Securities and Exchange Board of India (SEBI) has released a consultation paper addressing the treatment of unclaimed funds and securities held by Trading Members (TMs). Under existing guidelines, TMs must settle client credit balances periodically. If clients are untraceable, TMs are required to make reasonable efforts to contact them and maintain an audit trail. For securities, margin pledges must be created in the Depository system, and securities must be credited directly to clients’ demat accounts. SEBI has introduced various safeguards, including the prohibition of off-market transfers and automatic pledging of unpaid securities. However, in cases where securities cannot be transferred due to incomplete information or untraceable clients, affected demat accounts are marked frozen.

The proposed mechanism defines unclaimed funds and securities as those that could not be credited due to unreachable clients or inactive accounts. TMs must attempt to contact clients through available channels and, if unsuccessful, must upstream unclaimed funds to Clearing Corporations (CCs). Additionally, a Designated Stock Exchange (DSE) will handle the transfer of unclaimed assets, and a Regulatory Oversight Committee will monitor implementation, with half-yearly reports submitted to SEBI.

SEBI invites public comments on the proposal until March 4, 2025, via its official portal or email. The feedback will help refine the policy to ensure the timely return of unclaimed funds and securities to rightful owners.

Securities and Exchange Board of India

Consultation Paper on “Treatment of unclaimed funds and securities of clients lying with Trading Members (TMs)”

Feb 11, 2025 | Reports : Reports for Public Comments

Objective

To protect the interest of investors, a mechanism to be introduced for treatment of unclaimed funds and securities of investors lying with the TMs.

Background:

For Funds Leg

1. As per the existing SEBI guidelines, TMs are required to settle the credit balance of clients lying with them on the first Friday and/or Saturday of every month or quarter.

2. In case a member is unable to settle the client accounts due to non-availability of bank accounts or non-traceability of clients, etc., as per stock exchange guidelines, TMs shall make all efforts to trace the clients to settle their funds lying with them and maintain an audit trail for such efforts made for tracing the clients.

For Securities Leg

3. As per paragraph 41.1 of SEBI Master Circular for Stock Brokers” dated May 22, 2024, TM or Clearing Member (CM) shall, inter alia, accept collateral from clients in the form of securities, by creating ‘margin pledge’ in the Depository system. Further, the TM / CM shall open a separate demat account for accepting margin pledge, which shall be tagged as ‘Client Securities Margin Pledge Account’. For the purpose of providing collateral in form of securities as margin, a client shall pledge securities with TM, and TM shall re-pledge the same with CM, and CM in turn shall re-pledge the same to Clearing Corporation (CC). The complete trail of such re-pledge shall be reflected in the demat account of the pledger.

4. Further, it was stipulated that the securities for pay-out shall be credited directly to the respective client’s demat account by the CCs.

5. Pursuant to implementation of various measures undertaken by SEBI to safeguard the client securities, such as, margin obligations to be given by way of pledge or re-pledge in the Depository system; prohibition on off market transfers; and transfer of client unpaid securities to client demat account in auto pledged manner in favor of TM, the holding of client securities with TM in their demat account has decreased substantially. As a result, securities of clients are routed only for the purpose of settlement obligation of the client and all other demat accounts of TM for holding client securities were either closed or frozen in the depositories system.

6. Thus, the demat accounts, from which TM could not transfer securities to the clients because of incomplete/ incorrect information of demat account of client, or because of non-traceability of clients or their legal heir/ nominees, etc., were marked frozen in the depositories system.

Existing mechanism for dealing with untraceable accounts of clients

7. Stock exchanges, on the treatment of inactive trading accounts, have advised their TMs to take the following steps:

7.1. Make all efforts to trace the clients to settle their funds and securities lying with them.

7.2. Maintain audit trail for such efforts made for tracing such clients to transfer such funds and/or securities to the respective clients.

7.3. As per requirement of upstreaming of clients’ funds to clearing corporations (CCs), such unclaimed funds of clients are also required to be up streamed to CCs on EOD basis.

7.4. In case of receipt of any claims from such clients, TMs are advised to settle the accounts immediately and ensure that the payment or transfer of securities is made to the respective clients only.

Need for Review

8. As on January 31, 2025, the total value of unclaimed funds was around INR 323 Cr. and unclaimed securities was around INR 182 Cr. Considering the substantial amount of unclaimed client funds and securities lying with TMs, it has been proposed to have a detailed mechanism for treatment of such unclaimed funds and securities, and steps to be taken to trace such clients.

Proposals

9. The proposed process for treatment of unclaimed funds and securities (both in physical and demat mode) lying with the TMs is as under:

Defining unclaimed Funds and Securities

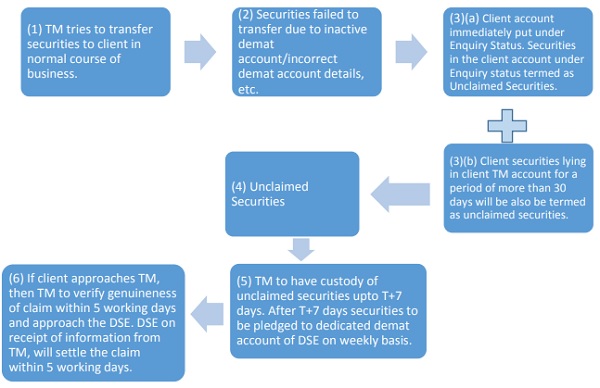

9.1. If the funds or securities could not be credited to the client bank account or demat account in the normal course of business, or the client is not reachable, such client accounts shall immediately be put under ‘enquiry status’. The TM(s) shall contact the clients through letters, e-mails, telephonically or any other means as feasible. TMs shall upstream such funds to clearing corporations as per upstreaming guidelines issued by SEBI, Exchanges and CCs.

9.2. The client funds with TMs which are put under ‘enquiry status’ shall be termed as ‘unclaimed funds’. Further, the client securities which are put under ‘enquiry status’ or lying with the TM for a period of more than 30 days shall be termed as ‘unclaimed securities’.

Treatment of unclaimed Funds and Securities

9.3. To ensure that unclaimed funds and/or securities of clients lying with the TMs are returned to the respective clients in a timely and efficient manner, in addition to the obligations of TMs with regard to running account settlement, stock exchanges shall ensure compliance of the following by TMs:

9.3.1. In case the whereabouts of the clients are not traceable, the introducer of the client, nominee of the client, employer of the client or any other related person whose details are available with the TM shall be approached or contacted by the TMs to trace the whereabouts of the client without disclosing any financial or holding details of the client.

9.3.2. TMs shall select any one of the stock exchanges having nation-wide terminals as the Designated Stock Exchange (DSE) (excluding those stock exchange(s) where member does not undertake any clientele trading) to register themselves for the purpose of transferring the unclaimed funds and pledging of unclaimed securities. The TMs shall provide all relevant details in this regard as per the format specified by the DSE and if required, the DSE may seek any other relevant document from the TMs.

9.3.3. TMs shall intimate other stock exchanges where it is registered as a TM about its decision of choosing the DSE. Once the DSE has been selected, the same cannot be changed except for de-recognition or exit of the stock exchange or any other specific direction from SEBI.

9.3.4. In case the TM has surrendered it membership or expelled or declared defaulter

9.3.4.1. In case the TM has been declared defaulter, all unclaimed funds up-streamed by TM to CC shall be down streamed and transferred directly to the dedicated bank account of the DSE, and all unclaimed securities in the demat account of the TM including unclaimed securities frozen in the depositories system shall be transferred to the dedicated demat account of the DSE.

9.3.4.2. In case a TM ceases to be a SEBI registered Stock Broker due to merger with other TM or due to transfer of business to other TM, the merged entity or transferee TM shall be responsible for the receiving & processing the claims from the client or their legal heir or nominee, and provision of this circular & other circulars as issued by SEBI or stock exchanges from time to time, shall be applicable to the merged entity or transferee TM.

9.3.4.3. In case, the TM ceases to be a member of the DSE on account of surrendering its membership with the DSE, the TM shall select any other stock exchange as the DSE where the TM is registered. TM shall intimate other stock exchanges where it is registered as a TM about its decision of choosing the new DSE. TM shall further inform the earlier DSE to immediately transfer the unclaimed funds with accrued interest to the newly selected DSE and/or pledge the unclaimed securities from their demat accounts in favor of such dedicated demat account of the newly selected DSE and shall provide all relevant details in this regard to the new DSE. In order to ensure seamless shifting of pledged securities from one DSE to another DSE, depositories should provide port functionality in their system wherein one DSE can shift pledge on securities of TM to another DSE.

For unclaimed Funds

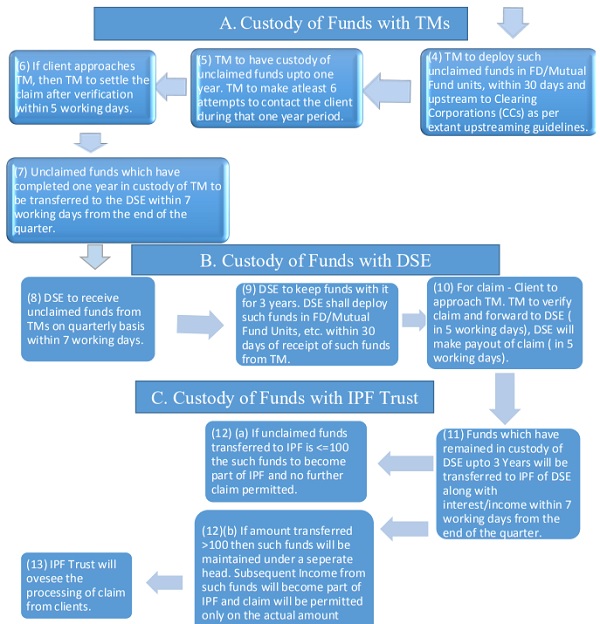

9.3.5. TMs shall set aside the unclaimed funds of clients and shall deploy the same on the premise of highest degree of safety and least market risk such as investments in units of Liquid and Overnight Mutual Fund Schemes, Fixed Deposits (FDs), etc. such that the same can be up-streamed to CC, within 30 days of the funds becoming unclaimed. Such funds/units of mutual funds/FDs shall be up-streamed to CCs as per the extant guidelines prescribed by SEBI. The facility for deploying the unclaimed funds is being provided to the TM so that the investors can earn at least a minimum interest/income on the unclaimed funds. TM shall ensure that the investments can be redeemed as and when required without any cost to settle investor claims and for transfer of such funds to the DSE after one year.

9.3.6. In case the funds remain unclaimed for a period of one year from the day the funds have been marked as unclaimed funds, then such funds, including accrued interest, if any, shall be down streamed from CCs and transferred to the dedicated bank account of the DSE opened for this purpose on quarterly basis within 7 working days from the quarter ending June, September, December and March along with relevant details such as financial ledger balances, list of clients, interest accrued, if any, and any other information as may be sought by the DSE. Unclaimed funds of clients which have been lying with TMs for more than one year as on date of implementation of this guideline, shall be transferred to the dedicated bank account of the DSE within 30 days from the date of implementation of this guideline.

9.3.7. Before transfer of the unclaimed funds to the DSE, at least 6 attempts shall be made by the TMs to reach out to the clients.

9.3.8. TMs shall submit a monthly report to stock exchanges regarding client-wise details of unclaimed funds (other than those funds already transferred to DSE) lying with the TMs within 7 working days of the following month. The DSE shall share details of unclaimed funds of clients lying with it and its TMs, with the clients, as and when any update about client information is received or on half-yearly (September/March) basis within 7 working days from the end of the half-year.

9.3.9. For client(s) whose funds remain unclaimed for a period of 3 years with the DSE:

9.3.9.1. Such unclaimed funds (including accrued interest) lying with DSE shall be transferred to the Investor Protection Funds (IPF) of the DSE on quarterly basis within 7 working days from the end of the quarter (June, September, December and March).

9.3.9.2. Pursuant to transfer of such funds to IPF, if total amount of unclaimed fund (including accrued interest) is upto INR 100 for a client then no further claim on such funds shall be permitted from IPF.

9.3.9.3. If total amount of unclaimed fund (including accrued interest) is more than INR 100, then clients shall continue to be entitled to claim such unclaimed funds from the IPF. The same shall be maintained under a separate head in IPF and can be used only for settling claims of such clients.

9.3.9.4. However, all interest or income from such unclaimed funds after transferring to IPF, shall be added to the IPF corpus and subsequent claim from clients shall be limited to the amount transferred to IPF (i.e. initial unclaimed amount including interest accrued till the end of fourth year).

9.3.9.5. Once the unclaimed funds (including accrued interest) are transferred to IPF, the IPF Trust shall oversee the processing of claims from clients; or their legal heirs or nominees.

For unclaimed Securities

9.3.10. TMs shall pledge all unclaimed securities post completion of 7 days of the securities being marked as unclaimed securities, from their demat accounts in favor of the dedicated demat account of the DSE, on weekly basis within 3 working days from the end of every week. The depositories shall allow pledge transactions from existing frozen demat accounts of TMs in favor of such dedicated accounts of DSE only and shall tag the respective client UCC.

9.3.11. After pledging of such securities, depositories shall not permit subsequent changes in the client UCC in the depository system without the approval of the DSE.

9.3.12. TMs shall provide all requisite information, as specified by DSE, while pledging unclaimed securities to the DSE. If required, the DSE may seek any other relevant document from the TMs.

9.3.13. In case of Corporate Action, benefits such as dividend, bonus, etc. received by TM on pledged securities, shall be credited in the respective client ledger and shall transfer or pledge the same to DSE on quarterly basis within 7 working days from the end of every quarter.

9.3.14. TMs shall submit a quarterly report to DSE regarding client-wise details of unclaimed securities lying with it (except the securities already pledged in favor of DSE) within 7 days of the following month. The DSE shall share details of unclaimed securities lying with it and its TMs and/or pledged with it, with the clients, as and when any update about client information is received or on half-yearly (September/March) basis within 7 working days from the end of the half-year.

Role of DSE

9.4. The DSE shall have a dedicated bank account to receive unclaimed funds of clients from the TMs.

9.5. The DSE shall share the list of the TMs who have opted their exchange as the DSE on their website.

9.6. The DSE shall make efforts to trace the clients based on the information available in the Unique Client Code (UCC) database of all stock exchanges, depositories, KYC Registration Agencies, etc. If such clients are found to be registered with other members based on the above databases, the DSE shall send SMS or e-mails to such clients regarding their unclaimed funds and/or securities, on their registered e-mail id and/or mobile number.

9.7. The DSE shall disclose the details of unclaimed amount lying with it and with its TMs on its website to be updated on quarterly basis within 7 working days from the end of the quarter (June, September, December and March) in the following format:

| Net unclaimed funds as on end of quarter (DD/MM/YYYY) | |||

| Number of clients whose funds are lying unclaimed | Net Unclaimed Amount (INR Cr.) |

Interest/income accrued (INR Cr.) | Out of the unclaimed funds, amount transferred to IPF (in terms of paragraph 9.3.9) |

–

| Total unclaimed Securities as on end of quarter (DD/MM/YYYY) | |

| Number of clients whose securities are lying unclaimed | Value of Unclaimed Securities (INR Cr.) |

Further, the process of filing claim for such unclaimed funds/securities along with relevant documents to be submitted shall also be displayed on its website.

9.8. The DSE and TM shall provide a search facility on their website for clients or nominee of the client or legal heir of the client to enquire if there are any unclaimed funds/securities due to them and lying with the DSE or its TMs. The search criterion may be based on combination of PAN or Date of Birth or Depository Participant Identification (DP ID) or Client Identification (Client ID) with E-mail ID or Mobile No. along with One Time Password (OTP) verification. Upon verification, the status of unclaimed funds/securities, if any, for the client account will be displayed with contact details of the concerned person of the TM/DSE without revealing the exact quantum of such funds/securities. Further, to know the exact details of unclaimed funds/securities, the client or nominee of the client or legal heir of the client shall contact the concerned person of the TM/DSE.

9.9. DSE shall deploy the unclaimed funds on the premise of highest degree of safety and least market risk such as investments in units of Liquid and Overnight Mutual Fund Schemes, Fixed Deposits (FDs), T-bills, Central Govt. Securities, within 30 days of receipt of the same from TM. The DSE shall also have a dedicated demat account with both the depositaries to receive unclaimed securities pledged by TMs.

Process for Claim of Unclaimed Funds and Securities

Before the unclaimed funds or securities are transferred or pledged to DSE

9.10. If a claim is received from the client; or legal heir or nominee of the client, before the unclaimed funds or securities are transferred or pledged to DSE, the TM shall verify the genuineness of the claim and settle it within a period of 5 working days, after compliance with the applicable laws.

After the unclaimed funds or securities are transferred or pledged to DSE

9.11. Upon receipt of claim from a client; or their legal heir or nominee, after the unclaimed funds or securities are transferred or pledged to DSE, the TM shall verify the genuineness of the claim after proper due diligence, and approach the DSE within 5 working days from the receipt of complete and necessary information, such as, bank account details of client; or their legal heir or nominee, client UCC, client PAN etc. The detailed checklist of documents in this regard shall be specified by the DSE in consultation through Industry Standards Forum (ISF).

9.12. On receipt of request from TMs,

9.12.1. For Unclaimed Funds: The DSE shall process the same and transfer the funds (including accrued interest), if any, after adequate due diligence, to the respective client; or their legal heir or nominee, within 5 working days from the date of receipt of complete and necessary information from TM.

9.12.2. For Unclaimed Securities: The DSE shall process the same and transfer the securities directly to the demat account of client or their legal heir or nominee as provided by member within 5 working days from the date of receipt of complete and necessary information from TM. Depository shall provide a mechanism for auto transfer of unclaimed securities directly to the demat account of the client or their legal heir or nominee as provided by the DSE.

9.12.3. In case of default of the TM, all subsequent claims by the client for the unclaimed funds/securities shall be made to the DSE directly. In this scenario, the DSE shall verify the genuineness of the claim and process such claim within 10 working days from the receipt of complete and necessary information.

9.12.4. The TMs/DSE will not charge any fee for maintenance of unclaimed funds/securities and for putting efforts to reach out to the client.

9.12.5. The final pay-out to client, shall be made by TM or DSE, as the case may be, subject to applicable taxes, etc.

9.13. The process flow for treatment and claim of unclaimed funds and/or securities is enumerated at Annexure-1.

Monitoring Implementation of the Mechanism

9.14. The Regulatory Oversight Committee (ROC) of DSE shall oversee the implementation of steps or processes involved in transfer of unclaimed funds from TMs to DSE, subsequently from DSE to IPF of DSE and pledging of unclaimed securities from TMs to DSE, and processing of claims from clients; or their legal heirs or nominees. The DSE shall submit a half-yearly report to SEBI and the governing board of DSE on the above within 30 days from half-year ending by September and March.

Public Comments on this Consultation Paper:

Public comments are invited on the proposal for treatment of unclaimed funds and securities of clients lying with Trading Members. The comments/ suggestions should be submitted latest by March 04, 2025 through the following link:

https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPubl icComments=yes

In case of any technical issue in submitting your comment through web based public comments form, you may send your comments through e-mail to aruns@sebi.gov.in, pankajc@sebi.gov.in & mrd_pod3@sebi.gov.in with the subject: “Treatment of unclaimed funds and securities of clients lying with Trading Members” on the proposals at para 9 above.

Issued on: February 11, 2025

Process Flow for Unclaimed Funds