File ITR-4 (Sugam) Online FAQs

1. Who is eligible to file ITR-4 for AY 2021-22?

ITR-4 can be filed by a Resident Individual / HUF / Firm (other than LLP) who has:

♦ Income not exceeding ₹ 50 Lakh during the FY

♦ Income from Business and Profession which is computed on a presumptive basis u/s 44AD, 44ADA or 44AE

♦ Income from Salary / Pension, One House Property, Agricultural Income (up to ₹ 5000/-)

♦ Other sources which include (excluding winning from Lottery and Income from Race Horses):

- Interest from Savings Account

- Interest from Deposit (Bank / Post Office / Cooperative Society)

- Interest from Income Tax Refund

- Family Pension

- Interest received on enhanced compensation

- Any other Interest Income (e.g., Interest Income from unsecured loan)

2. Who is not eligible to file ITR-4 for AY 2021-22?

- ITR-4 cannot be filed by an individual /HUF / Firm (other than LLP) who:

- is a Residents Not Ordinarily Resident (RNOR), and Non-Resident Indian

- has total income exceeding ₹ 50 Lakh

- has agricultural income in excess of ₹ 5,000/-

- is a Director in a Company

- has income from more than One House Property;

- has income of the following nature:

- winnings from lottery;

- activity of owning and maintaining race horses;

- income taxable at special rates u/s 115BBDA or Section 115BBE;

- has held any unlisted equity shares at any time during the previous year

- has deferred income tax on ESOP received from employer being an eligible start-up

- is not covered under the eligibility conditions for ITR-4

3. What are the changes in ITR-4 as compared to previous years?

As compared to previous years, ITR-4 of AY 2021-22 has an option where, if you wish to opt for the new tax regime u/s 115BAC, you need to select Yes in the new form.

Please note that individual or HUF opting for new tax regime u/s 115BAC has to mandatorily file Form 10-IE before due date of filing of return u/s 139(1). After filing Form 10-IE, original return or revised return is required to be filed mandatorily to avail the benefit of new tax slab u/s 115BAC and Acknowledgement Number and Date of filing Form 10IE are mandatory fields in ITR-4.

4. What documents do I need to file ITR-4?

You will need to keep the below documents ready (as applicable) to file ITR-4:

- Form 16

- Form 26AS

- Form 16A

- Bank Statements

- Housing Loan Interest Certificates

- Receipts for Donation Made

- Rental Agreement

- Rent Receipts

- Investment premium payment receipts – LIC, ULIP etc.

5. What is the presumptive taxation scheme for users filing ITR-4?

According to Sections 44AA of the Income Tax Act (1961), a person engaged in business or profession needs to maintain regular books of accounts under certain circumstances as per specific conditions. To relieve small taxpayers from such compliance burden, the Income Tax Act has framed the presumptive taxation scheme u/s 44AD, 44ADA and 44AE. A person adopting the presumptive taxation scheme can declare income at a prescribed rate. The Act has laid out presumptive taxation schemes (for ITR-4 users) as given below: ·

- Section 44AD: Computation of income on estimated basis in the case of taxpayers (being a Resident Individual, Resident HUF, or Resident Partnership Firm (other than LLP) engaged in certain business subject to certain conditions.

- Section 44ADA: Computation of professional income on estimated basis for Assessee being a resident in India and engaged in a profession referred to in section 44AA (1) subject to certain conditions.

- Section 44AE: Computation of income on estimated basis in the case of taxpayers (being an Individual, HUF, Firm (other than LLP) or any other person being a resident or non-resident) engaged in the business of plying, leasing or hiring goods carriages, who owns not more than ten goods carriages at any time during the previous year.

6. Who is not eligible for the presumptive taxation scheme of Section 44AD?

The scheme of Section 44AD is designed to give relief to small taxpayers engaged in any business, except the following businesses:

- Business of plying, hiring, or leasing goods carriages referred to in sections 44AE

- A person carrying on any agency business

- A person earning income in the form of commission or brokerage (e.g., insurance agents)

- Any business whose total turnover or gross receipts exceeds ₹ 2 Crore

Apart from the above, a person who is required to maintain books of accounts as referred to in Section 44AA (1) is not eligible for presumptive taxation scheme u/s 44AD.

7. The gross receipts for my business in the year are more than ₹ 2 Crore. Can I opt for presumptive taxation scheme of 44AD?

No. You can opt for the presumptive taxation scheme of section 44AD only if the total turnover or gross receipts from your business do not exceed the limit prescribed (i.e., ₹ 2 Crore).

8. I opted for the presumptive taxation scheme u/s 44AD for my last filed ITR. If I don’t opt for it any time in the next 5 years, what will happen?

If you opt for presumptive taxation scheme then you are required to follow the same scheme for the next 5 years. If you don’t, the presumptive taxation scheme won’t be available for you for next 5 years. For example, you claimed to be taxed on presumptive u/s 44AD for AY 2019-20, AY 2020-21 and AY 2021-22. However, for AY 2022-23, let’s say you did not opt for the presumptive taxation scheme. In this case, you will not be eligible to claim benefit of presumptive taxation scheme for next five AYs (AY 2023-24 to 2027-28).

9. Who can opt for presumptive taxation scheme of Section 44ADA?

The presumptive taxation scheme of Section 44ADA can be adopted by a resident in India carrying on specified profession whose gross receipts do not exceed ₹ 50 Lakh in a FY. Following professions are specified profession:

- Legal

- Medical

- Engineering or Architectural

- Accountancy

- Technical Consultancy

- Interior Decoration

- Any other Profession as notified by CBDT

10. I opted for presumptive income scheme of Section 44AD or 44ADA. Can I claim further deduction of expenses after declaring profit at applicable rate under respective sections of gross receipts?

No, a person who opted for the presumptive taxation scheme is deemed to have claimed all deduction of expenses. Any further claim of deduction is not allowed after declaring profit at specified rate. However, you can claim deductions under Chapter VI-A.

11. I opted for the presumptive income scheme of Section 44ADA. Do I have to pay Advance Tax in respect of income from profession covered in Section 44ADA?

Yes. Anyone opting for the presumptive taxation scheme u/s 44ADA is liable to pay 100% of Advance Tax on or before 15th March of the previous year. If you fail to pay the Advance Tax by 15th March of previous year, you will be liable to pay interest as per Section 234B and Section 234C. Any amount paid by way of Advance Tax on or before 31st March will also be treated as Advance Tax paid during the FY ending on that day.

12. I opted for presumptive taxation scheme of Section 44ADA. Do I need to maintain books of accounts as per Section 44AA?

If you are engaged in a specified profession as referred in Sections 44AA (1) and opt for presumptive taxation scheme of Section 44ADA (declare income @50% of the gross receipts), you are not required to maintain the books of accounts in respect of specified profession (i.e., the provision of Sections 44AA will not apply).

13. I opted for presumptive income scheme of Section 44AE. Do I need to maintain books of accounts as per Section 44AA?

Section 44AA of the Income Tax Act, 1961 has provisions relating to maintenance of books of account by persons engaged in Business / Profession. In case you opt for the presumptive taxation scheme of Section 44AE, the provisions of Section 44AA relating to maintenance of books of account will not apply.

14. I opted for the presumptive taxation scheme of Section 44AE. Do I have to pay Advance Tax in respect of income from business covered in Section 44AE?

Yes, You will be liable to pay Advance Tax. There is no concession with regard to the payment of Advance Tax if you opted for the presumptive taxation scheme of Section 44AE.

15. How do I compute income from a House Property which is partly self-occupied and partly let-out?

A house property may consist of two or more independent units, one of which is self-occupied and the remaining is used for any other purpose (i.e., let-out or used for own business). Income from such property will be computed in the following manner:

1. Part / unit which is occupied by you for your residence throughout the year will be treated as an independent property and income from such a part / unit will be computed in the manner as described in the ITR-4 user manual in case of a self-occupied property.

2. Part / unit which is let out will be treated as an independent property and income from such a part / unit will be computed in the manner as described in the ITR-4 user manual in case of let out property.

16. What is the tax treatment of unrealized rent that is subsequently realized?

Any subsequent recovery of unrealized rent will be deemed to be your income under the head Income from House Property in the year in which such rent is realized (whether or not you are the owner of that property in that year). It will be charged to tax after deducting a sum equal to 30% of unrealized rent.

17. Can my employer TAN be quoted in place of PAN?

No. PAN should never be quoted in the textbox where TAN is to be quoted, as the purposes for which PAN and TAN are allotted are different. TAN is a unique identification number which is allotted to parties who deduct or collect tax at source. PAN is a unique identification number issued to keep a linking of the transactions carried by a person like payment of tax, TDS / TCS credit, Return of Income, Return of Wealth, correspondence with the Income Tax Department or correspondence by the ITD, investments made by a person, loan taken by a person, etc.

18. What is the due date of Filing ITR-4 for AY 2021-22 (FY 2020-21)?

For AY 2021-22 (FY 2020-21) the due date of filing of ITR-4 is 31st July 2021.

File ITR-4 (Sugam) Online – User Manual

1. Overview

The pre-filling and filing of ITR-4 service is available to registered users on the e-Filing portal. This service enables individual taxpayers, HUFs, and firms (other than LLPs) to file ITR-4 online through e-Filing portal. This user manual covers the process for filing ITR-4 online.

2. Prerequisites for availing this service

| General |

|

| Others |

|

3. Form at a Glance

ITR-4 has six sections that you need to fill before submitting the form and a preview page where you can validate all your details filled. The sections are as follows:

- Personal Information

- Gross Total Income

- Disclosures

- Total Deductions

- Taxes Paid

- Total Tax Liability

Here is a quick tour of the various sections of ITR-4:

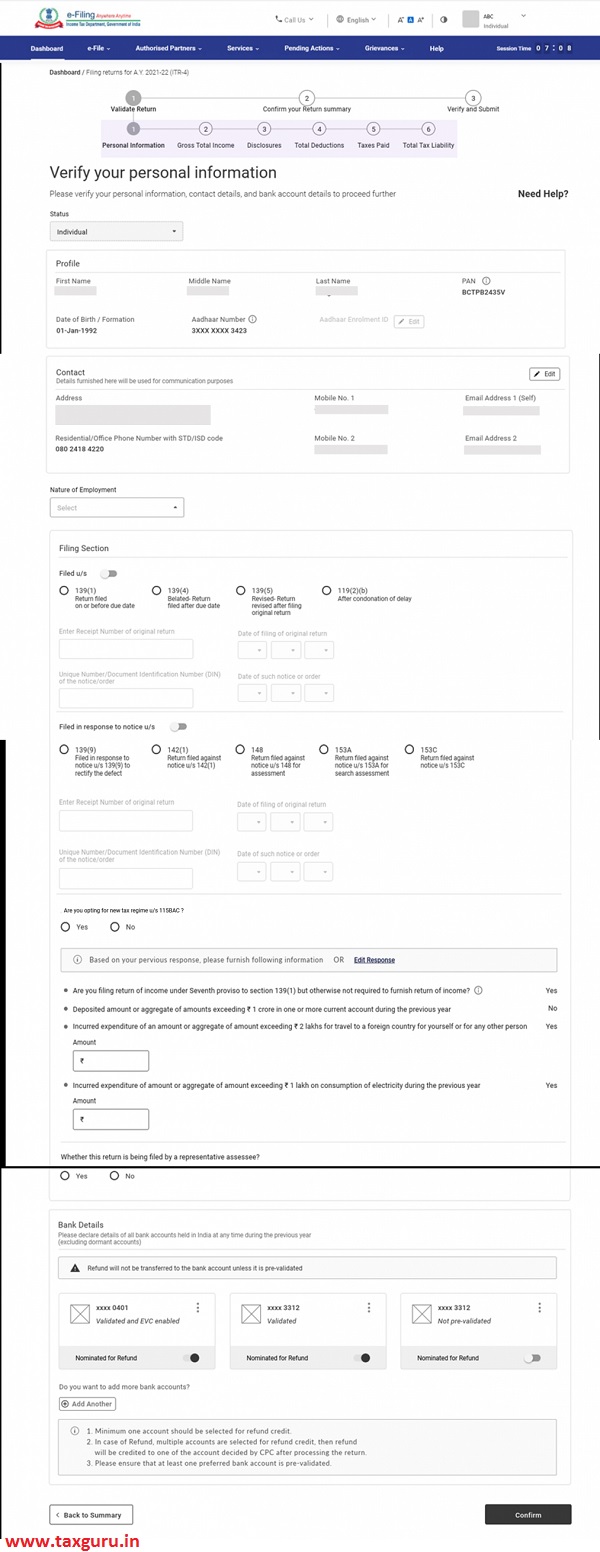

3.1 Personal Information

In the Personal Information section of the ITR, you need to verify the pre-filled data which is auto-filled from your e-Filing profile. You will not be able to edit some of your personal data directly in the form. However, you can make the necessary changes by going to your e-Filing profile. You can edit your contact details, filing type details, authorized representative, partner details (if applicable) and bank details in your e-Filing profile.

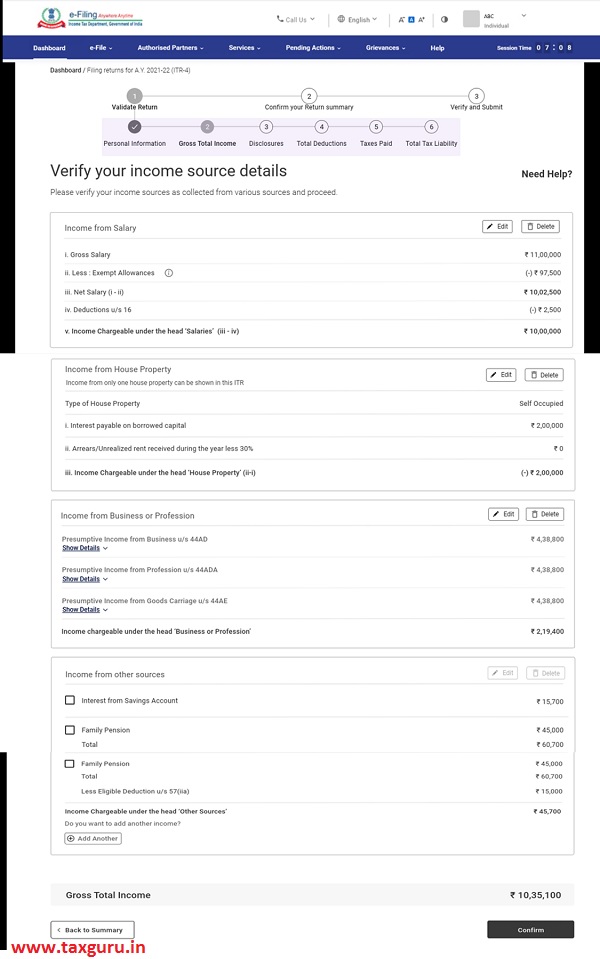

3.2 Gross Total Income

In the Gross Total Income section, you need to review the pre-filled information and verify your income source details from salary / pension, house property, business or profession and other sources (such as interest income, family pension, etc.). You will also be required to enter the remaining / additional details including your exempt income, if any.

Note: Some parts of this section will be greyed off depending on whether you’re an HUF or a firm (other than LLP).

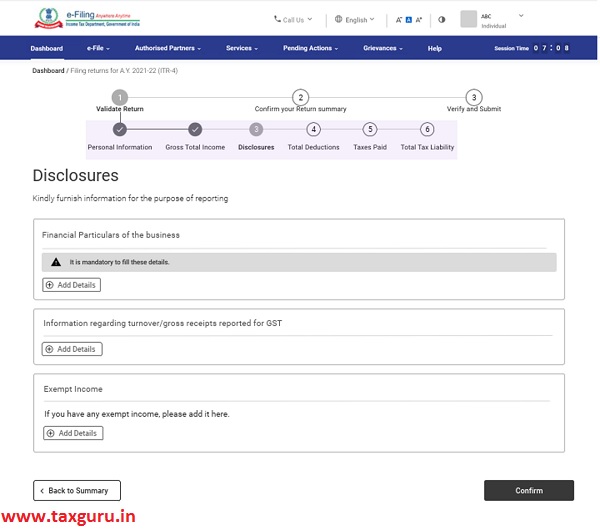

3.3 Disclosures

In the Disclosures section, you need to provide details of financial particulars related to presumptive business, gross receipts reported for GST and exempt income.

Note: The deduction in respect of the investment / deposit / payments for the period 1st April 2020 to 31st July 2020 cannot be claimed again, if already claimed in the AY 20-21.

3.4 Total Deductions

In the Total Deductions section, you need to add and verify any deductions you need to claim under Chapter VI-A of the Income Tax Act.

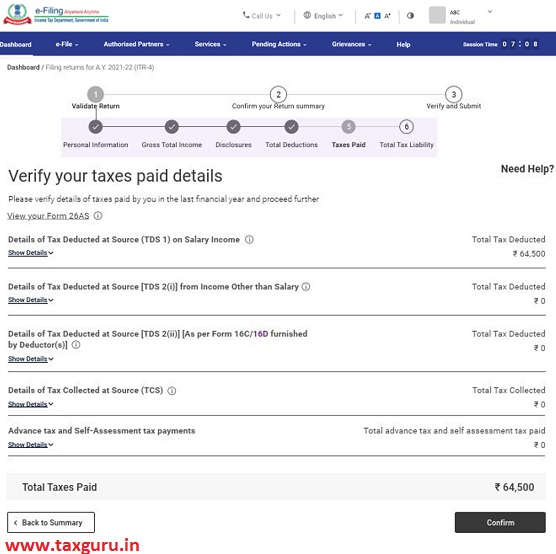

3.5 Taxes Paid

In the Taxes Paid section, you need to verify taxes paid by you in the previous year. Tax details include TDS from Salary / Other than Salary as furnished by the Payer, TCS, Advance Tax and Self-Assessment Tax.

3.6 Total Tax Liability

In the Total Tax Liability section, you will be able to view your computation of income, computation of tax and total tax, cess and interest. You need to check your tax liability details as per the sections you filled previously in the computation of tax section.

Note: For more details, refer to the instructions to file ITR issued by CBDT for AY 2021-22.

4. How to Access and Submit

You can file and submit your ITR through following methods:

- Online Mode – through e-Filing portal

- Offline Mode – through Offline Utility

Refer to the Offline Utility (for ITRs) user manual to learn more.

Follow the steps below to file and submit the ITR through online mode:

Step 1: Log in to the e-Filing portal using your user ID and password.

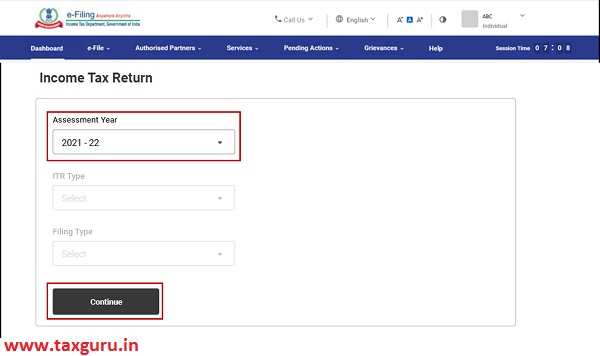

Step 2: On your Dashboard, click e-File > Income Tax Returns > File Income Tax Return.

Step 3: Select Assessment Year as 2021 – 22 and click Continue.

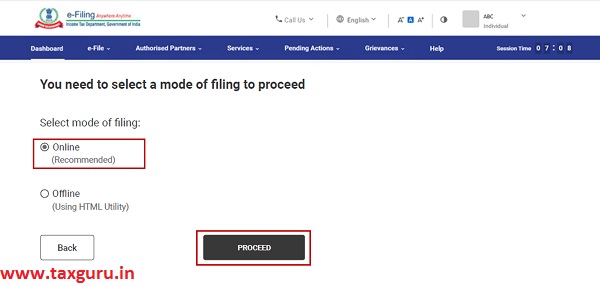

Step 4: Select Mode of Filing as Online and click Proceed.

Note: In case you have already filled the Income Tax Return and it is pending for submission, click Resume Filing. In case you wish to discard the saved return and start preparing the return afresh click Start New Filing.\

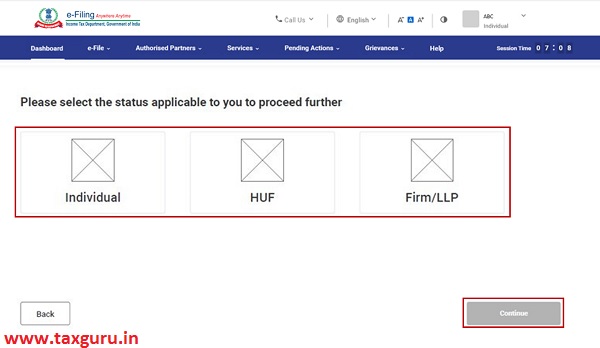

Step 5: Select Status as applicable to you and click Continue to proceed further.

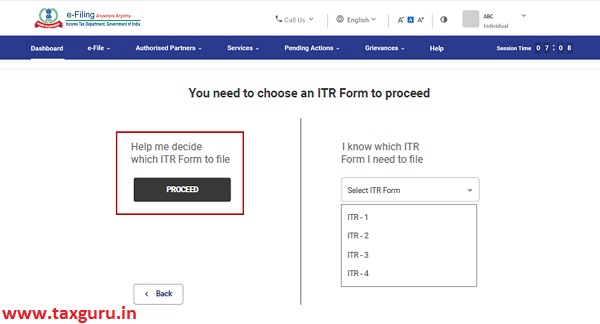

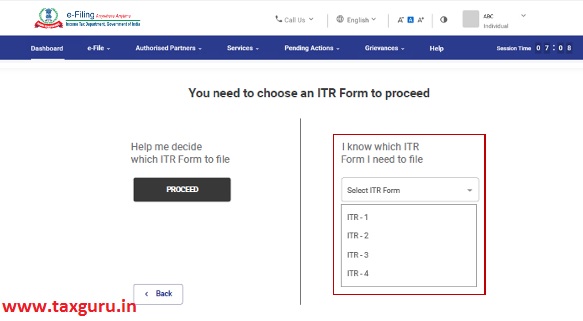

Step 6: You have two options to select the type of Income Tax Return:

- If you are not sure which ITR to file, you may select Help me decide which ITR Form to file and click Proceed. Once the system helps you determine the correct ITR, you can proceed with filing your ITR.

- If you are sure which ITR to file, select I know which ITR Form I need to file. Select the applicable Income Tax Return from the dropdown and click Proceed with ITR.

Note:

- In case you are not aware which ITR or schedules are applicable to you or income and deductions details, your answers in response to a set of questions will guide in determining the same and help you in correct / error free filing of ITR.

- In case you are aware of the ITR or schedules applicable to you or income and deduction details, you can skip these questions.

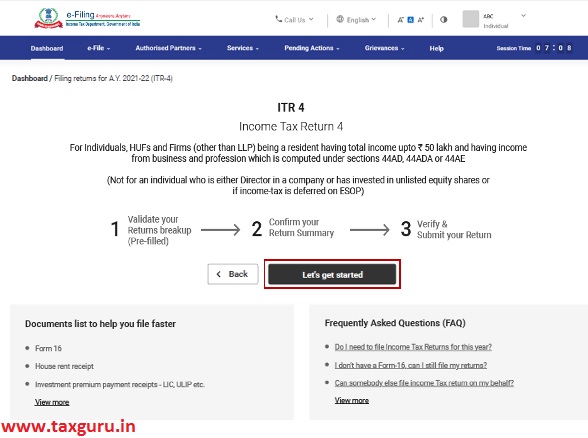

Step 7: Read the instructions to fill the form carefully and note the list of documents needed and click Let’s Get Started.

Step 8: Select the checkboxes applicable to you and click Continue.

Step 9: Review your pre-filled data and edit it if necessary. Enter the remaining / additional data (if required) and click Confirm at the end of each section.

Step 10: Enter your income and deduction details in the different section. After completing and confirming all the sections of the form, click Proceed.

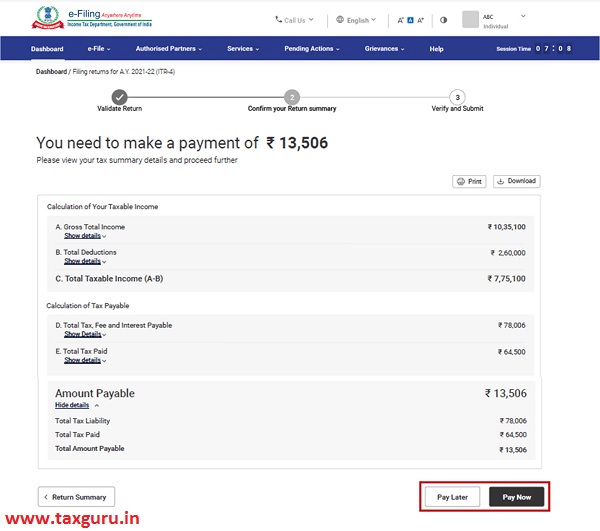

Step 10a: In case there is a tax liability:

You will be shown a summary of your tax computation based on the details you provided. If there is tax liability payable based on the computation, you will get the Pay Now and Pay Later options at the bottom of the page.

Note:

- It is recommended to use the Pay Now option. Carefully note the BSR Code and Challan Serial Number and enter them in the details of payment.

- If you opt to Pay Later, you can make the payment after filing your Income Tax Return, but there is a risk of being considered as an assessee in default, and liability to pay interest on tax payable may arise.

Step 10b: In case there is no tax liability (No Demand / No Refund) or if you are eligible for a Refund

After paying tax, click Preview Return. If there is no tax liability payable, or if there is a refund based on tax computation, you will be taken to the Preview and Submit Your Return page.

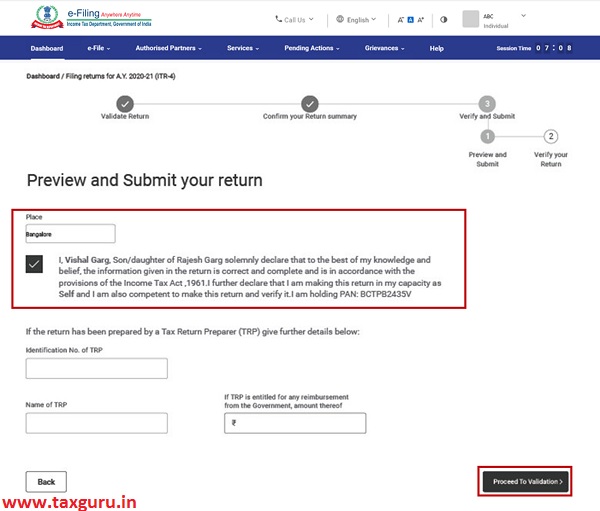

Step 11: On the Preview and Submit Your Return page, enter Place, select the declaration checkbox and click Proceed to Validation.

Note: If you have not involved a tax return preparer or TRP in preparing your return, you can leave the textboxes related to TRP blank.

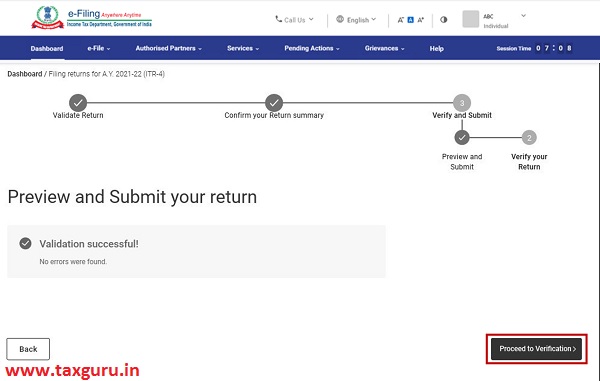

Step 12: Once validated, on your Preview and Submit your Return page, click Proceed to Verification.

Note: You will be shown a list of errors in your return, if any. You need to go back to the form to correct the errors. If there are no errors, you can proceed to e-Verify your return by clicking Proceed to Verification.

Step 13: On the Complete your Verification page, select your preferred option and click Continue.

It is mandatory to verify your return, and e-Verification (recommended option – e-Verify Now) is the easiest way to verify your ITR – it is quick, paperless, and safer than sending a signed physical ITR-V to CPC by post.

Note: In case you select e-Verify Later, you can submit your return, however, you will be required to verify your return within 120 days of filing of your ITR.

Step 14: On the e-Verify page, select the option through which you want to e-Verify the return and click Continue.

Note:

- Refer to the How to e-Verify user manual to learn more.

- If you select Verify via ITR-V, you need to send a signed physical copy of your ITR-V to Centralized Processing Center, Income Tax Department, Bengaluru 560500 by normal / speed post within 120 days.

- Please make sure you have pre-validated your bank account so that any refunds due maybe credited to your bank account.

- Refer to the My Bank Account user manual to learn more.

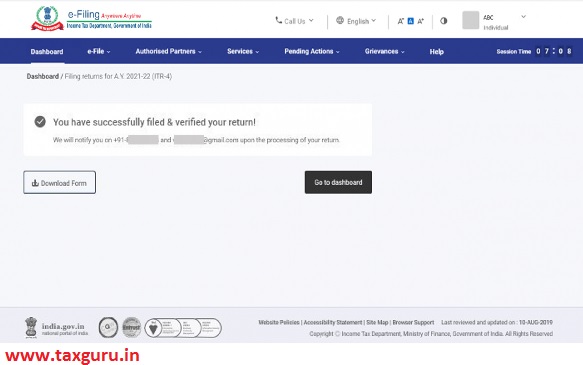

Once you e-Verify your return you, a success message along with the Transaction ID and Acknowledgment Number. You will also receive a confirmation message on your mobile number and email ID registered with the e-Filing portal.

4. Related Topics

- Login

- My Profile

- Register Yourself

- Authorize/Register as Representative

- Forgot Password?

- Dashboard

- My Bank Account

- Generate EVC

- Offline Utility

- Income tax forms (Upload)

- ITR Status

- How to e-Verify