Case Law Details

Cameron Manufacturing (India) Private Limited Vs Regional Director (NCLT Chennai)

NCLT Permits Financial Statement Revision Because Accounting Errors Were Inadvertent; Revision of Financial Statements Allowed Because Misclassifications Did Not Alter Financial Position; NCLT Approves Revised Financial Statements Because Corrections Were Needed for True and Fair View; Financial Statement Revision Allowed Because Section 131 Covers Inadvertent Accounting Misclassifications; NCLT Rejects Objections to Revision Because Section 131 Enables Correction of Adopted Financial Statements.

The National Company Law Tribunal (NCLT), Chennai, allowed an application under Section 131 of the Companies Act, 2013, permitting the petitioner company to revise its financial statements for FY 2019-20 after finding that certain entries had been inadvertently misclassified and required correction to present a true and fair view of the company’s financial position.

The petitioner stated that during FY 2019-20 it had advanced an Inter Corporate Deposit (ICD) of ₹30 crore to its related party, Schlumberger Solutions Private Limited (SSPL), of which ₹16,00,12,514 had been repaid, leaving an outstanding balance of ₹13,99,87,486 as on 31 March 2020. The company submitted that this outstanding ICD had been mistakenly classified as “Trade Receivables” instead of “Short-Term Loans and Advances.” Interest income of ₹1,48,17,808 earned on the ICD had also been incorrectly shown as “Interest Income on Bank Deposits,” while the ICD balance had been reflected under Cash Flow from Operating Activities instead of Cash Flow from Investing Activities. The company further stated that the related party disclosures omitted details of the ICD and interest income and that the disclosure required under Section 186(4) had been inadvertently omitted. According to the petitioner, these errors were clerical, unintentional, and noticed after the financial statements had been approved by the shareholders but before filing with the Registrar of Companies.

The Registrar of Companies (RoC) opposed the application, contending that the revisions involved significant amounts and amounted to violations of Sections 129(5), 143(2), and 186(4) of the Companies Act requiring compounding under Section 441 rather than revision. The RoC also argued that the company had become aware of the discrepancies before filing the financial statements and that the revisions could affect subsequent financial statements and stakeholders.

In response, the petitioner submitted that Section 131 specifically permits voluntary revision where financial statements do not comply with Sections 129 or 134. It maintained that the errors were confined to FY 2019-20, had not been carried forward to subsequent years, and that the interest income had already been offered to tax in the income tax return for the relevant financial year.

The Tribunal examined the proposed revisions and observed that the reclassification of ₹13,99,87,486 merely shifted the amount from “Trade Receivables” to “Short-Term Loans and Advances,” both falling under current assets, without affecting the company’s overall asset position. It also reviewed the ledger accounts and bank statements and found that the interest received from SSPL corresponded with the loan transaction, with differences arising because the bank statements reflected net amounts after deduction of tax at source while the ledger showed gross interest income.

The Tribunal held that Section 129 requires financial statements to present a true and fair view and comply with the prescribed accounting standards and Schedule III. It concluded that the incorrect classification of the ICD, interest income, and cash flow entries constituted inadvertent accounting errors and that the proposed revisions were limited to correcting those misclassifications and consequential adjustments without materially altering the company’s financial position. The Tribunal further accepted the management’s explanation that it chose to invoke Section 131 after the financial statements had already been approved rather than delay statutory filing. It also held that proceedings under Section 131 provide a procedural mechanism for revising financial statements and do not affect any adjudication or other proceedings that may be initiated separately by the RoC or any statutory authority. The Tribunal also granted liberty to the Income Tax authorities to examine the transactions in accordance with law.

Accordingly, the Tribunal permitted the company to revise its financial statements for FY 2019-20, subject to filing the certified copy of the order with the Registrar of Companies, convening a general meeting to consider and approve the revised financial statements, making the required newspaper publications, filing the revised financial statements and related reports with the Registrar within the prescribed period, and disclosing the reasons for revision in the Board’s Report. It clarified that the order would not prevent any statutory authority from seeking information or initiating proceedings in accordance with law and that any applicable taxes or charges would remain payable. The petition was allowed.

FULL TEXT OF THE NCLT JUDGMENT/ORDER

1. Under consideration is an application filed by Cameron Manufacturing (India) Private Limited under Sections 131 of Companies Act, 2013 (hereinafter, the Act), seeking the following reliefs,

i. Pass an order to allow the preparation of the revised Financial Statement in accordance with Section 131 of the Companies Act. 2013 tor the Financial Year 2019- 20.

ii. Pass such other orders/ directions as this Tribunal may deem fit and proper in the facts and circumstances of the case.

BRIEF FACTS OF THE CASE

2. It is stated that this application has been filed for seeking an approval to revise the Financial Statement for the FY 2019 — 2020 in accordance with Section 131 of the Companies Act r/w Rule 11, 14 and 77 of the National Company Law Tribunal Rules, 2016 (NCLT Rules, 2016).

3. It is stated that during the FY 2019-20 the Applicant Company lent a sum of Rs. 30,00,00,000 (Rupees Thirty Crores) to Schlumberger Solutions Pvt. Ltd (hereinafter, SSPL), a related party of the Applicant, as Inter Corporate Deposit(“ICD”). A sum of Rs. 16,00,12,514 (Rupees Sixteen Crores Twelve Thousand Five Hundred and Fourteen) has been repaid by SSPL. The total amount due from SSPL as on 31.03.2020 is Rs. 13,99,87,486/- (Rupees Thirteen Crores Ninety-Nine Lakhs Eighty-Seven Thousand Four Hundred and Eighty-Six).

4. It is stated that the Applicant has complied with the relevant provisions of the Companies Act, 2013 with respect to grant of the ICD. The extract of a copy of the minutes of the board meeting dated 1.03.2019 evidencing compliance is annexed with the application.

5. It is stated that the Financial Statements of the Company have been prepared in accordance with the relevant provisions of the Companies Act. 2013, except to the extent as stated herein. It is stated that notice dated 25.12.2020 was issued to the Board of Directors for approval of the Financial Statements. The Board of Directors in the Meeting dated 31.12.2020 approved the Financial Statements for the FY 2019-20.

6. It is stated that the Applicant called for the meeting of the shareholders to approve the Financial Statements for FY 2019-2020. The meeting of the shareholders took place on 31.12.2020 at Tidel Park, Ill Floor, Villankurichi Rd, Civil Aerodrome Post, Coimbatore, Tamil Nadu 641014 in accordance with the applicable provisions of the Companies Act, 2013 and the financial accounts for the FY 2019 — 20 was unanimously approved by the shareholders.

7. It is stated that the Financial Statements for FY 2019-2020 have been audited by Price Waterhouse & Company, Chartered Accounts LLP having their office at 252, Veer Savarkar Marg, Shivaji Park, Dadar (West), Mumbai – 400 028, Maharashtra.

8. It is stated that after adoption of the Financial Statements by the shareholders for FY 2019-20 at the Annual General Meeting held on 31.12.2020 but prior to filing of the same with the Registrar of Companies in compliance with Section 137 of the Companies Act, 2013, it was noticed by the management that there was an error in the Audited Annual Financial Statements of the Company for FY2019 —2020 relating to the classification of the Inter Corporate Deposit.

9. It is stated that for FY 2019-20, the outstanding amount of Inter Corporate Deposit (unsecured) to the extent of 13,99,87,486 (Rupees Thirteen Crores Ninety Nine Lakhs Eighty Seven Thousand Four Hundred and Eighty Six) provided to SSPL was erroneously classified as ‘Trade Receivables’ instead of ‘Short Terms Loans and Advances’ as per Schedule III prescribed under Section 129 of the Companies Act, 2013. As a result of the classification, the interest income of Rs. 1,48,17,808 from the ICD was inadvertently included in ‘Interest Income on Bank deposits’ under Note 17 i.e., ‘Other income’ of the Balance Sheet. However, the same was correctly classified under correct item ‘Other income’ in the Statement of Profit and Loss.

10. It is stated that the disclosure in related party transactions did not include interest income and Inter Corporate Deposits (ICD) given/repaid during the FY 2019-2020. However, the correct amount of ICD outstanding was included under “Trade Receivables”. ICD balance was included in Cash Flow from Operating Activities as against Cash Flow from Investing Activities. Interest Income was however correctly classified as Cash Flow from Investing Activities.

11. It is stated that because of the misclassification under the head “Trade Receivables”, the requisite disclosure as required under Section 186(4) of the Companies Act 2013 was inadvertently omitted while preparing the Financial Statement for the FY 2019-2020. However, the Financial Statements have complied with other provisions of Section 186 of the Companies Act.

12. It is stated that the compliances were revised and the Financial Statements were filed with the Ministry of Corporate Affairs.

13. It is stated that the mistake was unintentional and without any bad faith or an intention to deceive any person. The error of misclassification is only clerical in nature. The Applicant states that, it was much after the Financial Statements were signed by the Auditors, this issue was noticed by the management. The Applicant brought forth the observations to the attention of the Auditors as soon as the above misclassification/ compliances as a result of misclassification came to its knowledge vide an e-mail dated 22.03.2021 which contained a letter dated 01.03.2021.

14. Hence, present application has been filed before the Tribunal seeking an order to revise the Financial Statements to rectify the inadvertent errors that have crept in and make the following corrections:

a. The reclassification of outstanding amount of Inter Corporate Deposits (unsecured) of Rs. 13,99.87.486 (Rupees Thirteen Crores Ninety Nine Lakhs Eighty Seven Thousand Four Hundred and Eighty Six) as ‘Short Terms Loans and Advances’ as per Schedule Ill prescribed under Section 129 of the Companies Act, 2013.

b. Reduction of interest income of Rs. 1,48,17,808/- from the ‘Interest Income on Bank deposits’ under Note 17 ‘Other income’ of P&L and add it to other income under Note 17. Accordingly, new balance for Other income under Note 17 ‘Other income’ will be Rs, 1,52,96,008/- (4,78,200 + 1,48,17,808). Disclosure in related party transactions of the interest income and ICD given/repaid during the FY 2019-2020.

c. Reclassification of ICD balance as Cash Flow from Investing Activities instead of Cash Flow from Operating Activities

d. The requisite disclosure as required under Section 186(4) of the Companies Act 2013 for the year ended 31st March 2020,

15. It is stated that the once the fact of misclassification was brought to the notice of the Board of the Directors, it was decided by the management to file an application under Section 131 of the Companies Act. 2013 before this Tribunal. In view of the same, a board resolution was passed taking on record such an error in the Financial Statement for FY 2019-20 and after obtaining professional advice in the matter a decision was taken to file an application before this Tribunal for revision of the Financial Statement.

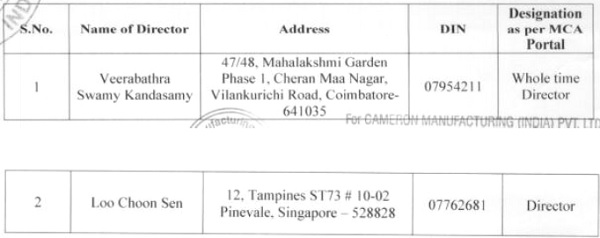

16. It is stated that the Board of Directors for FY 2019-2020 is as under,

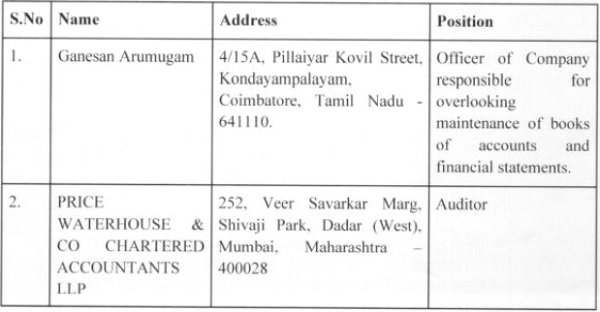

17. The details of the Auditors of the Company for FY 2019-2020 are extracted as under:

Comments of The Registrar of Companies

18. The RoC filed a Memo vide SR No. 1796 dated 10.04.2024 and Report vide S.R. No. 4546 dated 11.09.2024.

19. It is stated that the Applicant in para 4(7) of the Application has admitted that the management of the Company noticed that there was an error in classification of the Inter Corporate Deposit of the Financial Statements for the Financial year 2019- 2020 prior to filing of the same in MCA portal.

20. It is stated that there was an erroneous classification of the amount of Rs. 13,99,87,486/- as “Trade Receivables” instead of “Short term loans and advances” ; interest income of Rs.1,48,17,808/- from loan was included in “interest income on bank deposit”; Inter Corporate deposit balance was included in cash flow from operating activities instead of cash flow from investing activities’ as against the manner prescribed in Schedule III prescribed in Section 129(5) of Companies Act, 2013. The revision of such a huge amount may not be appropriate to consider as the misclassification being a violation of provisions of Section 129(5) read with Schedule – III of the Companies Act, 2013 and the same has to be compounded under Section 441 of Companies Act, 2013 by the Applicant.

21. It is stated that the revision may not be appropriate since the erroneous figure might have its effect in the returns of the company for the subsequent years financial which is used by different stakeholders, Tax authorities, Banks etc.

22. It is stated that the Applicant has stated that the requisite disclosure under Section 186 (4) of Companies Act, 2013 was inadvertently omitted while preparing the Financial Statements for the FY 2019-2020. The revision may not be appropriate to consider as the same is in violation of provisions of Section 186(4) of the Companies Act, 2013 and the same has to be compounded under Section 441 of Companies Act, 2013 by the Applicant.

23. It is stated that in the Independent Auditor’s Report as a part of financial statements filed for the FY 2019-20, the Auditor has disclosed that “In our opinion and to the best of our information and according to the explanations given to us, the aforesaid financial statements give the information required by the Companies Act, 2013 (“the Act”) in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India, of the state of affairs of the Company as at March 31, 2020, and profit and its cash flows for the year then ended”. However, in few months the management discovered a huge accounting error to the tune of Rs. 139,987,486/- & Rs. 14,817,808/-, which implies that the disclosure given by the Auditor does not give a true and fair view of the affairs of the company as the same is an violation of provisions of Section 143(2) of the Companies Act, 2013 and the same has to be compounded under Section 441 of Companies Act, 2013 by the Applicant.

24. It is stated that in para 4 (12), the Company has enclosed the e-receipt of financial statements for FY 2019-20 filed in MCA portal on 08.09.2021 vide SRN: T41382482.

25. It is stated that the Company was aware of the discrepancies in its financial statements of FY 2019 – 20 well before its filing in MCA portal on 08.09.2021 as evidenced in para 4 (12) and the amounts reported are corresponding with the balance sheet filed with MCA21 by the Recipient Company (Schlumberger Solutions Private Limited) concerned in the FY 2019- 20.

26. It is stated that in this petition for voluntary revision of the financial statement for FY 2019-20, the company has not impleaded the Central Government (Section 131 delegated to Ministry of Corporate Affairs, New Delhi) and Income Tax Department as per the provisions of Section 131 of Companies Act, 2013. Hence directions in this regard are sought and further, the RoC seeks at least eight (8) weeks’ time to file report in the matter upon serving petition impleading Ministry as respondent.

Affidavit of Service

27. In compliance with the order of the Tribunal dated 12.01.2022, the Petitioner served the copy of the Petition on the Auditor of the Company i.e., Price Waterhouse & Co. The proof of service has been filed vide SR No. 417 dated 25.01.2022.

28. This Tribunal vide order dated 17.08.2022 directed the Petitioner to implead the RD, MCA and the existing auditor of the company as respondents and to issue necessary advertisement under Rule 77(4) of the NCLT Rules, 2016. In compliance, the Petitioner filed an Affidavit dated 12.10.2022 vide SR No. 5577 evidencing the publishing of the present petition in Trinity Mirror (Coimbatore Edition) and Makkal Kural Tamil (Coimbatore Edition) on 01.10.2022. As per the AoS dated 26.10.2022, the copy of the Petition has been served on the Ministry of Corporate Affairs, RD and the Auditor of the Company PWC. Further, the acknowledgement cards and the consignment tracking reports have been filed vide SR No. 6293 dated 29.11.2022.

29. This Tribunal vide order dated 22.01.2025 also directed the Petitioner to serve copy of the Petition on the IT Department. Affidavit of Service has been filed vide SR No. 966 Dated 10.03.2025. Since none appeared for the Income Tax Department, on 12.01.2026, the right of the Income Tax Department to file reply was closed.

Response to the Report of the ROC

30. Response has been filed by the Petitioner to the report of the RoC vide SR.No.5679 dated 25.11.2024.

31. The Petitioner has stated that the error was noticed before the filing of return. However, as the same was approved by the shareholders in the AGM and signed by the directors and auditors, the Board of Directors of the Petitioner thought it fit to file a Petition under Section 131 of the Companies Act, 2013 seeking for voluntary revision.

32. Section 131 states that if it appears to the directors of a company that the financial statement of the company/report of the Board of Directors does not comply with the provisions of Section 129 or 134, they may prepare revised financial statements/report after obtaining the approval of the Tribunal. It is stated that the misclassification is in violation of Section 129(5) and has to be compounded in consonance with the spirit of Section 131 of the Companies Act, 2013. This error is only in the FY 2019-20 and has not been carried forward in the subsequent financial years. Hence, the argument, that the petition is not maintainable in view of violations of the Companies Act, 2013 and compounding proceedings must be pursued, is against the objective of Section 131.

33. It is stated that the violation of Section 143(2) and Section 186(4) of the Companies Act, 2013 claimed by RoC is only a consequential error which would be rectified once the revision as sought for is permitted by this Tribunal.

34. It is stated that the interest income of Rs. 1.48,17,808 from the loan amount has already been offered to tax while filing the Income tax return for the Financial Year 2019-20. The present petition is limited to the revision as stated therein and all the requirements under the Income Tax Act, 1961 have been complied with.

35. It is stated that the financials have been filed within the specified time period as extended by the Ministry of Corporate Affairs vide General Circular No: 18/2020 dated 21 April, 2020. It is further submitted that the RoC has confirmed that the amounts which have been misclassified are corresponding to the balance sheet of the recipient company namely, Schlumberger Solutions Private Limited.

Memo filed by the Petitioner

36. On 13.02.2026, this Tribunal directed the Petitioner to file proof regarding the interest received from the third parties along with the ledger statements. Memo has been filed by the Petitioner vide Sr. No. 1619 dated 09.04.2026 in compliance of the order dated 13.02.2026.

FINDINGS OF THIS TRIBUNAL

37. The present Petition has been filed under Section 131 of the Companies Act, 2013 seeking permission to revise and rectify certain misclassifications and consequential errors in the financial statements of the Petitioner Company for the FY 2019-2020.

38. Section 131 of the Companies Act, 2013 reads as follows:

“131. Voluntary revision of financial statements or Board’s report

(1) If it appears to the directors of a company that —

(i) the financial statement of the company; or

(ii) the report of the Board,

do not comply with the provisions of section 129 or section 134 they may prepare revised financial statement or a revised report in respect of any of the three preceding financial years after obtaining approval of the Tribunal on an application made by the company in such form and manner as may be prescribed and a copy of the order passed by the Tribunal shall be filed with the Registrar:

Provided that the Tribunal shall give notice to the Central Government and the Income tax authorities and shall take into consideration the representations, if any, made by that Government or the authorities before passing any order under this section:

Provided further that such revised financial statement or report shall not be prepared or filed more than once in a financial year:

Provided also that the detailed reasons for revision of such financial statement or report shall also be disclosed in the Board’s report in the

relevant financial year in which such revision is being made.

(2) Where copies of the previous financial statement or report have been sent out to members or delivered to the Registrar or laid before the company in general meeting, the revisions must be confined to —

(a) the correction in respect of which the previous financial statement or report do not comply with the provisions of section 129 or section 134; and

(b) the making of any necessary consequential alternation…”

39. The Petitioner submits that it had extended loans to its related party, namely, Schlumberger Solutions Private Limited (“SSPL”). According to the Petitioner, the loan amount and the interest income earned thereon were inadvertently misclassified in the financial statements in FY 2019-2020. The proposed corrections are set out below:

| S. No. | Amount (Rs.) | Wrong Classification Correct | Classification |

| 1 | 13,99,87,486/- | Trade Receivables | Short Term Loans and Advances |

| 2 | 1,48,17,808/- | Interest Income on Bank Deposit | Interest Income from Loan |

| 3 | 13,99,87,486/- | Cash Flow from Operating Activities | Cash Flow from Investing Activities |

40. It is observed that the reclassification of Rs.13,99,87,486/-pertains to the current assets portion of the balance sheet. Under Schedule III of the Companies Act, 2013, both Trade Receivables and Short-Term Loans and Advances were disclosed under the broad head of Current Assets. Consequently, the proposed correction merely involves a reclassification within the same asset category and does not affect the overall asset position of the Company.

41. With regard to reclassification of interest income, the Petitioner has produced the ledger account of SSPL as well as the corresponding bank statements. The material particulars are tabulated below:

| S. No. | Date | Amount in Ledger

(Rs.) |

Amount in Bank Statement (Rs.) |

| 1 | 03.10.2019 | 56,60,959 | 50,94,863 |

| 2 | 02.01.2020 | 53,74,931 | 48,37,438 |

| 3 | 31.03.2020 | 37,81,918 | 34,16,240 |

42. The amounts reflected in the bank statements correspond to the net sums received after deduction of tax at source (TDS), whereas the ledger records reflect the gross interest income. Upon examination of the documents placed on record, it appears that the aforesaid amounts were received from SSPL towards interest on the loan advanced by the Petitioner.

43. Section 129 of the Companies Act, 2013 mandates that financial statements shall give a true and fair view of the state of affairs of the Company, comply with the accounting standards notified under Section 133, and be prepared in the manner prescribed under Schedule III. Therefore, where the financial statements do not accurately reflect the true nature of transactions and require correction to present a true and fair view, the jurisdiction under Section 131 can be invoked.

44. Based on the ledger extracts, bank statements, and other supporting documents, we are satisfied that the interest income was inadvertently disclosed as interest income from bank deposits instead of interest income from loans. Similarly, classification of loan amount under Trade Receivables instead of Short-Term Loans and Advances appears to be an inadvertent accounting error. The consequential modification sought in the cash flow statement, namely, reclassification of the amount from Cash Flow from Operating Activities to Cash Flow from Investing Activities, is a consequential adjustment arising from the correction of the principal classification. The proposed revision does not alter the financial position of the Company in any material respect and only seeks to correctly present the nature of the transaction.

45. Accordingly, we find merit in the submission of the Petitioner that the proposed revisions are limited to correcting inadvertent misclassifications and are necessary for presenting a true and fair view of the financial statements. The revisions are confined to the corrections required for compliance with Section 129 of the Companies Act, 2013 and the consequential changes flowing therefrom.

46. We are satisfied that the Petitioner Company fulfils the requirements of Section 131 of the Companies Act, 2013 read with Rule 77 of the National Company Law Tribunal Rules, 2016 and is entitled to seek revision of its financial statements for the FY 20192020.

47. The Petitioner has also submitted that the interest income of Rs.1,48,17,808/- arising from the loan transaction has already been offered to tax while filing its Income Tax Return for the relevant financial year. In this case, despite service of notice, the Income Tax Authorities have not entered appearance. Considering the above, liberty is given to examine the transactions in accordance with the relevant law.

48. The RoC has contended that the Petitioner was aware of the alleged misclassifications at the time of filing the financial statements and therefore ought not to be permitted to revise the same. Section 131 contemplates revision of financial statements that have already been adopted, laid before the Annual General Meeting, or filed with the RoC. Further, non-filing/ delayed filing of financial statements attracts significant penal liabilities under the statute. We find that the explanation provided by the management that they opted to utilise the provision under Section 131 of the Companies Act, 2013 instead of postponing of the filing of financial statements before the RoC is plausible. The very purpose of the provision is to enable correction of financial statements which are subsequently found.

49. The RoC has further contended that the misclassifications constitute offences punishable under Sections 129(7), 186(13) and 143(15) of the Companies Act, 2013.

50. In this regard, reference is made to the legislative intent behind Section 131 permits a company, subject to appropriate safeguards and approval of the Tribunal, to revise financial statements that do not present a true and fair view of its affairs. The same has been enumerated in the Report of the Standing Committee, 2011 which is extracted hereunder:

“The change proposes to provide procedural requirement in respect of revision in accounts in certain cases. The present law is silent in respect of re-opening or re-casting of accounts. In certain cases, particularly in cases relating to fraud, there may be need to re-open/recast accounts to reflect true and fair accounts. In case of Satyam, such recasting was ordered by the Court. The provisions in the Bill mandate such re-opening on the order of Court or Tribunal. In other cases the re-opening is being permitted, through order of Tribunal, with adequate safeguards.”

51. Accordingly, proceedings under Section 131 of the Companies Act, 2013 are confined to providing a procedural mechanism for the revision of financial statements. This Order shall not affect any adjudication proceedings, or any other proceedings initiated or proposed to be initiated by the RoC or any other statutory authority in accordance with law.

52. In view of the foregoing discussion, this Tribunal is satisfied that the financial statements, as originally filed, do not accurately reflect the true nature of the transactions undertaken by the Company and therefore require revision to present a true and fair view as contemplated under Section 129 of the Companies Act, 2013. We accordingly permit the Petitioner Company to revise and recast its financial statements in terms of this Order. We are satisfied that the Petitioner fulfils the requirements under Section 131 of the Companies Act, 2013 and Rule 77 National Company Law Tribunal Rules, 2016. Accordingly, the Petitioner is permitted to revise its financial statements for the Financial Year 2019-2020 in accordance with the applicable accounting standards and the corrections set out in the Petition. This Tribunal directs as under:

a. Certified copy of the order be filed by the petitioner with the Registrar of Companies within 30 days after receipt of the same.

b. A general meeting be called within two months and notice of such general meeting along with reasons for the change in financial statements be published in newspapers in English and in vernacular language. In the general meeting, the revised financial statements, statement of directors and the statement of auditors be put up for consideration before a decision is taken on the adoption of the revised financial statements. On approval of the general meeting, the revised financial statements along with the statement of auditors or revised report of the Board, as the case may be, shall be filed with the Registrar of Companies within thirty days of the date of approval by the general meeting.

c. The detailed reasons for revision of such a financial statement or report shall also be disclosed in the Board’s Report in the relevant financial year in which revision is made.

d. It is made clear that this order shall not preclude any of the authorities from seeking any information or documents from the petitioner, in accordance with law, in the process of any proceedings as per the revised financial statement of the petitioner-company.

e. Further, in the said process, if the Petitioner-Company is required to pay any charges or taxes, it is liable to pay the same, in accordance with law.

f. For the aforesaid reasons, the instant petition is allowed and the petitioner is permitted to revise the financial statement of the company for the year 2020 — 2021 as per the accounting standards.

g. However, in terms of the second proviso to Section 131 (1) of the Companies Act, 2013, the Petitioner Company cannot seek for the revised Financial Statement again for the Financial Year 2020 — 2021.

53. With the above directions, the present Company Petition CP/155/CHE/2021 stands allowed.

54. File be consigned to records.

Author Bio