Summary:India introduced the Electronic Gold Receipt (EGR) framework through SEBI to create a regulated, exchange-traded security backed one-to-one by physical gold stored in registered vaults, addressing limitations of physical gold, Gold ETFs, Sovereign Gold Bonds, and digital gold. Recognised as a security under the Securities Contracts (Regulation) Act, EGRs allow investors to deposit physical gold, receive demat receipts, trade them on stock exchanges, and redeem them for physical gold through SEBI-registered Vault Managers. The framework aims to improve price discovery, transparency, standardisation, and integration of physical gold with financial markets, while encouraging organised gold trading and recycling. Despite its robust regulatory design, adoption remains limited due to factors such as inadequate vault infrastructure, demat account requirements, limited liquidity, and competition from Gold ETFs. The article concludes that the long-term success of EGRs depends on expanding the ecosystem through greater institutional participation, wider vault networks, market-making mechanisms, and enhanced retail accessibility rather than further regulatory redesign.

1. INTRODUCTION

India is among the world’s largest consumers of gold, with jewellery and investment accounting for a significant share of domestic demand. However, existing investment avenues each carried material limitations: physical gold suffered from purity uncertainty and fragmented pricing; Gold ETFs lacked direct physical redeemability; Sovereign Gold Bonds (“SGBs”) offered no physical backing; and digital gold platforms operated outside SEBI’s regulatory perimeter.

Against this backdrop, SEBI introduced the framework for operationalizing the Gold Exchange in India vide SEBI Circular no. SEBI/HO/CDMRD/DMP/CIR/P/2022/07 dated January 10, 2022 — a regulated, exchange-traded security backed one-to-one by physical gold held in registered vaults. The policy objectives were explicit: infuse transparency in gold transactions and over a period of time enable India to emerge as a global price setter for the commodity.

2. WHAT IS AN ELECTRONIC GOLD RECEIPT?

2.1 Legal Character

Electronic Gold Receipts are ‘securities’ as notified under Section 2(h)(iia) of the Securities Contracts (Regulation) Act, 1956 (“SCRA”), vide Government of India Gazette Notification S.O. 5401(E) dated December 24, 2021. This brings EGRs within SEBI’s full regulatory jurisdiction.

EGR means an electronic receipt issued on the basis of deposit of underlying physical gold in accordance with the regulations made by the SEBI under section 31 of the SCRA.

Each EGR represents ownership of physical gold which complies with either LBMA Good Delivery standard gold or with the India Good Delivery Standard, held with a SEBI-registered Vault Manager.

EGR’s created by the Vault Manager/s are not linked with the unique bar reference number of the physical gold, i.e., gold deposited against EGR1 can be delivered against conversion of EGR2 into gold (for the same contract specifications). Further, the physical gold deposited at one location of a Vault Manager, can be withdrawn from different location of same or different Vault Manager (depending on the availability of physical gold).

2.2 EGR vs Other Gold Products — Comparative Matrix

| Parameter | EGR | Physical Gold | Gold ETF | Digital Gold |

| Legal Form | SCRA, Sec 2(h) | Commodity / tangible asset | Mutual Fund Unit | Contractual claim (unregulated) |

| Physical Backing | Direct — named vault, named gold | N/A — the investor holds the commodity directly | Pool held by custodian for AMC | Provider claim; no independent verification |

| Relevant Law | SEBI (Vault Managers) Regulations, 2021 | BIS (hallmarking only) | SEBI (Mutual Funds) Regulations, 2026 | Outside SEBI perimeter |

| Demat Form | Yes | No | Yes (MF units) | No |

| Physical Redemption | Yes — via Vault Manager | N/A | Not at retail level; cash NAV | Per provider T&Cs; unregulated |

| Exchange Traded | Yes (BSE / NSE) | No | Yes (ETF on exchange) | No |

| Price Discovery | Spot Price Polling Mechanism | Fragmented / dealer-quoted | NAV-based (± tracking error) | Provider-set spread |

| Counterparty Risk | Vault Manager + Exchange CC | Self / dealer | AMC + Custodian | Unregulated provider |

| Storage Cost | Storage charges | Self / bank locker | Borne by fund (in expense ratio) | Provider fee |

SGBs (discontinued fresh issuances from 2025) are excluded from the matrix as they have no physical backing and mandate cash settlement — a structurally distinct product.

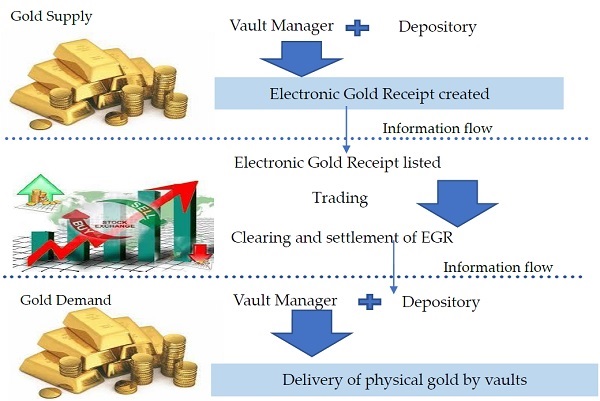

3. THE EGR LIFECYCLE

The operational framework for EGR creation, trading of EGR on stock exchanges, and conversion of EGR into physical gold, is governed by SEBI Master Circular SEBI/HO/MRD/MRD-PoD-1/P/CIR/2024/87 dated June 24, 2024 (“SEBI EGR Master Circular”), read with SEBI (Vault Managers) Regulations, 2021.

| Sl. No. | Stage | Process | Key Activities | Entities Involved |

| 1 | Deposit Request | Depositor initiates request through Depository interface | Depositor selects Vault Manager, recognised vault, quantity, purity, weight and authorised representative details. System generates a deposit request letter. Request remains active for 3 working days. | Beneficial Owner, Depository, Vault Manager |

| 2 | Physical Deposit & Verification | Gold is presented at recognised vault | Vault Manager verifies KYC documents, packing list, customs documents (where applicable), indemnity letter and other prescribed documents. Gold bars are weighed and matched with deposit request and packing list. | Depositor, Vault Manager |

| 3 | Acceptance of Gold | Vault Manager accepts eligible gold for deposit | Only gold received through imports or stock exchange/s accredited domestic refineries is accepted. Further, existing gold already lying in the vault that has never exited the vaulting infrastructure and meeting prescribed criteria can be considered for conversion into EGR. Vault Manager issues physical/electronic acknowledgement to depositor. | Vault Manager |

| 4 | Creation of EGR | Vault Manager creates EGR in common interface | Upon acceptance of gold, Vault Manager records prescribed details (beneficial owner, DP, vault, purity, bar number, refiner details, etc.) and creates EGR. A copy of purity certificate is also uploaded in the interface. | Vault Manager, Depository |

| 5 | Credit to Demat Account | EGR credited to beneficial owner | EGR reflects in the demat account of the beneficial owner maintained with the Depository Participant. Depository makes EGR available for trading. | Depository, Depository Participant (DP) |

| 6 | Trading on Exchange | EGR traded as a security | EGRs are traded on the EGR segment of recognised stock exchanges. Clearing Corporation settles trades by transferring EGRs and funds between market participants. | Stock Exchange, Clearing Corporation, Broker, Depository |

| 7 | Holding & Reconciliation | EGR remains backed by physical gold in vault | Vault Manager and Depositories perform continuous reconciliation between outstanding EGRs and physical gold stored in recognised vaults. | Vault Manager, Depositories |

| 8 | Redemption Request | Beneficial owner requests physical gold | EGR holder submits withdrawal request through Depository interface for conversion of EGR into physical gold. Depository forwards request to Vault Manager. | Beneficial Owner, Depository, Vault Manager |

| 9 | Extinguishment & Physical Delivery | EGR converted back into physical gold | Vault Manager delivers physical gold to beneficial owner and simultaneously extinguishes the corresponding EGR. Depository updates records and informs Stock Exchanges and Clearing Corporations. | Vault Manager, Depository, Beneficial Owner, Stock Exchange, Clearing Corporation |

Two-way convertibility—physical gold into EGRs and EGRs back into physical gold—is a fundamental feature of the EGR framework. The ability to convert EGRs into underlying physical gold helps anchor EGR prices to the value of the underlying commodity and facilitates arbitrage where pricing discrepancies arise. In the absence of a credible redemption mechanism, an exchange-traded instrument may trade at a sustained premium or discount to the value of the underlying asset.

A key differentiator between EGRs and Gold ETFs is that EGRs are designed around physical delivery and redemption of gold, whereas physical redemption is generally not available to retail investors in Gold ETFs. This feature seeks to strengthen the linkage between the traded instrument and the underlying physical gold ecosystem.

4. POLICY RATIONALE — PROBLEMS THE FRAMEWORK SOUGHT TO SOLVE

| Problem Identified | Supporting Fact / Observation | How the EGR Framework Responds |

| India was a major gold consumer but not an influential participant in global price discovery | India consumes approximately 800–900 tonnes of gold annually and is one of the world’s largest gold markets. Despite this, India has historically remained a price taker in global gold markets. | Establishes a regulated spot gold market with transparent exchange-based trading and price discovery. |

| Lack of transparent and efficient domestic spot price discovery | Physical gold trading occurs through a fragmented network of jewellers, bullion dealers and intermediaries, resulting in multiple reference prices across markets. | Introduces exchange-traded EGRs with centralised order matching and publicly observable prices using the ‘spot price polling mechanism’ |

| Absence of a comprehensive and regulated gold market ecosystem | Prior to EGRs, India lacked an integrated framework combining trading, vaulting, settlement, assaying and delivery under a single regulatory architecture. | Creates a unified ecosystem involving Stock Exchanges, Depositories, Clearing Corporations and SEBI-regulated Vault Managers. |

| Need for greater assurance regarding quality and standardisation of gold | Variations in purity standards and market practices can create information asymmetry and increase transaction costs. | Permits creation of EGRs only against gold meeting prescribed standards and held within regulated vault infrastructure. |

| Limited integration of physical gold with financial markets | Physical gold largely remained outside mainstream market infrastructure and financial market mechanisms. | Converts physical gold into a dematerialised and exchange-traded security capable of being held and transferred through the depository system. |

| Need to encourage broader market participation | Traditional bullion markets may be less accessible to certain categories of investors. | Provides a standardised exchange platform accessible to retail investors, jewellers, bullion dealers, banks and other eligible participants. |

| Low levels of organised gold recycling | A significant portion of gold remains idle or circulates outside formal market channels. | Creates a regulated framework through which eligible physical gold can enter the formal market ecosystem and be traded efficiently. |

| Logistical inefficiencies in physical gold ownership and transfer | Physical movement, storage and verification of gold can involve significant cost, risk and operational complexity. | Introduces fungible, dematerialised EGRs supported by regulated vaulting and delivery infrastructure. |

5. ADOPTION AND MARKET RESPONSE

BSE launched the EGR trading segment in October 2022. NSE’s EGR segment was also launched this year in May 2026 under SEBI’s framework. As of the day of writing this article, there are three SEBI registered Vault Managers namely Brink’s India Private Limited (Mumbai), Malca-Amit JK Logistics Private Limited (Mumbai) and Sequels Logistics Private Limited (Ahmedabad).

Structural Adoption Barriers

| Barrier | Analysis |

| Vault infrastructure gap | Limited number of registered Vault Manager locations in the early phase restricts geographic accessibility for physical gold deposit — particularly relevant for semi-urban and rural gold holders. |

| Demat account requirement | EGR participation requires a demat account and exchange access. While active demat accounts approached ~228 million (CDSL+NSDL), this represents a fraction of India’s gold-buying population. |

| Thin market circularity | Liquidity attracts participants; participants create liquidity. Absent a market-maker or Authorised Participant (AP) framework, EGRs face a classic thin-market problem. |

| Competition from Gold ETFs | Gold ETFs have an established investor base, AMC distribution networks, no direct vault charges, and decades of regulatory familiarity. EGR offers features not available in Gold ETFs, particularly retail-level physical redemption, but currently faces accessibility and liquidity challenges. |

6. GLOBAL COMPARISON

| Parameter |

India (EGR) |

USA (GLD/IAU) | China (SGE) | UK (ETC) |

Turkey (BIST) |

| Exchange Traded |

Yes (BSE, NSE) |

Yes (NYSE Arca) | Yes (SGE) | Yes (LSE) |

Yes (Borsa Istanbul) |

| Physical Backing |

Direct — vault-held gold |

Yes — HSBC vaults, London | Yes — SGE member vaults | Yes — custodian-held |

Yes |

| Physical Redemption |

Yes — retail accessible |

APs only (institutional) | Yes — direct delivery | Institutional primarily |

Yes |

| Market Maturity |

Nascent (est. 2021) |

High (est. 2004) | Very High (est. 2002) | High (est. 2003) |

High |

| Retail Participation |

Limited (early stage) |

Primarily institutional | High | Primarily institutional |

High |

| Regulatory Body |

SEBI |

SEC / CFTC | PBoC / SGE Rules | FCA |

BRSA / CMB |

| Liquidity |

Limited |

Very high (billions USD/day) | Very high | High |

Moderate–High |

| Unique Structural Feature |

Two-way retail redemption |

AP creation/redemption model | Mandatory gold routing via SGE | ETC (non-fund) structure |

Bank-integrated gold deposits |

Key Lessons from Global Experience

| Lesson | Analysis and Applicability to India |

| Institutional liquidity anchors (US) | GLD achieved scale because large institutional arbitrageurs (AP mechanism) kept prices efficient and provided depth. EGRs lack a comparable institutional participation pathway. Designating bullion dealers or banks as EGR market makers could be transformative. |

| Bank-channel accessibility (Turkey) | Turkey’s gold bank deposits achieved mass retail adoption by integrating gold investment into existing banking relationships — no exchange account required. India could explore bank intermediation in EGR creation/redemption without dismantling the SEBI framework. |

| Mandatory routing (China / SGE) | SGE achieved market dominance partly through regulatory mandate — all newly mined and imported gold is channelled through the SGE. India has not adopted this approach. Without a demand anchor, EGR liquidity depends entirely on voluntary adoption. |

| Infrastructure before liquidity | Both GLD and SGE were built on pre-existing institutional infrastructure (NYSE Arca listing with DTCC clearing and LBMA-standard custodianship for GLD; SGE’s established physical delivery and member vault network for the Chinese market). India is building vault infrastructure from scratch — a multi-year process that requires realistic timelines. |

The EGR framework does not appear to suffer a fundamental regulatory design failure. The constraints are (a) insufficient vault geographic coverage; (b) demat-barrier limiting addressable market; (c) absence of institutional market-making; and (d) insufficient time for network effects to develop. Awareness is a downstream symptom of these structural gaps, not the root cause.

7. THE ROAD AHEAD

| Proposed Development | Rationale / Analysis |

| Authorised Participant / Market-Maker framework | Designating bullion dealers or banks with two-way quoting obligations would address the thin-market problem — the most critical structural gap identified in this analysis. Analogous to the AP model in US ETFs. |

| Bank intermediation in EGR creation | Permitting scheduled commercial banks to accept gold deposits and facilitate EGR creation would eliminate the demat-account barrier for a significant segment of India’s gold-holding population. |

| Expansion of registered Vault Managers | Geographic expansion of vault locations — including commodity warehousing companies and refiners — is essential to reduce the physical accessibility gap, particularly in Tier 2/3 cities. |

| Gold ETF–EGR integration | A regulatory pathway for Gold ETF schemes to hold EGRs as their underlying gold exposure would create structural institutional demand for EGRs, aligning India’s two largest formal gold segments. |

These proposals represent analytical inferences and potential regulatory directions, not confirmed SEBI proposals. Readers should monitor SEBI consultation papers and Annual Reports for confirmed initiatives.

8. CONCLUSION

The EGR framework is structurally sound and internationally informed. It’s regulatory architecture — covering securities law, exchange regulation, vault manager oversight, and depository integration — addresses genuine market gaps. The key achievements are infrastructural: a new securities category, functional exchange segments, and a physically backed demat gold holding mechanism.

What remains uncertain is adoption. International experience demonstrates that sustainable gold market liquidity requires at least one of three foundations: large institutional participation, accessible retail distribution, or regulatory demand anchors. EGRs have not yet secured a foothold on any of these pillars, but none of the structural obstacles is insuperable.

The framework’s long-term viability will be determined less by regulatory design — which is adequate — and more by the pace of ecosystem development and the willingness of institutional participants to provide the liquidity infrastructure that retail adoption requires.

******

Disclaimer: The views expressed in this article are personal and are based on publicly available regulatory materials and market information available as on the date of writing. While reasonable efforts have been made to ensure accuracy, the author does not warrant the completeness, accuracy, adequacy, or continued validity of the information contained herein. The article is intended solely for educational and informational purposes and should not be construed as legal, tax, investment, or professional advice. Readers are advised to independently verify all applicable laws, regulations, circulars, and other relevant materials before acting upon any information contained in this article.

Author Bio