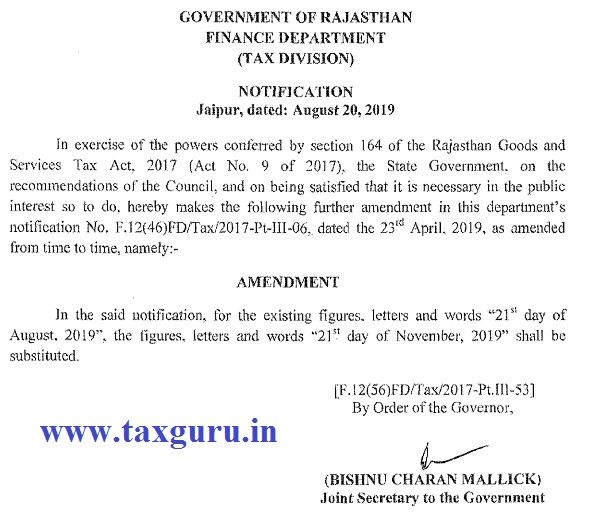

State Govt. of Rajasthan has issued a notification no. F.12(56)FD/Tax/2017-Pt. 111-53 dated 20-08-2019 extending date of applicability of Rule 138E of inserted vide Rule 12 of Rajasthan State Goods and Service Tax (Fourteenth) Amendment Rules, 2018 from 21-08-2019 to 21-11-2019.

Originally Rule 138E was supposed to come into effect from 21-06-2019 [notification no. F. 12 (4 6) FD/T AX/2017-Pt-III-06 dated 23-04-2019]. It was further extended upto 21-08-2019 vide notification no. F, 12(46) FD/Tax/2017-Pt IFF 17 dated 24-06-2019.

At present provisions of Rule 138E will come into effect from 21-11-2019 in the State of Rajasthan.

As per Rule 138E, if a supplier being a composition dealer do not file GST returns for two consecutive tax periods and any other supplier who does not file GST returns for a consecutive period of two months can-not generate “Part-A” of e-way bill.

For composition dealer word “ two consecutive tax period” has been used for filing of GST returns. For F.Y. 2019-20 due date to file GSTR-4 is 30-04-2020. However tax need to be discharged by filing form GST CMP-08 by 18th of the month succeeding the quarter for which CMP-08 needs to be filed. For Apr-June, 2019, extended due date to file Form GST CMP-08 is 31-08-2019.

Other taxpayers need to file return on monthly basis.

Rule 138E is self explanatory which is reproduced below for your reference:

“138E. Restriction on furnishing of information in PART A of FORM GST EWB-01.-

Notwithstanding anything contained in sub-rule (1) of rule 138,

no person (including a consignor, consignee, transporter, an e-commerce operator or a courier agency)

shall be allowed to furnish the information in PART A of FORM GST EWB-01 in respect of a registered person, whether as a supplier or a recipient, who,—

(a) being a person paying tax under section 10, has not furnished the returns for two consecutive tax periods; or

(b) being a person other than a person specified in clause (a), has not furnished the returns for a consecutive period of two months:

Provided that the Commissioner may, on sufficient cause being shown and for reasons to be recorded in writing, by order, allow furnishing of the said information in PART A of FORM GST EWB 01, subject to such conditions and restrictions as may be specified by him:

Provided further that no order rejecting the request of such person to furnish the information in PART A of FORM GST EWB 01 under the first proviso shall be passed without affording the said person a reasonable opportunity of being heard:

Provided also that the permission granted or rejected by the Commissioner of State tax or Commissioner of Union territory tax shall be deemed to be granted or, as the case may be, rejected by the Commissioner.

Explanation:- For the purposes of this rule, the expression “Commissioner” shall mean the jurisdictional Commissioner in respect of the persons specified in clauses (a) and (b) .”.

Rajasthan Goods and Services Tax (Fourteenth Amendment) Rules, 2018 can be downloaded from link given below:

http://finance.rajasthan.gov.in/PDFDOCS/TAX/GST/F-GST-7895-31122018.pdf

Author Bio