Case Law Details

ACIT Vs Lingaiah Amidyala (ITAT Hyderabad)

The appeal was filed by the Revenue against the order of the Commissioner of Income Tax (Appeals) for Assessment Year 2019-20, challenging the deletion of an addition of ₹3,15,38,320 made towards long-term capital gains based on a seized loose sheet allegedly showing receipt of cash over and above the registered sale consideration for immovable property.

Background of the Case

The assessee, an individual earning salary income from Yashoda Healthcare Services Pvt. Ltd., filed the original return of income declaring ₹64,90,640. A search under Section 132 was conducted in the Yashoda Group, followed by a search in the assessee’s case, during which certain loose sheets and documents were seized. Pursuant to notice under Section 153A, the assessee filed a return declaring the same income. The Assessing Officer completed the assessment under Section 153A by making an addition of ₹3,15,38,320 as capital gains, alleging that the assessee had received cash over and above the cheque consideration reflected in the registered sale deeds.

Basis of the Addition

The Assessing Officer relied upon Page 24 of Annexure A/LA/RES/01, which mentioned the sale of 698.66 square yards at ₹52,000 per square yard, recording total consideration of ₹3,63,30,320, including ₹47,92,000 by cheque and ₹3,15,38,320 in cash. Since the extent of land and cheque component matched the registered sale deeds, the Assessing Officer concluded that the assessee had received the alleged cash component and added it as capital gains.

Order of the Commissioner (Appeals)

The Commissioner (Appeals) deleted the addition. He observed that although Section 292C creates a presumption regarding documents found during search, the presumption is rebuttable. The assessee denied receipt of any cash over and above the cheque payments. The Assessing Officer had also examined both purchasers under Section 131, and they categorically denied making any cash payments beyond the amounts recorded in the sale deeds.

The Commissioner (Appeals) further noted that the loose sheet did not specify the nature of payment, transaction date, property particulars or other essential details. Apart from the loose sheet, no corroborative evidence was produced to establish receipt of cash. The registered sale deeds reflected consideration received entirely through cheques, and the stamp valuation matched the recorded consideration. Relying on judicial precedents, the Commissioner (Appeals) held that no addition could be sustained merely on the basis of an uncorroborated loose paper and directed deletion of the addition.

Revenue’s Arguments Before the Tribunal

The Revenue contended that the Commissioner (Appeals) incorrectly recorded that the assessee had denied the contents of the seized document during the statement under Section 132(4). It argued that the assessee had neither denied nor explained the seized document, repeatedly stating that he did not remember or could not comment on it. Since the details in the seized document matched the registered sale deeds regarding land extent and cheque payments, the Revenue argued that it constituted a speaking document proving receipt of cash. The Revenue also relied upon Sections 132(4A), 292C of the Income-tax Act and Section 114 of the Indian Evidence Act to contend that the burden lay on the assessee to rebut the presumption attached to documents found during search.

Assessee’s Contentions

The assessee submitted that the seized page was merely a dumb document lacking date, nature of transaction, identity of parties, details of payments, signatures or handwriting attributable to the assessee. It was argued that the document itself indicated that ₹92,88,320 was yet to be paid, whereas no evidence showed that such amount was ever received. The assessee also relied upon the registered sale deeds and the purchasers’ statements denying any cash payment. It was contended that no addition could be made solely on the basis of an uncorroborated loose sheet.

Tribunal’s Findings

The Tribunal observed that the Commissioner (Appeals) had incorrectly stated that the assessee denied the document during the Section 132(4) statement. The statement showed that the assessee neither admitted nor denied its contents. However, the Tribunal noted that the assessee consistently denied receipt of any cash by not offering such income in the return filed under Section 153A and through submissions made during appellate proceedings.

The Tribunal emphasized that both independent purchasers, examined by the Assessing Officer under Section 131, categorically denied making any cash payments. Despite recording these statements, the Assessing Officer failed to bring any additional evidence contradicting them.

The Tribunal further observed that the seized document itself mentioned that ₹92,88,320 remained “to be paid.” There was no evidence establishing whether or when this amount was actually paid. Consequently, the Revenue failed to prove receipt of this amount during the relevant assessment year.

Regarding the remaining amount, the Tribunal held that the entire addition rested solely upon the loose sheet. Since the document was unsupported by forensic examination, handwriting verification, independent evidence or corroborative material, it could not by itself establish receipt of on-money. The registered sale deeds and the purchasers’ statements directly contradicted the allegation of cash payments.

The Tribunal reiterated that the presumption under Section 292C is rebuttable, and the assessee had successfully rebutted it by producing registered sale deeds, relying on the purchasers’ statements, and consistently denying receipt of any cash. It also held that no addition could be made merely on the basis of a dumb document lacking necessary particulars without independent corroborative evidence.

Decision

The Tribunal upheld the order of the Commissioner (Appeals), holding that the Revenue failed to establish that the assessee had received any cash over and above the registered sale consideration. It concluded that the seized loose sheet, without corroborative evidence, could not justify the addition. Accordingly, the Revenue’s appeal was dismissed.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

The captioned appeal is filed by the Revenue, feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals)-12, Hyderabad dated 29.09.2022 for the A.Y. 2019-20 on the following grounds :

“1. The Ld. assessee.CIT(Appeals) erred both in law and on facts of the case in granting relief

2. On the facts and in the circumstances of the case, and in law, whether the Id. CIT(Appeals) is correct in deleting the addition made on the basis of seized material towards LTCG.

3. On the facts and in the circumstances of the case, and in law, the Ld.CIT(Appeals) ought to have considered the contents of seized page no. 24 of Annexure A/LA/RES/01 as a speaking document, particularly when the details extent of land sold and cheque component of consideration are matching with those of the sale deed.

4. On the facts and in the circumstances of the case, and in law, the Id. CIT(Appeals) failed to appreciate the fact that cash of Rs.3,15,38,320/- was actually received by the assessee from the sale of immovable property as evidenced by the notings available in the seized material.”

2. The brief facts of the case are that assessee is an individual, deriving salary income from M/s. Yashoda Healthcare Services Pvt. Ltd., and filed the original return of income for the AY 2019-20 on 25-09-2019, admitting income of Rs.64,90,640/-. The case was processed u/s.143(1) of the Act. A search and seizure operation u/s.132 was conducted in the case of Yashoda Group on 22-12-2020. Thereafter, a warrant was issued in the case of the assessee and search was conducted u/s.132 of the Act and during the course of search some documents / loose sheets were found and seized. Subsequently, Notice u/s. 153A was issued to the assessee by the Assessing Officer. In response to the notice u/s.153A, the assessee filed his return of income on 26-11-2021 declaring total income of Rs.64,90,640/-, which comprises of Income from Business & income from other sources. Accordingly, Notices u/s.143(2) and 142(1) were duly issued and served on the assessee by the AO. After examining the material on record and the information furnished by the assessee, Assessing Officer had completed the assessment u/s 153A of the Act on 30.03.2022 interalia making addition of Rs.3,15,38,230/- under the head income from capital gain. The finding of the Assessing Officer is recorded in Para 4 of his order to the following effect :

“4. On perusal of the explanation of the assessee it clearly indicates that, there is denial of cash received amounting to Rs:3,15,36,320/- and moreover it is exactly matching with the extent and sale consideration declared by him in his return of income that which was received-over and above the sale consideration. Further the assessee also could not substantiate with proper evidence. Hence, the explanation given in lieu of show cause notice is vague in nature, hence, it is not considered. In view of the above it is. proposed to add an amount of Rs.3,15,38,32OI-under the head income from capital gain.”

3. Feeling aggrieved by the order passed by the assessing officer, assessee filed appeal before the Ld. CIT(A), who allowed the appeal of assessee.

4. Feeling aggrieved by the order passed by the Ld. CIT(A), the Revenue is in appeal before us on the grounds mentioned herein above.

5. Firstly, Ld. DR had drawn our attention to the order passed by the ld.CIT(A). In as much as our attention was drawn to para 5.5 of the order of ld.CIT(A) which is to the following effect :

“5.5 I have considered the submissions of the AR and the order of the AO. It is seen that the appellant has sold the said property admeasuring 698.66 sq. yards vide two registered sale deeds dated 26.09.2018 to Shri Amand Krishnakanth and M/s. Rutuja Projects for considerations of Rs.27,27,000/- and 20,65,000/- respectively. On perusal of the sale deeds, it can be seen that the appellant has paid the entire sale consideration as per the deed through cheques. However, on the basis of seized document at page no.24, the AO observed that the appellant has also received Rs.3,15,38,320/- in cash over and above the actual sale consideration. The relevant extract of seized document was reproduced by the AO in the assessment order and hence not reproduced here again. Section 292C of the Income Tax Act casts a presumption that the contents of the books of account or other documents found during search are true and belong to such person. Hence prima facie, there is a presumption that the contents of page no.24 seized during search are true and belong to the appellant. However, this is a rebuttable presumption. The appellant has denied the contents under oath in a statement u/s.132(4) recorded during search. He claimed that he has not received any on-money over and above the cheque payments. The AO has examined the buyers viz, Shri Amand Krishnakanth and Shri Produturi Puma Chandrasekhar Reddy under oath u/s.131 of the Act and both have denied any payment of cash over and above the cheque payments mentioned in the sale deed. In other words, both the seller and the buyers have rebutted the presumption enshrined in Section 292C of the Act. There is no other corroborative evidence brought on record by the AO to substantiate that cash over and above the cheque payments have been received by the appellant. Besides, as contended by the AR, the loose paper does not mention the nature of payment, date of transaction, particulars of property etc. Though the details of square yards and the cheque component match with the actual sale deed, the denial of receipt and payment of cash by the seller and buyer, requires the AO to bring further corroborative evidence to prove that the cash was actually received by the appellant. On perusal of the sale deed, the SRO market value of the property sold is as per the cheque value received by the appellant. No evidence has been brought on record to prove that the market value is higher than the SRO value and cash over and above the SRO value has been paid other than the loose paper. In the case of Pr.CIT vs Delco India (P) Ltd, [2016] 67 taxmann.com 357 (Delhi), the Hon’ble Delhi High Court held that no addition u/s.68 could be made when both the parties whose names appear in the loose paper denied the transaction. In the case of Dy.ClT vs C.Krishna Yadav [2011] 12 taxmann.com 4 (Hyderabad, Tribunal) the jurisdictional ITAT held that unsigned loose slips of paper without establishing nexus to the business of the assessee and non-examination of parties written on the loose slips to corroborate the notings, imply that the addition is made based on suspicion and therefore deleted the addition. In the case of Gyan Kumar Agarwal vs ACIT [2013] 30 taxmann.com 114 (ITAT, Hyderabad), the jurisdictional ITAT held that no addition can be made merely on the basis of notings on a dumb document. Respectfully following the decisions of the jurisdictional ITAT, the AO is directed to delete the addition of Rs.3,15,38,320/-. Accordingly, the appeal of the appellant on this issue is ALLOWED.

6. Before us, ld. DR submitted that the ld.CIT(A) has wrongly mentioned the fact in his order whereby he has mentioned that the assessee had denied the contents of the statement u/s 132(4) of the Act recorded during the search. Ld. DR had also drawn our attention to the statement recorded during the course of search and our attention was drawn to Page 9 of paper book which is to the following effect :

”Q.32 As per the details mentioned in page no.24 of Anx A/LA/RES/01, you have sold 698.66 sq.yrds of land ® 52,000/-per sq.yrd and received sale consideration of Rs.3,63,30,320/-, out of which you have received .you have received an amount of Rs.47,92,000/- by way of cheque and balance amount of Rs.3,15,38,320/- in cash. Therefore you have to offer Capital gains on the total sale consideration of Rs.3,63,30,320/- as against the cheque amount of Rs.4792000/-. What is your explanation.

Ans. I don’t know and I don’t remember anything about the contents of the page no.24 of the Anx A/LA/RES/01.

Q.33 As per the details mentioned in the page–no.24 of.Anx A/LA/RES/01 i.e., the extent of land and the cheque amount of Is.47,92,000/- are exactly matching with the extent and sale consideration declared by you in your return of income are exactly matching. In these circumstances, bow can you say that you have not received the cash as mentioned in the page no24 of Anx A/LA/RES/01.

Ans. I don’t remember and I cannot say anything.

Q.34 Phase produce the sale deed for the sale of plot measuring about 698.66 sq.yrds’ situated at Nizamabad?

Ans. Presently, I am not having the sale deed and I will produce the sale deed copy ‘within 4 days.

Q.35 As per ec.132(4A) of the Income Tax Ac; 1961 where any books of accounts or other documents are found in the procession or control of any person, it may be presumed that, such books of accounts or other documents belong to such person and the contents of such books of accounts or other documents are true. Therefore, it is presumed that the contents of the page no.24 of Anx A/LA/RES/01, belong to you arid are true and correct and accordingly, the sale consideration has to be adopted at Rs.3,63,30,320/- as against the sale consideration of Rs.47,92,00/-declared by you in your Return of Income for the AY.2019-20. What do you say?

Arts. I don’t know anything and I cannot comment anything.”

7. It was the submission of the ld. DR that perusal of the statement recorded u/s 132(4) of the Act, it is apparent that the assessee has not denied to have the contents of Page 24, from the documents / loose sheets vide Annexure A/LA/RES/01, found during the course of search from the residential premises of the assessee. It was submitted that the findings of ld.CIT(A) were based on incorrect assumption of the fact and therefore, the order of the ld.CIT(A) is required to be set aside and the order of the Assessing Officer is required to be restored. In support of his case, ld. DR had filed the Written Submissions which is to the following effect :

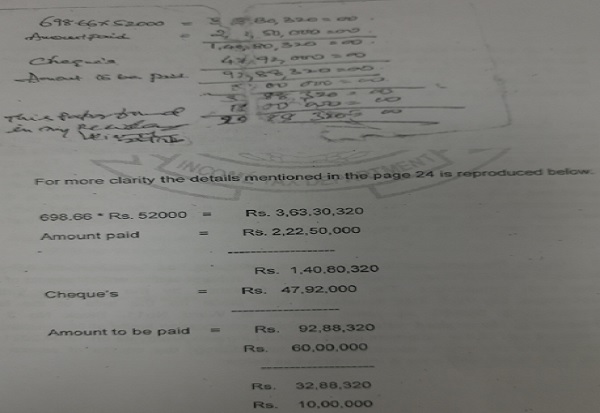

“A search u/ s. 132 of LT Act was conducted in the case of Yashoda Group on 22/12/2020. As part of search operation a warrant was issued in the case of assessee Sri Lingiah Amidyala who derived his salary income for AY.2019-20 from Yashoda Health Care Services Pvt. A search was conducted u/ s. 132 of the Act., in the assessee residence. During course of search and seizure proceedings certain documents/loose sheets were found and sized vide Annexure -A/LA/RES/0 1, serially from 1 to 31. From the search proceeding to scrutiny proceeding assesse had failed to explain detail of page-24 where it was clearly mentioned that 698.66 Sq. Yards of plot was sold @ 5200 per sq.yard for a total sale consideration of Rs.3,63,30,320/- and out of it Rs.47,92,000 was received by way of cheque and remaining of Rs.3, 15,38,320/-in cash.

In the Sale Deed 9948/2018 & 9949/2018 also mentioned sale of land admeasuring 698.66 Sq. Yards situated at Ward No. 11 Block No.3 at Kanteswhwar, Nizamabad and amount of Rs.47,92,000 was received by way of cheque for sale consideration. Further, during the whole proceeding starting from search operation u/s. 132, statement recording of the assessee and during the scrutiny proceeding, assessee had not explained anything about the slip i.e page, no. 24 just had avoided the asked question saying I have no comment on it. From the above fact and circumstances of the case, the hon’ble bench may kindly consider the contents of seized page no.24 of Annexure A/LA/RES/01 as a speaking document, particularly when the detailed . extent of land sold and cheque component of consideration are matching with those of the sale deed.

8. Per contra, ld. AR had submitted that page 24 of the paper book which had been reproduced by the Assessing Officer in the order was a dumb document.

9. Ld. AR further submitted that the whole basis of Page 24 out of documents seized vide Annexure A/LA/RES/01 is incorrect as in the said document, the amount of the total consideration was mentioned as Rs.3,63,30,320/-. The ld. AR had submitted that two sale deeds were executed on the same day in favour of two persons i.e., on 26.09.2018. It was also submitted that out of the total consideration, the amount to be paid was mentioned as Rs.92,88,820/-. The ld. AR had made two-fold statements namely, that the assessee is a seller and as per the sale deed, the assessee has to receive the consideration and was not to pay the consideration and secondly, it was the contention of the ld. AR that as per Page 24, the entire sale consideration has not been paid and a sum of Rs.92,88,320/- was yet to be paid. Ld. AR further submitted that no evidence has been brought on record to show that the amount of Rs.92,88,320/- was received by the assessee. Further, it was submitted that this document is a dumb document as neither the date nor the nature of the transaction have been mentioned. No details of payments received by the assessee are mentioned like date of payment, person who has paid. Further, the said document is not signed by the assessee and lastly, it was submitted that the document is not in the handwriting of the assessee. Further, it was submitted that no addition can be made on the basis of dumb document, unless the facts are corroborated by any independent evidence.

9.1. The ld. AR had also drawn our attention to the provision of section 292C of the Act and on the basis of the provision of section 292C of the Act, it was submitted that all the conditions mentioned in clause 2 of section 292C are required to be cumulatively fulfilled before invoking the provisions against the assessee u/s 292C of the Act. To substantiate his case, Ld. AR had relied upon various judgments which are to the following effect :

1. Chariminar Bottling Co. (P) Ltd – ITA No.1344/H/2013.

2. PCIT Vs. Tarun Kumar Goyal dt.24.08.2022 of Telangana High Court.

3. ITA Nos.456 and 457/Hyd/2020 in the case of Tarun Kumar Goyal.

4. DCIT Vs. C.Krishna Yadav reported in 46 SOT 250.

5. Romi Lal Nanda Vs. ITO – ITA No.792/Del/2016.

6. CIT Vs. S.M. Aggarwal – Order dt.29.03.2007 of Delhi High Court.

7. CIT Vs. Vivek Aggarwal – Order dt.09.02.2015 of Delhi High Court.

8. CIT(Central)-3, Vs. Sri Praveen Juneja – Delhi High Court.

9. DCIT, Central-1, Bhopal Vs. Jasjeet Singh Walia – ITA No.183/Ind/2020.

10. ACIT Vs. Ld. DR. Kamala Prasad – 3 ITR (Trib) 533.

11. Zinab Investment (P) Ltd. Vs. DCIT – ITA 783/Hyd/2020.

12. Gyan Kumar Aggarwal Vs. ACIT – 2013 30 Taxmann.com 114.

13. PCIT Vs. Delco India (P) Ltd. of Delhi High Court – (2016) 67 taxmann.com 357.

10. In rebuttal, the ld. DR had submitted that burden of proof to rebut the contents of document found during the course of search lies on the assessee and he relied upon section 132(4a) and section 292C of the Act. Besides the above, he also relied upon section 114 of the Indian Evidence Act. It was further submitted that page 24 (one of the impounded documents during search i.e., Annexure-A/LA/RES/01) was not a dumb document as the figure of cheque amount mentioned in the said document matches with the figure mentioned in the sale deed dt.26.09.2018. It was also the contention of the assessee that the assessee has not denied the transaction mentioned in Page 24 reproduced hereinabove and therefore, the adverse inference is required to be drawn against the assessee as the assessee owns the said document.

11. We have heard the rival submissions and perused the material on record. The basis of deleting the addition by the ld.CIT(A), mentioned in para 5.5 of his order, was reproduced at Para 5 of this order. The whole order of the ld.CIT(A) revolves around, the fact that the assessee had denied the contents of alleged page 24 in the statement recorded u/s 132(4) of the Act. However, the finding of ld.CIT(A) is contrary to the record which is clear from the reading of the statement reproduced hereinabove, more particularly, answer to questions 32 to 34 while recording statement on 23.12.2020 wherein the assessee had neither admitted nor denied the document. On the basis of the above replies by assessee, it is clear that the assessee has neither denied the contents of alleged page 24 during the course of search nor admitted the receipt of the amount. However, it is clear from the written submissions of the assessee filed before the ld.CIT(A) that the assessee had denied to have received money over and above the sale consideration mentioned in the sale deed. The above fact of denial can be inferred from the fact that assessee had not admitted the said income of Rs.3,15,38,320/- in return of income filed in response to section 153A of the Act. Further, the fact remains that the purchasers of the property in their statements recorded u/s 131 of the Act have denied to have made any cash payment over and above the sale consideration mentioned in sale deeds to the assessee.

12. As a matter of fact, the Assessing Officer had recorded the statements of Shri Produturi Purna Chandrasekhar Reddy and Shri Amand Krishnaiah on 25.03.2012, who have categorically denied the payment of any amount in cash to the assessee over and above the sale consideration mentioned in the sale deeds. It was for the Assessing Officer to bring more evidence, thereby contradicting the statements of these two people. Nonetheless, the statement of these two persons have been recorded by the Assessing Officer wherein these two persons had categorically denied to have made any ‘on money’ to the assessee. There is no evidence / explanation brought on record by the Assessing Officer explaining the contents of Page 24, more particularly when the assessee has to receive the payment whereas it was mentioned at Page 24, the assessee has to pay the amount.

13. The Assessing Officer though has examined the purchasers but they have denied to have made any payment of ‘on money’ to the assessee. Thus, the Assessing Officer has not brought any contradictory evidence to prove the payment of ‘on money’ to the assessee. The ld. DR had submitted that the date of the amount of cash paid should be taken as the date of sale i.e., 26.09.2018. In our view, if the above said contention has been taken as correct, then the whole amount is required to be received by the assessee on the date of registration itself. Though, from page 24, it appears that the amount of Rs.92,88,320/- was yet to be paid to the assessee but no evidence has been brought on record to say in which year the said amount was received by the assessee i.e., whether immediately after the registration of sale deed or in subsequent financial year or thereafter. Therefore, to that extent, we are in agreement with the argument of the ld. AR. Furthermore, Assessing Officer had failed to establish that the amount of Rs.92,88,320/- was paid on or after the date of registration of property, at page 24 as it was mentioned as “to be paid”. In the light of the above, we are of the opinion that the Revenue has not been able to prove that the amount of Rs.92,88,320/- was paid during the year under consideration i.e., at the time of registration of sale deed relevant to A.Y. for the year under consideration. Therefore, the amount of Rs.92,88,320/- is required to be deleted.

14. The balance amount after deleting the amount of Rs.92,88,320/- which remained, added by the Assessing Officer was Rs.2,22,50,000/-. In this regard, the ld. DR had pointed out that the said amount forming part of the document was recovered from the residential premises of the assessee. The focus of ld. DR is on the answers given by the assessee to question nos.32 to 35. Perusal of question and answers for Q.32 to Q.35, it is abundantly clear that the assessee has not admitted the contents of the said document and further the assessee has not agreed that the sale consideration received by the assessee was Rs.3,63,30,320/-.

14.1 Admittedly, the two registered sale deeds were executed in favour of two independent purchasers, who are unrelated to the assessee. These two purchasers namely, Shri Produturi Purna Chandrasekhar Reddy and Shri Amand Krishnaiah, on examination, on oath had denied to have made any cash payment to the assessee. The above said fact of registering the property at the value mentioned on the sale deeds, if considered in the light of the statement recorded by the Assessing Officer u/s 131 of the Act, then the necessary conclusion would be that no “on money” was received by the assessee on account of sale / registration of the two properties. The conclusion of the Assessing Officer was solely based on Annexure 24, which was reproduced in Page 3 of the assessment order. Now we are confronted with the issue whether the said Annexure 24 on stand alone basis can form basis for the addition in the hands of the assessee, more particularly, when the said document is contrary to the registered sale deeds and also the statements recorded by the Assessing Officer under section 131 of the I.T. Act ? The law is fairly settled in this regard that no addition can be made on the basis of a dumb document found during the course of search / seizure and it is essential for the Revenue to bring on record the corroborative evidence to prove the receipt of “on money” by the assessee.

15. Further, we are in agreement with the findings recorded by the Hon’ble High Court of Telangana in the case of PCIT Vs. Tarun Kumar Goyal (placed at page 46 of the paper book) wherein the Hon’ble High Court had held that no addition can be made in the hands of assessee merely based on dumb document which is not corroborated with any other independent evidence. As mentioned hereinabove, the conclusion of the Assessing Officer that the assessee had paid or received an amount of Rs.2,22,50,000/- was based on surmises and conjectures as the said page 24 is not a speaking document and no inference can be drawn based on the said document. The Assessing Officer has not brought any forensic evidence to prove the handwriting on the said page 24 as that of the assessee and was made with a view to recording the alleged sale transaction.

16. In the present case, ld.CIT(A) after examining the documents and the decisions placed before him had deleted the addition. In our view, no fault can be found on the basis of the conclusion drawn by the ld.CIT(A). The contention of the ld. DR that as per the provision of section 132(4) of the Act and section 292C of the Act, the onus is on the assessee to rebut the contents of the document found during the course of search / seizure. The perusal of section 292C makes it abundantly clear that the presumption as to the contents of the document found in the possession of the assessee during the course of search is a rebuttable presumption and the assessee can very well rebut the transaction by bringing contrary evidence on record. Lastly, Page 24 is a dumb document as the necessary details are not provided and the assessee has denied the contents of the said document by bringing on record (1) registered sale deeds which clearly belies the payment of ‘on money’ on the sale transaction. (2) The Assessing Officer had examined the purchasers of the property who had denied to have made payment in cash over and above the sale consideration to the assessee. (3) the assessee has not admitted that he has received any cash payment on account of sale of these properties and (4) the Assessing Officer has not asked any question to the purchasers about the making of the cash payment and the year of making the cash payment to the assessee. Examining the issue in the light of the above, we are of the opinion that no interference to the findings of the ld.CIT(A) can be called for. Accordingly, the appeal of the Revenue is dismissed.

17. In the result, the appeal of the Revenue is dismissed.

Order pronounced in the Open Court on 26th April, 2023.

Author Bio