GST Major Amnesty Scheme u/s 128A

No Interest No Penalty for FY 2017-18, 2018-19 and 2019-20

Summary: The GST Amnesty Scheme 2024, introduced via Section 128A of the CGST Act, offers a conditional waiver of interest and penalties for tax demands from FY 2017-18 to 2019-20 under Section 73. To qualify, taxpayers must fully pay outstanding tax dues by March 31, 2025. The scheme excludes certain demands, such as erroneous refunds, unless the full tax amount, including penalties, is settled. Taxpayers must withdraw pending appeals before applying and submit necessary documentation via Forms GST SPL-01 or SPL-02. The waiver does not cover self-assessed interest on late returns. Payments can be made using Input Tax Credit (ITC) except for reverse charge or erroneous refunds, which require cash payments. The scheme applies to CGST, SGST, IGST, and Compensation Cess. While aimed at reducing litigation, the process involves extensive compliance, multiple verification stages, and potential rejections, leading to further appeals. The GST Council is urged to consider extending the deadline and broadening the scheme’s scope to enhance its effectiveness in dispute resolution and revenue collection. Taxpayers should carefully evaluate risks, procedural requirements, and financial implications before opting for the scheme.

A. BACKGROUND

> The GST Amnesty Scheme has been introduced vide Section 146 of Finance (No. 2) Act 2024 (No. 15 of 2024) dated 16th August 2024 based on the recommendation made in the 53rd GST Council Meeting to provide Conditional Waiver of Interest or Penalty or both for demands related to the Financial Years 2017-18, 2018-19, and 2019-20 under Section 73 of the CGST Act, subject to certain conditions, through Section 128A of the CGST Act.

> In its 54th meeting, the GST Council introduced Rule 164 to the CGST Rules through Notification No. 20/2024 dated 08.10.2024, outlining the procedure and conditions for closing proceedings under Section

> Additionally, Notification No. 21/2024, dated 08.10.2024, sets March 31, 2025, as the deadline for taxpayers to fully pay tax demands to benefit from the waiver of interest or penalties under Section 128A.

> Further, clarification regarding application and the procedure was given by issuing Circular 238/32/2024-GST- Dated- 15/10/2024.

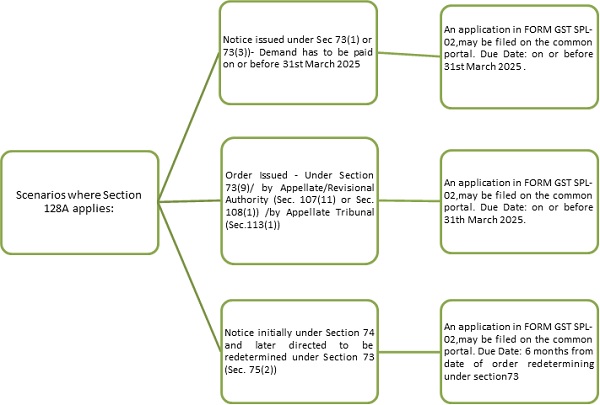

B. SCOPE OF SECTION 128A

> No interest or penalty will be charged, and all related proceedings for the specified notice, order, or statement (as outlined below) will be considered fully settled under the following conditions:

If a taxpayer has outstanding tax liabilities for the period from July 1, 2017, to March 31, 2020, and the taxpayer settles the full tax amount as outlined in the notice, statement, or order on or before the date specified in the official

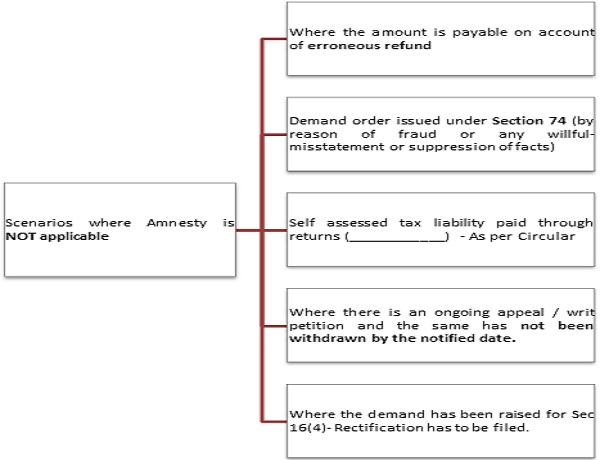

C. EXCLUSIONS

D. POINTS TO REMEMBER BEFORE FILING SPL FORMS

- Taxpayers must withdraw any appeal or writ petition related to Section 128A proceedings before applying for a waiver of interest or penalty.

- A withdrawal order must be attached with the application in FORM GST SPL-01 or SPL-02 or submit proof of filing if the order is pending and upload the final order within one month of receipt.

- For multiple notices / orders under Section 73 (July 2017 to March 2020), file a separate FORM GST SPL-01 or SPL-02 for each.

- If a notice / order contains multiple issues including erroneous refund as one of its demands, in such cases waiver applications can only be made after paying the full tax amount, including any incorrect / erroneous refunds along with interest & penalty, since it does not qualify for the amnesty scheme settlement.

- Waiver application also comes along with foregoing the benefit of tax litigation and are also subject to restrictions / limitations. Hence a careful evaluation of all facts & available options along with the pros & cons should be done as an informed decision-making process before making waiver application.

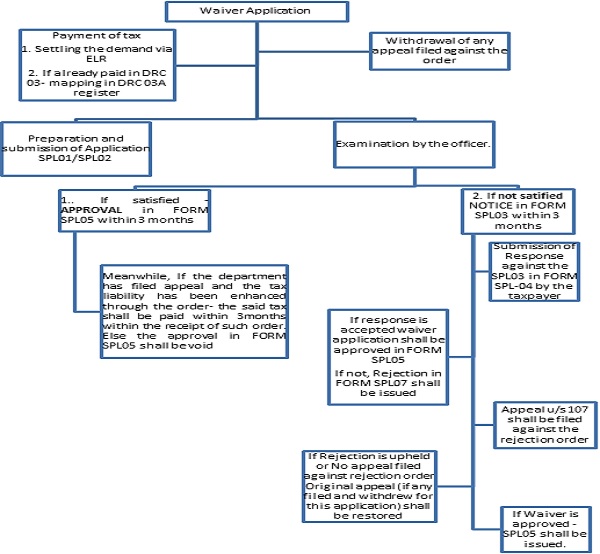

E. WAIVER APPLICATION PROCESS UNDER SECTION 128A – KEY STEPS:

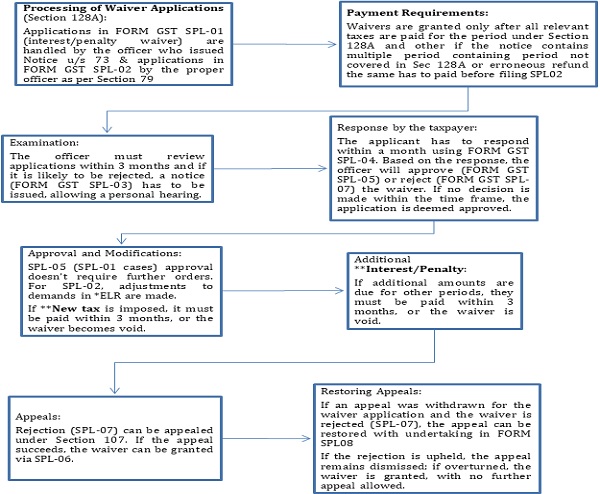

F. PROCESSING OF SPL APPLICATION FORMS

G. CLARIFICATIONS ISSUED VID CIRCULAR 238/31/2024 DATED 15TH OCTOBER 2024

| S.NO | Taxpayer Question | Clarification by CBIC |

| 1. | Whether the benefit under Section 128A available to taxpayers who paid the full tax amount before the section came into effect? | Yes, payments made towards tax demands, even before Section 128A came into effect, will be considered if paid by the notified date, as long as they were intended for that specific demand. |

| 2. | Can the tax amount recovered by tax officers from another person on behalf of the taxpayer be treated as tax paid towards a specific demand under Section 128A? | Yes, any amount recovered by tax officers from another person on behalf of the taxpayer will be considered as tax paid towards the demand if recovered by the notified date under Section 128A. |

| 3. | Can the interest or penalty amounts recovered by tax officers for demands under Section 73 for the financial years 2017-18, 2018-19, and 2019-20 be adjusted against the tax payable for the same demand under Section 73 for those years? | No, amounts paid or recovered as interest or penalty cannot be adjusted against tax dues. Refunds of such amounts are not allowed as per Section 128A. |

| 4. | Is the benefit under Section 128A applicable if the tax due has already been paid and the notice or demand under Section 73 relates only to interest and/or penalty? | The benefit under Section 128A can apply if the tax has been paid and the demand only concerns interest or penalty. However, it does not cover interest due to late return filing or delayed reporting, as this is considered self- assessed and directly recoverable. |

| 5. | Can a taxpayer get partial waiver of interest or penalty by paying part of the tax and disputing the rest? | No, Section 128A only allows waiver if the full tax amount in the notice/order is paid. |

| 6. | If a notice covers periods eligible and not eligible for waiver under Section 128A, can the taxpayer still claim a waiver? | Yes, but the taxpayer must pay the total tax demanded. The waiver applies only to periods covered by Section 128A. |

| 7. | Can a waiver application be filed if the notice involves tax demand due to erroneous refunds? | Yes, but the full tax amount must be paid, including the erroneous refund. Waiver benefits apply to tax other than the erroneous refund. |

| 8. | What happens if a taxpayer does not pay additional tax demanded after an appeal while seeking waiver under Section 128A? | If additional tax is not paid within three months of the appellate order, the waiver benefits granted under Section 128A will be void. |

| 9. | What is the process to avail waiver if an SLP is pending before the Supreme Court? | The taxpayer must withdraw the SLP and submit proof of withdrawal with the waiver application in the prescribed form. |

| 10. | Does Section 128A waiver apply to IGST and Compensation Cess? | Yes, waivers under Section 128A are also applicable to IGST and Compensation Cess, provided the full payment of CGST, SGST, IGST, and Compensation Cess is made. |

| 11. | Does Section 128A cover cases of wrongly availed transitional credit? | Yes, if the transitional credit was availed during the period covered under Section 128A and a demand notice was issued under Section 73, it is included under the waiver provisions. |

| 12. | Does the waiver under Section 128A apply to penalties, late fees, or fines? | The waiver applies to penalties under sections like 73, 122, and 125, but does not cover late fees, redemption fines, or similar charges. |

| 13. | Can payment for availing waiver under Section 128A be made using ITC? | Yes, the tax payment can be made using Input Tax Credit (ITC) or cash. However, payments for reverse charge or erroneous refunds must be made in cash only. |

| 14. | If the tax demand reduces due to retrospective changes in Section 16, should the full amount in the notice be paid to avail benefits under Section 128A? | No, as per Rule 164(5), the amount payable for availing benefits under Section 128A should be calculated after deducting the amount not payable due to changes in Section 16(5) and (6). Taxpayers need to pay only the adjusted amount and should provide a breakdown of deductions in FORM GST SPL-01 or SPL-02. There’s no need for a rectification application if the adjustment is due to these retrospective changes, as per the special procedure notified on October 8, 2024. |

| 15. | If an applicant has paid tax through FORM GST DRC-03, is it mandatory to file FORM GST DRC-03A or adjustment against tax demand before applying in FORM GST SPL-02? | Yes. If an order has been issued in FORM GST DRC-07, DRC-08, or APL-04, and the applicant has paid through FORM GST DRC- 03, they must adjust this payment against the tax demand in the Electronic Liability Register as per Rule 164(2) before filing FORM GST SPL-02. |

| 16. | If an applicant has paid full or partial tax through FORM GST DRC-03, are they required to file FORM GST DRC-03A to adjust this tax amount against a demand in FORM GST DRC-07, DRC-08, or APL-04? | Yes, the applicant must file FORM GST DRC- 03A to adjust the tax amount paid through FORM GST DRC-03 against the demand as per the order in FORM GST DRC-07, DRC- 08, or APL-04, before submitting the application in FORM GST SPL-02, as per rule 164(2). |

–

| Note: The Circular is only for clarification and remains as administrative instruction and it can never impose any condition. At any point of time this circular may not prevail over the statutory law. |

H. APPLICATION FORM AND ONLINE PROCEDURE

GSTIN has issued various advisories to aid the taxpayer in submitting this SPL forms in the portal. One of the major advisory to be noted is that the Advisory released on Jan 14th, 2025.

1. One of the eligible conditions for filing application under waiver scheme is to withdraw the appeal applications filed against the demand order/notice/statement for which waiver application is to be submitted. In this regard, it is to inform that for the appeal applications (APL 01) filed before First Appellate authority, withdrawal option is already available in the GST portal.

2. However, for the appeal applications (APL 01) filed before 21.03.2023, withdrawal option is not available in GST portal.

3. For such cases, the taxpayers are advised to submit their request for withdrawal of appeal applications to the concerned Appellate Authority.

4. The Appellate authority will forward such requests to GSTN through State Nodal officer for withdrawal of such appeal applications (i.e. filed before 21.03.2023 and not disposed off) from backend .

5. GSTIN has also given a grievance redressal mechanism in the self service system in case of any queries or issues. The same can be accessed through the following link: https://selfservice.gstsystem.in

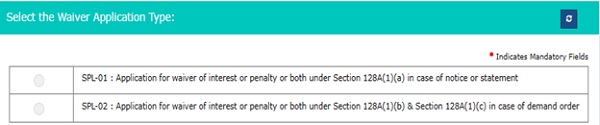

6. Below are the steps to be followed for SPL-01

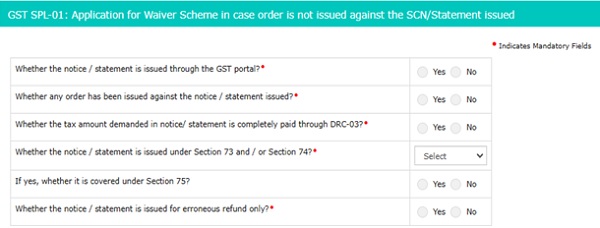

7. Upon selecting SPL-01 the below page appears.

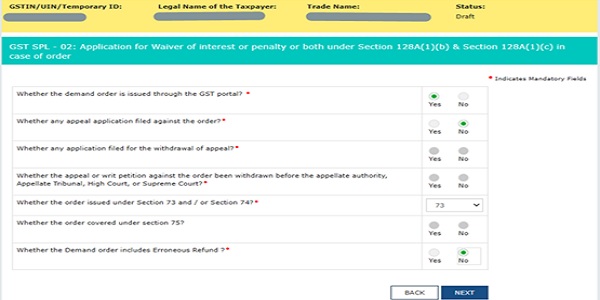

8. Upon selecting SPL-02 the below page appears.

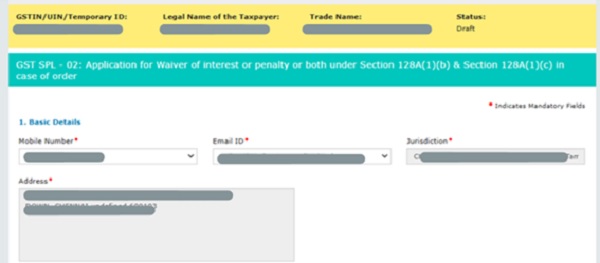

9. On careful selection of the options the application form appears. The application form has seven parts in total (This applies to both SPL01 and SPL02 with minor changes)

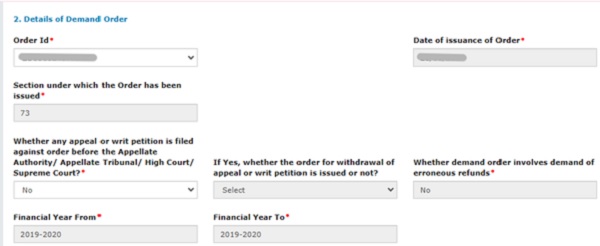

10. Details of Demand order- Order ID has to be selected- Date of issuance and Section are auto-populated. Details of appeal status have to be filled.

Note: If “No” is selected for the question “Whether the demand order issued through the GST portal- Then the demand order details have to be entered manually.

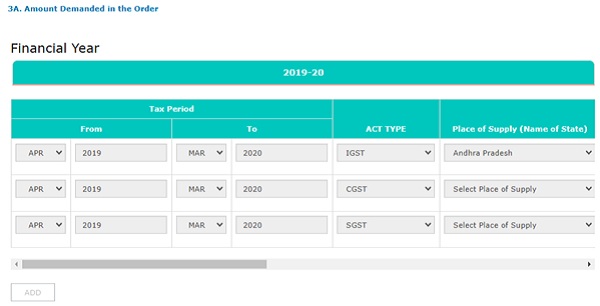

b. i). Details of Demand is auto populated

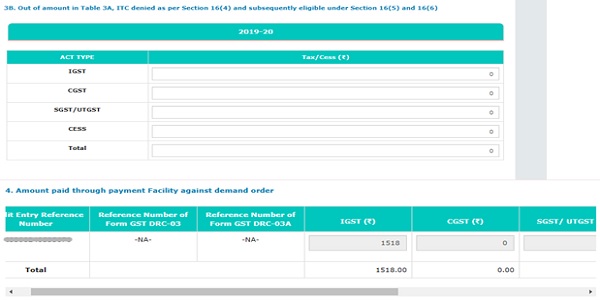

ii). Out of total demand – Details of Demand raised for ITC for violation of Section 16(4) which is now eligible u/s 16(5) and 16(6) are to be entered in this table

c) Details of Payment of tax are auto populated – If paid through DRC 03 and adjusted through DRC 03A the reference number of the same will be reflected and if the same is settled against the liability Credit entry reference number will be reflected

–

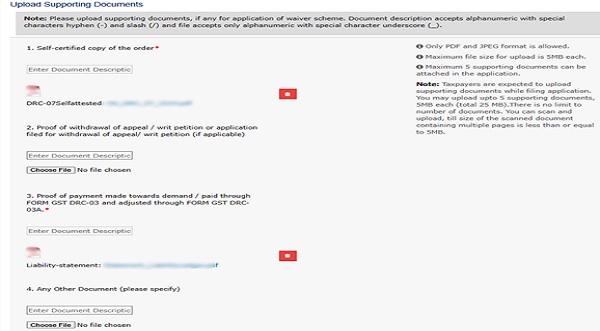

d) Further, the following supporting documents are required to be uploaded. Hence, it is advised to keep the same ready:

i. Self-attested copy of the Order in original

ii. Proof of withdrawal of Appeal/ Writ application

iii. Proof of payment of tax DRC 03 and adjusted through DRC 03A (If adjusted through E-Liability ledger then the E-liability register shall be uploaded as proof)

iv. Any other supporting documentation

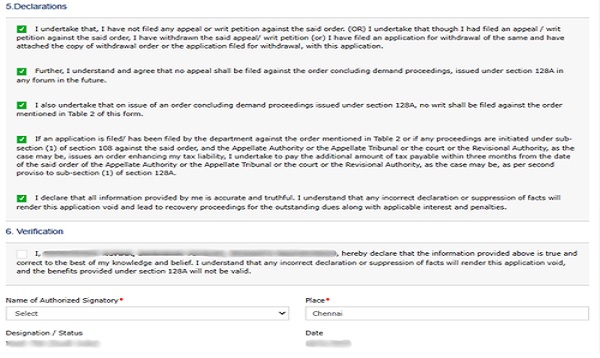

e) A set of declarations has to be submitted by selecting the check box and finally, a verification has to be submitted by the authorized signatory.

I. Conclusion

The waiver application and process under Section 128A serves as a relief mechanism but imposes a burdensome procedural compliance, various limitations and stringent timeline on taxpayers. The long chain of verification followed by possible rejection and then appeals again puts in a longer path of compliance and litigations in a circular manner. Considering various limitations in the framework of the scheme GST Council should also consider widening the scope in the larger interest of settling more disputes, minimizing litigation and expediting revenue collections.

Although the scheme was introduced on August 16, 2024, with provisions enacted w.e.f. November 1, 2024, the necessary forms were made available on the portal only in January 2025, however, the time limit to avail the benefit under the scheme is only till March 31, 2025. Hence, the taxpayer requires mindful time in order to analyze the underlying risk and computing the benefits of availing of this scheme. Therefore, CBIC should consider extending the time limit for the taxpayers to apply for this scheme.

There are multiple decisions making at multiple stages which also results in choosing one over the other, thereby foregoing opportunity benefit of the other. Taxpayers should exercise abundant care & caution and take informed decisions to assess the cost benefit analysis in determining whether to take advantage of the amnesty scheme or to contest any outstanding issues.

****

Author: CA Saradha Hariharan, Co-Founder of GGSH & Co. LLP, Chartered Accountants, Chennai. She is a A distinguished Chartered Accountant specializing in GST and an enthusiastic speaker and author in the field of Indirect Taxes.

Author: CA Saradha Hariharan, Co-Founder of GGSH & Co. LLP, Chartered Accountants, Chennai. She is a A distinguished Chartered Accountant specializing in GST and an enthusiastic speaker and author in the field of Indirect Taxes.