Achieving a tax-free rental income of ₹20,00,000 is a goal many property owners aspire to. With the recent changes introduced in the Union Budget 2025, there are strategic avenues to minimize tax liabilities on rental earnings. This guide delves into the detailed steps, leveraging deductions under Section 24 of the Income Tax Act, 1961, and understanding the implications of the latest budgetary provisions.

Page Contents

Understanding the Union Budget 2025 Reforms

The Union Budget 2025 has introduced significant tax relief measures aimed at boosting the disposable income of the middle class. Notably, the income tax exemption limit has been raised, allowing individuals earning up to ₹12,00,000 annually to be exempt from paying income tax under the new tax regime. This reform is expected to enhance consumer spending and stimulate economic growth.

Leveraging Section 24 of the Income Tax Act, 1961

Section 24 provides deductions that can significantly reduce taxable income from house property. The two primary deductions are:

- Standard Deduction [Section 24(a)]: A flat deduction of 30% on the Net Annual Value (NAV) of the property.

- Interest on Housing Loan [Section 24(b)]: Deduction of up to ₹2,00,000 on the interest paid for a housing loan, applicable if the property is rented out.

Strategic Application for Tax Efficiency

By effectively applying these deductions, property owners can reduce their net taxable rental income. For instance, after accounting for the standard deduction and housing loan interest, if the net taxable income is brought down to ₹12,00,000, the individual becomes eligible for a rebate under Section 87A, effectively nullifying the tax liability.

Step-by-step process to minimize your tax liability after announcement of Union Budget 2025

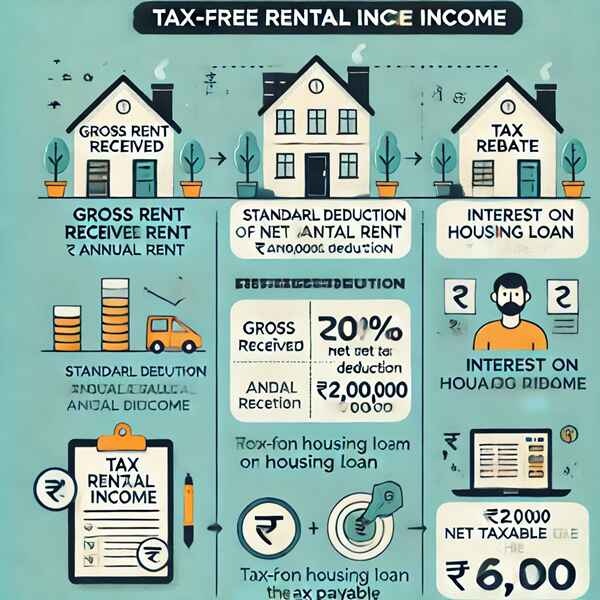

Step 1: Calculate Gross Rent Received

Mr. X rents out his property for an annual rent of ₹20,00,000.

Step 2: Apply Deductions Under Section 24 of the Income Tax Act, 1961

1. Standard Deduction [Section 24(a)]

Under Section 24(a), a standard deduction of 30% is allowed on the Net Annual Rent (gross rent received minus municipal taxes paid).

In this example:

- Gross Rent Received = ₹20,00,000

- Municipal Taxes Paid = ₹0 (assumed)

- Standard Deduction = 30% of ₹20,00,000 = ₹6,00,000

Net Rental Income after Standard Deduction:

= ₹20,00,000 – ₹6,00,000

= ₹14,00,000

2. Interest on Housing Loan [Section 24(b)]

If the property is rented out and a housing loan is taken, the borrower can claim a deduction of up to ₹2,00,000 for the interest paid on the loan.

In this example:

- Interest on Housing Loan = ₹2,00,000

Net Rental Income after Deduction Under Section 24(b):

= ₹14,00,000 – ₹2,00,000

= ₹12,00,000

Important Note:

- Deduction under Section 24(b) is allowed only if the house is let out.

- If the house is self-occupied and the taxpayer has opted for the new tax regime, this deduction cannot be claimed.

Step 3: Apply Tax Rebate Under Section 87A

As per the Union Budget 2025, if the net taxable income is up to ₹12,00,000, the taxpayer is eligible for a rebate of up to ₹60,000 under Section 87A. This rebate effectively reduces the tax liability to zero.

In this example:

- Net Taxable Income = ₹12,00,000

- Rebate = ₹60,000

- Tax Payable = ₹0

Summary

By efficiently using the deductions available under Sections 24(a) and 24(b), Mr. X successfully reduces his taxable income to ₹12,00,000. Thanks to the rebate under Section 87A, his tax liability becomes zero.

Result:

Mr. X earns a tax-free rental income of ₹20,00,000 annually.

Author Bio

Yes… assessee can claim deduction of up to Rs. 60 000 from FY 2025-26 under section 87A if he has opted for new tax regime.

Deduction u/s 87A will be in new tax regime

Yes, you can take a deduction of up to Rs. 60,000 from AY 2026-27 under section 87A if an assessee has opted for new regime.

Great !! Thanks For Sharing !!