Securities and Exchange Board of India (SEBI) has released a consultation paper to review the regulatory framework governing the permissible business activities for Asset Management Companies (AMCs) under Regulation 24 of the SEBI (Mutual Funds) Regulations, 1996. The objective is to seek public comments and suggestions on proposals aimed at enhancing the scope of activities AMCs can undertake.

Currently, Regulation 24 primarily restricts AMCs to managing and advising “pooled assets” that are “broad-based” (i.e., having at least 20 investors with no single investor holding over 25% of the corpus). This framework, implemented in 2011, sought to mitigate conflicts of interest arising from differential fee structures and resource diversion, issues that “Chinese Walls” were deemed insufficient to address. Representations from the Mutual Fund industry and the Association of Mutual Funds in India (AMFI) have prompted this review as an “ease of doing business” initiative.

The consultation paper proposes significant relaxations, primarily allowing AMCs to provide management and advisory services to non-broad-based pooled funds. To address potential conflicts such as differential fees, diversion of resources, contrary trade positions, front-running, and inter-business asset transfers, SEBI has proposed several safeguards. These include potential caps or ranges on fees for non-broad-based funds, restrictions on performance-linked fees, enhanced disclosure of fund performance, and rigorous monitoring by the Unit Holder Protection Committee (UHPC) and the AMC Board. Segregation of key investment personnel and a prohibition on inter-business transfer of securities on unfavourable terms are also proposed.

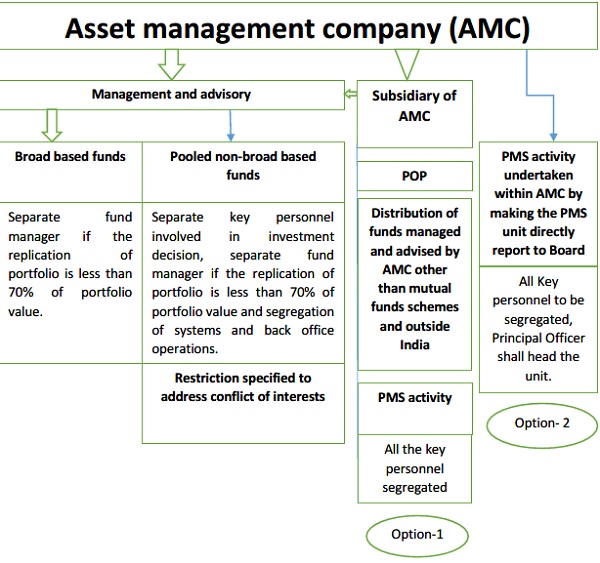

Additionally, SEBI is reviewing resource sharing between Mutual Fund operations and Portfolio Management Services (PMS) units, proposing two options: either requiring PMS activities through a distinct subsidiary with segregated key personnel or allowing PMS within the same entity but as a separate business unit with segregated key employees reporting directly to the AMC Board. The paper also explores expansion of permissible ancillary business activities, such as AMCs or their subsidiaries acting as Point of Presence (POP) for pension funds or as global distributors for funds managed or advised by the AMC outside mutual fund schemes, subject to stringent regulatory oversight and ring-fencing measures. The public now has an opportunity to provide comments on these proposals, which aim to balance business expansion with robust investor protection.

Securities and Exchange Board of India

Jul 07, 2025 | Reports : Reports for Public Comments

Click here to provide your comments

Consultation Paper On Review Of Regulatory Framework On Permissible Business Activities For Asset Management Companies (AMCS) Under Regulation 24 Of The Sebi (Mutual Funds) Regulations, 1996

1. Objective

1.1. The objective of this consultation paper is to seek comments/ suggestions from public on the proposals regarding review of regulatory framework for the business activities of an Asset Management Company (AMC) of a Mutual Fund, as currently specified under Regulation 24 of the SEBI (Mutual Funds) Regulations, 1996 (“MF Regulations”).

2. Background

2.1. Regulation 24 of the MF Regulations, inter alia, provides for the business activities that an AMC can presently undertake, subject to compliance with the conditions specified thereunder.

2.2. While Regulation 24(a) of MF Regulations restricts AMCs from acting as a trustee of any Mutual Fund, Regulation 24(b) of MF Regulations restricts AMCs from undertaking any business activity other than in the nature of management and advisory services provided to pooled assets including offshore funds, insurance funds, pension funds, provident funds, or such categories of foreign portfolio investor, as may be specified by SEBI.

2.3. The current construct of the Regulation 24 was implemented in 2011 based on the recommendation of a committee that was constituted to examine the suggestions of Association of Mutual Funds in India (AMFI) on ‘Permissible activities to be carried out by AMCs’. Prior to 2011, AMCs were permitted to undertake activities in the nature of asset management and advisory services provided the key personnel of the AMC, the systems, back office, bank and securities account were segregated activity-wise and systems existed to prohibit access to inside information of various activities (“Chinese walls”). However, the committee was of the view that actual conflict of interest may arise due to differential fee structure for Mutual Fund as a product vis-a-vis other products and therefore any consequent inequitable treatment to different sets of investors cannot be addressed through the creation of Chinese walls.

2.4. The abovementioned committee was of the view that such conflicts can be addressed by requiring AMCs to restrict themselves to management of funds of only ‘broad based’ entities with at least 20 investors; and no single investor accounting for more than 25% of the corpus of the fund. Accordingly, the term ‘pooled assets’, which were essentially broad based, was introduced under Regulation 24(b) of the MF Regulations, and it was provided that there should be no conflict of interest due to any differential fee structure charged by AMCs.

2.5. Additionally, Regulation 24 (b) of MF Regulations, inter alia, restricts the AMC, through itself or through its subsidiary to undertake certain other activities such as providing services to non-broad based funds (however such service can be provided through the portfolio management service license), distributing financial products and sharing of resources across various functions.

2.6. In this regard, from time to time representations have been received from the Mutual Fund industry and through AMFI to review Regulation 24(b) of MF Regulations.

2.7. As part of the review of Regulation 24 (b) of MF Regulations, comments were sought from the Mutual Fund industry including AMFI.

2.8. Accordingly, as an ease of doing business initiative and with the objective of enhancing the scope of permissible activities under Regulation 24(b) of MF Regulations, based on the inputs of AMFI, certain relaxations have been proposed in the current provisions under the MF Regulations. This consultation paper seeks suggestions of the public on the below mentioned proposals with respect to review of Regulation 24(b) of MF Regulations.

3. Proposals

3.1. Relaxation of broad basing requirement:

3.1.1. Current requirements:

a) Regulation 24(b) of the MF Regulations currently permits an AMC to provide management and advisory services to pooled assets which are broad based in nature.

b) Further, AMCs desirous of providing management and advisory services to non-broad based funds, need to mandatorily obtain PMS license to do the same.

3.1.2. Over the years, several AMCs have highlighted that the broad basing requirement under Regulation 24(b) has proven to be a barrier and does not provide level playing field to AMCs of MFs vis-à-vis other intermediaries engaged in providing management and advisory services to non-broad based funds. During discussions, the industry also highlighted that there are opportunities related to management and advisory of pooled assets, wherein, the domain expertise is available with the AMCs. However, restrictions due to the broad basing criteria do not permit AMCs to take up such mandates.

3.1.3. AMFI has also represented that AMCs may be facilitated to expand their business opportunities by relaxing the broad basing requirement and AMCs may be permitted to serve non-broad based funds as well.

3.1.4. In view of the same, it was decided to review and consider relaxing the broad basing requirement and permitting AMCs to serve pooled non-broad based funds as well, subject to strong governance and regulatory controls that would address any concerns related to conflicts of interest situations.

3.1.5. In case the broad basing requirement is relaxed, the following conflicts are, inter-alia, likely to arise:

a) Differential fees for pooled non-broad based funds and diversion of resources:

MF Regulations prescribe limitation on fees and expenses charged to the investors of the scheme for each scheme type (equity, debt etc.). The maximum fees including investment management and advisory is capped at 2.25% of the net assets of the scheme as governed under Regulation 52 of MF Regulations. However, AMCs for its other activities like management and advisory of pooled non-broad based fund, where a fund would consist of few large clients, may charge performance linked fees as agreed between the investor and the AMC. In view of prevailing performance linked fee structure in other fund management activities and in order to earn super normal profits from investors of pooled non-broad based funds, the fund manager may be motivated to generate higher returns for pooled non-broad based funds. Hence, the prospects of earning higher income/revenue from managing pooled non broad based funds may entice the AMC to compromise the interest of investors of broad based funds. On the flip side, conflicts may also arise when AMC charges a discounted fee from the investors of pooled non-broad based fund by utilising the resources of Mutual Fund and charging the cost of such resources to the Mutual Fund.

Further, diversion of resources in favour of pooled non-broad based fund may affect retail investors in two ways:

i. When key personnel, research capabilities, analytical resources etc. are shifted away from broad based funds to pooled non-broad based funds, it may result in Mutual Funds being left with fund managers with lack of skill and experience, potentially leading to suboptimal investment outcomes.

ii. If the costs associated with managing pooled non-broad based funds are inappropriately allocated to or borne by the mutual fund investors, the same will result in an unfair increase in the overall expenses charged to mutual fund investors.

b) Risk of contrary trade positions and front running:

Same investment team managing both broad based funds and pooled non-broad based funds may gain insights into large trades. A fund manager may buy stock for a pooled non-broad based client while simultaneously selling it in broad based fund, which may potentially manipulate prices or may place the order for pooled non-broad based funds prior to placing the order for broad based funds for the benefit of the investors of pooled non-broad based funds. This may lead to instances of front running or contrary trade positions, which puts retail investors at a disadvantage.

c) Risk of trading based on inside information of Mutual Fund operations:

While managing and advising both broad based and pooled non-broad based funds, AMCs may be inclined to favour pooled non broad based clients by allowing trades based on the inside information from Mutual Fund operations, thereby benefitting these clients at the cost of mutual fund investors.

d) Inter business transfer of assets on unfavourable terms to mutual fund investors:

AMC may transfer low quality debt assets or assets which are likely to default from the portfolio of a pooled non-broad based investor to a broad based fund. This undermines the principle of fair treatment and fiduciary duty.

3.1.6. To address the above mentioned potential conflicts that may arise in case of relaxing broad-based requirements, the following safeguards are proposed:

3.1.6.1. Differential fees for pooled non-broad based funds and diversion of resources:

a) As can be seen at para 3.1.5 (a) above, diversion of resources from broad based to pooled non-broad based funds by AMC is linked to the fee structures applied to different investor groups, which may be to the disadvantage of mutual fund investors. Hence, to address the concern relating to diversion of resources, it is proposed that AMCs may be required to ensure that the resources dedicated to pooled non-broad based funds should be proportionate to the fee earned by AMC from such funds vis-à-vis fees from investors in mutual fund schemes and that mutual fund investors are not made to bear the cost of servicing mandates for pooled non-broad based funds.

b) Further, as mentioned in para 3.1.5 (a) above, while there is potential conflict of interest if an AMC charges a higher fee from pooled non-broad based client for providing preferential services (as this may incentivize the AMC to divert resources away from broad based funds), offering discounted fees to pooled non-broad based clients by cross subsidizing the cost through mutual fund schemes also results in mutual fund investors bearing a disproportionate share of expenses. Hence, fees charged from pooled non-broad based clients may be mandated to be within a certain specified range. Further, additional monitoring measures may also be considered. Accordingly, the following measures are proposed:

i. Cap on fee differential:

A range of fees may be prescribed for AMCs to charge from their pooled non-broad based funds. There can be two approaches to deciding the range:

Approach 1: A cap and floor on the fees that can be charged by the AMCs for management and advisory to pooled non-broad based funds. A cap may be prescribed in line with the maximum TER allowed to be charged for a similar mutual fund scheme. The floor on the fees may be decided based on the existing TER of a similar scheme; OR

Approach 2: An upper limit on the maximum permissible difference between fees from similar broad based mutual fund schemes and pooled non-broad based funds (e.g. maximum x% higher or lower than the TER charged to similar mutual fund scheme).

ii. Further, to avoid any preferential treatment to pooled non-broad based funds, charging of any performance related fees by AMCs may be restricted.

iii. AMCs may be required to disclose the performance of pooled non-broad based funds vis-à-vis performance of the comparable mutual fund schemes on a half yearly basis to all investors

iv. Additional Monitoring measures:

a) AMCs providing services to pooled non-broad based funds, may be required to have a written policy which specifies the reason for any fee differential between pooled non-broad based fund and the comparable mutual fund scheme of the AMC. The difference in fees may be due to mandate complexity, customization, reporting size etc. The same may also be placed before the Board of the AMC.

b) The Unit Holder Protection Committee (UHPC) may be required to periodically review fee differentials, ensuring that deviations are justified, documented and comply with the cap/floor on fees as proposed at para 3.1.6.1 (b) (i). This would in turn ensure that no unfair advantage is being given to the investors in the pooled non-broad based funds. The findings of the UPHC may be placed before the AMC Board, Trustees and may also be required to be submitted to SEBI.

c) The basis of resource allocation by AMCs to any pooled non-broad fund, may be reviewed by their UHPC on a periodic basis.

d) The key personnel involved in investment decision-making, back office operations or fund management, including fund managers for pooled non-broad based funds may be required to be segregated. The fund manager may be common only if the investment objectives and asset allocation are same and the portfolio is replicated across all the funds managed by the fund manager. The replication of minimum 70% of portfolio value shall be considered as adequate for the purpose of said compliance, provided that AMC has in place a written policy for trade allocation and it ensures at all points of time that the fund manager shall not take directionally opposite positions in the schemes managed by him.

e) Since the same entity (AMC) shall be undertaking management and advisory services to both broad based and pooled non-broad based funds, top management functions like CEO, CFO etc. would naturally oversee the entire business operations. Further, Compliance Officer (CO) may also be permitted to be shared considering that common CO would mean centralized compliance function which ensures uniformity in policy enforcement, reduces duplication and comprehensive view of regulatory risk. Moreover, CO does not engage in investment decision making or client interaction.

3.1.6.2. Risk of contrary trade positions and front running:

a) To address the issue of front running by pooled non-broad based funds, it is proposed that the principle of fair and equitable treatment and the requirements specified in Clause 12.29 of Master Circular for Mutual Funds dated June 27, 2024, which, inter-alia, requires AMCs to put in place a written policy that clearly defines the roles and responsibilities of various teams involved in fund management, order placement, execution etc., use an automated Order Management System with clear order instructions to employees placing order on behalf of AMCs etc., may be extended to cover investors across all pooled vehicles managed by the AMC, whether broad based or pooled non-broad based funds.

b) The restrictions relating to engaging in contra trade within a period of six months from the date of purchase or sale of equity and equity related securities and the restriction on investment in thematic funds, as applicable to AMCs providing management and advisory to the FPIs based out of IFSC not falling under Clause 17.3.1. of the Master Circular dated June 27, 2024, may be made applicable to AMCs providing management and advisory services to pooled non-broad based funds.

c) Further, the framework on Institutional mechanism for prevention of potential market abuse including front-running and fraudulent transactions in securities, issued by SEBI vide circular dated August 05, 2024 already provides the broad framework to identify, monitor and address specific types of misconduct including front-running, insider trading, misuse of sensitive information etc.

3.1.6.3. Risk of trading based on inside information of Mutual Fund operations:

a) SEBI (Prohibition of Insider Trading) Regulations, 2015 (‘PIT Regulations’) would prohibit entities from acting or dealing in securities based on the Unpublished Price Sensitive Information (UPSI), which would prohibit pooled non-broad based funds from dealing in securities based on UPSI. With respect to prohibiting insider trading in the investments/redemption by pooled non-broad based funds in mutual fund units, it may be highlighted that mutual fund units have been brought under the ambit of PIT Regulations. These safeguards to an extent would deter entities from engaging in acts or deals in mutual fund units based on the UPSI.

b) Further, AMC may be required to ensure that the activity performed for pooled non-broad based funds does not emanate from any information obtained through Mutual Funds operations.

c) Additionally, it may also be specified that the information used for the advantage of pooled non-broad based fund should not put mutual fund investors at any disadvantage.

3.1.6.4. Inter business transfer of assets on unfavourable terms to mutual fund investors:

To protect the interest of the mutual funds investors and to avoid any transfer of securities to or from mutual fund scheme on unfavorable terms, at this stage it is proposed that the transfer of securities between pooled non-broad based fund and mutual fund schemes may not be allowed.

3.1.7. In addition to the above, following safeguards are proposed in case of AMCs providing management and advisory services to pooled non-broad based funds:

a) Pooled non-broad based fund, to which management and advisory service is provided by AMCs, shall be required to be appropriately regulated i.e. either domestically or in foreign jurisdictions.

b) In case of funds from foreign jurisdictions, such funds shall be required to be established in countries which are either members of Financial Action Task Force (FATF) or are signatories to IOSCO MMOU (The International Organization of Securities Commissions- Multilateral Memorandum of Understanding) and shall be required to comply with Press note 3 if the proposed investment is from any of the countries which shares a land border with India.

c) AMC or its subsidiary providing management and advisory service to pooled non-broad based funds as proposed to be allowed above shall ensure compliance with the conditions specified at points (i) to (v), (vii) and (viii) of Proviso 1 of Regulation 24(b) of MF Regulations, which, inter-alia, requires AMC to satisfy the Board that bank and securities accounts are segregated activity wise, capital adequacy requirements are met separately for each such activity, there is no material conflict of interest across the different activities, disclosures regarding absence of conflict/ presence of unavoidable conflict of interest situations, ensure fair treatment of investors across different products and independence to key personnel handling the relevant conflict of interest etc.

d) The systems, back office may be segregated activity wise and systems should exist to prohibit access to inside information.

e) AMCs shall be required to ensure that the service proposed to be provided under Regulation 24(b) of MF Regulations are regulated activities and does not lead to reputational risk which can impact the interest of mutual fund investors. Such services provided by AMC under Regulation 24(b) of MF Regulations may not be regulated under MF Regulations but shall be required to be regulated by other regulators or foreign jurisdictions or by SEBI under other SEBI Regulations (for e.g., Investment Advisers Regulations). In such cases, these services may be governed under the respective regulatory framework and AMCs shall be required to:

-

-

- take appropriate declaration/undertaking from the client that such services do not come under regulatory purview of MF Regulations.

- to make disclosure to the client that no recourse is available to them with SEBI under MF Regulations for their grievances related to such services of AMC.

-

3.1.8. Consultation/ Proposal 1:

a) Whether the proposal regarding relaxation of broad based criteria for AMCs as mentioned above is appropriate?

b) If pooled non-broad based funds are allowed to be managed by AMCs, whether there are any additional conflicts of interest that need to be considered apart from those mentioned at para 3.1.5 above?

c) Whether the proposals regarding safeguards to be imposed at paras 3.1.6 and 3.1.7 are appropriate? Whether there are any additional safeguards required to be imposed to address each of the conflicts mentioned at para 3.1.5 above?

d) As regards the conflicts relating to fee differential and diversion of resources, which of the two approaches mentioned at para 3.1.6.1 (b) (i) above would be more effective?

e) Whether there are any perceived risks associated with sharing of Compliance Officer, top management functions like CEO, CFO etc. when the AMC undertakes management and advisory services for both broad based and pooled non-broad based funds?

f) Any additional suggestion may be provided with appropriate rationale. 3.2. Resource Sharing:

3.2.1. Current requirements:

a) Regulation 24 (b) of MF Regulations, inter alia, restricts the AMC, through itself or through its subsidiary to undertake management and advisory services to non-broad based funds. However, such service can be provided through the portfolio management service license by ensuring that key personnel of the asset management company, the system, and back office, bank and securities accounts are segregated activity wise and there exist system to prohibit access to inside information of various activities.

b) Further, only fund managers are required to be separate for each separate broad based fund managed by the AMC as per the requirements specified in Proviso 1 of Regulation 24 (b) of MF Regulations. MF Regulations also mandate systems to prohibit access to inside information of various activities when AMC undertakes management and advisory services to non-broad based funds under PMS route.

3.2.2. It was represented by the AMCs that when managerial personnel of the AMC and Portfolio Management Services (PMS) are allowed to be common, the segregation of duties between PMS and MF can be done in the following manner to avoid conflicts of interest:

a) Operational Segregation: Different teams handle investments, back-office operations, and compliance for PMS and MF.

b) Chinese Walls: Different fund managers and operations team who are involved in day to day decision making to prevent information sharing between PMS and MF functions.

3.2.3. When key managerial positions are shared, including Principal Officers of PMS, the possibility of access to and thereby misuse of sensitive information cannot be ruled out and hence, the concern needs to be addressed.

3.2.4. In terms of SEBI (Portfolio Managers) Regulations, 2020, Principal Officer is defined as under:

“Principal Officer” means an employee of the portfolio manager who has been designated as such by the portfolio manager and is responsible for: -(i)the decisions made by the portfolio manager for the management or administration of portfolio of securities or the funds of the client, as the case may be; and(ii)all other operations of the portfolio manager.

3.2.5. In view of the definition of Principal Officer, Principal Officer is responsible for overall operations of the PMS and involvement of Principal Officer in the MF function may lead to conflict of interest.

3.2.6. The following two alternatives are proposed to address the issue of segregation of key employees in case AMC undertakes management and advisory services under PMS route:

a) Option 1: To ensure segregation of key employees of PMS and to prohibit access to inside information of various activities, management and advisory services undertaken by AMC as PMS may be provided through the subsidiary of the AMC with distinct key personnel. This would help mitigate cross sharing of information and bring about better governance and independent oversight into the activities of the AMC and its subsidiary. However, to reduce the research cost, it is proposed that the research personnel and resources (subscriptions, research reports etc.) may be allowed to be shared between Mutual Funds operations and PMS unit.

Implications of Option 1:

-

-

- PMS license to be obtained by the AMC’s subsidiary.

- All key personnel (including fund managers and compliance officers) engaged in the PMS business may be employed by the subsidiary and there may not be any overlapping roles with the Mutual Fund business.

- Independent governance and reporting lines have to be established within the subsidiary for the designated key personnel.

-

b) Option 2: PMS activity may continue to be allowed in the same entity. However, PMS unit may be required to operate as a distinct business unit separated through Chinese walls with all the key employees segregated as already specified in the MF Regulations. Further, the PMS unit may be required to directly report to the Board of the AMC without the involvement of the CEO, CIO, COO, CFO, etc., of the AMC.

As the overall operations are overseen by the Principal Officer of a PMS, the Principal Officer may be required to directly report to the Board of the AMC. However, to reduce the research cost, it is proposed that the research personnel and resources (subscriptions, research reports etc.) may be allowed to be shared between Mutual Funds operations and PMS unit.

Implications of Option 2:

-

-

- All key personnel (including fund managers and compliance officers) for PMS may be segregated from those handling Mutual Fund operations, with no overlap in roles or reporting lines.

- A dedicated Principal Officer for PMS would be required to be appointed within the AMC who will be responsible exclusively for the PMS business.

- The Principal Officer may be required to report directly to the Board of the AMC, to ensure autonomy and independence in decision making.

-

3.2.7. Consultation/ Proposal 2:

a) Whether the proposals at para 3.2.6 above are appropriate?

b) Whether any additional safeguards are required to be put in place to enhance the effectiveness of above proposals?

c) Whether there are any perceived risks associated with sharing of research personnel and resources (subscriptions, research reports etc.) between Mutual Funds operations and PMS unit?

d) Whether the compliance officer should be allowed to be common in MF and PMS function?

e) Any additional suggestion may be provided with appropriate rationale. 3.3. Expansion of permissible business activities:

3.3.1. Presently AMCs and its subsidiaries are only allowed to provide services which are in the nature of management and advisory of pooled funds. AMFI has represented that AMCs and its subsidiaries may be permitted to undertake business activities ancillary to its core fund management operations, such as distribution and marketing services etc., which are related to fund management.

3.3.2. Two specific ancillary activities proposed by AMFI are –

a) AMC/ its subsidiary to act as Point of Presence (POP) for pension funds as per the regulatory framework specified by Pension Fund Regulatory and Development Authority (PFRDA); and

b) AMC/ its subsidiary to act as global distributor to funds which are managed and/or advised by the AMC or its subsidiary.

3.3.3. With respect to the request of AMC/ its subsidiary to act as POP, presently subsidiaries of the AMCs are allowed to provide such POP services as pension fund manager under direct plan to the investor i.e., without receiving directly or indirectly any commission or fees from the investor or the pension fund.

3.3.4. Considering that the activity of pension fund management and POP services comes under the ambit of PFRDA and any service provided by AMCs or its subsidiaries w.r.t. pension funds are governed by the regulatory framework specified by PFRDA, subsidiaries of the AMCs which are registered as pension funds may be allowed to provide POP service and receive the compensation allowed by PFRDA for such services. However, the AMC may be required to ensure that the interest of the mutual fund investors is protected and not compromised while providing such services.

3.3.5. With respect to request of AMC/ its subsidiary to act as global distributor of funds, presently, AMCs are allowed to market or sell only direct plans of the mutual funds scheme managed by them. For marketing and selling direct plans of the mutual funds schemes, AMCs may continue to be allowed to register as distributor through overseas subsidiary. However, AMCs may be required to ensure that no commission or fees is received for such distribution of direct plans of mutual funds schemes of the AMCs.

3.3.6. With respect to the funds managed and advised by AMC other than mutual funds schemes and outside India, it is proposed that AMCs may be allowed to distribute funds managed and advised by the AMCs other than mutual fund schemes through its subsidiary, provided such distribution activities and fund management activities are regulated by a foreign regulator/jurisdiction and is in compliance with the regulatory framework specified by such foreign regulator/jurisdiction.

3.3.7. Further, these ancillary activities must fall within the regulatory oversight of any domestic regulator or foreign regulator/jurisdictions, ensuring that all such operations remain within the ambit of a recognized regulatory framework.

3.3.8. In case of services to foreign entities in foreign jurisdictions, the same should be undertaken in countries which are either members of Financial Action Task Force (FATF) or are signatories to IOSCO MMOU (The International Organization of Securities Commissions- Multilateral Memorandum of Understanding), and complies with Press note 3 if the proposed investment is from any of the countries which shares a land border with India.

3.3.9. Further, both the proposed activities i.e. POP and global distribution need to be ring fenced by the AMC by undertaking these activities through subsidiaries of the AMCs. The subsidiaries of the AMCs undertaking such ancillary business activities may be required to ensure compliance with the conditions specified in Proviso 1 as mentioned at para 3.1.7(c) and Proviso 2 of Regulation 24(b) of MF Regulations on the requirement of segregation of bank and securities account including capital adequacy, etc., as applicable.

3.3.10. Consultation/ Proposal 3:

a) Whether the proposals at para 3.3.4 to 3.3.9 above are appropriate?

b) Whether there are any additional safeguards that need to be imposed to ensure that such ancillary activities do not create conflict of interest with the core fund management responsibilities of the AMC?

c) Whether any additional compliance/ disclosure measures should be considered for the subsidiary when acting as POP/ distributing funds managed and advised by AMC other than mutual fund schemes, to ensure transparency and accountability in the operations of such subsidiaries?

d) Any additional suggestion may be provided with appropriate rationale

3.4. Other proposals:

3.4.1. Under the framework as proposed above, AMC may provide management and advisory services to pooled non-broad based funds irrespective of the route through which the foreign entity chooses to invest in India.

3.4.2. With respect to management and advisory services provided by AMCs or its subsidiaries, to entities operating through International Financial Services Centres (IFSC), which are investing in India through FPI route, specific provisions are specified in Clause 17.3 of the Master Circular dated June 27, 2024.

3.4.3. With respect to management and advisory services provided by AMCs or its subsidiaries, to entities operating through IFSC, which are investing in India through other than FPI route, specific provisions are not prescribed.

3.4.4. It is observed that the investments through Foreign Direct Investment (FDI) and Foreign Venture Capital Investor (FVCI) route shall be majorly in unlisted securities. Therefore, the restrictions under Clause 17.3.3 of the Master Circular dated June 27, 2024 on contra trade and investment in thematic schemes may not be applicable for such entities.

3.4.5. Accordingly, it is proposed that the relevant conditions as applicable for broad based funds and as proposed for pooled non-broad based funds may also be made applicable for such entities investing in India through other than FPI route from IFSC. All other requirements as specified by Government of India, RBI, SEBI or any other authority with respect to FDI and FVCI, issued from time to time, will be applicable to such entities.

3.4.6. Further, since AMC and its subsidiaries are proposed to be allowed to provide management and advisory services to pooled non-broad based funds, it is proposed that the framework specified under Clause 17.3 of the Master Circular dated June 27, 2024, for AMC or its subsidiary managing and advising FPIs operating out of IFSC, may be aligned with the broad framework proposed for managing and advising the broad based and pooled non-broad based funds. A visual representation of the proposed broad framework is placed at Annexure A.

3.4.7. Consultation/ Proposal 4:

a) Whether the proposal at para 3.4.5 and 3.4.6 above are appropriate?

b) Whether there are any specific types of entities or investment strategies (within the FDI/ FVCI framework) that should be explicitly excluded or subject to enhanced scrutiny under this proposal?

c) Whether there are any additional safeguards or disclosure requirements to be imposed on the AMC when advising on investments in unlisted securities?

d) Any additional suggestions may be provided with appropriate rationale.

4. Public Comments on this Consultation Paper

4.1. Public comments are invited for the proposals at paragraph 3.1, 3.2, 3.3 and 3.4 above. The comments/ suggestions should be submitted by the following modes latest by July 28, 2025-

4.1.1. Preferably through Online web-based form

The comments may be submitted through the following link: https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentActio n.do?doPublicComments=yes

4.1.2. Through Email

In case of any technical issue in submitting your comment through web based public comments form, you may send an email to peterm@sebi.gov.in or tarung@sebi.gov.in or gopikaj@sebi.gov.in with a subject: “Consultation paper on review of restrictions on business activities of Asset Management Companies (AMCs) under Regulation 24(b) of SEBI (Mutual Funds) Regulations, 1996 (“MF Regulations”)”

Issued on: July 07, 2025

(End of Consultation Paper)

Annexure A