The Ministry of Corporate Affairs (MCA) has imposed a significant penalty of Rs. 7 Crore on Planify Capital Limited for violating the Companies Act. The case revolves around Planify Capital Limited, a company engaged in fundraising for start-ups. Despite regulatory restrictions, the company facilitated the sale of shares to investors through its platform, violating Section 42 of the Companies Act, 2013. The company’s unauthorized issuance of securities and public advertising has led to this punitive action.

The MCA issued a show cause notice to Planify Capital, highlighting several violations, including exceeding the limit of 200 persons for private placement offers and utilizing public advertisements to inform the public about securities issues. Planify Capital’s response claimed a single allotment to Planify Enterprises Private Limited, followed by transfers to 76 investors. However, investigations revealed a more complex transaction structure, implicating the company in breaching regulations.

The adjudication process uncovered discrepancies, including misleading valuation reports and improper use of the company’s platform for securities transactions. Despite attempts to justify actions, Planify Capital’s conduct breached legal provisions.

****

GOVERNMENT OF INDIA

MINISTRY OF CORPORATE AFFAIRS,

OFFICE OF REGISTRAR OF COMPANIES,

NCT OF DELHI & HARYANA

4TH FLOOR, IFCI TOWER, 61, NEHRU

PLACE, NEW DELHI -110019

ORDER FOR PENALTY UNDER SECTION 42 OF THE COMPANIES ACT, 2013 IN THE MATTER OF ADJUDICATION OF PLANIFY CAPITAL LIMITED (CIN: U65990HR2021PLC093712)

Appointment of Adjudicating Officer: –

1. Ministry of Corporate Affairs vide its Gazette Notification No. A-42011/112/2014-Ad.II, dated 24.03.2015 appointed the undersigned as the Adjudicating Officer in exercise of the powers conferred by section 454(1) of the Companies Act, 2013 (hereinafter known as Act) r/w Companies (Adjudication of Penalties) Rules, 2014 for adjudging penalties under the provisions of this act.

Company: –

2. Whereas the company viz. Planify Capital Limited (hereafter known as ‘company’ or ‘subject company’) is a registered company with this office under the provisions of section 7 of the Companies Act, 2013, having its registered office as per MCA 21 registry at PLOT NO.1014, ANSAL ESCENIA, SECTOR-67, GURUGRAM, Gurgaon, Haryana- 122001. The financial & other details of the subject company for immediately preceding F.Y.2022-23 as available on MCA-21 portal is stated as under:

|

S. No. |

Particulars | Details as on FY 2022-23 |

| 1. | Paid up capital (in thousands of INR) | 83,745.753 |

| 2. | a. Revenue from operation (in thousands of INR) | 3,85,583.75 |

| b. Other Income (in thousands of INR) | 83.19 | |

| a. Profit for the Period (in thousands of INR) | 7045.95 | |

| 3. | Holding Company | No |

| 4. | Subsidiary Company | No |

| 5. | Whether company registered under Section 8 of the Act? | No |

| 6. | Whether company registered under any other special Act? | No |

3. Facts about the Case: –

I. On the basis of the information which had come to notice, it was seen that the Company has been acting as a fund-raising platform for start-ups and is engaged in selling of shares of unlisted companies to investors through its website https://www.planifv.in/ (Planify Platform]. It had come to notice that the company had also campaigned and raised funds for itself through its platform. (Weblink: https://www.planifyin/research-reportiplanify/.)

Following details are available on the above mentioned link:-

|

Total number of Subscribers (Investors) |

76 |

| Total amount Raised | Rs. 1,00,00,000 |

| Face Value per Share | Rs. 1 |

| Stock Price per Share | Rs. 100 |

–

|

Pitch Video Details |

Link

https://www.youtube.com/watch?v=d5cqHFB- ZTk&t=35s Dated 07-June-2023 |

II. Accordingly, a SCN was issued to the company and its directors on 02.11.2023, inter alia pointing out the following violations:

a) Pursuant to Section 42(2) of the Act r/w Rule 14 of the Companies (Prospectus and Allotment of Securities) Rules, 2014, a company making private placement offer shall not make it to not more than 200 persons in aggregate in a financial year. While it is observed that the subject company issued securities in an open forum and violated the said provisions.

b) Pursuant to Section 42(7) of the Act, no company issuing securities under section 42 shall release any public advertisements or utilize any media, marketing or distribution channels or agents to inform the public at large about such an issue. Use of Planify platform for raising securities, putting pitch information, raising money from general public through platform amounts to issuance of public advertisements or utilization of media, marketing or distribution channels or agents to inform the public at large about such an issue.

c) Pursuant to Section 42(8) of the Act, a company making private placement shall file with the Registrar a return of allotment in form PAS-3 including a complete list of all allottees, with their full names, addresses, number of securities allotted within 30 days as prescribed under rule 12 Companies (Registration Offices and Fees) Rules, 2014. It is observed that while the subject company has issued securities to 76 subscribers, but form PAS -3 has not been filed for the said issuance.

III. That in response to the SCN issued, a reply from the company was received on 27.11.2023 which inter-alia stated as under:

a) I would like to clarify that subject Company has issued and allotted 4,53,530 equity shares on 27th June, 2022, to only 1 allottee i.e., Planify Enterprises Private Limited. So, your contention that Company has issued securities on an open forum and violated provisions of Section 42(2) of Companies Act, 2013 is incorrect. Filed form PAS-3 with paid challan is duly attached for your kind reference.

b) I would like to inform your good office that the link of YouTube video which you have referred as the supporting basis of your contention that Company has utilized public advertisement, media, marketing or distribution channel to inform public at large regarding such issue. The specific video was an interview about the Company and for informational purpose only. Chairman of the Company have only talked about the fund-raising system and how Company operates and helps entrepreneurs in fund raising for growth of their businesses. There was no intension to advertise about private placement in that interview video.

c) I would like to inform your good office that till date Company has issued and allotted equity shares through private placement basis only 1 time i.e., on 27th June, 2022, to only 1 allottee i.e., Planify Enterprises Private Limited for 4,53,530 equity share. And for such allotment Company has also filed form PAS-3 within time period of 15 days as specified under section 42(8) vide SRN F14001028 on 5th July, 2022.

IV. Considering the reply of the company, a hearing in the matter was scheduled on 27.02.2024, wherein Shri. Rajesh Kumar Singla, Director of the company appeared.

V. In response to the issues raised during the hearing held on 27.02.2024, a reply was received from the company on 12.03.2024 which inter alia stated as follows [the queries are shown in BOLD]:

a) Kindly explain business model of the subject Company.

Planify is a fintech startup that focuses on building Indian private companies at your fingertips. Planify offers stocks that are not yet listed to investors (Angel, Accredited Investors, VC, AIF, and PE Funds) so that the exchange of hands can become easy in unlisted companies. As per the Memorandum of Association (MOA) of the Company, the main business objectives of the Company are as under

To carry on the business or profession of stock broker, sub-broker, dealer, jobber, market maker, portfolio manager, underwriter, dealer or broker or agent in securities, financial instruments, capital market/money market instruments of all kinds, company deposits, mutual funds, national saving certificates and other government securities issued or guaranteed by a body corporate, company, public sector company, Government, Municipality or anybody in India or abroad whether they are listed or not for the time being, and to acquire or takeover the business of any individual, partnership or corporate body, carrying on business/profession, as brokers, sub-brokers, underwriters, jobbers, members, agents, traders of all types of shares and stock and to hold one or more membership of any recognized stock exchange of India/OTC Exchange of India/National Stock Exchange of India.

To acquire, hold, sell, buy, or otherwise deal in any shares, units, stocks, debentures, debenture-stock, bonds, mortgages, obligations, and other securities by original subscription, tender, purchase, charge gift, or otherwise and to subscribe for the same, either conditionally or otherwise, and to underwrite, sub-underwrite or guarantee the subscription thereof to purchase and sell above-mentioned securities.

b) As mentioned in the SCN, the amount of Rs. 1 crore has been raised from 76 investors (source website of Planify platform). However in your reply to SCN it is mentioned that shares have been issued to Planify Enterprises Private Limited. Clarify this dichotomy as to why such misinformation is available/hosted on the Planify platform. Further provide share transfer details of this transaction.

Planify Enterprises Private Limited has transferred 453530 shares of Planify Capital Limited to 76 investors.

c) Provide copies of all agreements / MOU and related documents entered between Planify Capital and Planify Enterprises. Relevant copies of Minutes of Board Meeting /General Meeting for these transactions.

Board Meeting Minutes of Board Meeting dated 01st April 2022 of Planify Capital Limited is provided.

d) In your response dated 25.11.2023 you have mentioned about PAS- 3 form (SRN F14001028 dated 05.07.2022) wherein valuation report has been attached. It is observed that while the valuation report is in respect of Planify Capital Limited, however at various places the figures of Planify Enterprises have been

used for the purpose of valuation. Please clarify.

I would like to clarify that Planify Capital Limited was incorporated on 16th March 2021 and took the registered valuer’s report. Hence facts’ about the Valuation Report are a matter for which the Registered Valuer is responsible.

e) It seems that the Planify Platform is being operated by Planify Capital, however during the oral submission it has been indicated that Planify Enterprises have sold the shares of Planify Capital through Planify Platform. Provide copy of agreement/ MOU and related documents in this regard wherein Planify Enterprise has used the Planify Platform. Whether the object clause of the Planify Enterprise allowed it to undertake sale and purchase (to deals in) shares.

Please refer Memorandum of Association (MOA) and Articles of Association (AOA) of Planify Enterprises Private Limited

f) It is seen that Planify Capital is owner of shares of various listed/ unlisted companies. On perusal of Financial Statements, these shares have been shown as Non-current Investment and Inventories. Provide justification/ basis for such classification. Whether appropriate disclosures have been made in the financial statements about such classifications.

I would like to clarify that M/s Planify Capital Limited is holding shares in various listed and unlisted Companies in its capacity as “Non-Current Investments” and holding shares of a few Companies as Inventory to further channel the distribution of the same to investors.

g) Is Planify Capital Limited registered as an NBFC?

I would like to clarify that M/s Planify Capital Limited is not an NBFC Company; hence it is not required to get registered as an NBFC Company.

VI. Thus, the subject company sold its shares to Planify Enterprises Private Limited [a group company] and then sold the shares using the Planify platform to 76 persons.

4. Factor considered for Adjudication:

I. At the time of issuance of the SCN to the subject company, it appeared that it had used its platform for issuing its shares to the public. However, during the proceedings, it emerged that the subject company had carried out a more nuanced transaction, which may be understood using the following chart:

II. Thus, the subject company sold its shares to Planify Enterprises Private Limited [identified by subject company as group company managed by same promoter] and then sold the shares using the Planify platform to 76 persons. Thus, the argument advanced by the subject company was that the transactions, involving buying and selling of securities of the subject company, taking place on the Planify Portal were actually secondary market transactions. Therefore, it was argued that section 42 cannot be invoked with regard to these transactions as the subject company was not directly issuing the shares to the people at large using the Planify portal.

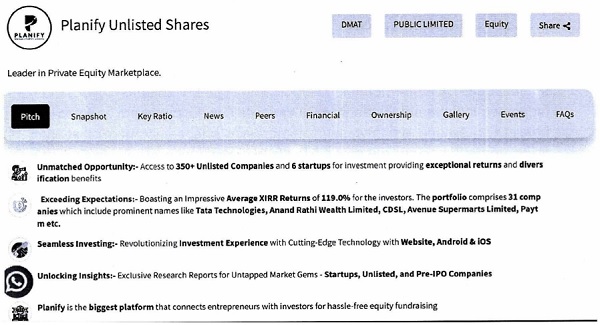

III. The screenshot of the dashboard of the Planify platform used for selling the shares of the subject company is as under:

Iv. The screenshot contains the highlights of the pitch information in respect of the subject company. It indicates two streams of business of the subject company, (1) access to companies and investors to invest in the shares of unlisted companies, and (2) its own portfolio of shares which has yielded average XIRR returns of 119%.

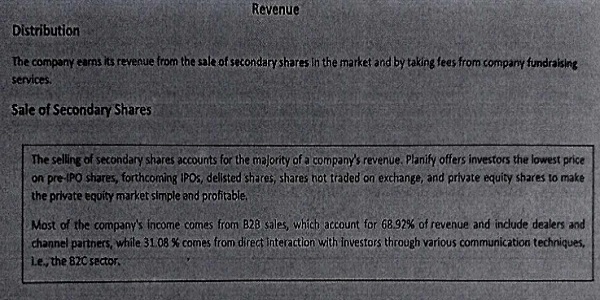

V. This pitch information does not clearly indicate that the subject company does not merely provide a platform for exchange of shares between the companies and the potential investors, rather it tends to buy the shares from the companies and then enters into secondary market transactions to sell the shares to the investors on the platform. However, in its annual report for FY 2021-22, hosted on its platform, this information has been provided. The extract of the same is as under:

It is apparent that close to one-third of its sale comes from B2C, involving direct interaction with individual customers.

VI. The reply of the subject company with regard to the valuation report is unsatisfactory. The subject company cannot entirely cast away the responsibility of the valuation to the valuer. The valuation report [Saugat KC IBBI registration no. IBBURV/05/2019/11636] has been attached to the form PAS-3 filed with the registry and it has also been showcased on the platform. It is an admitted position that the subject company was incorporated on 16th March, 2021, yet the valuation report of the subject company contains financials from 2019. The valuation report shows the date of incorporation as 24th November, 2018 and the CIN as U74990DL2018PTC342098, which belongs to Planify Enterprises Private Limited. This information shows that the valuer had actually been valuing a different company of the group and giving the impression that the subject company is being valued. People at large were also misled by this valuation report.

VII. The subject company has given the minutes of the Board meeting dated 01st April, 2022, wherein the following item was approved:

GENERAL AUTHORISATION TO UTILIZE PLATFORM OF THE COMPANY

The Chairman informed the Board necessity to generally authorize M/s Planify Enterprises Private Limited to utilize Company’s virtual platform. The Board discussed the matter and the following resolution was passed

“RESOLVED THAT pursuant to applicable provisions of the Companies Act, 2013 and Rules framed there under, including any enactment, re-enactment or modifications thereof M/s Planify Enterprises Private Limited, group Company being managed by the same promoters, be and is hereby generally authorized to utilize the virtual platform of the Company.

“RESOLVED FURTHER THAT all the Directors of the Company, for the time being, be and are hereby severally authorized to sign and execute all such documents and papers as may be required for the above purpose.”

VIII. It is evident that the subject company did not engage in selling its own shares on the platform, rather the shares were issued to Planify Enterprises Private Limited, which transferred them to the investors, after the general authorization from the subject company to use the Planify platform. However, clearly, instead of carrying out the valuation in respect of the subject company [whose shares were being transacted], valuation was done in respect of Planify Enterprises Private Limited.

IX. The list of 76 shareholders who bought the shares from Planify Enterprises Private Limited using the platform has been provided by the subject company. The list shows that almost all of them are individuals, some of them have bought as little as 100 shares. The consideration per share is variable, extending from Rs. 85 to Rs. 197. Shri Rajesh Kumar Singla HUF has bought 3,51,558 shares at Rs. 85 per share. He is also a director (promoter category) and shareholder in the subject company as well as in the Planify Enterprises Private Limited.

X. Now section 42(7) of the Companies Act, 2013 lays down certain prohibitions, one of them is the use of a “distribution channel”. The present facts clearly indicate that Planify Platform used by Planify Enterprises Private Limited was a “distribution channel” of the subject company to inform the public at large about the issue of the subject company. It was for this reason that Planify Enterprises Private Limited was given the authorization to utilize the Planify platform [owned by the subject company] so that the shares of the subject company can be transferred to the potential buyers. It is evident that the information related to the buying of shares of the subject company were hosted on the Planify platform, along with crucial information related to the pitch, financial ratios, news, etc. This was followed by Youtube videos and advertorials in the news portal, which encouraged people at large to buy the shares of the subject company. The shares were largely bought by individuals.

XI. During the adjudication proceedings in respect of a similar matter in respect of Mayas heel Retail India Limited, .it was noted that a Fundraising Agreement was entered into, which gave the subject company the right to find potential investors for “Mayas heel Retail India Limited” on its platform. In the present case, since both the companies are in the same group, there was no fundraising agreement, as such. However, the general authorization has been given through a Board resolution. Further, in the case of Mayasheel Retail India Limited, it was seen that Planify Capital Limited had published an misleading advertorial on 31.12.2021 in ANI and other news portals like Business Standard and Print to generate interest in people for transacting in shares through Planify Platform.

XII. As per the financial statements of Planify Enterprises Private Limited for past two preceding financial years, details of Stock-in-trade and investment are as follows:

|

Particulars |

F.Y. 2022-2023 | F.Y. 2021-2022 |

| Non-current investments | 00 | 00 |

| Stock-in-trade | Rs. 12,03,333 | Rs. 12,01,814 |

XIII. It cannot be denied that the purpose of the selling the shares to Planify Enterprises Private Limited was to only find the potential investors for the subject company through the Planify Platform. The real intention was to issue the shares to the public at large. Thus, the first transaction whereby the shares of the subject company were issued to Planify Enterprises Private Limited was merely a smokescreen. Thus, the provisions of section 42(7) of the Companies Act, 2013 stood violated.

XIV. It is also clarified that while in the context of secondary market transactions, section 58(2) provides for free transferability of securities of a public company and also provides for enforceability of a contract in respect of transfer of securities, such provision would be applicable subject to section 42(7). In the present case, the private placement of shares of the subject company to Planify Enterprises Private Limited was solely done to find potential buyers for its securities through the Planify platform, thereby it results into creation of a distribution channel, which is prohibited under section 42(7). Thus, the selling of shares of the subject company [bought by Planify Enterprises Private Limited through private placement] on the Planify platform would not get the protection of section 58(2) as this selling was not a transaction simpliciter between the buyer and the seller of securities as envisaged under section 58(2), rather it emanated out of a private placement which created a distribution channel [a prohibited act] for selling of securities to the public at large on the platform and thus it is violative of section 42(7).

XV. On the basis of the records available in this office and on the basis of the submission made by parties, it is seen an amount of Rs 3,89,53,017 was raised by the subject company through the Planify platforms by selling its 4,53,530 shares to Planify Enterprises Private Limited and subsequently those were offered to 76 investors. This transaction is violative of section 42(7) for the aforesaid reasons.

XVI. In the present case, the penalty is leviable under section 42(10) of the Act. As far as returning the money to the subscribers under section 42(6) is concerned, clause (b) of the proviso section 42(6) clearly provides that such an eventuality would arise if the company is unable to allot the securities. In the present case, since the securities have been allotted, the issue of returning the monies to the subscribers does not arise.

5. The relevant provision of the section 42 of the Act is as under: –

42. Issue of shares on private placement basis.—

(1) A company may, subject to the provisions of this section, make a private placement of securities.

(2) A private placement shall be made only to a select group of persons who have been identified by the Board (herein referred to as “identified persons”), whose number shall not exceed fifty or such higher number as may be prescribed [excluding the qualified institutional buyers and employees of the company being offered securities under a scheme of employees stock option in terms of provisions of clause (b) of subsection (1) of section 62], in a financial year subject to such conditions as may be prescribed.

(3) A company making private placement shall issue private placement offer and application in such form and manner as may be prescribed to identified persons, whose names and addresses are recorded by the company in such manner as may be prescribed:

Provided that the private placement offer and application shall not carry any right of renunciation.

Explanation I.—”private placement” means any offer or invitation to subscribe or issue of securities to a select group of persons by a company (other than by way of public offer) through private placement offercum-application, which satisfies the conditions specified in this section.

Explanation II.—”qualified institutional buyer” means the qualified institutional buyer as defined in the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended from time to time, made under the Securities and Exchange Board of India Act, 1992, (15 of 1992).

Explanation III.—If a company, listed or unlisted, makes an offer to allot or invites subscription, or allots, or enters into an agreement to allot, securities to more than the prescribed number of persons, whether the payment for the securities has been received or not or whether the company intends to list its securities or not on any recognised stock exchange in or outside India, the same shall be deemed to be an offer to the public and shall accordingly be governed by the provisions of Part I of this Chapter.

(4) Every identified person willing to subscribe to the private placement issue shall apply in the private placement and application issued to such person alongwith subscription money paid either by cheque or demand draft or other banking channel and not by cash:

Provided that a company shall not utilise monies raised through private placement unless allotment is made and the return of allotment is filed with the Registrar in accordance with sub-section (8).

(5) No fresh offer or invitation under this section shall be made unless the allotments with respect to any offer or invitation made earlier have been completed or that offer or invitation has been withdrawn or abandoned by the company:

Provided that, subject to the maximum number of identified persons under sub-section (2), a company may, at any time, make more than one issue of securities to such class of identified persons as may be prescribed.

(6) A company making an offer or invitation under this section shall allot its securities within sixty days from the date of receipt of the application money for such securities and if the company is not able to allot the securities within that period, it shall repay the application money to the subscribers within fifteen days from the expiry of sixty days and if the company fails to repay the application money within the aforesaid period, it shall be liable to repay that money with interest at the rate of twelve per cent. per annum from the expiry of the sixtieth day:

Provided that monies received on application under this section shall be kept in a separate bank account in a scheduled bank and shall not be utilised for any purpose other than—

(a) for adjustment against allotment of securities; or

(b) for the repayment of monies where the company is unable to allot securities.

(7) No company issuing securities under this section shall release any public advertisements or utilise any media, marketing or distribution channels or agents to inform the public at large about such an issue.

(8) A company making any allotment of securities under this section, shall file with the Registrar a return of allotment within fifteen days from the date of the allotment in such manner as may be prescribed, including a complete list of all allottees, with their full names, addresses, number of securities allotted and such other relevant information as may be prescribed.

(9) If a company defaults in filing the return of allotment within the period prescribed under sub-section (8), the company, its promoters and directors shall be liable to a penalty for each default of one thousand rupees for each day during which such default continues but not exceeding twenty-five lakh rupees.

(10) Subject to sub-section (11), if a company makes an offer or accepts monies in contravention of this section, the company, its promoters and directors shall be liable for a penalty which may extend to the amount raised through the private placement or two crore rupees, whichever is lower, and the company shall also refund all monies with interest as specified in sub-section (6) to subscribers within a period of thirty days of the order imposing the penalty.

6. Adjudication of penalty: –

a. That the provision pursuant to sub-section (7) of Section 42 of the Act, no company issuing securities under this section shall release any public advertisements or utilize any media, marketing or distribution channels or agents to inform the public at large about such an issue. The subject company has violated sub-section (7) of section 42 of the Act. The penal provision for the same is provided at sub-section (10) of Section 42 of the Act.

b. Section 42(7) of the Act provides the ceiling upto which a penalty can be imposed on the company, directors and promoters. In the present case, the Rs. 3,89,53,017 was raised by selling the shares to Planify Enterprises Private Limited, which in turn acted as a “distribution channel” for selling the shares to the investors on the Planify platform. The amount raised is more than Rs. 2 crores, so the amount of penalty cannot exceed Rs. 2 crores.

c. Since this provision does not provide for a fixed penalty, the provisions of rule 3(12) of the Companies (Adjudication of Penalties) Rules, 2014 are applicable. The said provision reads as under:

“(12) While adjudging quantum of penalty, the adjudicating officer shall have due regard to the following factors, namely:-

a. size of the company;

b. nature of business carried on by the company;

c. injury to public interest;

d. nature of the default;

e. repetition of the default;

f. the amount of disproportionate gain or unfair advantage, wherever quantifiable, made as a result of the default; and

g. the amount of loss caused to an investor or group of investors or creditors as a result of the default:

Provided that, in no case, the penalty imposed shall be less than the minimum penalty prescribed, if any, under the relevant section of the Act.”

d. The paid-up capital of the company is Rs. 8,37,45,753/-. Its profit after tax during FY 2021-22 was Rs. 8,25,33,526, which has reduced to Rs. 70,45,950 in FY 2022-23. However, the subject company has reserves and surplus amounting to Rs. 4.5 crores in FY 2022-23. The nature of the business is evident from above and the company has not even registered itself as an NBFC. The business of the company involves risks for the retail investors which may lead to injury to public interest. The company has in the present matter raised money for itself but otherwise it has raised money for other companies, whereby it has acted as a “distribution channel” for companies to reach out to investors, in a manner which is prohibited under section 42(7) for the reasons cited above. It is not possible to quantify the amount of total gain or loss in this matter. Again, it may be noted that the company had provided a misleading copy of the valuation report, as seen above.

e. Considering that all the aggravating factors are stacked up against the company, this is fit case to impose the maximum penalty on the company for the violation of section 42(7). Similarly, the liability of Shri Rajesh Kumar Singla is undeniable as he is the very face of the company and its mind and soul, which is evident from the advertorials and the social media of the company. Thus, he is also liable for maximum penalty under section 42(7).

f. As regards the role of other directors is concerned, the role of independent directors is governed by section 149(12) which reads as under:

“149 (12) Notwithstanding anything contained in this Act,—

(i) an independent director,.

(ii) a non-executive director not being promoter or key managerial personnel, shall be held liable, only in respect of such acts of omission or commission by a company which had occurred with his knowledge, attributable through Board processes, and with his consent or connivance or where he had not acted diligently.”

g. Clearly, the non-executive directors/independent directors are in the know about the business model of the company. The Board resolution authorizing Planify Enterprises Private Limited to utilize the Planify platform for selling the shares of the subject company which is the core default in this case was in their knowledge too. Thus, the non-executive directors/independent directors or other directors/promoters as on the date of the date of private placement, i.e. 27th June, 2022 made to Planify Enterprises Private Limited would be liable for the default of section 42(7). Each of them are liable to a penalty of one-half of the maximum penalty provided under section 42(7).

h. Now in exercise of the powers conferred on the undersigned vide Notification dated 24th March, 2015 and having considered the reply submitted by the subject company in response to the notice on 31.10.2023 and hearing in the matter held on 19.12.2023 and further reply dated 16.01.2024, hereby impose the penalty on the company and its officers in default under section 42 (10) of the Act r/w Rule 3(12) of the Companies (Adjudication of Penalties) Rules, 2014, for violation of section 42 (7) of the Companies Act, 2013 which are as follows:-

|

Violation |

Penalty imposed on company/ director(s)/promoter(s) |

Total penalty imposed u/s 42 of the Companies Act, 2013 in INR |

| A | B | C |

| Section 42 (7) | PLANIFY CAPITAL LIMITED | 2,00,00,000 |

| Sh. Rajesh Kumar Singla | 2,00,00,000 | |

| Ms. Urmila Rani Singla | 1,00,00,000 | |

| Sh. Davinder Kumar Singla | 1,00,00,000 | |

| Sh. Uttam Prakash Agarwal | 1,00,00,000 |

7. Order:

a. Names of party as mentioned in the table above are hereby directed to pay the penalty amount as per column no. ‘C’ In case of parties other than company, such amount is required to be paid out of their own funds.

b. The said amount of penalty through online by using the website mca.gov.in (Misc. head) in favor of “Pay & Accounts Officer, Ministry of Corporate Affairs, New Delhi, payable at Delhi, within 90 days of receipt of this order, and intimate this office with proof of penalty paid.

c. Appeal against this order may be filed with the Regional Director (NR), Ministry of Corporate Affairs, B-2 Wing, 2nd Floor, Paryavaran Bhawan, CGO Complex, Lodhi Road, New Delhi-110003 within a period of sixty days from the date of receipt of this order, in Form ADJ [available on Ministry website mca.gov.in] setting forth the grounds of appeal and shall be accompanied by a certified copy of the order. [Section 454(5) & 454(6) of the Act read with Companies (Adjudicating of Penalties) Rules, 2014].

d. Your attention is also invited to section 454(8) of the Act in the event of non-compliance of this order.

Place: New Delhi.

(Pranay Chaturvedi, ICLS)

(Adjudicating Officer)

Registrar of Companies,

NCT of Delhi & Haryana

No. ROC/D/ADJ/Section42/Planify/1662-1667

Date: 03-04-2024