PFRDA has introduced Retirement Income Schemes (RIS) and drawdown options under the National Pension System (NPS) through Circular dated May 15, 2026, to provide flexible periodic payouts during the post-retirement phase while allowing continued market-linked corpus growth. The framework, aligned with the PFRDA (Exits and Withdrawals under the NPS) (Amendment) Regulations, 2025, permits Government and Non-Government subscribers to receive monthly, quarterly, or annual payouts up to the age of 85 years. Subscribers can opt for Systematic Payout Rate (SPR) or Systematic Unit Redemption (SUR) methods. The RIS Steady scheme introduces a gradually declining equity allocation from 35% at age 60 to 10% at age 75 onwards. PFRDA clarified that drawdown withdrawals will not affect the mandatory annuitisation requirement of 20% or 40% of corpus, thereby preserving the minimum lifelong pension requirement. The circular also mandates disclosures regarding market risks, payout resets, asset rebalancing, residual corpus treatment, and retirement income projections to ensure informed decision-making by subscribers.

Pension Fund Regulatory and Development Authority

Circular No.: PFRDA/2026/31/MWnR/01 | Date:15th May 2026

To,

All Stakeholders under NPS,

Subject: Introduction of Retirement Income Schemes (RIS) and Drawdown options under the National Pension System (NPS)

1. Building upon the frameworks established through Circular No. PFRDA/2016/8/PFM/03 dated 04 November 2016, Circular No. PFRDA/2023/30/SUP-CRA/10 dated 27 October 2023, and Circular No. PFRDA/2024/17/PDES/02 dated 01 October 2024, the Authority hereby introduces Retirement Income Schemes (RIS) and Drawdown Options under the National Pension System (NPS).

2. In line with the PFRDA (Exits and Withdrawals under the NPS) (Amendment) Regulations, 2025, this initiative aims to provide subscribers with more flexible periodic payout options during their decumulation phase while continuing to support corpus appreciation through the Retirement Income Schemes.

3. Under the RIS, subscribers are provided the flexibility to select a phased withdrawal of their designated pension corpus through any drawdown option. Consequently, these withdrawals shall have no impact on the mandatory annuitisation requirement of 20% or 40% of the corpus, as the case may be, thus ensuring that the minimum statutory requirement for a life-long pension remains intact.

4. These drawdown options shall be available to Government and Non-Government Subscribers (NGS) under NPS. The subscribers will he allowed to receive payouts on a periodical basis viz. monthly, quarterly or annually, for a period up to 85 years of age or as per the choice exercised by the subscriber, at the time of their exit from NPS.

5. These guidelines shall take effect from the date notified by the Authority, following the implementation of necessary system capabilities and operational framework.

This Circular and the related Guidelines are issued in exercise of the powers conferred under Section 14 of the Pension Fund Regulatory and Development Authority Act, 2013.

Yours Sincerely,

Dr. Alpana Vats,

(General Manager)

Guidelines for Retirement Income Schemes (RIS) and Drawdown options under the National Pension System (NPS)

1. Objective

The primary objective is to optimize periodic payouts for subscribers during the decumulation (payout) phase through drawdown options via the specific life cycle fund for the decumulation under NPS. It aims to enhance cashflow predictability and corpus longevity through continued support to corpus appreciation, thus minimizing the risk of early corpus exhaustion before the end of the drawdown period.

2. Retirement Income Schemes

The new life cycle scheme available to the subscriber for receiving their periodic payouts shall be called as Retirement Income Schemes (RIS).

Following variant is available under the RIS-

a. RIS Steady- This would employ a continuously declining, annual glide path that reduces equity exposure from 35% at age 60 to a floor of 10% at age 75, held constant thereafter until age 85.

Table l— Age-bracket wise Asset Class Distribution under RIS Steady

| Age Bracket | Asset Class E | Asset Class C | Asset Class G |

| Up to 60 years | 35% | 10% | 55% |

| 61 years | 33% | 11% | 56% |

| 62 years | 31% | 12% | 57% |

| 63 years | 29% | 13% | 58% |

| 64 years | 27% | 14% | 59% |

| 65 years | 25% | 15% | 60% |

| 66 years | 23% | 16% | 61% |

| 67 years | 21% | 17% | 62% |

| 68 years | 19% | 18% | 63% |

| 69 years | 17% | 19% | 64% |

| 70 years | 15% | 20% | 65% |

| 71 years | 14% | 20% | 66% |

| 72 years | 13% | 20% | 67% |

| 73 years | 12% | 20% | 68% |

| 74 years | 11% | 20% | 69% |

| 75 years | 10% | 20% | 70% |

| 76 years | 10% | 19% | 71% |

| 77 years | 10% | 18% | 72% |

| 78 years | 10% | 17% | 73% |

| 79 years | 10% | 16% | 74% |

| 80 years and above | 10% | 15% | 75% |

3. Drawdown Options

The subscribers will receive periodic payouts from the lumpsum portion of their accumulated pension wealth through the following drawdown options. The choice of the drawdown option will be made by the subscriber at the time of closure of a pension account after which fresh contributions will stop. Subscribers may opt for any one of the following options for the drawdown-

a) Systematic Payout Rate (SPR) (Default)

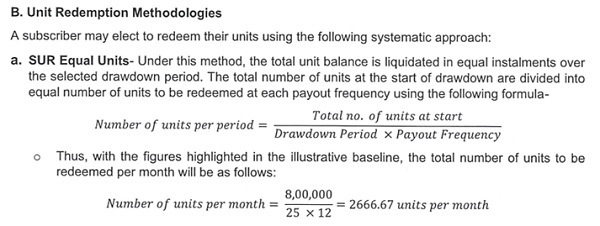

b) Systematic Unit Redemption- SUR-Equal Units

Details of the representative calculation methodology for the drawdown methods are presented at Annexure A and B.

4. Specific Guidelines:

| Parameter | Details |

| Eligibility | i. Subscribers of Government and Non-Government Subscribers (NGS) under NPS, who wish to receive systematic payouts from their designated pension corpus, up to maximum age of 85 years. |

| Options for Drawdown |

i. Subscribers opting for the drawdown options will also have the option of continuing with their existing pension fund.

ii. The subscriber shall have the option to switch their Pension Fund once in every two financial years. |

| Treatment of Corpus in theEvent ofDemise |

If a subscriber using the drawdown facility passes away during the payout phase, the remaining balance in their account, after accounting for any scheduled payments already made, will be paid in accordance with the PFRDA (Exits and Withdrawals under the National Pension System) Regulations, 2015, as amended from time to time. |

| Redemption Method |

The units from each asset class shall be redeemed for amount withdrawal in proportion to wealth in respective asset class. |

| Payout frequency |

i. Subscribers may elect to receive periodic payouts on a monthly, quarterly or annual basis.

ii. Upon the successful processing of a drawdown request, periodic payouts shall be initiated from the following month. iii. For subscribers opting for the Systematic Payout Rate (SPR), the payout rate and the resulting payout amount shall be reset annually. This reset will occur on the subscriber’s date of birth, based on the prevailing market value of the drawdown corpus. iv. The asset rebalancing as per the age brackets, would also occur as per subscriber’s date of birth, based on the prevailing market value of the drawdown corpus. |

| Charges | The charges shall be governed as per existing framework applicable to such schemes. |

| Residual Corpus | Under the SPR option of systematic income drawdown, there may be certain residual corpus left from the component utilized for obtaining the payouts at the end of the drawdown period. The subscriber will have the choice to:

a) Withdraw entire residual corpus as lump sum. b) Combine the residual corpus with the annuity component (if deferred) to purchase an annuity in line with the PFRDA (Exits and Withdrawals under the NPS) (Amendment) Regulations, 2025, as amended from time to time. |

5. Subscriber Disclosures

To ensure informed decision-making and mitigate risks associated with market-linked decumulation, all Pension Funds (PFs) and/or Central Record Keeping Agencies (CRAs) or any other intermediary as directed by the Authority from time to time, shall inter alia provide detailed disclosures on the following:

a) No guarantee or Assurance clause in respect of the periodic payouts

b) The pay outs are subject to market risk.

c) Illustration of benefits along with Residual corpus projection preferably through a calculator or a simulator on the website.

d) Subscriber shall receive a Retirement Income statement (separate from Tier I or Tier II statements) containing:

i. Reset Notification: For SPR subscribers, a notification on every birthday detailing the reset of systematic payouts based on the prevailing market value and new age based payout rate.

ii. Asset rebalancing summary: A report on the shift in asset classes (E, C, G) according to declining (RIF steady) glide paths.

Annexure — A

Methodology for Determining Systematic Payout Rates (SPR)

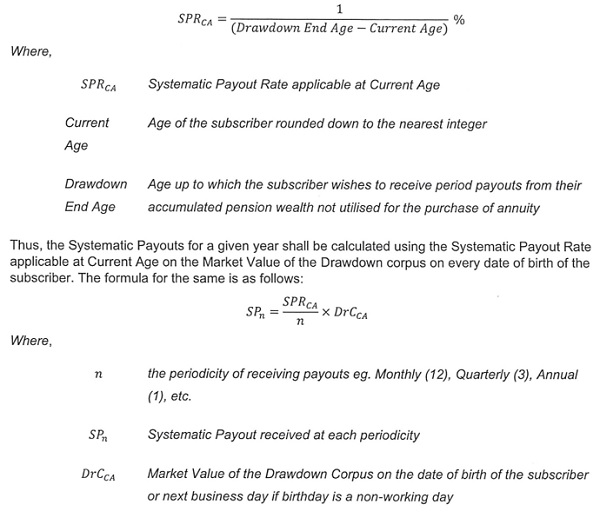

The various drawdown options allow a subscriber to receive a designated portion of their accumulated pension wealth “), at exit, through periodic payouts. This Annexure outlines the calculation for the age-wise maximum permissible Systematic Payouts (SP) under the SPR option of the drawdown facility.

A. Calculation of Systematic Payout Rate (SPR) and Systematic Payout

The Systematic Payouts (SP) shall be a factor of the Systematic Payout Rate applicable at a certain “Current Age” under the SPR option. The Systematic Payout Rate shall be dependent on the Drawdown End Age and the Current Age of the subscriber.

Reset of Systematic Payouts

- The Systematic Payouts (SP) will be reset on every birthday of the subscriber with the reset of the Systematic Payout Rate.

- The subscriber shall receive constant Systematic Payouts calculated using the above methodology from the period from his current date of birth up until his next date of birth.

B. Illustrative Table for Systematic Payout Rates as per Current Age-

For a subscriber exiting the system at age 60 and selecting to drawdown through SPR, up until the Drawdown End Age of 85 years, the age-wise Systematic Payout Rate shall be as per table below:

| Age | Payout Rate |

| 60 | 4.00% |

| 61 | 4.17% |

| 62 | 4.35% |

| 63 | 4.55% |

| 64 | 4.76% |

| 65 | 5.00% |

| 66 | 5.26% |

| 67 | 5.56% |

| 68 | 5.88% |

| 69 | 6.25% |

| 70 | 6.67% |

| 71 | 7.14% |

| 72 | 7.69% |

| 73 | 8.33% |

| 74 | 9.09% |

| 75 | 10.00% |

| 76 | 11.11% |

| 77 | 12.50% |

| 78 | 14.29% |

| 79 | 16.67% |

| 80 | 20.00% |

| 81 | 25.00% |

| 82 | 33.33% |

| 83 | 50.00% |

| 84 | 100.00% |

Annexure — B

Methodologies for Systematic Unit Redemption (SUR)

A. Illustrative Baseline

The following parameters serve as the basis for the calculations and examples provided herein:

| Parameter | Value |

| Corpus | Rs. 80 lakhs |

| NAV at the time of opting drawdown | 10.0000 |

| Units at the time of opting drawdown | 8,00,000.0000 |

| Age of exit | 60 years |

| Drawdown period | 25 years |

| Payout frequency | Monthly i.e. 12 per year. |