Dr. Vidya V Devan[1]

E-commerce, or electronic commerce, refers to the buying and selling of goods and services over the internet. It represents the digital transformation of traditional business activities, enabling seamless transactions across geographical boundaries. As one of the fastest-growing sectors in the Indian economy, e-commerce has revolutionized consumer behavior, business models, and market dynamics. As it was recognised as the major area of sales and services, the tax was levied on e-commerce transactions. But the conventional territorial-based taxation system posed significant challenges for both e-commerce operators and the government, leading to inefficiencies in tax administration and compliance. Recognizing these issues, while introducing the new indirect tax regime, the Goods and Services Tax (GST) incorporated specific provisions aimed at the effective levy and administration of taxes on e-commerce transactions. This shift marked a significant reform in the indirect tax regime, addressing complexities related to jurisdictional ambiguities and ensuring a more streamlined approach to taxation in the digital economy. The article analyzes the key GST provisions for e-commerce, focusing on regulatory frameworks, compliance requirements, and associated challenges. It examines how the indirect tax reform addresses jurisdictional complexities, enhances tax administration, and streamlines compliance in the digital economy.

Origin And Evolution Of E- Commerce

The first instance of e-commerce was in the 1960s, to facilitate the transfer of documents, companies used an electronic system called the Electronic Data Interchange (EDI). Online shopping, known as tele-shopping, was first invented in 1979 by a businessman Michael Aldrich, to facilitate online transactions between customers and companies or between companies. In 1982 The Boston Computer Exchange (BCE) created an online platform for people to buy and sell used computers. The first web browser was introduced in 1990 known as “World Wide Web’ by Tim Berners-Lee, a computer scientist.” Since it was the only web browser available at the time with an intuitive user interface, it was undoubtedly a remarkable development. The public availability of the Internet in 1991 enabled the emergence of online retail by providing a platform for businesses and consumers to interact digitally. It was in 1994 that the very first online transaction took place. This involved the sale of a CD between friends through an online retail platform called Net Market. The establishment of Amazon in 1994 and e-Bay in 1995 transformed e-commerce by pioneering online shopping platforms. Originally launched as an online marketplace for books, it has diversified to include a vast array of product categories across numerous industries. Netflix, a popular streaming service that offers a vast library of movies, TV shows, and original content across various genres was launched in 1997 and Pay Pal launches online payment system in 1998.

The e-commerce industry has evolved significantly, driving traditional retailers to adopt new technologies to compete with the rise of major online platforms like Amazon, Flipkart, Myntra, and Snapdeal, which have simplified buying and selling in the digital marketplace.

The rise of smartphones enabled mobile commerce (m-commerce), while social media platforms like Instagram, facebook etc integrated shopping features, merging e-commerce with social networking.

The COVID-19 pandemic significantly accelerated the global adoption of e-commerce, reshaping consumer behavior and business operations worldwide. With restrictions on physical movement and the closure of brick-and-mortar stores, both businesses and consumers increasingly turned to digital platforms for transactions. This shift not only led to a surge in online retail but also facilitated greater access to international markets, enabling businesses to expand their customer base beyond geographical constraints. Moreover, advancements in digital payment systems, logistics, and supply chain management further supported this rapid transformation. As a result, the pandemic acted as a catalyst for unprecedented growth in the e-commerce sector, reinforcing its role as a fundamental component of the modern global economy.

The current phase of e-commerce is characterized by the integration of artificial intelligence (AI) and augmented reality (AR), which are transforming online shopping experiences. AI-driven algorithms enhance personalization by analyzing consumer preferences and providing tailored product recommendations, while AR enables immersive interactions, such as virtual try-ons and interactive product visualizations. These advancements bridge the gap between physical and digital shopping, improving customer engagement and decision-making. As a result, AI and AR are redefining the e-commerce landscape, making online shopping more dynamic, intuitive, and customer-centric.

E- Commerce Models

Selling through an e-commerce website typically involves three key parties: the seller or supplier, the e-commerce platform (e.g. Amazon) and the customer or the buyer. Based on the interactions between these parties, e-commerce operates under three primary models.

1. Online Marketplace Model

In the online marketplace model, an online centralized platform is provided connecting manufacturers/ retailers with the customers. The platform itself does not own or stock the products or has the expertise to provide services being sought by the customers; instead, it merely facilitates the transactions and may offer additional services such as payment processing, customer support and logistics. The actual supply of goods is done by the respective suppliers. The platform generates revenue by charging from the supplier the fees or commissions for using the marketplace and accessing its customer base.eg. Amazon, Flipkart, Myntra, etc.

Similarly, suppliers of services, such as cab services, and food delivery providers, operate through e-commerce platforms that facilitate transactions between service providers and customers. These platforms act as intermediaries, connecting users with service providers while managing payments, logistics, and customer interactions. eg. Uber, Ola, Swiggy, Zomato etc.

2. Direct Sales Model

In the direct sales model, businesses sell their products or services directly to consumers through their own online stores or websites. Customers browse the company’s website, select products/services, and complete the purchase directly with the supplier. Eg. Urban ladder, first cry, Biba, etc.

3. Inventory Model

In the inventory model, inventory of goods/services is owned by the ECO that it supplies to customers. The platform takes responsibility for warehousing, inventory management, and fulfillment of orders. Eg. Amazon, Flipkart, Snapdeal, etc.

4. Another way of classifying the e-commerce transactions is on the basis of supplier-recipient combination, for instance, Business-to-Consumer (B2C), Business-to-Business (B2B), Consumer-to-Consumer (C2C), Consumer to Business (C2B), Consumer to Government (C2G), Government to Consumer (G2C) and Business to Government (B2G).

E-commerce industry is constantly evolving, and new innovative models may emerge over time.

E-Commerce and Taxation in India

With the adoption of new economic strategies of liberalisation and globalisation, in 1995 e-commerce was launched in the country which showed an expeditious growth within a short span of time. There was unprecedented growth of e-commerce from the year 2000 which entirely changed the pattern of traditional shopping and providing of general amenities. The high hop in the development of mode of online payment methods, gaining momentum of smart phone and the introduction of 3G and 4G were an added advantage for e-commerce.

The erstwhile indirect taxation which revolved round the physical presence and movements did not have proper provisions for levying tax on these types of activities. The Centre imposed Service Tax, Central Sales Tax and several States imposed VAT as they maintained warehouse in the States. Certain States levied entry tax for delivering products in the jurisdiction of their State. This led to double taxation and utter confusions, causing difficulties for the e-commerce operators. The lack of precise provisions for the levy sometimes resulted in the leakage of revenue to the government. This issue could be answered only when there is a composite levy on goods and services, which India sought to accomplish by the implementation of GST.

Taxation of E-Commerce Under GST

E-commerce transactions involving the supply of goods, services, or both are subject to Goods and Services Tax (GST) in the same manner as other taxable supplies, unless specifically exempted under the law. Recognizing the unique nature of e-commerce, the GST framework incorporates some special provisions for its administration.

They are

- Specific provisions in Sec. 9(5) of Central Goods and Services Tax Act, 2017/ Sec.5(5) Integrated Goods and Services Tax Act, 2017.

- Mandatory Registration for E-Commerce Operators

- The tax will be collected at source from the e-commerce operators.

- A special form is prescribed for return filing.

As per Section 2(44) of CGST Act “electronic commerce” means the supply of goods or services or both, including digital products over digital or electronic network.

Section 2 (45) of CGST Act defines “electronic commerce operator” as any person who owns, operates or manages digital or electronic facility or platform for electronic commerce.

Before the implementation of GST, there was ambiguity regarding the classification of e-commerce operators, particularly whether it applied to platform owners or businesses using digital platforms for transactions. The GST framework has since clarified this definition, encompassing both entities managing e-commerce platforms and those conducting business through them, ensuring comprehensive tax compliance.

In the GST framework, taxation is determined based on the nature of the transaction—whether it is intra-state or inter-state. On intra-state supply, which occurs within a single state or union territory, Central Goods and Services Tax (CGST) and concerned State Goods and Services Tax (SGST) will be levied. On inter-state supply, involving transactions between different States or Union Territories, is subject to Integrated Goods and Services Tax (IGST).

Levy of GST on e-commerce.

The concept of levy in GST is governed by section 9 in the Central Goods and Services Tax Act, 2017(CGST) and section 5 in the Integrated Goods and Services Tax Act, 2017(IGST). These impose the GST on all intra state\interstate supplies of goods and services, except alcoholic liquor for human consumption and specified spirits used in liquor production. Section 9(5) of the CGST Act and Section 5(5) of the IGST Act is particularly relevant to e-commerce transactions.

If a supplier supplies through an ECO those which are notified under section 9(5) of the CGST Act/ section 5(5) of the IGST Act, the tax on such services is to be paid by the ECO as if he is the supplier liable to pay tax on the supply of such services. Here the tax is imposed on neither the supplier nor the recipient of supply, but the electronic commerce operator (‘e-commerce operator’) through which the supply is affected.

The proviso to Section 9(5) of the CGST Act/section 5(5) of the IGST Act states that if an e-commerce operator lacks a physical presence in the taxable territory, their representative in that territory is responsible for tax payment. If no such representative exists, the operator must appoint a person in the taxable territory to fulfill tax obligations on their behalf.

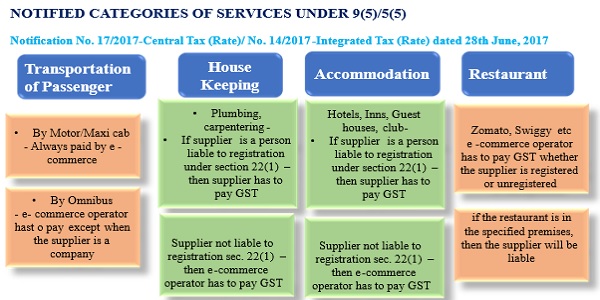

E-commerce operator is liable to pay tax for certain notified categories. The Government has notified following services in this regard vide Notification No. 17/2017-Central Tax (Rate); 14/2017 Integrated Tax dated 28.06.2017 as amended from time to time. As of now, four services are notified under this category, services by way of transportation of passengers, services by way of providing accommodation in hotels, services by way of housekeeping, supply of restaurant service

i) Services by way of transportation of passengers

The Central Government, based on the recommendations of the Council, has notified that in the case of certain services, such as passenger transportation via radio-taxi, motor cab, maxi cab, or [motor cycle, omnibus or any other motor vehicle][2], the tax on supplies must be paid by the e-commerce operator.[3]

The provision under GST stipulates that the tax on services related to the transportation of passengers by an omnibus is to be paid by the e-commerce operator, except when the service is supplied by a company. In cases where a company is the service provider, it is not the e-commerce operator’s responsibility to collect and remit the tax.

ii) Services by way of providing accommodation in hotels

The Central Government, also notified that for services related to accommodation in hotels, inns, guest houses, clubs, campsites, or similar commercial places, the e-commerce operator is responsible for paying the tax. This applies unless the service provider is already liable for registration under Section 22(1) of the Central Goods and Services Tax Act.[4]

iii) Services by way of housekeeping

The Central Government has notified that for housekeeping services, such as plumbing and carpentry, provided through an e-commerce operator, the operator is responsible for paying the tax, unless the service provider is already liable for registration under Section 22(1) of the Central Goods and Services Tax Act.[5]

iv) Supply of restaurant service

In 2021 supply of restaurant services other than the services supplied by restaurants, eating joints, etc. located at specified premises was also included in the list.[6]

The notification also clarifies that “specified premises means premises providing hotel accommodation service having declared tariff of any unit of accommodation above seven thousand five hundred rupees per unit per day or equivalent.”

Hence e-commerce operators must pay tax on restaurant services, except those provided by restaurants located at “specified premises.” In the case of restaurants within the premises of a hotel providing the accommodation with a declared tariff of more than ₹7,500 per unit per day or equivalent then the supplier has to pay the tax.

Section 9(5) CGST/5(5)IGST clarifies that the liability to pay tax on supplies made through an e-commerce operator rests with the operator, treating them as the “supplier liable to tax.” As a result, the actual suppliers, are not responsible for paying tax on services provided through the e-commerce platform except in certain specified cases.

Opta Cabs (P) Ltd. V. Range Csd4, Appellate Authority for Advance Ruling, GST, December 4, 2018

An appeal was filed against the advance Ruling No. KAR/ADRG 14 /2018 dated 27th July 2018. The appellant argues that it is not liable to pay GST as the services are merely booked through its platform and not supplied through it. The Advance Ruling Authority has held that the appellant is an electronic commerce operator under 2(45) CGST Act, 2017 and therefore liable to pay on the services provided.

Appellate authority observed that the services of transportation of passengers supplied to the consumers through the applicant is deemed that, the applicant is the supplier liable to pay tax in relation to the supply of such service by the taxi operator – in accordance with the provisions of section 9(5) read with Notification No. 17/2017-Central Tax (Rate), dated 28.06.2017. The applicant is liable to pay tax on the amounts billed by him on behalf of the taxi operators for the service provided in the nature of transportation of passengers through it. The court upheld the decision of advance ruling authority and ordered that the appellant is liable to pay GST on the transportation services provided through its platform.

The e-commerce operator and composition scheme.

Under the Goods and Services Tax (GST) regime, e-commerce operators are not eligible to opt for the composition scheme, which is designed for small taxpayers to pay tax at a fixed rate on their turnover. The composition scheme is available to businesses with a lower turnover, but e-commerce operators, due to the nature of their business and the complexities involved in tax collection at source, are excluded from this option. As a result, e-commerce operators must comply with the regular GST provisions, including collecting and remitting taxes on transactions, without the benefit of the simplified composition scheme.

Registration Requirements for E-Commerce Businesses under GST

Section 24 of the CGST Act specifies compulsory registration for businesses in certain cases, even if their turnover is below the prescribed threshold. This includes e-commerce operators, inter-state suppliers, and those required to pay tax under reverse charge etc.

The following categories of persons related to e-commerce shall be required to take compulsory registration under this Act, –

Section 24(iv) person who are required to pay tax under of section 9(5)

Section 24 (ix) persons who supply goods or services or both, other than supplies specified under sub-section (5) of section 9, through such electronic commerce operator who is required to collect tax at source under section 52;

Section 24 (x) every electronic commerce operator who is required to collect tax at source under section 52.

Since Online Information and Database Access or Retrieval (OIDAR) services fall under the scope of e-commerce operators the provisions specifically related to OIDAR services are also to be considered here.

Section 24 (xi) every person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered person

Section 24 (xia) every person supplying online money gaming from a place outside India to a person in India.

Under the GST framework, certain categories of individuals clarifies the entities related to e-commerce who have to take compulsory registration. These includes persons who areare required to pay tax under Section 9(5), those supplying goods or services through an e-commerce operator obligated to collect tax at source under Section 52, and e-commerce operators themselves who must collect tax at source. Additionally, provisions related to Online Information and Database Access or Retrieval (OIDAR) services apply to entities supplying such services from outside India to consumers in India, except for those who are already registered under GST. The same obligation extends to individuals or businesses supplying online money gaming services from outside India to persons in India, ensuring compliance with the tax regulations for cross-border digital services.

Registration form for the e – e-commerce operator

Rule 12 of CGST Rules, 2017 specifies the registration form for the e-commerce operator. Any person required to collect tax at source in accordance with the provisions of section 52 shall submit an application, duly signed or verified in FORM GST REG-07 for the grant of registration through the common portal

Significant GST Mechanisms for E-Commerce Compliance: Tax Collected at Source (TCS)

Every ECO (not being an agent) is required to collect an amount calculated at the rate not exceeding 1%, of the net value of taxable supplies made through it, where the consideration with respect to such supplies is to be collected by such ECO. The amount so collected is called as Tax Collection at Source. When the consumers are placing the order through the e commerce platform for a particular product/ service, the actual supplier supplies the selected product/services to the consumer . The collection of consideration for the product/services, handling of goods, etc. is undertaken by the ECOs depending upon the arrangement between the supplier and ECO – Online Marketplace Model. The ECO thereafter deducts its commission from the consideration for the goods or services collected by it and the tax@ 1% and passes on the net consideration to the supplier.

i.e When a supplier supplies through an ECO portal and the payment for that supply is collected by the ECO, the Government has placed a responsibility on such ECO to collect an amount @ 1% from such supplier.

When the payment is made or the return is filed by the e-commerce operator (ECO), it enables the government to obtain detailed information regarding the supply that has occurred, thereby facilitating the tracking of transactions. This process serves as a preventive measure against revenue leakage, ensuring greater transparency and compliance within the e-commerce sector. By mandating the filing of returns and tax payments, the GST framework enhances the ability to monitor and trace taxable supplies, reducing the potential for tax evasion.

Exceptions:

(1) in case of notified services under section 9(5) of the CGST Act/ section 5(5) of the IGST Act, the tax on such services is to be paid by the ECO as if he is the supplier liable to pay tax on the supply of such services.

(2) Where a supplier supplies the goods or services or both on his own account through a website hosted by him, there is no requirement to collect tax at source.

Special form for return filing

In the case of returns fining also GST has introduced specified forms for the e-commerce operators. Rule 67 of Central Goods and Services Tax Rules, 2017 prescribes the form and manner of submission of statement of supplies through an e-commerce operator

An ECO liable to collect TCS shall furnish a monthly statement in Form GSTR-8 electronically through the common portal. Form GSTR-8 contains the details of supplies of goods or services or both effected through ECO including the supplies of goods or services or both returned through it. The details of tax collected at source under section 52(1) shall be made available electronically to each of the registered suppliers on the common portal after filing of FORM GSTR-8 for claiming the amount of tax collected in his electronic cash ledger after validation. The details in GSTR-8 should be furnished on/before 10th day of the month succeeding the calendar month in which tax has been collected at source.

Clarification on the place of supply of Online Services supplied by the suppliers of services to unregistered recipients.

Several states raised concerns regarding the non-receipt of their entitled share of the Integrated Goods and Services Tax (IGST). In response, a study was conducted by multiple states, and the findings were submitted to the GST Council. The primary conclusion of the study highlighted that the revenue loss arises from issues related to the determination of the place of supply. To address this, the Central Board of Indirect Taxes and Customs (CBIC) issued a clarification aimed at preventing such discrepancies and ensuring the proper allocation of IGST revenue. Through Circular No. 242/36/2024-GST dated the 31st December 2024 CBIC clarifies that combined reading of the definitions of ‘electronic commerce’ and ‘electronic commerce operator’ as per section 2(44) and section 2(45) of CGST Act, along with rule 46(f) of CGST Rules, leads to an understanding that all services supplied to unregistered recipients over a digital or electronic network, either by the supplier using his own digital or electronic facility/platform or through any other electronic or digital platform owned and operated by an independent electronic commerce operator, will be covered under proviso to rule 46(f) of CGST Rules. It is, accordingly, clarified that provisions of the proviso to rule 46(f) of CGST Rules shall be applicable in respect of all the online supplies of services supplied to an unregistered recipient, in addition to the supply of online money gaming and OIDAR services.in respect of the supply of any such online/ digital services, OIDAR services, and online money gaming to unregistered recipients, the suppliers are mandatorily required to record the name of the State of the recipient on the tax invoice, irrespective of the value of supply of such services, and to declare place of supply of the said services as the location of the recipient (based on the name of State of the recipient) in their details of outward supplies in FORM GSTR-1/1A.

It is also mentioned that if the supplier fails to issue invoice in accordance with the said provisions by not recording correct mandatory particulars, including recording of name of State of unregistered recipient in respect of such supplies, he may be liable to penal action under the provisions of section 122(3)(e) of CGST Act.

Challenges And Advantages

Advantages

The introduction of the Goods and Services Tax (GST) in India has significantly benefited e-commerce operators by simplifying the tax structure, and replacing multiple state VAT laws, service tax, and excise duties with a unified system that reduces compliance complexities. It ensures uniform taxation across states, enhancing interstate trade by eliminating Central Sales Tax (CST) and entry taxes, thereby lowering logistics costs and improving supply chain efficiency, allowing businesses to reach remote customers more effectively. GST also eliminates cascading taxes through the input tax credit (ITC) mechanism, reducing overall costs. Additionally, it promotes regulation and transparency by mandating registration and record maintenance curbing tax evasion. The Tax Collected at Source (TCS) mechanism simplifies compliance by ensuring tax is collected at the time of payment and remitted to the government. Moreover, GST enhances the ease of doing business by minimizing administrative burdens, allowing e-commerce operators to focus on growth. The introduction of standardized tax rates and product/service classifications further reduces confusion and ensures consistency. Collectively, these factors create a favorable environment for e-commerce businesses to thrive under the GST regime.

Challenges

E-commerce operators have benefited from the GST regime but face significant challenges, including increased compliance burdens due to the Tax Collection at Source (TCS) mechanism, requiring monthly GSTR-8 filings and complex refund adjustments. Multiple state-wise registrations add administrative costs, while input tax credit (ITC) mismatches affect seller cash flow. Compliance costs rise with frequent filings, necessitating tax experts or software. Ambiguities in tax classification, varying GST rates, and constant policy changes create operational disruptions. Managing returns and reconciling tax credits is complex, especially for small sellers who must register despite low turnover. Moreover, keeping precise transaction records for reconciliation is essential to prevent penalties. Addressing these challenges through policy refinements and automation could streamline compliance and reduce operational burdens.

Conclusion

Overall, the GST provisions for e-commerce, including TCS, mandatory registration, and ITC regulations, have enhanced tax transparency and streamlined revenue collection. While these measures come with compliance challenges, they also offer opportunities for improved tax governance and digital record-keeping. With continuous policy refinements, simplified compliance mechanisms, and greater automation, GST can become even more efficient and supportive of the e-commerce sector’s growth. By leveraging technology and regulatory improvements, businesses can navigate GST requirements more smoothly, fostering a more robust and competitive digital economy.

[1] Assistant Professor, Gulati Institute of Finance and Taxation, Thiruvananthapuram, Kerala. E mail id drvidyavdevan@gmail.com, Ph 9349727106.

[2] Notification No. 17/2021-Integrated Tax (Rate) dated, 18th November, 2021/ Notification No. 17/2021- Central Tax (Rate) dated, 18th November, 2021

[3] Notification No. 17/2017-Central Tax (Rate) dated the 28th June, 2017 / Notification No. 14/2017-Integrated Tax (Rate) dated the 28th June, 2017 For the purposes of this notification,- (a) “radio taxi” means a taxi including a radio cab, by whatever name called, which is in two-way radio communication with a central control office and is enabled for tracking using Global Positioning System (GPS) or General Packet Radio Service (GPRS);

(b) “maxi cab”, “motor cab” and “motor cycle” shall have the same meanings as assigned to them respectively in clauses (22), (25) and (26) of section 2 of the Motor Vehicles Act, 1988 (59 of 1988).

[4] Notification No. 17/2017-Central Tax (Rate) dated the 28th June, 2017 / Notification No. 14/2017-Integrated Tax (Rate) dated the 28th June, 2017

[5] Notification No. 23/2017-Central Tax (Rate) dated the 22nd August, 2017 / Notification No. 23/2017-Integrated Tax (Rate) dated the 22nd August, 2017.

[6] Notification No. 17/2021-Integrated Tax (Rate) dated, 18th November, 2021/ Notification No. 17/2021- Central Tax (Rate) dated, 18th November, 2021