in holding that the assessee had carried out non genuine and illegal activity of money laundering which could not be considered as charitable in nature and therefore, the registration granted was required to be cancelled.

15) The learned Pr. CIT(C) erred in holding that the activities carried out by the assessee were not genuine and the same were not carried out in accordance with the objects of the Institution and therefore, the registration granted was required to be cancelled.

16) The learned Pr. CIT(C) failed to appreciate that the transactions carried out by the assessee with HUF India Pvt. Ltd. were under external pressure and misrepresentation of facts and no benefit was received therefrom by the trustees or related parties and therefore, there was no reason to cancel the registration on that ground.

17) The Ld. Pr. CIT(C) erred in not appreciating that the correct facts in respect of the transactions entered into by the assessee with HUF India Pvt. Ltd. and there was no reason to cancel the registration granted on the said ground.

18) The learned Pr. CIT(C) erred in holding that the assessee had debited personal expenses of Shri Abhishek Kulkarni as an application of income which resulted in violation of the provisions of section 13(1)(c) and accordingly, the registration granted was required to be cancelled.

19) The learned Pr. CIT(C) erred in holding that by debiting the personal expenses of Shri Abhishek Kulkarni, the assessee had violated the provisions of section 12AA(3) and 12AA(4) and also section 12AB(4) and hence, the registration granted was required to be cancelled.

20) The Id. Pr. CIT(C) failed to appreciate that Shri Abhishek Kulkarni had incurred expenses on behalf of the assessee which were reimbursed to him and hence, it was not a case of incurring any personal expenses of Shri Abhishek Kulkarni and accordingly, there was no violation of the provisions of section 13(1)(c) of the Act and hence, the cancellation of the registration on the said ground was not justified at all.

21) The learned Pr. CIT further erred in holding that the employees of the assessee were also working for other concerns owned by Kulkarni Family and therefore, the cost incurred to that extent could not be considered as an application of income towards the charitable objects and therefore, it resulted in violation of the provisions of section 12AA(3) and 12AA(4) as well as section 12AB(4) and accordingly, the registration granted was required to be cancelled.

22) The learned Pr. CIT failed to appreciate that the salary paid to the employees was only in respect of the work carried out by them for the assessee and simply because some of the employees were also working for the other entities owned by Kulkarni Family was not a reason to hold that the part of the salary paid was not towards the objects of the trust and hence, cancellation of registration on the said ground was not justified.

23) The Ld. Pr. CIT(C) erred in not appreciating that the salary paid to the concerned employees was commensurate with the work carried out by them for the assessee and hence, simply because they may have provided their services to other concerns of related persons did not imply that the assessee had provided benefit in violation of the provisions of section 13(1)(c).

24) The learned Pr. CIT further erred in holding that the assessee had diverted its funds to the specified persons and their concerns by not charging interest on the loans given which was not in accordance with the objects of the assessee company and hence, the registration granted was required to be cancelled on this ground.

25) The learned Pr. CIT further erred in holding that the assessee had paid salary to Mrs. Shobha Kulkarni and Ms. Abhilasha Kulkarni which was unreasonable / bogus and thereby had provided benefits to the related persons and accordingly, the provisions of section 12AA(3) and 12AA(4) were attracted as well as was clauses (a) and (e) to explanation of section 12AB(4) were attracted and therefore, the registration granted to the assessee was required to be cancelled.

26) The learned Pr. CIT(C) further erred in holding that the assessee had incurred repairs and maintenance expenses of the building owned by the Directors and/or the related concerns which resulted in providing benefit to the related persons and therefore, the assessee had violated the provisions of section 12AA(3) and (4) as well as provisions of section 12AB(4) and therefore, the registration granted to the assessee was required to be cancelled.

27) The learned Pr. CIT(C) failed to appreciate that the assessee had not provided any benefit to the related parties either in the form of salary or incurring of repairs and maintenance expenses and therefore, there was no reason to cancel the registration granted to the assessee.

28) The learned Pr. CIT(C) erred in not appreciating the reasons because of which the assessee had provided interest free advances to the Directors and their concerns and therefore, the cancellation of registration on the said ground was not justified.

29) Under the facts and circumstances of the case, the Ld. PCIT (Central) erred in passing the order of cancellation under section 12AA(3)/(4) and 12AB (4) based purely on assumptions and incorrect facts without properly appreciating that there was no violation of the provisions under Sections 11 to 13 of the Income Tax Act.

30) The Ld. Pr. CIT(C) erred in not appreciating that the expenditure incurred by the assessee on behalf of Yashawi Education Society was in the form of donation to the said charitable organization and hence, no benefit was provided by the assessee to the related persons by incurring the said expenses.

31) Without prejudice to the above grounds, the assessee submits that if at all, there is any violation of the provisions of section 13(1)(c), in that event, the income to that extent could be taxed but cancellation of registration granted u/s 12AA/12AB was not justified on the said issue.

32) The learned Pr. CIT(C) further erred in holding that the assessee was running a hotel which was a commercial activity and the same was not in accordance with the objects of the assessee and therefore, the registration granted was required to be cancelled.

33) The learned Pr. CIT(C) failed to appreciate that the assessee was not running the hotel on commercial basis and it was incidental to the main objects of the assessee and accordingly, there was no reason to cancel the registration on the said ground.

34) The learned Pr. CIT(C) failed to appreciate that the hotel activity carried out by the assessee was in furtherance to the objects of the trust and accordingly, there was no reason to cancel the registration on the ground that the said activity was carried out on commercial basis.

35) The learned Pr. CIT(C) erred in holding that the assessee had incurred expenditure on non genuine activity by showing the same as stipend paid in cash and therefore, the assessee had committed a specified violation as per section 12AB(4) and therefore, the registration granted was required to be cancelled.

36) The learned Pr. CIT(C) failed to appreciate that the assessee had paid stipend in cash to some of the trainees and the expenditure incurred was genuine and hence, the assessee had not committed any specified violation of law and accordingly, the cancellation of registration on the said ground was not justified.

37) The learned Pr. CIT(C) further erred in relying upon the affidavit of Shri Vishwesh Kulkarni wherein he had admitted that the assessee was not engaged in charitable activities without appreciating that the said affidavit was incorrectly given and the assessee had filed a retraction affidavit to that effect.

38) The learned Pr. CIT(C) erred in not appreciating that the assessee had not committed any specified violation as referred to in section 12AB(4) in any of the years and therefore, the cancellation of registration granted u/s 12AA and 12AB is not justified and the assessee prays for restoration of the registration granted to it.

39) The Ld. Pr. CIT(C) has erred in holding that the activities of the appellant are not genuine and are not being carried out in accordance with the objects of the Assessee company, despite extensive documentary evidence filed during the course of proceedings.

40) The Ld. Pr. CIT(C) erred in not appreciating the correct facts of the case while cancelling the registration granted to the assessee u/s. 12AA/12AB of the Act and accordingly, the registration granted may kindly be restored.

41) The appellant craves leave to add, alter, amend or delete any of the above grounds of appeal.

39. Ground of appeal No.1 by the assessee relates to the order of the Ld. Pr.CIT(C) cancelling the registration dated 29.09.2025 as barred by limitation.

40. The Ld. Counsel for the assessee submitted that a survey u/s 133A was conducted on the assessee on 06.03.2024 during which various incriminating documents and information was gathered and the Ld. Pr.CIT(Central) held that the same indicated the activities carried out by the assessee were not genuine and/or not being carried out in accordance with the objects of the assessee for which it was granted the registration. Subsequently, it has been mentioned by the Ld. Pr. CIT(C) that the ITO (E), Ward 2, Pune has submitted a proposal to the CIT(E), Pune vide letter dated 26.08.2024 for cancellation of the registration which was duly endorsed by Addl. CIT(E), Pune vide letter 28.08.2024. Subsequently, upon centralisation of the case to the charge of Ld. DCIT, Central Circle 2(2), Pune, the proposal for cancellation was transferred to the office of Ld. Pr. CIT(C), Pune by Ld. CIT(E), Pune vide letter dated 31.12.2024. The Ld. Pr. CIT(C) issued show cause notices on 10.02.2025 and 13.08.2025 and an order was passed on 29.09.2025 cancelling the registration.

41. The Ld. Counsel for the assessee referring to provisions of sub-section (5) of section 12AB drew the attention of the Bench to the same and submitted that no order cancelling the registration shall be passed after the expiry of 6 months calculated from the end of the quarter in which the first notice is issued by the Principal Commissioner calling for document or information or for making any enquiry under clause (i) of sub-section (4).

42. Referring to clause (i) of sub-section (4) of section 12AB he submitted that as per the said provision the Principal Commissioner shall call for such documents or information from the Trust or Institution or make such enquiry as he thinks necessary in order to satisfy himself about the occurrence or otherwise of any specified violation.

43. He submitted that when survey was conducted on the assessee on 06.03.2024 it is logical that there would be some reason with the department for conducting the survey. Further, the survey action was conducted by the ITO(E), Ward 2, Pune which otherwise means that the Ld. CIT(E) has given the approval to conduct the survey. He submitted that the purpose of survey would be to make enquiry with regard to various issues. Referring to the order passed by the Ld. Pr. CIT(C) he submitted that the order mentions instances of specified violations noticed during the course of the survey action. Therefore, once the department finds out the instances of alleged specified violation in the survey proceedings, the time limit of 6 months from the end of the quarter should be considered from the date of conducting the survey action. Since the survey action u/s 133A was conducted in the instant case on 06.03.2024 therefore the order cancelling the registration ought to have been passed within a period of 6 months from 31.03.2024 which works out to 30.09.2024. However, the order cancelling the registration has been passed on 29.09.2025, therefore, the same is clearly barred by limitation.

44. Without prejudice to the above, he submitted that the Assessing Officer had also submitted a proposal for cancelling the registration on 26.08.2024 which was duly endorsed by Ld. Addl. CIT(E) on 28.08.2024. He submitted that no action was taken by the Ld. CIT(E) and on 31.12.2024 the case was transferred to the office of Ld. Pr. CIT(C). He submitted that the proposal for cancellation was given on 26.08.2024 and the first show cause notice was issued to the assessee by the Ld. Pr. CIT(C) on 10.02.2025 which is after a period of 5 months. No reason has been given for the delay in the proceedings for cancellation of the registration when the AO had written a letter on 26.08.2024 proposing for cancelling the registration. He accordingly submitted that once the proposal was already sent for cancelling the registration on 26.08.2024, the period of 6 months ought to have been calculated from 30.09.2024 which works out to 31.03.2025. Since the order cancelling the registration has been passed on 29.09.2025, therefore, the order passed by the Ld. Pr. CIT(C) is barred by limitation.

45. The Ld. CIT-DR on the other hand referring to the provisions of section 12AB(5) submitted that a perusal of the same makes it crystal clear that a very specific limitation has been provided in the Act itself for passing of the cancellation order u/s 12AB(4). He submitted that the sub-section states that the order of cancellation should be passed before the expiry of a period of six months calculated from the end of the quarter in which the first notice u/s 12AB(4)(i) is issued. Referring to the chronology of dates he submitted that the time barring date for passing the order was 30.09.2025 and the order u/s 12AB(4) cancelling the registration was passed on 29.09.2025. The assessee has not disputed the dates or service of notice. Thus, the order passed by the Ld. Pr.CIT(C), Pune was well within the time allowed by the section 12AB(5).

46. So far as the argument of the Ld. Counsel for the assessee that the action of survey u/s 133A or the date of proposal sent by the CIT (Exemption), Pune for cancellation (i.e. 28.08.2024) should be considered as the date for the notice u/s 12AB(4)(i) is concerned, he drew the attention of the Bench to the provisions of section 12AB(5) and submitted that there is no ambiguity regarding trigger for the limitation period given in section 12AB(5). It is the first notice sent by the PCIT/CIT under 12AB(4)(i). He submitted that the date of survey u/s 133A cannot be substituted in place for notice u/s 12AB(4)(i) for deciding the limitation period prescribed in section 12AB(5). He submitted that survey u/s 133A is placed in chapter XIII related to Income tax Authorities whereas section 11, 12 and 13 of the Act for trusts etc is a self-contained separate code in itself. He submitted that the main intention behind survey u/s 133A is information gathering and operates in entirely different domain as investigative tool. It is not an adjudicatory proceeding in itself. He submitted that the provisions u/s 12AB relating to powers of PCIT/CIT to grant or cancel registration are quasi-judicial proceedings. Thus, a survey under Section 133A is conducted by an Income-tax Authority (often an ITO or ACIT) to verify books of accounts whereas a cancellation proceeding under Section 12AB (4) is conducted by a Principal Commissioner or Commissioner specifically to adjudicate the trust’s registration status. The two authorities are different and their mandates are governed by different chapters of the Act. He accordingly submitted that since the order u/s 12AB(4) dated 29.09.2025 is within the limitation period as prescribed u/s 12AB(5), therefore, the grounds raised by the assessee be dismissed.

47. We have heard the rival arguments made by both the sides, perused the order of the Ld. Pr.CIT(C) and the paper book filed on behalf of the assessee. It is an admitted fact that the Ld. Pr.CIT(C) issued the first show cause notice dated 10.02.2025 and thereafter another notice on 13.08.2025 asking the assessee to submit its explanation as to why the registration granted u/s 12AB dated 21.06.2016 (applicable up to assessment year 2021-22) should not be cancelled and also the registration granted u/s 12AB(4)(i) r.w.s. 12AB applicable for assessment years 2022-23 to 2026-27 should not be cancelled. A perusal of provisions of section 12AB(5) clearly provides the limitation period for passing of an order u/s 12AB(4) according to which the order of cancellation should be passed before the expiry of a period of six months calculated from the end of the relevant quarter in which the first notice u/s 12AB(4)(i) is issued. Since the order in the instant case cancelling the registration has been passed by the Ld. Pr.CIT(C) on 29.09.2025 which is prior to the limitation period of 30.09.2025 therefore, such order is within the time prescribed u/s 12AB(5). We find merit in the argument of the Ld. CIT- DR that the date of survey u/s 133A cannot be substituted in place for notice u/s 12AB(4)(i) for deciding the limitation period prescribed in section 12AB(5). The other argument of the Ld. Counsel for the assessee that since the CIT(E) has given the approval to conduct survey which means the conducting of an enquiry about the cases or otherwise of any specific violation committed by the assessee company and therefore, the period of six months should be calculated from the quarter ending March, 2024 and the order should have been passed within a period of six months from the quarter ending March, 2024 is incorrect. Since in the instant case the Ld. Pr.CIT(C) has issued the first show cause notice on 10.02.2025, therefore the six months period shall be calculated from the end of the quarter ending March, 2025. Since the order cancelling registration has been passed on 29.09.2025, therefore, the same is not barred by limitation. Accordingly, the ground of appeal No.1 by the assessee is dismissed.

48. Grounds of appeal No.2 and 3 by the assessee relate to the order passed by the Ld. PCIT as without jurisdiction.

49. The Ld. Counsel for the assessee submitted that the proposal for cancellation was submitted by the ITO(E), Ward 2, Pune to the CIT(E) vide letter dated 26.08.2024. Thereafter, the CIT(E) transferred the proposal for cancellation to the Ld. Pr. CIT(C) vide letter 31.03.2024. Referring to the CBDT notification dated 22.10.2014 he submitted that the competent authority for granting and cancelling registration was the CIT(E), Pune. Referring to the provisions of section 127(2) he submitted that the assessment jurisdiction was transferred from Exemption to Central Circle. However, the same did not confer or transfer registration / approval functions as well as cancellation of registration. He submitted that as per the transfer order passed u/s 127, the case has been transferred from the ITO(E), Ward 2, Pune to the DCIT, Central Circle 2(2), Pune. He submitted that the jurisdiction over the assessee for granting registration u/s 12AB or cancellation of the same cannot be transferred by the CIT(E), Pune u/s 127(2) of the Act. The power to transfer jurisdiction from CIT(E) to the Ld. Pr.CIT(C), Pune is only with CBDT. Therefore, the Ld. Pr. CIT(C) cannot assume charge to decide the cancellation of registration without an order being passed by the CBDT transferring the case.

50. Referring to page 41 of the Paper Book, he drew the attention of the Bench to the letter for transfer of proposal for cancellation wherein there is no reference of any order passed by the CBDT. He accordingly submitted that the order passed by the Ld. Pr.CIT(C) cancelling the registration is invalid in law since he had no jurisdiction to cancel the registration granted to the assessee company. For the above proposition, he relied on the decision of the Delhi Bench of the Tribunal in the case of Aggarwal Vidya Pracharni Sabha v/s. Principal Commissioner of Income Tax reported in 228 TTJ 137 (Del) and the decision of Dehradun Circuit Bench of the Tribunal in the case of Sushila Devi Centre for Professional Studies Research vs. PCIT reported in 179 taxmann.com 610 (Dehradun). He also relied on the following decisions:

a) Arya Samaj Model Town vs. PCIT vide ITA No.4805/DEL/2024 order dated 04.06.2025

b) Meenakshi Foundation vs. PCIT vide ITA No.3952/DEL/2024 order dated 23.05.2025

c) Lakshmi Chand Charitable Society vs. PCIT vide ITA No.1803/Del/2024 order dated 22.08.2024

d) Richmond Educational Society vs. DCIT vide ITA No.4779/Del/2025 order dated 11.03.2026

e) Sushila Devi Centre for Professional Studies 7 Research vs PCIT (Central) reported in 179 com610

51. The Ld. DR on the other hand submitted that the contention of the assessee that the Ld. Pr.CIT(C) has no jurisdiction to cancel the registration granted to the assessee company u/s 12AA and u/s 12AB, which is vested with the Principal Commissioner/Commissioner of Income Tax (Exemption) vide CBDT Notification, is incorrect and based on partial reading of and exclusive reliance on only one notification of CBDT i.e. CBDT notification No.52/2014 dated 22.10.2014. He submitted that in order to get the complete picture we need to have conjointly read three CBDT Notifications issued under section 120 of the Act in respect of the jurisdiction of the income tax authorities and relevant provisions of the Act, particularly sections 120 and 127 of the Income Tax Act should be read conjointly. He drew the attention of the Bench to the following CBDT Notifications:

| Notifications | Subject | Date | |

| 1 | CBDT No.52/2014* | Jurisdiction of CIT (Exemptions) | 22.10.2014 |

| 2 | CBDT No.50/2014 | Jurisdiction of PCIT | 22.10.2014 |

| 3 | CBDT No.70/2014 | Jurisdiction of PCIT (Central) |

Note * – (along with Corrigendum Notifiation No.65/2014 dated 13.11.2014)

52. He submitted that the CBDT notification explains the jurisdiction of CIT(Exemptions) all over India. As per the CBDT Notification No.52/2014 (Annexure-1), Commissioner of Income-tax (Exemption), Pune exercises jurisdiction over all cases of persons in the territorial area of state of Maharashtra excluding Mumbai & Navi Mumbai claiming exemption under section 10,11, 12 13A & 13B of the Income-tax Act, 1961 and assessed or assessable by an Income-tax authority at serial numbers 225 to 227 and 236 to 241 (to be read as 236 to 250 as per Corrigendum Notification No.65/2014 dated 13.11.2014) specified in the CBDT No.50/2014 (Annexure-2) dated the 22nd October, 2014. The Income-tax authorities at serial numbers 225 to 227 and 236 to 250 are as under:

| 225 | PCIT/CIT, Nagpur-1 | 239 | PCIT/CIT, Pune-4 | 245 | PCIT/CIT, Thane-2 |

| 226 | PCIT/CIT, Nagpur-2 | 240 | PCIT/CIT, Pune-5 | 246 | PCIT/CIT, Thane-3 |

| 227 | PCIT/CIT, Nagpur-3 | 241 | PCIT/CIT, Pune-6 | 247 | PCIT/CIT, Nashik-

1 |

| 236 | PCIT/CIT, Pune-1 |

242 | PCIT/CIT, Kolhapur-1 | 248 | PCIT/CIT, Nashik-

2 |

| 237 | PCIT/CIT, Pune-2 |

243 | PCIT/CIT, Kolhapur-2 | 249 | PCIT/CIT, Aurangabad-1 |

| 238 | PCIT/CIT, Pune-3 |

244 | PCIT/CIT, Thane-1 | 250 | PCIT/CIT, Aurangabad-1 |

53. Thus, after conjoint reading of CBDT Notification No.52/2014 and Notification No.50/2014, the jurisdiction of CIT(Exemption), Pune can be read in three steps-

a. Jurisdiction over all cases of persons in the territorial area of state of Maharashtra excluding Mumbai & Navi Mumbai

b. Who are claiming exemption under section 10,11, 12 13A & 13B of the Income-tax Act, 1961.

c. Who are assessed or assessable by specified PCsIT notified as S.No.225 to 227 and S.No.236 to 250 in CBDT No.50/2014.

54. Thus, the three aspects of CIT(Exemptions) jurisdiction are- territory wise, claim of exemption-wise and specified PCIT-wise. A person who fulfils all these conditions will only fall under the jurisdiction of CIT(Exemptions).

55. He submitted that the jurisdiction of Principal Commissioners of Income-tax (Central) have been notified by CBDT Notification No. 70/2014 dated 13.11.2014 (Annexure-3). As per clause (b) of the notification, the Principal Commissioners/ Commissioners of Income-tax (Central) or Joint Commissioners of Income-tax subordinate to them, shall exercise powers and perform the functions as stipulated in the Income-tax Act, 1961 in respect of such cases or classes of cases or such persons or classes of persons, assigned to Assessing Officers subordinate to them, under section 127 of the said Act, from the date of publication of the notification. Therefore, once a case has been transferred by order u/s 127 (in common parlance “Centralized”) with the AO of the Central Circle subordinate to the PCIT(Central), then the PCIT(Central) shall have jurisdiction over that case.

56. The Ld. CIT-DR submitted that once a case is transferred u/s 127 to the AO subordinate to PCIT(C), then he shall exercise powers and perform the functions as stipulated in the Income-tax Act, 1961 in respect of such cases. Since the case of the assessee was transferred from ITO (Exemptions), Ward-2, Pune to DCIT, Central Circle-2(2), Pune vide order u/s 127 dated 19.1.2024 who is subordinate to PCIT, (Central), Pune, therefore, in view of CBDT notification the PCIT(C) shall exercise powers and perform the functions as stipulated in the Income-tax Act, 1961 in respect of such cases which will include power to cancel registration under section 12AB. Hence, the contention of the assessee that the Ld. Pr.CIT(C), Pune does not have power to cancel registration is without appreciating the correct legal position on this issue.

57. He submitted that the CIT(Exemptions), Pune have jurisdiction only in cases in the territorial area of Maharashtra excluding Mumbai & Navi Mumbai claiming exemption under section 10,11, 12 13A & 13B of the Income-tax Act, 1961 and assessed or assessable by PCsIT specified in CBDT Notification No.52/2014. The Pr.CIT (Central), Pune is not listed in in CBDT Notification No.52/2014. Hence, those cases, wherein PCIT, (Central), Pune has jurisdiction, are outside the jurisdiction of CIT(Exemption), Pune. Therefore, in the case of the assessee, which is under the jurisdiction of PCIT(Central), Pune, the CIT(Exemption), Pune has no powers of cancellation of registration and that power vests with PCIT(C), Pune.

58. So far as the various decisions relied on by the Ld. Counsel for the assessee are concerned, he submitted that in all these cases relied on by the Ld. Counsel for the assessee only one CBDT Notification No.52/2014 has been relied upon. Since the Revenue failed to bring to notice the subsequent notifications, therefore, by considering only one Notification the order could not have been held to be without jurisdiction.

59. Referring to the decision of the Delhi Bench of the Tribunal in the case of Legal Initiative for Forest and Environment (LIFE Trust) vs. PCIT vide SA No.129/DEL/2024 dated 09.08.2024, he submitted that the Tribunal has considered the CBDT Notification No.70/2014 and thereafter various other notifications and decided the issue in favour of the Revenue. Similar view has been taken by the Delhi Bench of the Tribunal in the case of Advantage India vs. PCIT reported in (2025) 178 com605 (Delhi-Trib.). He accordingly submitted that the grounds raised by the assessee challenging the jurisdiction of the Ld. Pr.CIT(C) be dismissed.

60. We have heard the rival arguments made by both the sides, perused the order of the Ld. Pr.CIT(C) and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. It is the contention of the Ld. Counsel for the assessee that the powers of granting and cancellation of registration under section 12AB(4) of the Act is exclusively vested with CIT(Exemption) as per CBDT Notification and therefore, the order passed u/s 12AA(3) and 12AA(4) and u/s 12AB(4) by the Ld. Pr.CIT(C) is null and void. We do not find any merit in the above argument of the Ld. Counsel for the assessee. We find merit in the argument of the Ld. CIT-DR that the contention of the assessee is based on partial reading of and exclusive reliance on only one notification of CBDT i.e. CBDT notification No.52/2014 dated 22.10.2014. However, the CBDT subsequently has issued two other notifications i.e. CBDT Notification No.50/2014 dated 22.10.2014 giving jurisdiction to the Pr.CIT(C) and the CBDT Notification No.70/2014 which gives jurisdiction to the Ld. Pr.CIT(C) all over India. As per the CBDT Notification No.52/2014, the Commissioner of Income-tax (Exemption), Pune exercises jurisdiction over all cases of persons in the territorial area of state of Maharashtra excluding Mumbai & Navi Mumbai claiming exemption under section 10, 11, 12, 13A & 13B of the Income-tax Act, 1961 and assessed or assessable by an Income-tax authority at serial numbers 225 to 227 and 236 to 241 (to be read as 236 to 250 as per Corrigendum Notification No.65/2014 dated 13.11.2014) specified in the CBDT No.50/2014 (Annexure-2) dated the 22.10.2014. Subsequently the CBDT has also issued another notification No.70/2014. A conjoint reading of these three notifications of CBDT make it abundantly clear that the CIT(Exemption), Pune does not exercise any jurisdiction in respect of the persons claiming exemption under section 10, 11, 12 13A & 13B of the Act which have been assigned to the Assessing Officers subordinate to Principal Commissioner of Income-tax (Central), Pune under section 127 of the said Act. Further, Notification No. 52 issued by the CBDT u/s 120(1) and 120(2) of the Act only authorizes the Commissioners of Income Tax (Exemption) to exercise and perform all the functions in respect of cases or classes of cases specified therein. But this notification nowhere provides that power to grant/refuse the registration or cancel the registration u/s 12AA shall also be exclusively vested in the Commissioners of Income Tax (Exemption) only and no other Commissioner or Pr. Commissioner can exercise such power. Power to grant/refuse the registration or cancel the registration u/s 12AB shall be governed by the provisions of the Income Tax Act which specifically gives this power to Pr. Commissioner or Commissioner. Once a case is transferred u/s 127 of the Act to the Assessing Officer of the Central Circle, the Pr. CIT (Central), shall exercise all the powers and perform the functions as stipulated in the IT Act in respect of the case so assigned to Assessing Officers subordinate to him.

61. We find an identical issue had come up before the Delhi Bench of the Tribunal in the case of Advantage India vs. PCIT (supra). In that case the Tribunal has elaborately discussed various circulars / Notifications issued by CBDT and has observed as under: