The order issued by the Office of Registrar of Companies, NCT of Delhi & Haryana, dated 22.05.2024, pertains to penalizing LinkedIn Technology Information Private Limited (hereafter referred to as “LinkedIn India”) for violations under Sections 89 and 90 of the Companies Act, 2013. The violations relate to the incorrect filing of forms regarding beneficial ownership and significant beneficial ownership.

1. Violations under Section 89: LinkedIn India filed an e-form MGT-6 stating that LinkedIn Technology Unlimited Company is the registered holder and LinkedIn Ireland Unlimited Company is the beneficial owner of 01 share, with the date of creation of beneficial interest as 11.01.2024. However, financial statements filed earlier indicated that the beneficial interest had arisen much earlier. Additionally, LinkedIn India failed to declare its significant beneficial owner as required by Section 90 of the Act.

LinkedIn India argued that the beneficial ownership always vested with LinkedIn Ireland, reaffirmed during an amalgamation in 2014. They claimed the filing was made to err on the side of caution due to the ambiguous language of Section 89(2). However, the reply was deemed unsatisfactory, and LinkedIn India was asked to provide reasons for the incorrect information. They reiterated their stance during a hearing.

The analysis found LinkedIn India’s response inadequate. It was concluded that both LinkedIn Technology Unlimited Company and LinkedIn Ireland Unlimited Company failed to make accurate declarations, rendering them liable for penalties.

2. Violations under Section 90: The analysis examined beneficial ownership through holding subsidiary relationships, reporting channels, and financial control. It found that Mr. Satya Nadella and Mr. Ryan Roslansky were significant beneficial owners due to their ability to control the subject company, as indicated by their positions within LinkedIn Corporation and Microsoft Corporation. The analysis also highlighted the appointment patterns of directors, suggesting their allegiance to Microsoft and LinkedIn.

Penalties Imposed:

- LinkedIn Technology Unlimited Company and LinkedIn Ireland Unlimited Company were penalized under Section 89(5) for violations between 21.12.2020 and 15.02.2024.

- Mr. Satya Nadella, Mr. Ryan Roslansky, and other directors were penalized under Section 90(10) and Section 90(11) for violations between 01.07.2020 and 15.02.2024.

- The penalties ranged from Rs. 50,000 to Rs. 5,00,000, to be paid within 90 days of receipt of the order.

Conclusion: The order underscores the importance of accurate filings regarding beneficial ownership and significant beneficial ownership. It reflects a meticulous examination of corporate structures and relationships to ensure compliance with the Companies Act, 2013. LinkedIn India’s attempts to justify its actions were deemed insufficient, leading to penalties for various entities and individuals involved.

GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS,

OFFICE OF REGISTRAR OF COMPANIES,

NCT OF DELHI & HARYANA

4TH FLOOR, IFCI TOWER, 61,

NEHRU PLACE, NEW DELHI – 110019

Order No. ROC/D/Adj/Order/Section 89&90/2246- 2256 Date: 22.05.2024

ORDER FOR PENALTY FOR VIOLATION UNDER SECTION 89 AND SECTION 90 OF THE COMPANIES ACT, 2013 IN THE MATTER OF LINKEDIN TECHNOLOGY INFORMATION PRIVATE LIMITED (CIN-U72900DL2009PTC197503)

1. Appointment of Adjudicating Officer: –

Ministry of Corporate Affairs vide its Gazette Notification No. A-42011/112/2014-Ad.II, dated 24.03.2015 appointed Registrar of Companies, NCT of Delhi & Haryana

as Adjudicating Officer in exercise of the powers conferred by section 454(1) of the Companies Act, 2013 (hereinafter known as Act) r/w Companies (Adjudication of Penalties) Rules, 2014 for adjudging penalties under the provisions of this Act.

2. Company: –

Whereas the company viz. LINKEDIN TECHNOLOGY INFORMATION PRIVATE LIMITED (herein after known as ‘company’ or ‘subject company’ or ‘LinkedIn India’) was incorporated on 31.12.2009 and has its registered office as per MCA21 Register address at 16A/20, WEA MAIN AJMAL KHAN ROAD, KAROL BAGH, NEW DELHI , Delhi , 110005, India. The financial & other details of the subject company for immediately preceding F.Y.2022-23 as available on MCA-21 portal is stated as under:

| S. No. | Particulars | Details |

| 1. | Paid up capital (INR in Millions) | 28.56 |

| 2. | a. Revenue from operation (INR in Millions) | 18,314.33 |

| b. Other Income (INR in Millions) | 419.78 | |

| c. Profit for the Period (INR in Millions) | 2402.29 | |

| 3. | Holding Company | Yes |

| 4. | Subsidiary Company | No |

| 5. | Whether company registered under Section 8 of the Act? | No |

| 6. | Whether company registered under any other special Act? | No |

3. Facts of the Case: –

I. It was noted that the company had filed an e-form MGT-6 vide SRN F91257345 dated 29.01.2024 wherein it is reported that LinkedIn Technology Unlimited Company is a registered holder and LINKEDIN Ireland Unlimited Company is a beneficial owner in respect of 01 share of the subject company and date of creation of beneficial interest has been shown as 11.01.2024. This ran contrary to the filings made in the financial statements of the subject company which showed that the beneficial interest had arisen much earlier. The company had also not declared its significant beneficial owner as required under the provisions of section 90 of the Act.

II. Accordingly, a Show Cause Notice (SCN) for Adjudication dated 15.02.2024 was issued to ascertain compliances of Section 89 and 90 of the Act.

4. Adjudication proceedings for issues concerning Section 89 of the Act:-

I. The queries [in bold] concerning the compliance of section 89 of the Act raised through the SCN dated 15.02.2024 and replies [in italics] received on 28.02.2024 are as follows:

It is observed from the record that company has filed form MGT-6 vide SRN F91257345 dated 29.01.2024 wherein it is reported that LinkedIn Technology Unlimited Company is a registered holder and LINKEDIN Ireland Unlimited Company is a beneficial owner of 01 share of the subject company and date of creation of beneficial interest has been shown as 11.01.2024. However, as per financial statement filed by the company vide form AoC-4 XBRL (SRN F69803310 dated 20.10.2023) filed for F.Y. 2022-2023, it is mentioned that LinkedIn Technology Unlimited Company, a company incorporated under the laws of Ireland holds 1 share (0.01%) in the company as a nominee shareholder of Linkedln Ireland.

In view of the above, declarations given under the provision of Section 89(1) and 89(2) (i.e. declaration given in MGT-4 and MGT-5) are incorrect. Further, it is seen that company was already aware of the fact that the registered owner and the beneficial owner w.r.t I (one) share is different. Thus, it is seen that form MGT-6 filed by company vide SRN-F91257345 is also not compliant with section 89(6) of the Act as the creation of beneficial interest predates 11.01.2024. Thus, the adjudicating officer has sufficient cause to believe that there is non-compliance of section 89.

Company’s Response:

- We would like to clarify that the beneficial ownership of One (1) equity share held by Linkedln Technology Unlimited Company (“Linkedln Unlimited”) vests and always vested with Linkedln Ireland Unlimited Company (“Linkedln Ireland”). This was reaffirmed when Linkedln India underwent an amalgamation with Uzanto Consulting India Private Limited in 2014. At the time of the merger, the beneficial ownership in respect of One (1) equity share held by Linkedln Unlimited was reaffirmed to be in favour of Linkedln Ireland and was duly disclosed to the High Court, the Registrar of Companies and other statutory authorities.

- Under the new Companies Act, 2013, the existence of this beneficial ownership has been noted in the annual returns filed since FY 20142015.

- Rationale for filing form MGT-6 – In light of Section 89(2) which states “Every person who holds ” we erred on the side of caution and filed form MGT-6 vide SRN F91257345 dated 29.01.2024. However, we note the date of creation has erroneously shown to be January 11, 2024, since the declaration(s) were submitted on the said date.

As you have correctly noted under the SCN, this has always been in existence as set out in the annual filings. As this appears to be either not required to be filed or is creating an ambiguity, Linkedln India stands to withdraw the filed form MGT-6 vide SRN F91257345 dated 29.01.2024 and seeks your accommodation for the withdrawal. Both, Linkedln Ireland and Linkedln Unlimited, owing to abundance of caution and the language of Section 89(1) and (2) of the Companies Act, had submitted their declaration(s), due to the potential ambiguity in the interpretation of Section 89.

- Based on our response above, the statement mentioned as per the financial statements filed for FY 2022-2023 and previous financial years are correct where Linkedln Ireland is the beneficial owner of One (1) equity share held by Linkedln Unlimited.

- As mentioned earlier, to err on the side of caution, both Linkedln Technology and Linkedln Ireland had made their declaration(s) on 11.01.2024. while the date of creation of beneficial interest is mentioned as 11.01.2024, as per our response above, this has already been in existence since 2014.

- Based on the above responses, we trust we have clarified the position of Linkedln India on the above declarations and subject to the consent of your good office, we would be glad to withdraw the form MGT-6 filed vide SRN-F91257345 given that Linkedln Unlimited had historically declared the beneficial ownership in favour of Linkedln Ireland and ensured that its corporate records are in alignment of this beneficial ownership,

- We request your good office to kindly consider the rationale for the recent filing, which in our opinion, show cause that Linkedln India has not committed a non-compliance under Section 89 as stipulated under the SCN.

II. The reply given by the subject company was found to be unsatisfactory. Thus, vide an email dated 04.03.2024, the company was asked to furnish the reasons for providing incorrect information in the e-form MGT-6 [SRN-F91257345] and its attachments w.r.t the date of creation/acquisition of beneficial interest in the shares. A hearing was also scheduled on 12.03.2024.

III. In its reply dated 12.3.2024, the subject company stated as follows:

LinkedIn India opted for a cautious approach and reaffirmed the beneficial ownership interest in favour of LinkedIn Ireland Unlimited Company, due to section 89 (2) of the Companies Act 2013, which uses the phrase every person who hold consequently LinkedIn India filed form MGT 6 via SRN F91257345 on 29.01.2024 to prevent any confusion.

The beneficial ownership of one (1) equity share held by LinkedIn Technology Unlimited Company has always vested with LinkedIn Ireland Unlimited Company a fact consistently reflected in the annual filings however it’s noted that the date of creation was erroneously indicated as 11.01.2024 due to submission of the declaration on that date.

IV. On the date of hearing on 12.03.2024, the authorized representatives of the company appeared and they reiterated the written submissions made by them.

5. Analysis of the non-compliance of section 89 of the Act

I. The reply of the company suggests that LINKEDIN IRELAND UNLIMITED COMPANY was always the beneficial owner in respect of the One share held by LINKEDIN TECHNOLOGY UNLIMITED COMPANY [as a registered owner]. Thus, the duty of the beneficial owner and the registered owner to make declarations actually arose after the incorporation of the company in 2009. The registered owner and the beneficial owner ought to have made these filings in accordance with the provisions of section 187C of the Companies Act, 1956 in Form 22B, which was the relevant form for filing such declaration at the time when the beneficial interest actually arose.

II. The company has itself admitted that the date of creation of beneficial interest has been erroneously declared in the Form MGT-4 and Form MGT-5 by the registered owner and the beneficial owner as 11.01.2024.

III. There is no question of withdrawal of the e-form as the company was supposed to file this e-form as per the requirements of law. However, the declarations filed by both the registered owner and the beneficial do not abide by the requirements of sub-section (1) and sub-section (2) of section 89, insofar as the timelines for filing the declarations have not been met and the date of creation of beneficial interest is also erroneous, a position also admitted by the company during the proceedings.

IV. Section 89(5) provides for penalty against the registered holder of shares and beneficial holder of shares if the declarations have not been made as required under sub-section (1) or sub-section (2) of section 89. Clearly by incorrectly disclosing the date of acquiring the beneficial interest, the provisions of as required under sub-section (1) or sub-section (2) have not been met. The date of default is being reckoned subsequent to the period of decriminalization of the provision w.e.f. 21.12.2020 and upto the date of issue of SCN on 15.02.2024.

6. Adjudication proceedings for issues concerning Section 90 of the Act:-

A1. Issue of SCN to the company on 15.02.2024

The queries [in bold] concerning the compliance of section 90 of the Act raised through the SCN dated 15.02.2024 and replies [in italics] received on 28.02.2024 are as follows:

It is seen that Microsoft Corporation, USA (ultimate holding company) is regularly filing statement of changes in beneficial ownership of securities with Security & Exchange Commission (SEC) (weblink : https://www.microsoft.com/en-us/Investor/sec-filings.aspx?year=2023&filing=xbrl. However, the subject company has not filed any eform BEN-2 on MCA 21 portal as required under Section 90 of the Act and rules made thereunder.

Company’s Response:

As far as Section 90 of the Companies Act is concerned, it is our understanding that it applies to cases: (1) when an individual directly or indirectly holds 10% of the shares of a company: (2) when the shares of a company are held by a body corporate, whether there exists an individual who holds majority stake in the member, being a body corporate, or holds majority stake in the ultimate holding company of the member of the company. In our case, there is no individual who is a shareholder of LinkedIn India. Secondly, the ultimate holding company is Microsoft Corporation, USA, a listed body corporate, where it is publicly reported that no individual holds a majority stake.

Accordingly, the adjudication officer has reasonable cause to believe that provision of section 90 and rules made thereunder have not been complied. Now, the company and concerned persons are required to furnish following information with supporting documents for further Adjudication proceedings:

Whether the company has received any declaration pursuant to subsection (1) of Section 90 of the Act. If yes, provide the copy of such declaration along with proof of receipt for the same.

Company’s Response: No, LinkedIn India has not received any declaration pursuant to sub-section (1) of Section 90 of the Companies Act as there are no significant beneficial owner(s), to the knowledge of LinkedIn India.

Whether the company has filed form BEN-2 in terms of sub-section (4) of Section 90 of the Act. If yes, provide the copy of the same. If no, provide reasons with supporting documents.

Company’s Response: No, LinkedIn India has not filed form BEN-2 in terms of subsection (4) of Section 90 of the Companies Act, as no person has filed, declared itself/himself or herself to be a significant beneficial owner.

Provide details of all the actions taken by the company to identify Its Significant Beneficial Owner in terms of section 90 of the Act.

Company’s Response: Even prior to the notification of the Companies (Significant Beneficial Owners) Rules, 2018, LinkedIn India had undertaken an exercise at the time of Microsoft Corporation’s acquisition of LinkedIn Corporation, to identify if there were any individual(s) who individually or along with a trust or any other person held 10% or more of the beneficial interest indirectly in LinkedIn India to which it was found that in Microsoft Corporation, the ultimate holding company, there were no single entity or individual that controlled 10% or more of the shareholding of Microsoft Corporation and thus there were no person who held any significant beneficial ownership. Since 2016, LinkedIn India continuously verifies the beneficial ownership records of Microsoft’s Corporation’s shareholding pattern as available on public records.

Based on public records, LinkedIn India had no reasonable cause to believe that there is any individual who is a significant beneficial owner of LinkedIn India.

Provide details of the individual(s) [name, PAN (if any), DIN (if any), Passport number, Nationality, correspondence address, email address] who exercise(s) control or significant influence on the company in terms of the provisions of section 90 of the Companies Act, 2013 r/w rules made thereunder.

Company’s Response: Based on the reasons stated above, Linkedln India is not aware of any such individual(s). LinkedIn India is managed by a professional board of directors.

Did the company comply with the mandatory compliance of issuing a BEN-4 notice as required in rule 2A(2) of the Companies (Significant Beneficial Owners) Rules, 2018? If no provide reasons thereof.

Company’s Response: Based on our above responses, LinkedIn India under Section 90(4A) and 90(5) did not have any reasons to believe that there are any individuals who hold significant beneficial ownership of LinkedIn India. Therefore, there was no further enquiry made under Form No. BEN-4.

Provide details of all the BEN-4 notices issued by the company, along with a copy thereof. You are also required to provide a copy of the replies received in this regard. For all correspondences, provide a dispatch proof and proof of receipt on the part of the company. Also furnish the information in the following format in respect of each BEN-4 notice issued by the company:

Company’s Response: As stated above, LinkedIn India had no reasonable cause to believe that there are any significant beneficial owners of Linkedln India.

Provide the details of the application moved by the company to the NCLT in terms of section 90(7) of the Act r/w rule 7 of the Companies (Significant Beneficial Owners) Rules, 2018, on the ground that no reply was received on the BEN-4 notice issued by it, or the reply that was received was unsatisfactory. If no such application was moved, provide the reasons thereof.

Company’s Response: No such application was moved by Linkedln India based on our assessment as stated above.

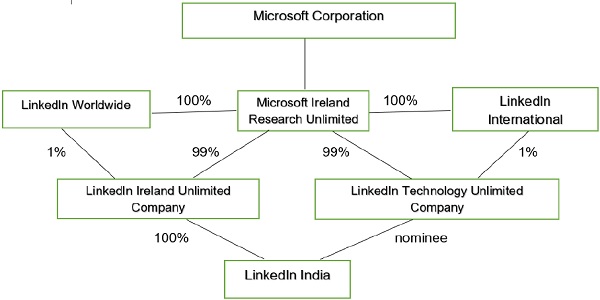

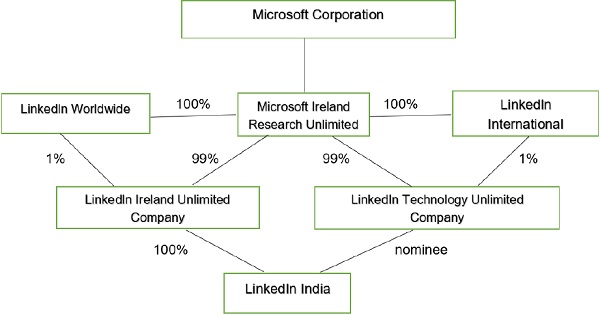

It is seen that Linkedln Ireland Unlimited Company is a member/shareholder of the company holding 100% or shares in the subject company as per Annual Returns filed for the financial year ending on 31.03.2022 and 31.03.2023 and thus falls in the description provided in clause (i) of Explanation III to rule 2(1)(h) of Companies (Significant Beneficial Owners) Rules, 2018. Please provide the details of all the upstream entities [name of the entity, country of registration/incorporation, unique identification number allotted by the respective registry] right up to the ultimate holding company along with the details of shareholdings in respect of each layer of shareholding. Also provide the details of the individual who holds majority stake in the ultimate holding company.

Company’s Response: Please see below the requested details of the upstream entities of LinkedIn India. Ultimately all group entities are wholly owned subsidiaries of Microsoft Corporation.

| Name of entity | Linkedln Ireland Unlimited Company |

| Country of registration | Ireland |

| Date of formation | November 11,2009 |

| Registered office | 70 Sir John Rogerson’s Quay Dublin 2, Ireland |

| Registration number | 477441 |

–

| Name of shareholders | Microsoft Ireland Research Unlimited Company | Linkedln Worldwide |

| Percentage of holding | 99% | 1% |

–

| Name of entity | LinkedIn Technology Unlimited Company | |

| Country of registration | Ireland | |

| Date of formation | November 11,2009 | |

| Registered office | 70 Sir John Rogerson’s Quay Dublin 2, | |

| Registration number address | Ireland 477442 | |

| Name of shareholders | Microsoft Ireland Research Unlimited Company | Linkedln International |

| Percentage of holding | 99% | 1% |

–

| Name of entity | Linkedln Worldwide |

| Country of registration | Isle of Man |

| Date of formation | August 28, 2013 |

| Registered office | 19-21 Circular Road, Douglas, Isle of Man |

| Registration number address | 010097F |

| Name of shareholder | Microsoft Ireland Research Unlimited Company |

| Percentage of holding | 100% |

–

| Name of entity | Linkedln International |

| Country of registration | Isle of Man |

| Date of formation | August 28, 2013 |

| Registered office | 19-21 Circular Road, Douglas, Isle of Man |

| Registration number address | 010098V |

| Name of shareholder | Microsoft Ireland Research Unlimited |

| Percentage of holding | Co100%mp |

–

| Name of entity | Microsoft Ireland Research Unlimited |

| Country of registration | CIreomlanpda |

| Date of formation | April 25, 2001 |

| Registered office | 70 Sir John Rogerson’s Quay Dublin 2, Ireland |

| address Registration number | 342235 |

| Name of shareholder (beneficial holder) | Microsoft Corporation |

Shareholding of Microsoft Ireland Research

It is to be noted that Microsoft Ireland Research Unlimited Company is a

subsidiary of Microsoft Corporation.

Shareholding of Microsoft Corporation

We would like to bring to your attention that there are no individuals who hold in excess of 10% stake in Microsoft Corporation.

The above can also be verified through other various filings made with the Securities Exchange Commission and public sources, which was also undertaken by Linkedln India from time to time, to ensure that there is no significant beneficial owner in Linkedln India.

Microsoft Corporation is run by a professional board and is not controlled by any single individual who has the right to exercise, or actually exercises, significant influence or control, in Microsoft Corporation.

A2. Analysis of company’s reply to the SCN dated 15.02.2024

I. The reply of the company is centered around the argument that there is no individual who holds a majority stake in the ultimate holding company [Microsoft Corporation]. Thus, the company does not have any SBO.

II. This position clearly ignores the other facet whereby a SBO is identified through the test of control or significant influence. Rule 2(1)(h) of the Companies (Significant Beneficial Owners) Rules, 2018 clearly provides for identification of a SBO where the individual has right to exercise, or actually exercises, significant influence or control, in any manner other than through direct holdings alone.

III. On the basis of the reply of the company, the holding structure of the subject company can be understood using the following chart:

IV. Another point to be noted from the reply of the company is that LinkedIn Corporation does not figure anywhere in the layer of upstream entities. It needs to be emphasized that till the acquisition of LinkedIn by Microsoft on 8th December, 2016, LinkedIn Corporation was the ultimate holding company of the subject company. Till date, the subject company continues to report LinkedIn Corporation as its holding company in its financial statements.

V. It is also apparent that despite the mandatory provisions under rule 2A(2) of the Companies (Significant Beneficial Owners) Rules, 2018, the company did not send the notice as per Form BEN-4 to Linkedln Ireland Unlimited Company [member of the subject company which holds its entire share capital], leading to a contravention of section 90(5) for which penalty has been provided under section 450. Also, in general the company and its officers failed to take necessary steps to identify its SBO leading to a violation of section 90(4A) of the Act, for which penalty is provided under section 90(11).

B1. Queries raised vide email dated 04.03.2024 and its reply

The queries [in bold] vide email dated 04.03.2024 and its corresponding reply (received on 12.03.2024 in italics) are as under:

The clause 61 and clause 62 of the Articles of Association of the company provides as under:

61. The Board may, from time to time, appoint such other officers, who may or may not be Directors of the Company, as it thinks fit.

62. The Board of the Company may from time to time authorize such Directors or officers of the Company as it may think appropriate to create binding commitments on behalf of the Company including for execution of all contracts, correspondence and agreements between the Company and any other entity.

You are required to provide the details of the “officers” as referred to clause 61 and 62 along with the powers and duties assigned to them.

Company’s response: The oversight and management of Linkedln India are conducted by its Board of Directors (“Board”). The Board has entrusted various day-to-day administrative and operational duties to different officers, including Mr. Ashutosh Gupta (Executive Director) and Mr. Sagar K S. who are responsible for executing all contracts, correspondence, and agreements. These officers operate under the guidance and supervision of the Board, adhering to its instructions and directives. Given below are the details regarding these officers as requested.

Name: Ashutosh Gupta

Nationality: Indian

E-mail ID: ******@linkedin.com

PAN: ***********

Employment status: Employee of LinkedIn India

Whether nominee of the holding company: Not applicable

Name: Sagar K S

Nationality: Indian

E-mail ID: ***@linkedin.com

PAN: **********

Employment status: Employee of Linkedln India

Whether nominee of the holding company: Not applicable

Whether the Board of Directors of the subject company report to any person. If yes, provide the details of such person

Company’s response: The Board of LinkedIn India operates independently and does not report to any person. The financials of LinkedIn India get consolidated with its ultimate holding company, as and if required under applicable law.

Whether any director of the company is a nominee of the holding company or the ultimate holding company. If yes, provide details in respect of each of such individual and his/her relationship with the nominator entity.

Company’s response: None of the directors of LinkedIn India have been nominated by either the holding company or the ultimate holding company. The Board of LinkedIn India selects directors with expertise in finance and law from among Microsoft employees. These individuals are identified by LinkedIn India’s board and are invited to join. Upon acceptance, they are formally appointed to the Board as per the provisions of the Companies Act, 2013.

Whether there is any agency/committee/any other body of persons other the Board of the company, which exercises powers in respect of execution of the works of the company. If yes, then provide the name of such agency/committee/any other body of persons, its role and functions, and provide the details of all persons comprising of such agency/committee/any other body of persons.

Company’s response: Apart from the Board of LinkedIn India, no other agency, committee, or group of individuals holds authority over the execution of LinkedIn India’s operations. As mentioned in our response to point (b), various officers are authorized by the Board of LinkedIn India to fulfill specific duties and responsibilities, and they act in accordance with the instructions, directions and under the supervision of the Board.

On the website of LinkedIn https://about.linkedin.com/?trk=homepage the following information has been provided:

Who are we?

LinkedIn began in co-founder Reid Hoffman’s living room in 2002 and was officially launched on May 5, 2003. Today, LinkedIn leads a diversified business with revenues from membership subscriptions, advertising sales and recruitment solutions under the leadership of Ryan Roslansky. In December 2016, Microsoft completed its acquisition of LinkedIn, bringing together the world’s leading professional cloud and the world’s leading professional network.

Therefore, you are required to specifically state as to whether Mr. Ryan Roslansky holds “control” or “significant influence” in the subject company. You may note that an individual may exercise “control” or “significant influence” in a company without holding any shares in it.

Company’s response: Please note that Mr. Ryan Roslansky serves as the CEO of the LinkedIn division within Microsoft. However, Mr. Ryan Roslansky does not participate in the day-to-day decision-making processes of LinkedIn India, which operates under the oversight and direction of its own Board. Mr. Ryan Roslansky does not independently or individually exert any control or significant influence over the operations of LinkedIn India. He is neither on the board of Linkedln India or attends or gives directions relating to day-to-day operations of LinkedIn India.

B2. Analysis of company’s response

I. The company gave the names of only two individuals who were specifically authorized under Clause 61 and 62 of the Articles of the company. Later on perusal of the records of the company it was seen that there were other officers who were specifically authorized by the Board but the details of those officers were not shared with this office.

II. The company denied that it has appointed any nominee directors to represent the holding company or its ultimate holding company. It rather stated that all appointments were done from amongst the Microsoft employees by the Board of the subject company. This aspect will be dealt in greater detail in the later part of the order, where it is seen that the submission of the subject company that it “selects” the employees of Microsoft for appointment on its Board is not accurate.

III. As regards Mr. Ryan Roslansky, the reply of the company was limited to the aspect of him not taking part in the day-to-day operations of the subject company, and that he did not independently and individually exert control or significant influence. The reply was certainly not satisfactory as the law does not provide that an SBO must necessarily take part in the day-to-day operations of a company or have direct control over the affairs of a company. It is clear that control, or the right to exercise such control or significant influence indirectly also tantamount to exercise of control and significant influence.

C1. Queries raised during the hearing on 12.03.2024 and its reply

In view of submissions made by the authorized representatives of the company during the hearing held on 12.03.2024, the following additional queries [in bold] were raised vide email dated 12.03.2024, against which the reply [in italics] was received on 19.3.2024, which is as under:

It is stated that Mr. Sagar K S, who does not hold any board level position in company is authorized to execute contract, etc. on behalf of the company. In this regard you are required to provide sample copies of such contracts/agreements/correspondences. Also provide a copy of the terms and conditions separately executed between the company and Mr. Sagar K S which empowers him to act on behalf of the company.

Company’s Response: Please refer to the below authorizations granted by the Board of LinkedIn India in favour of Mr. Sagar which empowers him to act for and on behalf of LinkedIn India.

(a) Circular resolution dated February 16, 2021: As per item no.2 and no.3, Mr. Sagar was granted authorization to execute, for and on behalf of LinkedIn India, all relevant documents in relation to (i) commercial agreements or arrangements involving LinkedIn India; (ii) Software Technology Park of India license; (iii) Service exports from India scheme; (iv) Other service provider license; (v) meeting the corporate social responsibility obligations on behalf of LinkedIn India; (vi) GWS – related documents; and (vii) any other statutory compliance document including, but not limited to, any LEIN renewal.

(b) Board meeting dated January 13, 2022: As per item no.10, Mr. Sagar was granted authorization to renew the legal entity identifier registration on behalf of LinkedIn India.

(c) Board meeting dated March 13, 2023: Mr. Sagar was granted authorization for the execution and registration of a lease deed for and on behalf of LinkedIn India.

***Certain contracts executed by Mr. Sagar were provided in the Annexure to the reply***

It is seen from your reply that the Board of LinkedIn India has selected directors with expertise in various disciplines especially in finance and law from among the Microsoft employees and you have stated that Microsoft employees are not nominees of Microsoft. So you are required to clarify as to whether Microsoft is unaware that their employees have taken Board level position in LinkedIn India and whether Microsoft can exercise its power and ask its employee to not join the board of LinkedIn India. You are required to once again explain as to why the employees of Microsoft appointed as directors in LinkedIn India will not be considered as nominee directors of Microsoft, as the financial statements clearly disclose that Microsoft Corporation is having control over the subject company with effect from December 8, 2016.

Company’s Response: Microsoft is aware that its employees are appointed on the board of LinkedIn India. The board invites selected Microsoft employees with specific financial or legal expertise to be appointed to the board. As per the internal policies of Microsoft, Microsoft employees are permitted to act as directors of a Microsoft group entity. We would like to submit that a mere right to reject the ability of an entity to its employee from becoming a director in another entity (whether related or not), would not make such person the nominee of such entity.

Microsoft exercises control over LinkedIn India as the ultimate holding company by virtue of shareholding of its subsidiaries, details of which has been provided in the earlier response.

With regard to issue as to whether Mr. Ryan Roslansky holds control or significant influence in the company, you have denied the same by stating that he does not participate in day-to-day decision making process of LinkedIn India. However, it is noted that Mr. Roslansky had come to India in November 2022 and visited your office in Bangalore where he met employees and customers. Several news articles and videos with regard his visit in India are available on the public domain which shows that Mr. Roslansky had shared his macro level plans about the Indian operations. He had spoken on length on the issue as to whether LinkedIn India is considering layoffs in India or not. He had also highlighted the importance of India company wherein he stated that close to 700 employees in India are working on R&D which is critical to LinkedIn globally. You are required to clearly state as to whether these 700 employees are on the payroll of the LinkedIn India or they are on the role of LinkedIn corporation.

Few articles and videos as available in the public domain are given below which you may rely upon while giving the reply.

I. https://www.youtube.com/watch?v=n_gCqnwXPOY

II. https://www.youtube.com/watch?v=2ilQyzATEWc

III. https://timesofindia.indiatimes.com/business/india-business/indians-networking-more-than-most-linkedin-ceo/articleshow/95497158.cms

Company’s Response: We wish to clarify that Mr. Roslansky visited the offices of LinkedIn India in his capacity as the newly appointed global CEO of LinkedIn Corporation. During his visit, aside from conducting meet-and-greet sessions with employees and meetings with customers who are subscribers on the LinkedIn platform (not specific to LinkedIn India), Mr. Roslansky did not engage in any meetings where he provided instructions or directions related to LinkedIn India, as he lacks the authorization from the board to issue such directives. Based on feedback from LinkedIn India personnel, he did express optimistic views about India publicly, including plans for expanding the R&D team in India. It’s important to note that such expansions are contingent upon contracts executed with other Microsoft entities, as reflected in the financial statements below, and are subject to relevant approvals within LinkedIn India, which operates under the supervision of the board of directors of LinkedIn India.

His statements regarding the expansion of the R&D team do not in any manner imply control over policy or day-to-day management decisions specific to LinkedIn India, which are the purview of the board of directors of LinkedIn India. Upon thorough review of Mr. Roslansky’s interviews and press clippings, it’s apparent that his remarks were made referring to LinkedIn as a group and not specifically to LinkedIn India. He referred to India as a revenue center and market for LinkedIn on a global scale, rather than specifically addressing LinkedIn India, as LinkedIn India does not manage the platform. When Mr. Roslansky referred to the ‘Company’ in his interviews, he was alluding to LinkedIn as a group, not singling out LinkedIn India. This can be ascertained when he uses LinkedIn and the Company interchangeably while discussing closure of fiscal year, revenue, subscriber base, and other metrics, which are not attributable to LinkedIn India.

Further, we would like to clarify that Mr. Roslansky had spoken about the layoffs at global level in LinkedIn and not specific to LinkedIn India. In relation to the R&D employees in India, we would like to clarify that 700 was an approximate number which changes from time to time depending on new hires and/or exits in the company.

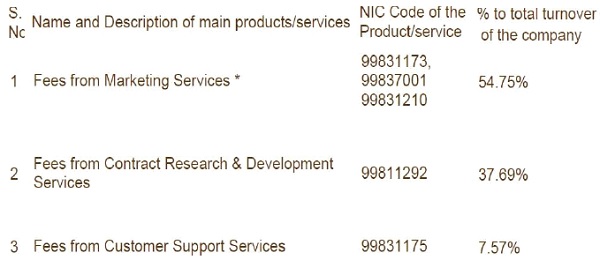

On perusal of the financial statement of the subject company for FY 2021-22, it is seen that the company has given following disclosures with respect to its revenue from operations:

These disclosures show that the company is earning sizeable amount of revenue from the R&D operations. So, it may be clarified as to whether the R&D operations in India are not influenced by any factors existing outside India. Also, whether Mr. Roslansky has no role in any critical decision-making with regard to the operations of the subject company.

Company’s Response: The marketing and R&D operations of LinkedIn India are carried out in accordance with contracts executed by LinkedIn India with various entities of the Microsoft group, including LinkedIn entities, under longterm agreements with such affiliates or related parties. These R&D contracts have been duly approved by the board of directors of LinkedIn India.

In light of the above authorization, we wish to confirm that aside from the counterparties and their advisors (both in tax and legal matters), no other parties were involved in the execution and fulfillment of these transactions. It’s pertinent to note that some of these revenue generating contracts pre-date Mr. Roslansky’s appointment as the CEO of LinkedIn Corporation, thereby excluding his direct or indirect involvement or influence in decision making relating to these contracts.

As previously stated, Mr. Roslansky serves as the global CEO of the LinkedIn Group. The business operations of LinkedIn India operate under the decentralized supervision of the LinkedIn India board. While LinkedIn India operates within the overarching policies of the group, these policies are implemented under the oversight of the Board.

It’s important to clarify that Mr. Roslansky does not make specific day-to-day management or policy decisions pertaining to the business operations of LinkedIn India. Therefore, he does not exercise direct control or significant influence over LinkedIn India’s operations.

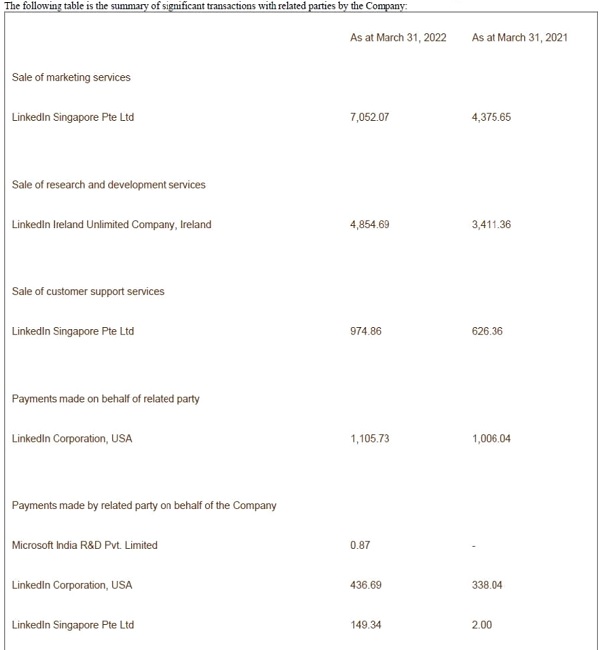

The following disclosures made by the subject company under the related party transactions may be noted:

It is seen that the subject company has made transactions on behalf of the related parties and similarly the related parties have made transactions on behalf of the subject company. You are required to state as to whether these transactions did not involve actors outside the Board of the subject company, if so then please indicate their role alongwith supporting documents.

Company’s Response: As previously communicated, LinkedIn India collaborates with various entities within the Microsoft group, including LinkedIn entities, under long-term contracts that have been duly executed with affiliated or related parties. These contracts have received approval from the board of directors of LinkedIn India.

In accordance with the authorization provided, we wish to confirm that aside from the counterparties and their advisors (both in tax and legal matters), no other parties were involved in the execution and fulfillment of these transactions.

C2. Analysis of company’s response

I. A copy of the agreement provided by the company [signed by Sagar K.S.] shows that it is an agreement entered into by the subject company with a supplier provide event management, project management, and booth set-up services for an event for the LinkedIn Legal and Public Policy and Economic Graph team. Interestingly, there is a clause in the agreement which states as under:

The same clause was visible in other agreements referred to as Statement of Work between the subject company and the third parties. It has already been noted above that LinkedIn Corporation, USA does not figure in the layers of upstream entities of the subject company in terms of shareholding, yet it has been consistently shown as a holding company. This issue will be dealt at length in the later part of the order.

II. The reply of the company with regard to the issue of nominee directors remained unclear, it completely failed to establish that the employees of Microsoft working in the subject company as directors would remain independent. This issue will be dealt at length in the later part of the order.

III. Earlier the company had replied that Mr. Ryan Roslansky serves as the CEO of the LinkedIn division within Microsoft. Now in its reply, the company submitted that he is the “global CEO” of LinkedIn Corporation and at other place he is referred as the “global CEO” of the “LinkedIn Group”. The designation itself indicates the sphere of influence of Mr. Roslanksy. The company also admitted that the Mr. Roslansky referred to the whole group in his statements and not just the subject company, which indicates of his role as a “global CEO”.

IV. The subject company also denied the presence of external influence in entering into contracts, as well as the fact that it was making and receiving payments for/from related parties. The presence of influence would be analyzed in the later part of the order and from the attending circumstances and other information on record.

D1. Queries raised e-mails dated March 20, 2024 and March 21, 2024 followed by the oral hearing on April 01, 2024 and its reply

The issues raised in the queries [in bold] and the reply of the company [in italics] are as follows:

You have admitted that Microsoft has a right to reject the ability of an entity to appoint its employee as a Director in such entity. It is apparent that such right can only be exercised by Microsoft over the person whom it controls. You are also required to refer to the explanation to Section 149(7) of the Companies Act, 2013 which clearly states that the Nominee Director can be appointed by any other person to represent its interest. It is clear that while exercising its right to reject, Microsoft would normally take into account its interest which are supposed to be safeguarded by its employee while being appointed in LinkedIn.

Company’s Response: LinkedIn India does not have insight on the considerations that Microsoft takes into account while deciding whether to reject an employee from serving as a director to an entity, or on the request of an employee to become a director either in a group entity or entities outside the group. We reiterate that a decision to not reject an employee from serving on a board does not mean that Microsoft nominated the employee.

For example, if an executive director of a listed company becomes a non-executive director or independent director of another company which is not affiliated with the said listed company, with the permission of its board where such person is a managing or executive director, then such person does not become the nominee of the company in which he/she is a managing director solely based on the ability of the listed company to grant its approval to the director to become a director in the non-affiliated entity.

You have admitted that Mr. Roslansky had referred to LinkedIn as a Group during his interviews and press clippings. This is precisely the issue raised by this office in its email dated 04.03.2024 wherein the following extract of the website of LinkedIn was reproduced:-

Who are we?

LinkedIn began in co-founder Reid Hoffman’s living room in 2002 and was officially launched on May 5, 2003.

Today, LinkedIn leads a diversified business with revenues from membership subscriptions, advertising sales and recruitment solutions under the leadership of Ryan Roslansky. In December 2016, Microsoft completed its acquisition of LinkedIn, bringing together the world’s leading professional cloud and the world’s leading professional network.

This shows the overall leadership role of Mr. Ryan Roslansky in the LinkedIn Group of which LinkedIn is a part.

Company’s Response: Mr. Ryan Roslansky is the CEO of LinkedIn Corporation, with LinkedIn India as one of its indirect subsidiaries. Being the CEO of LinkedIn Corporation, which in turn is owned and controlled by Microsoft Corporation, Mr. Roslansky serves as an employee of LinkedIn Corporation pursuant to an employment agreement with the said entity and reports to the board of LinkedIn Corporation. His role draws its authority and is subject to supervision of the board of LinkedIn Corporation and its controlling shareholder i.e. Microsoft Corporation. He does not, in any form or manner, exercise any independent or individual control or influence which is outside the supervision of the board of directors of LinkedIn Corporation and Microsoft Corporation.

Your reply also appears to be misleading as you have stated that Mr. Roslansky does not, in any manner, controls the day-to-day management decisions of LinkedIn. You may note that this issue has never been raised by this office. In fact, the previous mail has also highlighted his control in terms on a macro level, a fact which you have admitted by stating that when Mr. Roslansky speaks, he speaks on behalf of the whole group of which LinkedIn India is a part.

Company’s Response: We apologize for any misunderstanding. We believe that a contention was raised that Mr. Roslansky exercises ‘significant influence or control’ on LinkedIn India in his capacity as the CEO of LinkedIn Corporation. Please note that, in the absence of cogent evidence suggesting otherwise, we had abided by the guidance given by the Supreme Court of India, in the case of Vodafone International Holdings B.V. v. Union of India, where the court provided that, “Legal relationship between a holding company and WOS is that they are two distinct legal persons and the holding company does not own the assets of the subsidiary and, in law, the management of the business of the subsidiary also vests in its Board of Directors […] Holding company and subsidiary company are, however, considered as separate legal entities, and subsidiary are allowed decentralized management. Each subsidiary can reform its own management personnel and holding company may also provide expert, efficient and competent services for the benefit of the subsidiaries.” The Court explicitly disregarded the mere presence of ownership, parental control, management etc. of a subsidiary as factors relevant for determining whether corporate veil should be pierced. Reference may also be drawn towards a judgement of the High Court of Delhi where the Court gave support to the contention that, “it is not open to the holding company to dictate to the board of directors. The board of directors of a company must do all acts in the interest of the company, and its shareholders [….]”, holding that, “The directors of any company cannot and should not act as if they are puppets on a string, acting out a charade on the jerks and pulls of an invisible master puppeteer (the holding company) behind the curtain, behind a corporate veil.”

Mr. Roslansky is an employee of LinkedIn Corporation and with such position, at best, may act on such matters as may be authorized by the board of LinkedIn Corporation on matters requested by the board of LinkedIn India. The law relating to Significant Beneficial Owner(s), as captured under Section 90 of the Companies Act, 2013, does not stretch the concept of “control” and/or significant influence to include expert and competent services provided by one entity to another entity belonging to the same corporate group through an employee.

Further, exercise of significant influence/control or the right to exercise influence/control must necessarily flow from a source, typically either a statute or an agreement. Hence, Form Ben 2, to be filed to disclose the details and identity of a Significant Beneficial Owner under the Companies Act, 2013, provides for the attachment of agreement(s), instruments reflecting, inter alia, the presence of control or significant influence of the relevant party on the reporting company.

Reference may also be drawn to the statutory schemes in other countries. For example, the United Kingdom where the Statutory Guidance for determining “significant influence or control” as used under the (UK) Companies Act 2006 provides that: (a) the right to exercise significant influence or control is a right which, if exercised, would give rise to the actual exercise of significant influence or control; and (b) in the context of a company, a person may hold a right to exercise significant influence or control as a result of a variety of circumstances including the provisions of a company’s constitution, the rights attached to the shares or securities which a person holds, a shareholders’ agreement, some other agreement or otherwise. The said guidance then goes on to explicitly include, “person is an employee acting in the course of their employment and nominee for their employer, including an employee, director or CEO of a third party (such as a corporate director company), which has significant influence or control over the company [….]” in the category of roles and relationships which would not, on their own, result in that person being considered to be exercising significant influence or control in the relevant company.

It may be noted that a similar interpretation has been taken under the Corporate Transparency Act of the United States.

Further, please note that LinkedIn Group has consistently maintained that the ultimate beneficial ownership over the entities in the group vests solely with Microsoft Corporation. In this regard, please copy of the filing in respect of beneficial ownership made by LinkedIn Belgium before the Treasury-Federal Public Service Finance.

Please note that: (a) there is no agreement, instrument, or document of any kind between Mr. Roslansky and LinkedIn India that extends any right, power, or authority to Mr. Roslansky over the policies, procedures and/or practices of LinkedIn India, its operations or finance; (b) Mr. Roslansky is not and has never been a director of LinkedIn India and has never attended any of its meeting of the board; (c) Mr. Roslansky does not and has not held any shares in LinkedIn India; and (d) there are no corporate resolutions, charter documents or versions thereof which today or in the past authorized Mr. Roslansky to significantly influence and/or control the finance or operations of LinkedIn India. Thus, there exists no authority in Mr. Roslansky to either control and/or significantly influence the financial or operating policy decisions of LinkedIn India, which always vests and has vested with the board of directors of LinkedIn India.

Further, please note the text of Section 90 of the Companies Act, 2013 read with the relevant rules uses the term chief executive officer only in the limited context of a pooled investment vehicle and not of body corporates, which could have been added by the legislature. Even in this singular instance, such ‘chief executive officer’ has to be linked to a member of the reporting company and not the reporting company per se. Please note that Mr. Roslansky is not the chief executive officer of either of the two members of LinkedIn India. Mr. Roslansky is not authorized to participate in the financial or operational policy decisions of LinkedIn India.

Lastly, even the limited functions undertaken by Mr. Roslansky are subject to the review and oversight of the board of directors of LinkedIn Corporation and Microsoft Corporation.

While referring to the R&D contracts you have stated that these contracts have been duly approved by the Board of Directors. It is stated that these compliances have never been questioned by this office. However, it is important to note that during the hearing, this office was given to understand that the Indian entity is merely a back office whereas on perusal of the financial statements and the interviews given by Mr. Roslansky, it is seen that close to 700 employees have been employed in India in R&D operations, which would be critical to any tech company. You were specifically asked to point out as to whether Mr. Roslansky has any role in view of the R&D operations being done by the Indian entities on which you have simply stated that the contracts are executed by counter parties and their advisories. It is noted that execution of contract was not something that was referred to in this questionnaire and considering that transactions would have also taken place between LinkedIn Corporation US and LinkedIn India, where Mr. Roslansky is, in any case, one of the counter parties. As regards the issue that some of the contracts predate Mr. Roslansky’s appointment, it was never stated by this office that Mr. Roslansky would be able to exercise any control or significant influence directly or indirectly prior to his appointment. You have also clearly specified regarding “direct control or significant influence,” while clearly missing out that the provisions of Section 90 covers even the “right to exercise” which may not be direct.

Company’s Response:

LinkedIn India has about 477 employees who are working in the R&D division. Various operating entities of LinkedIn and Microsoft enter into R&D contracts with various entities including LinkedIn India for provision of R&D services (as evidenced in the financials of LinkedIn India). As submitted earlier, depending on the requirements of LinkedIn or Microsoft team, the relevant function heads reach out to the relevant R&D teams in India (there are several verticals with the R&D division with its own team leader and reporting structures) for the relevant research and development programmes. LinkedIn India charges such entities (which are customers of LinkedIn India as against entities controlling the R&D teams) on an arm’s length basis. Mr. Roslansky does not exercise any rights relating to the R&D division of LinkedIn India. He may as the CEO interact with his team in US for development of features or products who in turn outsource the work to LinkedIn India for development of such features or products as part of R&D activities while paying for such services, as evidenced in the financial statements of LinkedIn India.

Please note that there is no direct or indirect control and/or significant influence exercised by Mr. Roslansky in the financial and operating policy decisions or operations of LinkedIn India including the R&D activities of LinkedIn India. As customary in tech companies, R&D activities involving IT operations are part of the back-office operations of LinkedIn Group as a multinational organization. Thus, Mr. Roslansky directly or indirectly is not a counter party to the R&D services agreement and neither does he review or control the R&D operations of LinkedIn India.

Additionally, we are of the view that the ‘right to exercise’ has to be based on an authority of law or contract. In the present case, any right in favor of Mr. Roslanky over its affairs must be explicitly granted by the Company pursuant to an employment agreement with the company or authorization by the board. Merely being the CEO of LinkedIn Corporation does not grant Mr. Roslansky the ‘right to exercise’ control’ or ‘significant influence’ over LinkedIn India as authorization with respect to operations of LinkedIn India has to be approved by its board or shareholders, in accordance with the Companies Act, 2013. This is evident from the authority that was granted to the International Finance Director to execute employment agreement. Thus, the right to exercise has to stem either by authorization or as per law.

We would also like to refer to Paragraph 7.1 of Report of the Company Law Committee, 2016 on the objective of identifying the beneficial owner, which states that it is important to identify the beneficial owner due to misuse of corporate vehicles for the purpose of evading tax or laundering money for corrupt or illegal purposes, including for terrorist activities has been a concern worldwide. Complex structures and chains of corporate vehicles are used to hide the real owner behind the transactions made using these structures. Realizing this, jurisdictions world over have been putting in place mechanisms to identify the natural person controlling a corporate entity.

By simply assuming that the CEO who is merely an employee of the body corporate is a significant beneficial owner would result in a dangerous precedent where promoters of body corporates would simply appoint a titular CEO and provide a declaration and thus successfully defeating the objective of identifying the significant beneficial owner, who as per us should be a natural person who has the authority to individually and independently take decisions beyond and over the supervision of the board or shareholders (if such person is not holding any shares).

Further, as stated in our previous replies and based on filings with the SEC, there are no such persons at the ultimate holding company level i.e. Microsoft Corporation.

We would humbly like to submit that Microsoft Corporation and its subsidiary LinkedIn Corporation are professionally run companies without any significant beneficial owners, which is a departure from the common corporate structures in India which are promoter led. However, there are a number of banking companies and IT companies in India (listed and otherwise) which are professionally run without any promoter or significant beneficial owner.

It is seen that payments were clearly been made by LinkedIn India on behalf of LinkedIn Corporation US and vice versa and the transactions included other entities in the group. It is questionable that such transactions, on behalf of other companies, can be carried out by the directors of the Indian company alone without any apparent or latent external control or significant influence.

Company’s Response: We would like to clarify that all payments by LinkedIn India to the LinkedIn and Microsoft group entities are pursuant to valid agreements on arm’s length basis and in accordance with the existing industry standards and practices.

On perusal of Annexure 2 of your reply it is seen that the board meeting of the company held on 17.06.2011 in Mountain View, California, US had persons other than Board of Directors who were present. In the same meeting, it was decided that the authority to sign contracts of employment on behalf of the company was delegated to the International Finance Director (the “finance director”) of LinkedIn Ireland Limited. In this regard you are required to provide all such instances where people other than directors have attended your board meetings from time to time and also specify in which capacity they have attended such meetings, including the meeting held on 17.06.2011.

Company’s Response: The company would like to confirm that since incorporation on December 31, 2009, up to September 17, 2012, the board of LinkedIn India had invited members of the global finance and legal team to attend the board meetings solely to observe the board meeting process of LinkedIn India and have an understanding of applicability of laws relating to such proceedings.

Since September 17, 2012, no persons other than the directors have attended the board meetings of LinkedIn India. The minutes prior to September 17, 2012, notes Ms. Lora Blum (Vice President, Legal-Corporate & Assistant Secretary), Mr. Kent Buller (Chief Accounting Officer) and Ms. Lisa Laymon (Para legal and Senior Executive Administrator) as special invitees to the board meeting.

We would like to reiterate that Mr. Roslansky has never attended any board meeting of LinkedIn India and neither has any board member sought his consent relating to any of the agenda items approved by the board of LinkedIn India.

You are required to provide whether there is review of R&D operations besides the financial operations by the parent company of LinkedIn India including by an officer of the parent company. Thus, now you are required to provide all the correspondences, minutes exchanged with regard to the review of the R&D operations and financial operations of LinkedIn India by its parent companies.

Company’s Response: As stated above, no person reviews the R&D operations of LinkedIn India which are not consistent with the contracts executed by it with the counterparties which are availing the R&D services.

D2. Analysis of company’s response

I. Clearly, the company was not able to defend its stance that the employees of Microsoft appointed as directors in the subject company would not represent the interests of Microsoft. The example given by the company regarding the appointment of an executive director of a listed company as a non-executive director or independent director of another company which is not affiliated with the said listed company, is clearly not relevant in the present context as the companies in question here are connected to each other.

II. Here for the first time, the company reported that Mr. Roslansky has entered into an employment agreement with LinkedIn Corporation and his role is subject to supervision of the board of the LinkedIn Corporation and its controlling shareholder i.e. Microsoft Corporation. Later when the company was asked to produce the copy of the employment agreement, the same was denied on the ground that the subject company lacked access to it and thereafter on the ground that it is confidential. This aspect will be covered in the later part of the order.

III. The judgement of the Hon’ble Supreme Court in the Vodafone case cited by the company is in a different context. As far as the Companies Act, 2013 is concerned, it expressly recognizes the concepts of nominee directors and subsidiary companies whose Boards are in control of a holding company.

IV. The reply of the subject company concedes that as an employee of the LinkedIn Corporation he may be authorized by the Board of LinkedIn Corporation to act on matters which are requested by the Board of the subject company. This is the only reference of direct interaction of Mr. Roslansky in the affairs of the subject company. However, the company felt that this would not amount to control or significant influence.

V. The company has relied on the Statutory Guidance for determining “significant influence or control” under the UK Companies Act, 2006 to state that a person who is an employee acting in the course of their employment and nominee for their employer, including an employee, director or CEO of a third party (such as a corporate director company) is not on its own regarded as a person exercising significant influence or control. They have also submitted that the position is same under the Corporate Transparency Act of the United States.

VI. As far as the UK’s law is concerned the position of not treating an employee as a SBO is not absolute as already stated by the company. However, as regards the position in US1, the individual who is an important decision-maker, or an individual who has any other form of substantial control over the reporting company is to be reckoned for reporting as the beneficial owner of the reporting company. However, in US certain classes of companies are exempt from the reporting requirements.

VII. The company has also argued that there is no written agreement to signify that there is any link between Mr. Roslansky and the subject company and further argued that the rules provide for reporting of a CEO in case of a Pooled Investment Vehicle and not in other cases. This argument is not true as the rules provide for different tests to identify the SBO, such as the test to identify it through indirect holdings via member of a reporting company, wherein the CEO in relation to a Pooled Investment Vehicle is to be identified, the other test is identify an individual on the basis of right to exercise or actual exercise of control or significant influence other than through direct holdings alone. Both these tests are independent of each other. Though it is possible for an overlap in certain cases.

VIII. As far as the existence of a written agreement is concerned, there is no such requirement in law that a written agreement must pre-exist. The attending circumstances backed with corroborating material would be suffice to show the existence of control or significant influence. In any case, it is sufficient to show that there exists the “right to exercise control or significant influence”.

IX. The company has argued that the ‘right to exercise’ in the context of control or significant influence has to be based on an authority of law or contract and also if a CEO is regarded as a SBO then the companies would be tempted to appoint titular CEOs to find a get around.

X. The reply of the company is not justified as there is no prior requirement in the law that the significant influence and control can only be exercised through a written contract or under a law. Further, the apprehension regarding appointment of titular CEOs is also unfounded as the choice of appointing a global CEO is not driven by the reporting requirements under the Indian law.

XI. The company conceded to the participation of external members in the Board meetings of the company for a period of close to 3 years after the incorporation of the company in 2009 and also the fact that such individuals had the authority to take decisions on behalf of the company. It is noted that Ms. Lora Blum (Vice President, Legal Corporate & Assistant Secretary) had attended Board meetings during this period as an invitee and later went on to become a director of the subject company in 2014 for a period close to three years.

E1. Queries raised e-mail dated April 16, 2024 and its reply

The issues raised in the queries [in bold] and the reply of the company [italics] are as follows:

You have stated that LinkedIn India does not have insight about the considerations that are taken into account by Microsoft while deciding whether to reject an employee from serving as a director to an entity. On further examination, it is seen that the directors appointed in LinkedIn India are holding significant positions in LinkedIn Corporation as well as in Microsoft Corporation. The table below may be seen:

| Directors in Indian Company | Position in LinkedIn Corporation as per the Annual Report | Position in Microsoft Corporation as per the Annual Report |

| KEITH RANGER DOLLIVER | VICE PRESIDENT AND DIRECTOR | ASSISTANT SECRETARY |

| BENJAMIN OWEN ORNDORFF | VICE PRESIDENT AND DIRECTOR | ASSISTANT SECRETARY |

| HENRY CHINING FONG | ASSISTANT SECRETARY |

|

| MARK LEGASPI | ASSISTANT SECRETARY |

It is seen that while filing the e-form, these have been shown as Non-Promoter Director instead as “Promoter Director”. Further, non-reporting of these directors in India as nominees of the promoters is a significant lapse. These directors are exercising statutory roles under the laws/bylaws regulating LinkedIn Corporation and Microsoft Corporation. In addition, it appears that that LinkedIn India is unaware of the fact that two of its directors are also directors of LinkedIn Corporation. You are required to provide copies of MBP-1 submitted by these directors.

Company’s Response: We had clarified in our previous response the manner in which directors were appointed. They have been invited by LinkedIn India board. As per Section 2(69) of the Companies Act, 2013, a “promoter” means a person: (a) who has been named as such in a prospectus or is identified by the company in the annual return referred to in section 92; or (b) who has control over the affairs of the company, directly or indirectly whether as a shareholder, director or otherwise; or (c) in accordance with whose advice, directions or instructions the board of directors of the company is accustomed to act. Further, it is to be noted in the proviso of Section 2(69), that nothing in clause (c) shall apply to a person who is acting merely in a professional capacity.

The above also supports our argument relating to professional CEOs such as Mr. Satya Nadella and Mr. Ryan, who don’t have shareholding or board control, not to be deemed as ‘significant beneficial owner’ as they are merely discharging their professional role under the supervision of the board of the companies where they merely are employees.

Based on the above provisions, we believe that no director fulfils any of the criteria to be termed as a “promoter” of LinkedIn India and to be accordingly designated as a “promoter director”.

Regarding the director(s) being designated as a nominee director, we would like to reiterate, that a mere right to reject the ability of an entity to its employee from becoming a director in another entity (whether related or not), would not make such person the nominee of such entity. Microsoft exercises control over LinkedIn India as the ultimate holding company by virtue of shareholding of its subsidiaries, details of which has been provided in our previous responses.

The Board of Directors (“Board”) of LinkedIn India thereafter invites individuals from within LinkedIn and Microsoft group of companies, with such specific financial or legal expertise to be appointed to the Board. As such, historically these directors have been shown as professional directors in the filings at the time of appointment.

Please see attached as Annexure-1, copies of Form MBP-1 submitted by the directors (as mentioned in the query above) disclosing their interests as of March 31, 2014.

While pursuing the filings of the company on MCA21 portal, it is seen that the company has filed minutes of 10th and 12th AGM wherein the AGM was not attended by any of the director.

Further, in the 12th AGM, Mr Henry Fong and Mr Mark Legaspi were appointed as Director (who are office holder in LinkedIn Corporation) wherein none of the then existing director were present. Thus, it seems that the agenda of the meeting is set up persons other than director.

Company’s Response: Regarding the 12th annual general meeting (“AGM”) held on September 21, 2022, wherein Mr. Henry Fong and Mr. Mark Legaspi were appointed as Director(s), please note that while none of the directors attended the meeting, the agenda for the AGM was determined by the Board of LinkedIn India. In accordance with the Secretarial Standards-2 and the guidance note on Secretarial Standards-2 issued by the Institute of Company Secretaries of India, the absence of the directors and the reason thereof are noted by the chairperson as recorded in the minutes. Since the board meeting was conducted in India and the abovementioned directors were outside India, their respective leaves of absence were noted.

We would like to reiterate that the agenda was framed by the board of directors.

In your reply, you have stated that Mr. Roslansky serves as an employee of LinkedIn Corporation pursuant to an employment agreement. Please provide a copy of the employment agreement entered into between LINKEDIN CORPORATION and Mr. RYAN ROSLANSKY.

It is also noted that Mr. RYAN ROSLANSKY is shown as a President and CEO in the annual report of LINKEDIN CORPORATION. Mr. RYAN ROSLANSKY is also reported separately as CEO, LinkedIn in the annual report of Microsoft Corporation.

Company’s Response: Please note that LinkedIn India does not exercise any control or influence over LinkedIn Corporation, Mr. Ryan Roslansky and/or any access to documents, instruments, or deeds privy to such person(s) as LinkedIn India lacks legal authority to seek such confidential documents. In the absence of any authority or right vested in us to procure such document(s), we respectfully submit that will not be able to obtain the same and share it with your kind office.

Further, while Mr. Roslansky’s position and designation(s) in LinkedIn Corporation are a matter of public record, as conveyed by us in our reply dated April 9, 2024, Mr. Roslansky does not, either in his individual capacity or as a representative of LinkedIn Corporation acts as or can be termed as a significant beneficial owner of LinkedIn India.

Please refer to the note dated 20th July, 2020 shared by Mr. RYAN ROSLANSKY to all employees of the LinkedIn Group [https://news.linkedin.com/2020/july/a-message] wherein he has announced global layoffs which also covers the Asia Pacific region. The message of the CEO also lists out various steps which would be taken for employees of the LinkedIn Group who would be laid off. You may note that § 122(15) of the General Corporation Law of Delaware provides the following: powers to the Corporations:

Pay pensions and establish and carry out pension, profit sharing, stock option, stock purchase, stock bonus, retirement, benefit, incentive and compensation plans, trusts and provisions for any or all of its directors, officers and employees, and for any or all of the directors, officers and employees of its subsidiaries.

Clearly this provision also gives the “right to exercise” control to LINKEDIN CORPORATION over the management/policy decisions of the subject company. Please specify which individual exercises such control.

Company’s Response: Please note that we have already conveyed that Mr. Ryan Roslansky does not in any individual or independent form or manner participate in the operational or financial policy of LinkedIn India. Further, please note that since LinkedIn India is a private limited company incorporated in India, we cannot assume or relay any information, opinion, position, action, or omission, relating to law(s) of a foreign nation or the execution and/or implication of such law(s) on a foreign-incorporated entity. Similarly, we cannot assume expertise or authority to refer to or rely upon or interpret such legislations directly in legal proceedings emanating in India, relating to an Indian entity, from the (Indian) Companies Act, 2013. It is to be noted that the above referred provision is with respect to LinkedIn Corporation and does not empower individuals. We assume that LinkedIn Corporation, like any other body corporate, operates its business as per the directions of its board and/or its shareholders. Also, the above provision is limited only with respect to employee benefits and not with respect to all the management policies of its subsidiaries. Thus, a limited delegated authority over few select policies cannot be deemed to represent exercise of control over all the management/policy decisions of the subject company. Furthermore, such byelaws cannot override the provisions of the (Indian) Companies Act, 2013.

Please provide copies of the bylaws of LINKEDIN CORPORATION. Also state if any amendments were made during the last 4 years.

Company’s Response: Please note that LinkedIn India does not have any specific or special access to LinkedIn Corporation and/or documents relating to the said entity. LinkedIn Corporation is not our shareholder, and we don’t have any information or access rights (contractual or otherwise) to its policies and/or internal documents of any nature, except such documents as maybe publicly available and accessible to the general public. Further, we don’t have any visibility or access to the amendments made or proposed to be made to the bylaws of LinkedIn Corporation.

You are required to refer to item no. 11 of the minutes of the Board meeting dated 02.5.2022, which refers to appointment of “managing signatories” for opening, operating, managing and closing bank accounts [at all locations] of the subject company. The resolution also provides for “operating signatories” and “bank guarantee signatories”. There is no limit on the amount of transaction that can be carried out if there are two signatories. Again, the resolution clarifies that the transactions would be binding on the company. The resolution also notes that it will not supersede or replace any resolution adopted by the Board of Microsoft Corporation related to the authorities of the CFO or Treasurer to bind the Board of Microsoft Corporation. It is important to note that almost all the signatories are Assistant Treasurers of Microsoft Corporation. Thus, it appears that the financial powers of the subject company are well and truly in the hands of the officers of Microsoft Corporation. It is noted that when this office had specifically asked for the names of the officers specifically empowered as per article 62 of your AoA, the names of the Assistant Treasurers of the Microsoft Corporation were not provided.