On 5th July 2024, the National Financial Reporting Authority (NFRA) issued Order No. 019/2024, addressing professional misconduct by M/s Singh Ajay & Co. and CA Priyank Mittal during the statutory audit of Vikas Proppant and Granite Limited for FY 2020-21. The order follows a Show Cause Notice from January 2024 and action initiated under Section 132(4) of the Companies Act, 2013, based on information from SEBI. NFRA’s investigation revealed multiple failures by the auditors, including inadequate audit planning, failure to verify opening balances, and not reporting material misstatements such as non-provisioning of expected credit loss on trade receivables and lack of depreciation charges. Other significant lapses included insufficient audit work, improper auditing of related party transactions, and failure to obtain external confirmations for trade receivables. Consequently, a penalty of Rs. 2,00,000 was imposed on CA Priyank Mittal and Rs. 3,00,000 on the audit firm, with CA Priyank Mittal also being debarred for two years from auditing any company or body corporate. This order will be effective 30 days from issuance.

Government of India

National Financial Reporting Authority

7th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. 019/2024 Date: 05.07.2024

In the matter of M/s Singh Ajay & Co. and CA Priyank Mittal, under Section 132(4) of the Companies Act 2013 read with Rule 11(6) of National Financial Reporting Authority Rules 2018

1. This Order disposes of the Show Cause Notice (`SCN’ hereafter) no. NF-23/41/2022 dated 18.01.2024, issued to M/s Singh Ajay & Co. (hereafter referred to as audit firm) and CA Priyank Mittal (ICAI Membership No. 405669), partner of M/s Singh Ajay & Co. (ICAI Firm registration no. 007495C), Lucknow, Uttar Pradesh (both collectively called as ‘Auditors’ hereafter). CA Priyank Mittal is a member of the Institute of Chartered Accountants of India (`ICAI’ hereafter) and was the Engagement Partner (`EP’ hereafter) for the statutory audit of Vikas Proppant and Granite Limited (`Vikas’ or `the company’ hereafter) for the Financial Year (TY’ hereafter) 2020-21.

2. This Order is divided into the following sections:

A. Executive Summary

B. Introduction & Background

C. Lapses in the conduct of audit

D. Specific Lapses by audit firm

E. Article of Charges of Professional Misconduct by the EP

F. Penalty & Sanctions

A. Executive Summary

3. National Financial Reporting Authority (NFRA) is India’s independent regulator, in respect of matters relating to accounting and auditing, of prescribed classes’ of entities broadly described as ‘Public Interest Entities’ (PIEs).

4. NFRA initiated action under Section 132(4) of Companies Act 2013 against the Auditor of Vikas for professional or other misconduct in relation to Vikas’s statutory audit for FY 2020-21, pursuant to information received from Securities and Exchange Board of India (SEBI hereafter) indicating possible failure of the statutory auditor in reporting accounting mis-statements and following the Standards of Auditing.

5. This Order finds that the auditor failed to meet the relevant requirements of the Standards on Auditing (‘SA’ hereafter) in respect of several significant areas, reflecting gross negligence and lack of due diligence to perform audit of a Public Interest Entity (PIE). These include:

a. Failure to plan the audit and understand the nature of the audited entity and its environment as per SA 300 and SA 315.

b. Failure to verify opening balances required as per SA 510.

c. Failure to report material misstatement due to non-provisioning of the ECL on trade receivables (Vikas had trade receivables of Rs. 171.46 crores in FY 2020-21 which was more than seven times the sales of Rs. 23.60 crores) and not charging depreciation on lease hold land and plant & machinery.

d. Failure to demonstrate sufficiency and appropriateness of audit work in several critical aspects of the audit of the Financial Statements i.e., determining materiality, failure to report on the entity’s ability to continue as a going concern, failure to determine TCWG and communicate with them and failure to assemble the Audit File.

e. Failure to carry out proper audit of Related Party Transactions (`RPTs’ hereafter) of Vikas (trade payables to related parties were high as 93.09% of total trade payables and trade receivables from related parties were 68.38% of total trade receivable).

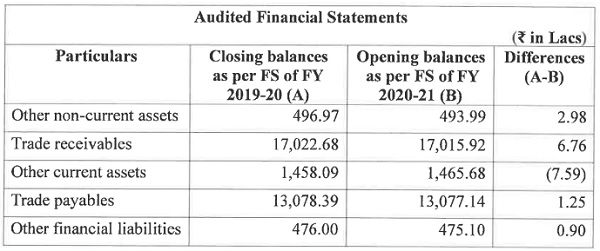

f. Failure to carry out external confirmation for Trade Receivables or any other alternative audit procedure to verify the audit assertions relating to Trade Receivables.

g. Failure of the audit firm to demonstrate compliance with the requirement of the Standards on Auditing concerning the Engagement Quality Control Reviewer.

6. Based on our investigation and proceedings under Section 132(4) of the Companies Act, 2013 and after giving the audit firm and EP an opportunity to present their case, we find the EP and Firm guilty of professional misconduct and impose through this Order a monetary penalty of Rs. 2,00,000/- (Two lakhs) on EP and Rs. 3,00,000/- (Three lakhs) on audit firm. In addition, the EP is debarred for two years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate. This Order will take effect after 30 days from its issue.

B. Introduction & Background

7. NFRA is a statutory authority set up under Section 132 of the Companies Act 2013 to monitor and enforce compliance of the auditing and accounting standards and to oversee the quality of service of the professions associated with ensuring compliance with such standards. NFRA is empowered under Section 132(4) of the Companies Act 2013 to investigate prescribed classes of companies and impose penalty for professional or other misconduct of the individual members or firms of chartered accountants.

8. The statutory auditors, both individuals and firms of Chartered Accountants, are appointed by the members of company under Section 139 of the Companies Act 2013. The statutory auditors, including the Engagement Partners and the Engagement Team that conduct the audit, are bound by the duties and responsibilities prescribed in the Companies Act, 2013 the rules made thereunder, the Standards on Auditing, including the Standards on Quality Control and the Code of Ethics, the violation of which constitutes professional misconduct, and is punishable with penalty prescribed under Section 132(4)(c) of the Companies Act 2013.

9. NFRA took up investigation under Section 132(4) of the Companies Act 2013 after receipt of a letter dated 23.11.2022 from SEBI regarding irregularities in the Related Party Transactions (RPT), non-provision of Expected Credit Loss (ECL) and non-charging of depreciation on lease hold land and plant & machinery during the statutory audit of Vikas during FYs 2018-19, 2019-20 & 2020-21.

10. As M/s Singh, Ajay & Co were the auditors of Vikas during FY 2020-21, NFRA vide letter dated 17.01.2023, sought the Audit File and other documents for the FY 2020-21 from the EP, who submitted the same on 02.03.2023. The company disclosed under Significant Accounting Policies in its Annual Report for the FY 2020-21, that it had prepared the Financial Statements (FS hereafter) in accordance with the Indian Accounting Standards (hereafter referred to as the ‘Ind AS’)2 as notified by Ministry of Corporate Affairs. On examination of the Audit Files and other documents, it was observed that the audit had prima facie been conducted in disregard of several SAs and relevant requirements of the Companies Act 2013. Despite this, the EP had issued an unmodified audit opinion in his Independent Auditor’s Report.

11. On being satisfied that there was sufficient cause to act under Section 132(4) of the Companies Act 2013, a SCN was issued to the EP and the Firm on 18.01.2024, asking them to show cause why action should not be taken for professional misconduct in the Statutory Audit of Vikas for the FY 2020-21. The EP was charged with professional misconduct of:

a) Failure to plan the audit and failure to understand the nature of the entity and its environment.

b) Failure to verify opening balances (as per SA 510).

c) Failure to determine materiality and performance materiality.

d) Failure to report the non-provisioning in respect of the Expected Credit Loss.

e) Failure to report on the entity’s ability to continue as a Going Concern.

f) Failure to evaluate the arm’s length pricing regarding the compliance of Section 177 & 188 of Companies Act, 2013 for the Related Party Transactions

g) Failure to report non-charging of depreciation of leasehold land and Plant and Machinery

h) Failure to assemble the Audit File within 60 days of the completion of the audit

i) Failure to obtain sufficient and appropriate audit evidence through external confirmations

j) Failure to determine appointment of Engagement Quality Control Reviewer (EQCR) (as per SA 220)

k) Failure to Determine TCWG and Communicate with them

12. The EP, vide letter dated 21.03.2024, requested a personal hearing which was held on 26.04.2024 through video conferencing wherein CA Priyank Mittal appeared on his own behalf as well as on behalf of the Firm and made submissions.

13. This Order is based on our review of the audit file, written response of the auditor, submissions made during the personal hearing and other material available on record. Each of the charges in the SCN is analysed and discussed herein below.

C. Lapses in the conduct of audit

Failure to plan the audit and failure to understand the nature of the entity and its environment

14. The auditors were charged with failure to plan the audit and failure to understand the nature of the entity and its environment. For performing audit in an effective manner, auditors were required to plan the audit of financial statements of Vikas in accordance with Para 3 and 8 of SA 3003. The Audit Strategy and Audit Plan must be documented in accordance with Para 11 of SA 300, but no such documentation is found in the Audit File submitted by EP vide letter dated 02.03.2023.

15. The auditors were also required to understand the nature of the business of Vikas by gaining an understanding of relevant industry, applicable regulatory structure etc. at macro level and gaining understanding of nature of the entity, its operations, its ownership, its governance & capital structure, and applicable financial reporting framework etc. at the entity level as required by para 11 of SA 3154. However, no audit documentation reflecting auditors understanding of the nature of the business of the entity was found in the audit file as required by para 11 of SA 300. The EP confirmed to NFRA vide letter dated 09.11.2023 (point no. 4) that there was no documentation available regarding his understanding of the audited entity & its environment and that most of the discussion were verbal and oral.

16. In his reply dated 21.03.2024 to the SCN, the EP submitted that the “audit was conducted under the risk and restrictions of COVID and during May-June 2021, some casualty happened at home. I started my audit from the 2nd LR. Due to some reasons, for some of my query’s management was not able to answer properly so I mentioned these points in Management Representation Letter which was earlier sent to you as Annexure No. 70″.

17. In his reply to NFRA the EP stated that, he started the audit from the 2nd LR5 (Limited Review). As per para 8 of SA 300, the auditor shall develop an audit plan that shall include a description of:

(a) The nature, timing and extent of planned risk assessment procedures, as determined under SA 315 “Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment”.

(b) The nature, timing and extent of planned further audit procedures at the assertion level, as determined under SA 330 “The Auditor’s Responses to Assessed Risks”.

(c) Other planned audit procedures that are required to be carried out so that the engagement complies with SAs.

18. It is evident from the Annual report of FY 2019-20 ( page number 15), that audit firm has given its consent to act as statutory auditors of the Company and has also given a certificate in accordance with Section 139, 141 and other applicable provisions of the Companies Act 2013 to the effect that their appointment, if made, shall be in accordance with the conditions prescribed and that they are eligible to hold office as Statutory Auditors of the Company. The audit firm was appointed as the statutory auditor for the FY 2020-21 onwards and the EP has given his audit report accordingly. In light of this, the defence that the audit was conducted after second Limited Review is irrelevant and is rejected.

19. Further, the EP’s reply “Due to the reasons, for some of my query’s management was not able to answer properly so I mentioned these points in Management Representation Letter “is not acceptable as it appears from his reply that the Management Representation Letter (MRL) was prepared by EP himself (MRL is a document which is prepared by management).

20. Considering the above, the charge that the auditors failed to comply with the provisions of SA 300 and SA 315 stands established.

Failure to verify opening balances (as per SA 510)

21. The auditors were charged with failure to verify opening balances. As per para 3 of SA 5106, the objective of the auditor with respect to opening balances is to obtain sufficient appropriate audit evidence about whether:

(a) Opening balances contain misstatements that materially affect the current period’s financial statements; and

(b) Appropriate accounting policies reflected in the opening balances have been consistently applied in the current period’s financial statements, or changes thereto are properly accounted for and adequately presented and disclosed in accordance with the applicable financial reporting framework.”

22. On the examination of the audit file, it has been noted that there were no work papers in relation to the verification of the Opening Balances even though FY 2020-21 was the first year of audit of Vikas by Singh Ajai & Co. The EP acknowledged vide letter dated 09.11.2023 (point no. 14) that opening balances were not verified.

23. In his reply dated 21.03.2024 to the SCN, EP submitted that “as per Para A2 of page no 5 of SA 510, the current auditor can place reliance on the closing balances contained in the financial statements for the preceding period, except when during the performance of audit procedures for the current period the possibility of misstatements in opening balances is indicated;” and that since he was appointed the auditor from the 2nd LR, he relied on the work of previous auditor; and that there was no misstatement in the previous audit report (Audit report of LR 1 of FY 2020-21) with regard to opening balances.”

24. It has been noted that there are differences between the closing balances (as per FS of FY 2019-20) and opening balances (as per FS of FY 2020-21) of Other non-current assets, Trade receivables, Other current assets, Trade payables and Other financial liabilities as on 31.03.2020. The auditors had disclosed figures for these balances as under:

Table 1

Audited Financial Statements

25. It is noted that the Audit Firm was appointed on 30.09.2020 for statutory audit of Vikas for FY 2020-21 and this was the first year of Audit for auditors. As per para 5 of SA 510, the auditor shall read the most recent financial statements and the predecessor auditor’s report thereon for information relevant to opening balance, including disclosures. The EP was the statutory auditor of FY 2020-21, so he should have verified the previous financial statements and auditor’s report to verify the opening balances. The contention of the EP that he was appointed on 30.09.2020 i.e. after 1st LR (Limited Review ended on 30.06.2020) is not tenable in view of the position discussed in para 18 above.

26. As para 6 of SA 510, The auditor shall obtain sufficient appropriate audit evidence about whether the opening balances contain misstatements that materially affect the current period’s financial statements by performing one or more of the following:

(i) Where the prior year financial statements were audited, perusing the copies of the audited financial statements including the other relevant documents relating to the prior period financial statements;

(ii) Evaluating whether audit procedures performed in the current period provide evidence relevant to the opening balances; or

(iii) Performing specific audit procedures to obtain evidence regarding the opening balances.

27. As there is no evidence in the audit file whether auditors have performed the procedure to verify the opening balances despite difference as shown in Table 1, the charge that auditors failed to obtain sufficient appropriate audit evidence about opening balances and violation of SA 510 stands established.

Failure to determine Materiality and Performance Materiality

28. The auditors were charged with failure to determine Materiality and Performance Materiality. As per Para 10 of the SA 3207, while establishing the overall audit strategy, the auditor shall determine Materiality for the financial statements as a whole. Further, as per Para 11 of the SA 320, the auditor should also determine Performance Materiality for purposes of assessing the risks of material misstatement and determining the nature, timing, and extent of further audit procedures.

29. However, there was no documentation in the audit file pertaining to the determination of Materiality and Performance Materiality. The EP confirmed to NFRA vide letter dated 09.11.2023 (point no. 5) that there is no documentation available for determination of Materiality and Performance Materiality. In his reply dated 21.03.2024 to the SCN the EP did not offer any comment on lack of documentation regarding determining Materiality and Performance Materiality.

30. Considering the above, the charge that the auditors failed to determine materiality and performance materiality as required by SA 320 stands established.

Failure to report the non-provisioning in respect of the Expected Credit Loss

31. The auditors were charged with failure to report non-provisioning in respect of Expected Credit Loss (ECL). The financial statements do not reveal any provision made on account of ECL on trade receivables as per Ind AS 1098. Table 2 shows that the Trade Receivables had been outstanding for a long time, as the Trade Receivables as at 31.03.2021 (Rs. 171.46 crore) were twice the combined sales for the last four years (Rs. 83.33 crore). Therefore, it is apparent that the outstanding Trade Receivables required provisioning.

Table 2

| (Rs. in crores) | |||

| No. | Financial Year | Sales | Trade Receivables |

| 1 | 2020-21 | 23.60 | 171.46 |

| 2

3 4 |

2019-20 | 6.96 | 170.15 |

| 2018-19 | 52.77 | 175.54 | |

| 2017-18 | Nil 167.21 | ||

32. The financial statements for FY 2020-21 do not reveal any provisioning for ECL on trade receivables of Rs. 171.46 crores as per Ind AS 109. Even though the trade receivables exceeded seven times the sales for FY 2020-21, the auditors failed to examine the matter with professional scepticism. There was no ageing analysis of trade receivables in the audit file and there was no testing for ECL either. The EP also confirmed to NFRA vide letter dated 09.11.2023 (point no. 12 &13) that there was no ECL provisioning policy in Vikas, hence ECL provisioning was not done, and no audit testing was carried out for the same. The EP did not report the non-provisioning by Vikas in the financial statements. In reply dated 21.03.2024 to the SCN as well the EP did not offer any comment on failure to report the non-provisioning in respect of the ECL.

33. As per Ind AS 109 companies are required to make ECL provisioning for trade receivables. Not having a documented ECL provisioning policy does not mean that no provision is required. In the current case since the trade receivable were outstanding for a long time the company should have made ECL provisions and since the company did not do so, it was the auditor’s duty to report the failure of the company in making ECL provisioning as per Ind AS 109.

34. Considering the above, the charge that the auditors failed to report the non-compliance by the company regarding ECL provision as per Ind AS 109 stands established.

Failure to report on the entity’s ability to continue as a Going Concern

35. The auditors were charged with failure to report on the entity’s ability to continue as a Going Concern. The Company had incurred a loss of 211.38 crore during FY 2020-21 and had a bank balance of only 23.12 lakhs as on 31.03.2021 which was the same as on 31.03.2020. The EP admitted in his statement dated 19.09.2022 recorded before SERI that there was no movement of funds with respect to sales and purchases and the salaries of the employees were paid by the sister concerns Vikas WSP Ltd and Vikas Chemigum Ltd. The trade receivables of 2171.46 crores was 91.4% of the net worth of Vikas as on 31.03.20210187.64 crore), but the sales were only 223.60 crores. Net current liability position was adverse (current assets of 2195.94 crore were much less than the current liabilities of n00.10 crore). This indicated that there were issues regarding the going concern status of the company, that were not considered by the EP.

36. As per para 9 of SA 5709, Going Concern “The objectives of auditor are:

a) To obtain sufficient appropriate audit evidence regarding, and conclude on, the appropriateness of management’s use of the going concern basis of accounting in the preparation of the financial statements;

b) To conclude, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern; and

c) To report in accordance with this SA”.

37. Further as per para 21 of SA 570, “If the financial statements have been prepared using the going concern basis of accounting but, in the auditor’s judgment, management’s use of the going concern basis of accounting in the preparation of the financial statements is inappropriate, the auditor shall express an adverse opinion”.

38. On the examination of the audit file, no documentation has been found regarding the appropriateness of the management’s use of going concern basis in the preparation of financial statements. The EP also confirmed the same to NFRA vide letter dated 09.11.2023 (point no. 15). In his reply dated 21.03.2024 to the SCN also the EP did not offer any comment on failure to report on the entity’s ability to continue as a Going Concern.

39. Considering the above, the charge that the auditors failed to report the non-compliance by the company regarding the appropriateness of the management’s use of going concern basis in the preparation of financial statements as per SA 570 stands established.

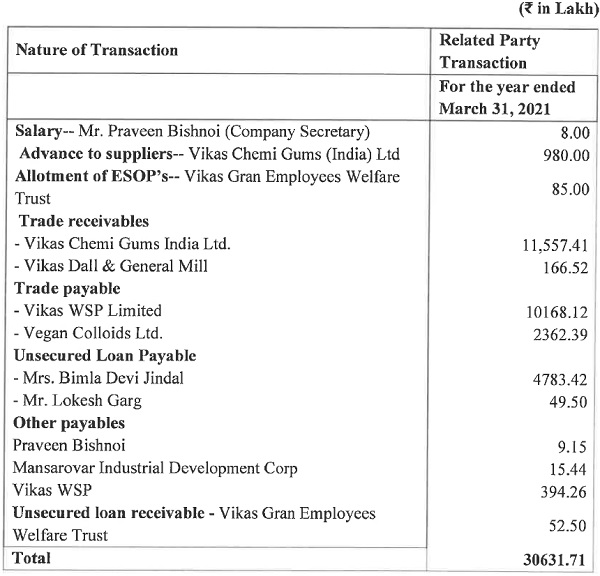

Failure to evaluate the arm’s length pricing regarding the compliance of Section 177 & 188 for the Related Party Transactions

40. The auditors were charged with not having evaluated the arm’s length pricing in compliance with Section 177 & 188 for Related Party Transactions. The details of Related Party Transactions disclosed in the financial statement for the FY 2020-21 (page no 112 & 113 of the Annual Report) were as follows (Table 3):

Table 3

41. It can be seen from Table 3 that: –

(a) Related party transactions disclosed in the financial statement for the FY 202021 under different headsl° were 2306.32 crores which were significant keeping in view the balance sheet size of 2388.89 crores.

(b) The total trade and other payables as on 31.03.2021 were 2134.61 crores, out of which Rs. 130.73 crore (97.12%) were with related parties.

(c) The total trade receivable as on 31.03.2021 were 2171.46 crore, out of which Rs. 117.24 crore (68.38%) were from related parties.

However, no audit documentation in the audit file was found regarding the arm’s length testing carried out for the Related Party Transactions.

42. Further, the entire sales of 223.60 crore during FY 2020-21 were made to the related parties but were not disclosed under Related Party Transactions. The EP vide letter dated 09.11.2023 (point no. 18 & 19) has admitted this.

43. The EP in the Independent Auditor’s Report under point (xiii) of Annexure A (page 91 of annual report) of FY 2020-21 had stated that, transactions with the related parties are in compliance with section 177 and 188 of Act, where applicable and the details have been disclosed in the notes to the standalone financial statements, as required by the applicable accounting standards”.

44. SA 55011 lays down requirements regarding audit of related party transactions and provides application guidance. However, in the Audit file submitted by the auditors there were no audit work papers in respect of identification of related party, nature of related party relationships and the details of related party transactions and outstanding balances which is in contravention of the provisions of SA 23012 and SA 550.

45. There are no audit work papers in respect of identification of related party, nature of related party relationships and the details of related party transactions and outstanding balances. In reply dated 21.03.2024 to the SCN the EP did not offer any comment on non-evaluation of the arm’s length pricing carried out for Related Party Transactions. This is a serious omission. Non-evaluation of related party transactions has been viewed seriously by International Regulators as well. For example, the PCAOB, the US Regulator”, censured and imposed monetary penalty of $ 30,000 collectively on the firm and respondents in the Matter of Seale and Beers CPAs, LLC, and Charlie B. Roy, CPA, for their failure inter alia to obtain, or ensure that the engagement team obtained, sufficient appropriate audit evidence for significant items reported in the financial statements, including related party transactions and expenses.

46. Considering the above, the charge that the auditors failed to evaluate the arm’s length pricing and non-disclosure of all Related Party Transactions as per Section 177 & 188 of the Companies Act, 2013 and SA 550 stands established.

Failure to report non charging of depreciation of leasehold land and Plant & machinery

47. The auditors wcre charged with failure to report non charging of depreciation on lease hold land and plant & machinery. The EP had identified and reported the following material weakness in the Internal Financial Controls for issuing the Report on the Internal Financial Controls under Clause (i) of Section 143(3) of the Companies Act, 2013: –

“The Company has not provided the Depreciation on its fixed assets, due to non-operation in the company.”

48. However, the EP had failed to qualify the Independent Auditor’s Report on the ‘Audit of Financial Statements’ even though he had identified material weakness in the internal controls of the company. The EP failed to consider the impact on the account of the non-charging of depreciation on the fixed assets. As the company had already reported a loss of Rs. 11.38 crore in FY 2020-21, the charge of the depreciation on the fixed assets would have increased the losses of the company.

49. It is noted that leased land, valued at 281.62 crore as on 31.03.2021, has not been subjected to depreciation as required in Ind AS 11614 for the FY 2020-21. Para 31 of Ind AS 116 states that “lessee shall apply depreciation to the property in depreciating the right-of-use asset”. As per the annual report for FY 2020-21 (page No. 97), the company had stated that “The Company is into business into the mining of Granite Blocks and manufacturing of Proppants”. It is evident from the valuation report that this land was meant for mining quarrying which are subject to depreciation as per the aforesaid standard. However, no depreciation had been charged on the leased land.

50. It is further noted that the Plant & Machinery valued at 295.46 crore as on 31.03.2020 & 31.03.2021, had not been subjected to depreciation as required in Ind AS 1615 for the FY 2020-21. The EP also confirmed the same to NFRA vide letter dated 09.11.2023 (point no. 8 & 10 and point no 5 of `Annexure 71′) that ‘As plant was not in operation during FY 2020-21, hence no depreciation has been charged on assets’ and there is no documentation available in this regard.

51. In his reply dated 21.03.2024 to the SCN, EP submitted that with respect to ‘false and misleading statement in the financial statement’ as mentioned by your good self (in para 26 to 32 of SCN) regarding non-charging of depreciation, my opinion is that it does not form the basis of qualification of audit report. For the purpose of reporting, the fact has been duly mentioned in ICFR and along with the notes of published results. Had my intentions been wrong it should not have disclosed anywhere”.

52. As per para 7 of SA 70516, the auditor shall qualify his opinion when, the auditor, having obtained sufficient appropriate audit evidence, concludes that misstatement, individually or in the aggregate, are material, but not pervasive, to the financial statements. Further, as per para 21 of SA 705, if there is a material misstatement of the financial statements that relates to specific amounts in the financial statements, the auditor shall include in the basis for opinion section a description and quantification of the financial effects of the misstatement, unless impracticable. If, it is not practicable to quantify the financial effects, the auditor shall so state in this section.

53. As per para 55 of Ind AS 16 “Depreciation of an asset begins when it is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management. Depreciation of an asset ceases at the earlier of the date that the asset is classified as held for sale (or included in a disposal group that is classified as held for sale) in accordance with Ind AS 105 and the date that the asset is derecognised. Therefore, depreciation does not cease when the asset becomes idle or is retired from active use unless the asset is fully depreciated”.

54. The EP has identified the issue of non-charging of depreciation for the leased land and the plant and machinery as he reported the same in ICFR but failed to report in his Independent Auditor’s Report as required by SA 705 and certified that the financial statements give a true and fair view despite the material misstatement.

55. Considering the above, the charge that the auditors made a false statement in the Independent Auditor’s Report that Vikas was in conformity with the Indian Accounting Standards (Ind AS), despite the violation of Ind AS 116, Ind AS 16, stands established.

Failure to assemble the Audit File within 60 days of the completion of the audit

56. The auditors were charged with failure to assemble the Audit File within 60 days of the completion of the Para 75 of SQC117 read with para A21 of SA 230 states that “an appropriate time limit within which to complete the assembly of the final audit file is ordinarily not more than 60 days after the date of the auditor’s report”. The date of Independent Auditor’s Report is 23.06.2021 for FY 2020-21. The EP has failed to comply with the provisions of SA 230 and SQC1 as explained in the subsequent paras.

57. As per the submission made by the EP vide email dated 25.04.2023 addressed to NFRA it is stated that “due to the long hospitalization and death of my father in law during the period of May and June-21 ginalization of audit period) documents remain scattered at different locations and in spite of my best efforts I am not able to make up some of them”. The EP in most of submissions made vide letter dated 09.11.2023 had admitted that no documentation was made while performing the statutory audit of

58. Para 75 of SQC1 read with para A21 of SA 230 states that “an appropriate time limit within which to complete the assembly of the final audit file is ordinarily not more than 60 days after the date of the auditor’s report”. Therefore, the auditors failed to comply with the provisions of SA 230 and SQC1, and were charged accordingly.

59. NFRA vide its letter dated 17.01.2023 had requested the auditors to submit the audit file by 02.02.2023. In response, the EP vide letter dated 05.02.2023 had requested one month extension of time to submit the audit file but was given time till 24.02.2023. The EP had submitted the audit file on 02.03.2023 but affidavit regarding completeness of audit file was not submitted along with audit file as required by NFRA vide letter dated 17.01.2023.

60. NFRA vide its mail dated 17.04.2023 requested the EP to submit the affidavit regarding completeness of audit file within 10 days. In response, EP vide email dated 25.04.2023 to NFRA had accepted that the submitted audit file was not complete.

61. It is evident that the audit file was not compiled within 60 days of completion of audit as required by SA 230 and SQC1. The audit documentation acts as a basis of the auditor’s report and as evidence that the audit was planned and performed in accordance with SAs and applicable legal and regulatory requirements. In the absence of proper audit documentation, there is no way for us to ascertain whether the required audit procedures were performed at all.

62. Considering the above, the charge that the auditors failed to assemble the Audit File within 60 days of the completion of the audit stands established.

Failure to obtain sufficient and appropriate audit evidence through external confirmations

63. The auditors were charged with failure to obtain sufficient and appropriate audit evidence through external confirmations. As on 31.03.2021 the company had a bank balance of 23.12 Lakhs, trade payable of 134.61 crore, and advance to suppliers of 20.43 crores. On examination of the audit work papers it was seen that no external confirmations of bank balances and third-party balance confirmation for trade payables, trade receivables and advance to suppliers was obtained by the EP. The EP also confirmed the same to NFRA vide letter dated 09.11.2023 (point no. 11) and stated that `Third party balances are subject to confirmation and responsibility of the management’. In the absence of external confirmation, the auditor is required to perform alternative audit procedures to obtain relevant and reliable audit evidence.

64. In absence of external confirmation from third party and any alternative procedure adopted by the auditors, the charge that the auditors failed to comply with the provisions of SA 50518 stands established.

Failure to determine appointment of Engagement Quality Control Reviewer (EQCR)

65. The auditors failed to determine the appointment of EQCR for the engagement of the audit of the Company which was required since Vikas was a listed Company during FY 2020-21. Para 19(a) of SA 22019 requires determination of appointment of an EQCR for audit of listed entities.

66. In reply dated 21.03.2024 to the SCN the EP did not offer any comment on appointment of EQCR.

67. SA 220 and SQC 1 lay significant emphasis on the appointment of EQCR, the work to be done by EQCR and documentation to be carried out by the EQCR. Vide para 7(b) of SA 220, engagement quality control review is defined as “process designed to provide an objective evaluation, before the report is issued, of the significant judgments the engagement team made and the conclusions they reached in formulating the report”.

68. Para 64 of SQC 1 casts a duty upon the EQCR partner to review important working papers relating to the significant judgments that the engagement team made and the conclusions they reached. Para 66 of SQCI requires that the engagement quality control reviewer conducts the review in a timely manner at appropriate stages during the engagement so that significant matters may be promptly resolved to the reviewer’s satisfaction before the report is issued. Paras 68-72 of SQC1 prescribe the criteria for the eligibility of engagement quality control reviewers and lay down the guidelines for ensuring his independence and objectivity for the assigned work of quality control in the engagement. For the listed entities, the SA 220 [Para 19(a)] makes it mandatory to ensure appoint an EQCR.

69. Non-appointment of EQC Reviewer has been viewed seriously by international regulators as well. For example, the PCA0B2° , the US Regulator, charged public accounting firm Stein & Company, LLP (Audit Firm) for its failure in audit of Health Talk Live, Inc. (“Health Talk”) noting that “The Firm improperly issued the audit report without obtaining an engagement quality review and concurring approval of issuance and thus violated Auditing Standard No. 7, Engagement Quality Review (“AS 7″)”. For this misconduct, PCAOB censured the Firm and imposed a civil money penalty of $5000. Similarly in another matter of Halperin Ilanit CPA (“Firm”) and Ilanit Halperin, PCA0B2‘ among other things stated that “The Firm failed to obtain engagement quality reviews for any of the Issuer Audits, and improperly permitted Cuentas, Enigma, and SuperCom to use its audit reports for the Issuer Audits without having obtained concurring approval of issuance from an engagement quality reviewer” and imposed a civil money penalty in the amount of $200,000 jointly and severally, on the Firm and Halperin; revoking the Firm’s registration and requiring Halperin to complete 40 hours of continuing professional education.

70. Considering the above, the charge that the auditors failed to comply with the provisions of SA 220 regarding appointment of EQCR stands established.

Failure to Determine TCWG and Communicate with them

71. The auditors were charged with failure to Determine TCWG and Communicate with them. No minutes of meeting or record of discussions with Those Charged With Governance (TCWG) were found in the audit file, as is required under SA 26022, Communication with Those Charged with Governance. No documentation was available regarding the communication made with TCWG required by SA 260. The EP also confirmed vide letter dated 09.11.2023 (point no.7) that there is no documentation available regarding ‘Communication with Those Charged with Governance’ and there was no documentation of communication made with the TCWG regarding the weakness identified in the internal controls (point no. 9). In reply dated 21.03.2024 to the SCN the EP did not offer any comment on failure to Determine TCWG and Communicate with them.

72. Considering the above, the charge that the auditors failed to comply with the provisions of SA 260 regarding appointment of EQCR stands established.

73. Failure to appropriately communicate with Audit Committee (which is a part of the TCWG) has been viewed seriously by international regulators too. For example, PCAOB, the US Regulator, charged the public accounting firm L.L. Bradford & Company, LLC (Audit Firm) for its failure to communicate with the audit committee during the audit of WebXU Inc.’s (“WebXU”) and noted that the “Firm also violated a PCAOB rule that requires a registered public accounting firm to communicate, in writing, to the audit committee……….. ” For this misconduct among others, the PCAOB censured the Firm, revoked its registration, and imposed a civil money penalty of $12500.

D. Specific Lapses by audit firm

74. The audit firm was appointed the statutory auditor of the company. The powers and duties of the statutory auditors have been prescribed under Section 143 of the Companies Act, 2013. The duties include making his report to the members of the company after taking into account the provisions of the Companies Act, 2013 the accounting and auditing standards (subsection 2); stating in his report and expressing opinion on matters listed in subsection 3; stating the reasons, if any of the matters required to be included in the audit report under this section is answered in the negative or with a qualification (subsection 4); complying with the auditing standards (subsection 9); and reporting to the Central Government matters which he believes involve the offence of fraud (subsection 12).

75. Paragraph 2 of SA 220 stipulates that Quality Control Systems, policies and procedures are the responsibility of the audit Para 6 of SA 220 states that the objective of the auditor is to implement quality control procedures at the engagement level that provide the auditor with reasonable assurance that (a) The audit complies with professional standards and regulatory and legal requirements and (b) The auditor’s report issued is appropriate in the circumstances.

76. Para 3 of SQC 1 states that the firm should establish a system of quality control designed to provide it with reasonable assurance that the firm and its personnel comply with professional standards and regulatory and legal requirements, and that reports issued by the firm or engagement partner(s) are appropriate in the circumstances. Para 7 of SQC-1 states that the firm’s system of quality control should include policies and procedures addressing (a) Leadership responsibilities for quality within the firm. (b) Ethical requirements (c) Acceptance and continuance of client relationships and specific engagements (d) Human resources (e) Engagement performance (f) Monitoring.

77. The lapses enumerated in SCN, and discussed in the foregoing paragraphs indicate that the Audit Firm failed to achieve the central purpose of the audit, and that there was no adequate basis to issue the audit report asserting that the audit was conducted in accordance with the SAs and ethical requirements and therefore we conclude that the Audit Firm failed to fulfil its duties prescribed under Section 143 of the Act. In addition, the audit firm remains responsible for all the lapses of EP, as detailed in the foregoing paragraphs as the EP conducted the audit on behalf of the audit firm, which was the statutory auditor of the company appointed under Section 143 of the Act.

78. In his reply dated 21.03.2024 to the SCN the EP submitted that “Total fees received by the firm from audit of Vikas Proppant and Granite Limited was and I re- ceived a total remuneration of from the firm during the FY 2020-21. How- ever, there was no specific remuneration for execution of audit of Vikas proppant and Granite Limited which I have received from the firm. My humble submission is that as I was the Engagement Partner and I solely executed the audit along with my staff Further, I am solely responsible for the inadvertent mistakes in the audit. No other partner was connected in execution of the audit. Hence reply of the firm is not attached herewith”.

79. As per para 3 of SQC 1, the firm should establish a system of quality control designed to provide it with reasonable assurance that the firm and its personnel comply with professional standards and regulatory and legal requirements, and that reports issued by the firm or engagement partner(s) are appropriate in the circumstances.

80. As discussed above, the Audit Firm has made departure from the Standards and the Companies Act, 2013 in the conduct of the audit of Vikas for FY 2020-21. The poor quality of audit, incomplete documentation and misleading responses further compound the professional misconduct on the part of the Audit Firm. Based on the foregoing discussion and analysis, we conclude that the Audit Firm has committed professional misconduct, as defined in the Chartered Accountant Act, 1949. In an audit engagement assigned to an Audit Firm, the responsibility of the Audit Firm is to ensure that its systems and processes are conducive to a high-quality audit in compliance with the Law and Professional Standards. We find that the Firm has failed in this regard.

E. Articles of Charges of Professional Misconduct by the Auditors

81. As discussed in the foregoing paragraphs, the EP has made departures from the Standards and in his conduct of the audit of Vikas Proppant & Granite Limited for the FY 2020-21. Considering the foregoing discussion, our findings on each article of charge listed out in the SCN, are stated below:

(a) The EP committed professional misconduct as defined by clause 5 of Part I of the Second Schedule of the Chartered Accountant Act, 1949 which states that a Chartered Accountant is guilty of professional misconduct when he ‘tails to disclose a material fact known to him which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement where he is concerned with that financial statement in a professional capacity”. This charge is proved as the EP failed to disclose in his report the material non-compliances by the company as explained in Para 31-55

(b) The EP committed professional misconduct as defined by clause 6 of Part I of the Second Schedule of the Chartered Accountant Act, 1949 which states that a Chartered Accountant is guilty of professional misconduct when he ‘fails to report a material misstatement known to him to appear in a financial statement with which he is concerned in a professional capacity”. This charge is proved as the EP failed to disclose in his report the material non-compliances by the company as explained in Para 31-55

(c) The EP committed professional misconduct as defined by clause 7 of Part I of the Second Schedule of the Chartered Accountant Act, 1949 which states that a Chartered Accountant is guilty of professional misconduct when he “does not exercise due diligence or is grossly negligent in the conduct of his professional duties”.

This charge is proved as the EP failed to exercise due diligence in the audit of the company in accordance with the SAs and applicable regulations, as explained in Para 31-73 above.

(d) The EP committed professional misconduct as defined by clause 8 of Part I of the Second Schedule of the Chartered Accountant Act, 1949 which states that a Chartered Accountant is guilty of professional misconduct when he “fails to obtain sufficient information which is necessary for expression of an opinion, or its exceptions are sufficiently material to negate the expression of an opinion”.

This charge is proved as the EP failed to conduct the audit in accordance with the SAs and applicable regulations and failed to analyse and report the appropriateness of accounting policy Para 14-73 above.

(e) The EP committed professional misconduct as defined by clause 9 of Part I of the Second Schedule of the Chartered. Accountant Act, 1949 which states that a Chartered Accountant is guilty of professional misconduct when he “fails to invite attention to any material departure from the generally accepted procedure of audit applicable to the circumstances”.

This charge is proved since the EP failed to conduct the audit in accordance with the SAs as explained in Para 31-46 & 56-70 above.

82. In addition to above, the Audit Firm has committed Professional Misconduct as defined in Section 132(4) of the Companies Act, 2013 read with Section 22 of the Chartered Accountant Act, 1949 as amended from time to time, by failing to exercise due diligence and being grossly negligent in the conduct of the statutory audit of the company, significantly in respect of matters explained at Section C and Section D above and thus, violated the SAs and SQC 1.

83. Therefore, we conclude that the charges of professional misconduct against the EP (CA Priyank Mittal) and the audit firm (M/s Singh Ajay & Co.) enumerated in the SCN dated 18.01.2024 stand proved based on our analysis of the evidence in the Audit File, the Audit Report issued by auditors, the submissions made by auditors, the annual report of Vikas for the FY 2020-21 and other materials available on record.

F. Penalty & Sanctions

84. It is the duty of an auditor to conduct the audit with professional scepticism and due diligence and report his opinion in an unbiased manner. Statutory audits provide useful information to the stakeholders and public, based on which they make their decisions on their investments or do transactions with the public interest entity’.

85. Section 132(4) of the Companies Act, 2013 provides for penalties in a case where professional misconduct is proved. The seriousness with which proven cases of professional misconduct are to be viewed, is evident from the fact that a minimum punishment is laid down by the law.

86. The EP in the present case was required to ensure compliance with SAs to achieve the necessary audit quality and lend credibility to Financial Statements. As we have explained in this Order, deficiency in the conduct of Audit, abdication of responsibility and inappropriate conclusions on the part of CA Priyank Mittal establish his professional misconduct.

87. Section 132(4)(c) of the Companies Act 2013 provides that National Financial Reporting Authority shall, where professional or other misconduct is proved, have the power to make order for—

(A) imposing penalty of— (I) not less than one lakh rupees, but which may extend to five times of the fees received, in case of individuals; and (II) not less than five lakh rupees, but which may extend to ten times of the fees received, in case of firms.

(B) debarring the member or the firm from—(I) being appointed as an auditor or internal auditor or undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate; or (II) performing any valuation as provided under Section 247 of Companies Act, 2013, for a minimum period of six months or such higher period not exceeding ten years as may be determined by the National Financial Reporting Authority.

88. As per the information furnished by CA Priyank Mittal vide email dated 21.03.2024, the audit fees of Vikas for the FY 2020-21 was in FY 2020-21 and total remuneration received from firm during FY 2020-21 was

89. Considering the proven professional misconduct, the nature of violations, principles of proportionality and deterrence against future professional misconduct, we in exercise of powers under Section 132(4)(c) of the Companies Act, 2013, hereby order:

I. Imposition of a monetary penalty of Rs. 3,00,000/- (Three Lakhs) upon the Audit Firm M/s Singh Ajay & Co.

II. Imposition of a monetary penalty of Rs. 2,00,000/- (Two Lakhs) upon CA Priyank Mittal.

III. In addition, CA Priyank Mittal is debarred for two years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate;

90. This Order will become effective after 30 days of its issue.

Sd/-

(Dr. Ajay Bhushan Prasad Pandey)

Chairperson

Sd/-

(Dr. Praveen Kumar Tiwari)

Full-Time Member

Sd/-

(Smita Jhingran)

Full-Time Member

Authorised for issue by the National Financial Reporting Authority.

(Vidhu Sood)

Secretary

Notes:

1 Rule 3 of NFRA Rules, 2018

2 Applicable financial reporting framework was the ‘Indian Accounting Standards (Ind AS)’ prescribed by Ministry of Corporate Affairs under Section 133 of Companies Act, 2013 (the “Act”) read with Companies (Indian Accounting Standards (Ind AS)) Rules, 2015 and other relevant provisions of the Act.

3 Standards on Auditing (SA) 300, Planning and Audit of Financial Statements

4. Standards on Auditing (SA) 315, Identiniing and Assessing the Risks of Material Misstatement Through Understanding the Entity and Its Environment

5 Appointed on 30.09.2020.

6 Standards on Auditing (SA) 510, Initial Audit Engagement – Opening Balances

7 Standards on Auditing (SA) 320, Materiality in Planning and Performing Audit

8 Indian Accounting Standard (Ind AS) 109, Financial Instruments

9 Standards on Auditing (SA) 570, Going Concern

1° loans & advances, Allotment of ESOP’s, Trade receivable, Trade payable, Unsecured loan payable, Other payable, Unsecured loan etc. as disclosed in note no. 26 of financial statement.

11 Standards on Auditing (SA) 550, Related Parties

12 Standards on Auditing (SA) 230, Audit Documentation

13 Public Company Accounting Oversight Board (PCAOB) Release No. 105-2017-038

14 Indian Accounting Standards (Ind AS) 116, Leases

15 Indian Accounting Standards (Ind AS) 16, Property, Plant and Equipment

15 Standards on Auditing (SA) 705, Modifications to the Opinion in the Independent Auditor’s Report

17 Standard on Quality Control (SQC) 1, Quality Control for Firms that Perform Audits and Reviews of Historical Financial Information, and Other Assurance and Related Services Engagements

18 Standards on Auditing (SA) 505: External Confirmations

19 Standards on Auditing (SA) 220: Quality Control for an Audit of Financial Statements

20 PCAOB release No. 105-2015-040 dated 03.12.2015.

21 PCAOB Release No. 105-2024-012 dated 19.03.2024.

22 Standards on Auditing (SA) 260, Communication with Those Charged with Governance

23 Public interest entity as defined in Rule 3 of NFRA Rules 2018