Case Law Details

ITO Vs Sai Balaji Developers (ITAT Hyderabad)

Section 68 Addition Deleted Because Source of Partner’s Capital Was Established: ITAT; ITAT Rejects Section 68 Addition Because Sale Proceeds Fully Explained Capital Contribution; Partner’s Capital Contribution Accepted Because Department Had Already Taxed Land Sale Proceeds; Section 68 Addition Cannot Survive Because Documentary Evidence Proved Source of Funds: ITAT

The Income Tax Appellate Tribunal (ITAT), Hyderabad, dismissed the Revenue’s appeal and upheld the order of the Commissioner of Income Tax (Appeals) [CIT(A)] deleting an addition of ₹68.75 crore made under Section 68 of the Income Tax Act, 1961 in the hands of a partnership firm. The dispute arose after the Assessing Officer (AO) treated the capital introduced by one of the partners, Mr. A. Ravi Kumar, as unexplained cash credit, except for ₹5.21 crore that was directly transferred from the partner’s bank account to the firm’s bank account.

The assessee explained that the total closing balance in the partners’ capital accounts included the opening capital balance, partners’ remuneration, and share of profit, apart from fresh capital introduced during the year. Out of the total capital, ₹65.79 crore represented capital introduced by Mr. Ravi Kumar, while the balance comprised opening capital, remuneration of ₹18 lakh, and partners’ share of profit of ₹4.67 crore. The Tribunal noted that the AO had incorrectly taken the entire closing balance into account without excluding these components.

The assessee further explained that the source of the partner’s capital contribution was the sale consideration received from the sale of agricultural land to Microsoft Corporation (India) Private Limited. The sale deed showed that the partner received approximately ₹127.47 crore (net receipt after TDS of about ₹126.19 crore) from the transaction. According to the assessee, these funds were used partly by transferring money directly to the firm’s bank accounts and partly by making payments directly to landowners on behalf of the firm for acquisition of land required for its real estate business. Documentary evidence, including registered sale deeds, bank statements, and details of payments, was produced before the authorities.

The CIT(A) examined the evidence and found that the actual increase in partners’ capital by way of fresh introduction was ₹65.79 crore, not the higher figure adopted by the AO. It was also found that the partner had transferred about ₹11.87 crore directly to the firm’s bank accounts and had made payments of about ₹54.11 crore directly to land vendors on behalf of the firm, aggregating to approximately ₹65.98 crore. These transactions were supported by bank statements and sale documents. The CIT(A) held that remuneration and share of profit credited to partners’ capital accounts originated from the firm’s books and could not be treated as unexplained cash credits. Accordingly, those amounts were excluded from the addition.

The Tribunal noted that the Department itself had assessed the sale of land by the partner in his individual assessment. In that assessment, the AO computed Long-Term Capital Gain of ₹125.87 crore arising from the sale of land to Microsoft Corporation (India) Private Limited, thereby accepting the sale consideration received by the partner. The Tribunal observed that this established the availability of funds in the partner’s hands for making the capital contribution to the firm.

Agreeing with the CIT(A), the Tribunal held that the assessee had explained the source of the capital introduced through documentary evidence, including sale deeds and bank statements, and had discharged the primary onus under Section 68. It found no error in the CIT(A)’s conclusion that the addition under Section 68 was unsustainable. Since the Department failed to controvert the factual findings recorded by the CIT(A), the Revenue’s appeal was dismissed.

The assessee had also filed a separate appeal. During the hearing, it was submitted that the appeal had been filed inadvertently as a regular appeal instead of a cross-objection, despite there being no grievance against the CIT(A)’s order. The assessee filed an application seeking withdrawal of its appeal, and the Department raised no objection. The Tribunal permitted the withdrawal and dismissed the assessee’s appeal as withdrawn. Consequently, the Revenue’s appeal was dismissed, and the assessee’s appeal was dismissed as withdrawn.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

These cross appeals filed by the Revenue and Assessee are directed against the Order dated 06.11.2024 of learned CIT(A)-National Faceless Assessment Centre [in short “NFAC”], Delhi, for the assessment year 2022-2023.

2. The Revenue has raised the following grounds of appeal:

i. “The CIT(A) failed to appreciate that the assessee could not establish the primary onus on its part to explain the sources of the capital introduction by the partner Sri. A. Ravi Kumar.

ii. The CIT(A) erred on facts and in law in concluding that the sources for capital introduction of Rs.65.97 Crores by partner Sri. A. Ravi Kumar remained explained merely relying on bank accounts of the partner and the assessee-firm as bank accounts are not conclusive books of account of the assessee-firm.

iii. The CIT(A) failed to appreciate that the AO has given due, credit for an amount of Rs.5.21 Crores being the amount of withdrawals made by the partner Sri. A. Ravi Kumar in his bank account favouring the assessee-firm and only added the difference amount of Rs.65.97 Crores towards unexplained cash credits u/s.68 of the I.T. Act, 1961.

iv. The CIT(A) failed to appreciate that having substantial sale proceeds on account of transaction made by the partner towards hi share with M/s. Microsoft Corporation Ltd cannot come to the rescue of partner to explain the introduction of capital by him to the firm.

v. The CIT(A) failed to appreciate that through the identify and creditworthiness of the transaction made by Sri. A. Ravi Kumar was established, the core element of genuineness of the same was not established by the assessee-firm.

vi. Any other ground that may be urged at the time of hearing.

3. The solitary issue arises in the appeal of the Revenue is whether in the facts and circumstances of the case the learned CIT(A) has erred in accepting the source of capital introduced to the tune of Rs.65.97 crores by the partner Sri Akula Ravikumar and thereby deleting the addition made by the Assessing Officer of Rs.68.75 crores u/sec.68 of the Income Tax Act [in short “the Act”], 1961 .

4. The assessee is a partnership firm and filed its return of income for the year under consideration on 07.11.2022, admitting a total income of Rs.4,67,73,330/-. The case of the assessee was selected for scrutiny and the Assessing Officer issued a show cause notice to the assessee to explain the source of introduction of the capital by the partners. The assessee filed a reply and submitted that out of the total closing balance in the capital account of the three partners of Rs.73.96 crores there is a credit in the partners’ capital account on account of share of profit of Rs.1,55,86,640/- each total amounting to Rs.4,67,59,919/-and remuneration of Rs.18 lakhs during the year under consideration. Further, there was an opening balance of Rs.3,32,10,611/- in the capital accounts of the partners. The remaining amount of Rs.65.79 crores was introduced by one of the partners, Sri Akula Ravi Kumar. The Assessing Officer accepted the source of introduction of the capital in the partners account to the tune of Rs.5,21,36,000/- as found from the bank accounts of the partner Sri Akula Ravi Kumar as well as bank account of the assessee firm out of the closing balance of Rs.73.96 crores and the balance amount of Rs.68.75 crores was added as unexplained cash credit u/sec.68 of the Act.

5. The assessee challenged the action of the Assessing Officer before the learned CIT(A) and explained that the Assessing Officer had not considered the opening balance in the capital account of the three partners, the share in the profit of the firm credited in the capital accounts of the partners as well as the remuneration credited to the capital accounts of the partners. Further, the assessee explained that the balance amount of Rs.65.79 crores was introduced by the partner Sri Akula Ravi Kumar by way of purchase consideration paid in respect of the land purchased by the assessee firm. The source of the said payment made by the partner was also explained as the sale of agricultural land by the said partner to M/s. Microsoft Corporate India Private Limited for a consideration of Rs.126.99 crores. Thus, assessee contended before the learned CIT(A) that the partner was having sufficient funds to make the said payment of Rs.65.79 crores in respect of the land purchased by the assessee partnership firm, which was credited in the capital account of the partner as introduction of the capital. The learned CIT(A) accordingly deleted the addition made by the Assessing Officer and aggrieved by the order of the learned CIT(A), the Revenue has filed the appeal before the Tribunal.

6. The learned DR has submitted that the Assessing Officer has given the reasons that, except the bank account transfer by Sri Akula Ravi Kumar of Rs.5,21,36,000/- the assessee failed to produce the supporting evidence to explain the source of the remaining amount for the introduction of capital in the hands of the partners. He has further submitted that the assessee has failed to produce any record to authorise the partner for making the said payment on behalf of the assessee firm in respect of the alleged purchase of land. He has relied upon the Order of the Assessing Officer and submitted that despite various opportunities given by the Assessing Officer the assessee failed to substantiate its claim with the help of supporting documents, as the assessee did not furnish copies of the bank account of the partner to show the source of the capital introduced during the year. From the bank account produced by the assessee before the Assessing Officer, the Assessing Officer found that only a sum of Rs.5,21,36,000/- was transferred from the partner’s bank account to the firm’s bank account and the remuneration amount remains unexplained.

7. On the other hand, the learned Authorised Representative for the Assessee has submitted that the Assessing Officer has made the addition by taking the closing balance in the capital account of the partner without excluding the opening balance, the shares of the partners in the profit of the firm credited in the capital account of the partners as well as the remuneration of the partners credited in the capital accounts of the partners. All these details were available before the Assessing Officer as part of the record and particularly, the profit and loss account as well as the bank account of the assessee and partners. Though the Assessing Officer has accepted the fact that the sum of Rs.5,21,36,000/- was transferred from the bank account of the partner Sri Akula Ravi Kumar to the bank account of the assessee firm however, the Assessing Officer has made the addition of Rs.68.75 crores without considering the fact duly explained with supporting evidence that the partner Sri Akula Ravi Kumar has transferred the sum of Rs.11,87,02,000/- from his bank account to the bank account of the assessee firm which is reflected from the bank account statements of the assessee as well as the partner. Apart from the said amount, the partner also made the payment for the business purpose of the assessee firm towards purchase consideration of the land to the tune of Rs.54,11,62,485/- total amounting to Rs.65,98,54,485/-. Thus, the learned Authorised Representative for the Assessee submitted that the assessee explained all the details before the Assessing Officer however, the Assessing Officer has accepted only the part amount of transfer from the bank instead of the full amount of Rs.11.87 crores and balance amount spent by the partner towards purchase of land on behalf of the firm to the tune of Rs.54.11 crores was not at all considered by the Assessing Officer despite the transactions are reflected in the bank account statements and sale deeds produced before the Assessing Officer. The learned CIT(A) has deleted the addition by considering all these facts manifest from the record. The learned Authorised Representative for the Assessee has referred to the sale deed dated 30.09.2021 placed at Page nos.281 to 404 of the paper book, whereby the partner Sri Akula Ravi Kumar as well as the assessee firm, transferred their respective shares in the land in favour of M/s. Microsoft Corporation (India) Private Limited and the partner received the consideration of Rs.126.19 crores, which is duly reflected in the said sale deed, and therefore, the source in the hands of the partner was also duly explained for making the payment of subsequent purchase of land on behalf of the assessee firm. The department has accepted the said transaction of sale of land by the partner for a consideration of Rs.126.19 crores and the same was also assessed by the Assessing Officer to tax in the hand of the partner Sri Akula Ravi Kumar while passing the assessment order u/sec.143(3) r.ws..144B of the Act dated 21.03.2024. He has filed copy of the said assessment order.

8. We have considered the rival submissions and carefully perused the relevant record. During the scrutiny assessment the Assessing Officer has made the addition on account of unexplained credit in respect of the capital introduced by the partners u/sec.68 of the Act by giving the reasons in Para nos.4.7 and 4.8 as under:

“4.7. Point wise rebuttal of reply of the assessee including analysis of any case law relied upon.

The assessee vide its reply dated 06.03.2024 reiterated its previous claim that the partner of this firm has sold a land in his individual capacity in favour of M/s. MICROSOFT CORPORATION LTD vide registered sale deed No. 14652/2021 during the year and this is the source of the capital which was subsequently introduced in the assessee firm.

However, the assessee once again failed to substantiate its contention by not producing the following documentary evidences as sought by this office for verification of assessee’s claim:

-

- Bank statement of the assessee, reflecting the relevant entry/entries through which such capital has been introduced in its capital account.

- Partner’s Capital Account

Further, from the perusal of the partner’s bank account, as produced by the assessee firm, it is observed that partner Mr. Akula Ravi Kumar had transferred the fund amounting to Rs.5,21,36,000/- only to the assessee as per the details mentioned below:

In view of the above, the genuineness of the transactions regarding the introduction of balance amount of such huge capital (i.e. 73,96,75,255/- minus 5,21,36,000/- equals to Rs.68,75,39,255/-) in the assessee firm during the year could not be verified.

4.8 Conclusion drawn:

During the course of assessment proceedings, the assessee was given sufficient opportunity through various notices (as per details given in table supra) to represent its case and was also requested to furnish details with regard to the above-mentioned transactions. Replies of the assessee have been considered and placed on record.

In view of the above facts and discussion, it is evident that the assessee had not submitted justified explanation and/or supporting documents/evidences (as detailed in the preceding para 4.7) regarding the substantial increase in firm’s capital during the year under consideration.

Therefore, an amount of Rs.68,75,39,255/- (being the unexplained amount of capital introduced in the assessee firm during the year) is being treated as Unexplained cash credits u/s 68 of the Act and hence, added back to the total income of the assessee for the year under consideration. [Addition: Rs.68,75,39,255/-]”

8.1. It is pertinent to note that the Assessing Officer has taken the closing balance in the capital account of the partners of the assessee firm, the details of which, are as under:

| S. No. | Name of the Partner | Op. Balance | Invested during the year (Net of drawings) | Remun eration | Share of Profit | Closing Balance |

| 1 | Mr A Ravi Kumar | 1,47,20,011 | 65,79,0 4,725 | – | 1,55,8 6,640 | 68,82, 11,376 |

| 2 | Mrs A Vasantha | 1,64,88,072 | – | 6,00, 000 | 1,55,8 6,640 | 3,26,74,712 |

| 3 | Mr A Varun Kumar | 20,02,527 | – | 12,00, 000 | 1,55,8 6,640 | 1,87,89,167 |

| TOTAL | 3,32,10 ,611 | 65,79,04, 725 | 18,00, 000 | 4,67,59, 919 | 73,96,7 5,255 |

8.2. From these details, it is clear that there was an opening balance in the partner’s capital account to the tune of Rs.3,32,10,611/- and a credit amount of share of the profit to the tune of Rs.4,67,59,919/- as well as a credit of Rs.18 lakhs on account of remuneration. Without even considering and excluding these credits and opening balance, the Assessing Officer has taken the closing balance of the partners’ capital account and then allowed transfer of Rs.5,21,36,000/- as found the transfer from the bank account of Sri Akula Ravi Kumar to the bank account of the assessee firm. These transfers were taken only from one bank account of the partner Sri Akula Ravi Kumar. The assessee also explained before the Assessing Officer that the partner has made the payment to the tune of Rs.54,11,62,485/-towards the purchase of land on behalf of the assessee firm. The Assessing Officer has not disputed the purchase of land by the firm during the year which is also reflected in the profit and loss account as part of the purchase during the year and also part of the closing stock of land. However, the Assessing Officer has made the addition on the ground that the assessee has not proved with documentary evidence the source of the said payment in the hand of the partner. It is pertinent to note that the assessee filed sale deed dated 30.09.2021 whereby Sri Akula Ravi Kumar the partner as well as the assessee firm along with other vendors sold the land to M/s. Microsoft Corporation (India) Private Limited for a total consideration of Rs.158,28,82,351/- out of which, the partner Sri Akula Ravi Kumar received a total consideration of Rs.127.47 crores and net amount after TDS of Rs.126.19 crores and therefore, the sale deed reflects the source of the fund in the hand of the partner Sri Akula Ravi Kumar to the tune of Rs.126.19 crores as net amount received after TDS. The said availability of fund is further corroborated by the assessment order in the case of the partner Sri Akula Ravi Kumar dated 21.03.2024 passed u/sec.143(3) r.w.s.144B of the Act whereby the Assessing Officer has assessed the said amount as capital gain in the hand of the said partner in Para no.4.6 and 5 of the said assessment order as under:

“4.6. Conclusion drawn:

In view of aforesaid facts and findings it is concluded that the assessee explanation to show cause notice is not satisfactory and the same has failed to show cause as to why the nature and status of the pieces of the land sold by the assessee to M/S MICROSOFT CORPORATION (INDIA) PRIVATE LIMITED during the F.Y. 2021-22 relevant to A.Y. 2022-23 should not be ‘Non-agricultural and capital asset u/s 2(14) of Income Tax Act, 1961 and as to why the capital gain on such transfer of capital asset should not be chargeable to tax.

In accordance with aforesaid conclusion the pieces of land sold to M/s MICROSOFT CORPORATION (INDIA) PRIVATE LIMITED during the F.Y. 2021-22 relevant to A.Y. 2022-23 is considered Capital Asset u/s 2(14) of the Income Tax Act, 1961. As such profits and gains from such transfer of capital asset is taxable under the head Capital Gain. Even after repeated requirement through notice u/s 142(1) the assessee did not furnish the calculation of gain from property transfer. However, from material gathered u/s 133(6) same is calculated below:

| Particulars | Rs. | Rs. |

| Sale consideration of property transferred to M/s MICROSOFT CORPORATION (INDIA) PRIVATE LIMITED | 1,27,47,09,413 | |

| Cost of acquisition (50,01,000 + 21,50,000 + 45,00,000 + 9,22,500 + 30,45,000) | 1,56,18,500 | |

| Cost of conversion (295988 + 14625 + 24000) | 3,34,613 | |

| Total Cost | 1,59,53,113 | |

| Long Term Capital Gain | 1,25,87,56,300 |

The assessee has failed to offer the Long Term Capital Gain of Rs.125,87,80,300/-calculated above for taxation. Hence, the said amount is added to his total income. Penalty proceeding u/s 270A is initiated for under reporting of such income.

The assessee has failed to establish his claim of cultivation of land with required documentary evidences. Hence, exemption claimed for agricultural income of Rs.66,125/- is disallowed and the same is treated as profit from business. Penalty proceeding u/s 270A is initiated for under reporting of such income.

| Sl. No. | Description | Amount (in Rs.) |

| 1 | Income as per Return of Income filed | Rs. 15,35,650/- |

| 2 | Income as computed u/s 143(1)(a) | Rs. 15,35,650/- |

| 3 | Variation in respect of the issue involved: | Rs. 125,88,22,425/- |

| (i) LTCG of Rs. 125,87,80,300 [as discussed above] | ||

| (ii) Agricultural income shown found to be business income of Rs. 66,125/- [as discussed above] | ||

| So, total Variation of Rs. 125,88,46,425/- | ||

| 4 | Total Income Assessed | Rs. 126,03,58,075/- |

8.3. Thus, the department itself has assessed the said sale consideration of Rs.127.47 crores for the purpose of capital gain to the tune of Rs.125.87 crores in the hand of the partner Sri Akula Ravi Kumar. Accordingly, the source in the hand of the patner is established beyond any doubt when the Assessing Officer has assessed the said amount in the hand of the partner on transfer of the land. The learned CIT(A) has decided this issue in Para nos.5.2 to 5.9 as under:

“5.2. Brief facts leading to the impugned addition is that case of the appellant was selected for scrutiny for the reason “substantial increase in capital in a year. During the course of assessment proceedings, appellant submitted that one of the Partners of the firm Sri Akula Ravi Kumar has made the contribution to the capital for the purpose of business of the appellant firm. The business of the Appellant firm involves developing of residential plots & other real estate development activities. And for the purpose of development, the appellant firm has purchased certain lands. Due to urgency in the matter to seal the deal for purchase of land partner of the appellant firm Shri Ravi Kumar has made the payments directly to the sellers of the land which is purchased for the purpose of promotion of the business of the appellant firm. Certain payments were directly transferred to the bank account of the appellant firm for the purpose of its business by partner Shri Ravi Kumar. The details of capital introduced by the partner Sri Akula Ravi Kumar were submitted before the AO along with bank statement as well as its source. However, not satisfied with the explanation submitted by the appellant, AO made the impugned addition u/s 68 of the Act.

5.3. It is the contention of the appellant that AO has not considered and accepted the entire capital introduction in spite of documentary evidences submitted in support of the capital introduced by the partner in the books of appellant firm ignoring the basic fact that the capital introduced by the partner of the firm has clear sources. That AO has accepted only the amounts which is reflecting the name of the firm as ‘Sai Balaji Developers’ and rest of the amounts paid by the partner for the purpose of business of appellant firm was not considered. Appellant has submitted the following details in respect of capital introduced by the partner Sri Akula Ravi Kumar as under:

| S.No. | Particulars | Amount (in Rs.) |

| a. | Transfer of funds by the partner Shri. Akula Ravi Kumar bank

account to Appellant bank |

11,87,02,000 |

| b. | Payments made by Shri. Akula Ravi Kumar for the purpose of business of the Appellant firm | 54,11,62,485 |

| TOTAL amount of capital

additions Shri. Akula Ravi |

65,98,64,485 |

Appellant has further submitted that during the year under consideration, partner Sh. Akula Ravi Kumar has paid certain amounts to the firm and certain amount directly to the landlords for purchase of the lands in the name of the appellant firm. All these amounts are transferred from the bank account of the partner Sri Akula Ravi Kumar and all the amounts duly recorded in the books of accounts of the appellant firm and the same is confirmed by the” partner Shri Ravi Kumar with his clear sources during the course of scrutiny proceedings before the AO. However, AO has only seen the name of the firm in the bank statement of the partner and even the direct bank transfer made by the partner to the firm’s bank account was not considered. Further, the amounts paid by the partner to the land lords for purchase of land was also ignored. In support of its contention appellant has uploaded the bank account statement of the partner highlighting the details of payment made by him directly to the landlords as well as to the appellant firm. The details of transfer of funds by the partner to the Appellant firm for its business purpose has been submitted by the appellant which is reproduced as under for the sake of clarity:-

1) From Partner HDFC A/c No. 50100114632838 (Annexure-6):

| S. No. | Date | Amount (in Rs.) | Appeared in Firm Bank Account | Reference Page Number of Bank Statement |

| 1 | 23-04-2021 | 50,000 | HDFC 50200017303375 | Annexure-4 (page no. 1) |

| 2 | 30-04-2021 | 1,00,000 | HDFC 50200017303375 | Annexure-4 (page no. 1) |

| 3 | 30-06-2021 | 20,00,000 | HDFC 50200017303375 | Annexure-4 (page no. 2) |

| 4 | 10-12-2021 | 1,00,00,000 | HDFC 50200017303375 | Annexure-4 (page no. 8) |

| 5 | 13-12-2021 | 1,50,00,000 | HDFC 50200017303375 | Annexure-4 (page no. 8) |

| 6 | 19-01-2022 | 50,00,000 | HDFC 50200017303375 | Annexure-4 (page no. 9) |

| 7 | 08-03-2022 | 1,00,00,000 | HDFC 50200017303375 | Annexure-4 (page no. 11) |

| 8 | 26-05-2021 | 18,90,000 | HDFC 50200027323037 | Annexure-5 (page no. 1) |

| 9 | 19-02-2022 | 3,00,000 | HDFC 50200027323037 | Annexure-5 (page no. 1) |

| Total (1) | 4,43,40,000 |

2) From Partner HDFC A/c No. 50200061880094:

| S. No. | Date | Amount (in Rs.) | Appeared in Firm Bank Account | Reference Page Number of Bank Statement |

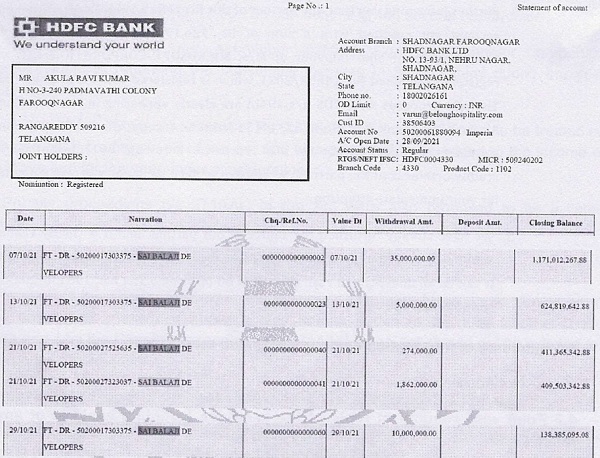

| 1 | 07-10-2021 | 3,50,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 5) |

| 2 | 13-10-2021 | 50,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 5) |

| 3 | 29-10-2021 | 1,00,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 6) |

| 4 | 12-11-2021 | 2,00,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 6) |

| 5 | 28-03-2022 | 25,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 7)* |

—-

| S. No. | Date | Amount (in Rs.) | Appeared in Firm Bank Account | Reference Page Number of Bank Statement |

| 1 | 07-10-2021 | 3,50,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 5) |

| 2 | 13-10-2021 | 50,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 5) |

| 3 | 29-10-2021 | 1,00,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 6) |

| 4 | 12-11-2021 | 2,00,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 6) |

| 5 | 28-03-2022 | 25,00,000 | HDFC 50200017303375 | Annexure-7 (page no. 7)* no.11) |

| 6 | 21-10-2021 | 18,62,000 | HDFC 50200027323037 | Annexure-8 (page no. 1) |

| Total (2) | 7,43,62,000

|

|||

| Grand Total (1+2) -A | 11,81,02,000 | |||

The above bank statement 50200061880094 of the partner is enclosed as Annexure 9.

B. Payments made by the partner for the lands purchased by the Appellant firm:

The details of payments made by the partner through his HDFC A/c No: 50200061880094 for the lands purchased by the Appellant firm are given below:

| S. No | Date | Particulars | Sale deed | Amount | Reference page number of bank statement |

| 1 | 11.10.2021 | Shetrunjay Properties (a dvan ce) |

10380/2023-Annexure-II | 45,00,00,000 | Annexure-10 (page no. 2) |

| 2 | 07.10.2021 | Farhana Yasmeen | 4117/2021 | 72,00,000 | Annexure-10 (page no.1 & 2 & 3) |

| 3 | 07.10.2021 | Farhana Yasmeen | 90,00,000 | ||

| 4 | 20.10.2021 | Farhana Yasmeen | 1,78,20,000 | ||

| 5 | 27.10.2021 | Farhana Yasmeen | 1,49,760 | ||

| 6 | 07.10.2021 | Mohammed lmitiyaz Pasha | 4151/2021 —Annexure-13 | 72,00,000 | Annexure-10 (page no.1 & 2

(Pages 3 & 4) |

| 7 | 07.10.2021 | Mohammed Imtiyaz Pasha | 90,00,000 | ||

| 8 | 07.10.2021 | Mohammed Imtiyaz Pasha | 1,78,20,000 | ||

| 9 | 07.10.2021 | Mohammed Imtiyaz Pasha | 6,97,725 | ||

| 10 | 14.10.2021 | Munoth Industries | 16449/2021 – Annexure-14 | 2,22,75,000 | Annexure-10 (page no. 2) |

| TOTAL – B | 54,11,62,485 | ||||

| Grand Total (A + B) from above | 65,98,64,485 |

5.4. It has further been submitted by the appellant that all the above payments are duly recorded in the books of account and supported by the above documentary evidences which were also submitted before the AO during the course of scrutiny proceedings. The sources of above payments made by the partner Sri Akula Ravi Kumar has also been explained before AO that during the year under consideration, the partner Shri Akula Ravi Kumar and the Appellant along with 4 other parties have jointly sold an agricultural land to M/s Microsoft Corporation (India) Private Limited for a sale consideration of Rs.158,28,82,351/- vide registered document number 14652/2021 on 30-09-2021. The share of the partner comes to Rs.126,19,62,319/- which can be seen at page no. 17 of the said sale deed. Further, the same is also seen from the bank account of the partner 50200061880094 as Annexure-16 at page No 1. The sale consideration received by the partner for Rs.126,19,63,319/- is the source for making the investments in the Appellant firm for Rs.65,98,64,485/-. These facts were also submitted during the course of scrutiny proceedings, but the AO has failed to appreciate it. Further, appellant has also contended that there is no cash deposit or unexplained entry for making the investment by the partner for the appellant firm. The clear source is from sale of agricultural land and the amount is clearly appearing in the bank account of the partner Sri Akula Ravi Kumar which is received from the well-known Multi National Company which is evidenced by the sale deed and bank account of the partner.

5.5. I have carefully gone through the grounds of appeal, facts of the case, assessment order passed by the AO, written submission as well as documentary evidences uploaded and judicial decisions relied upon by the appellant. After verification of the Balance Sheet and its annexed statements, it is found that the increase in capitals of the partners was Rs.65,79,04,725/- and not the amount of Rs.70,64,64,644/- as calculated by the assessing officer. The difference amount in the partner’s capital account of Rs.4,85,59,919/- represents the remuneration paid to Sri A. Varun Kumar of Rs.12,00,000/- & Smt. A. Vasantha of Rs.6,00,000/-. The balance amount of Rs.4,67,59,919/- represents the share of profit credited to the partner’s capital account. Thus the net increase in capital by way of introduction was only Rs.65,79,04,725/-. And this amount was stated to be introduced by the partner Sri A. Ravi Kumar. As the total remuneration and share of profit credited to the partner’s capital account of Rs.4,85,59,919/- does not require any supporting documentary evidence for sources and it was generated from the firm’s books of account, the integral part made in the total addition of Rs.68,75,39,255/-. On verifying the Balance Sheet as on 31.03.2022 and its annexed statements, the capital accounts of the partners are found to be as under:-

| Total capital of the partners as on 01.04.2021 | Rs. 3,32,10,611 |

| Capital introduced by Partner Sri A. Ravi Kumar | Rs. 65,79,04,725 |

| Remuneration credited to partners’ capital

account |

Rs. 18,00,000 |

| Share of profit credited to partners’ capital account | Rs. 4,67,59,919 |

| Total Capital of the partners’ as on 31.03.2022 | Rs. 73,96,75,255 |

As seen from the above, the actual increase in the partners’ capital was Rs.65,79,04,725/- not Rs.73,96,75,255/- as calculated by the AO. The difference of Rs.4,85,59,919/- in the partners’ capital account includes remuneration of Rs.12,00,000 paid to Sri A. Varun Kumar and Rs.6,00,000/- to Smt. A. Vasantha. The remaining amount of Rs.4,67,59,919/- represents the share of profit credited to the partners’ capital account. Consequently, the net increase in capital introduced was only Rs.65,79,04,725/- attributed to partner Sri A. Ravi Kumar. Since the total amount of Rs.4,85,59,919/- which includes remuneration and share of profit credited to the partners’ capital account, originates from the firm’s books and does not require external supporting evidence, therefore this amount is excluded from the overall addition of Rs.68,75,39,255/-, Thus, the addition to the capital of partners of the appellant firm representing remuneration & share of profit of Rs.4,85,59,919/- is deleted as it does not constitute as an unexplained cash credit u/s 68 of the Act.

5.6. In respect of the claim of capital introduction by partner Sri A. Ravi Kumar amounting to Rs.65,79,04,725/-, appellant has explained during the assessment proceedings that Mr. A. Ravi Kumar, in the previous year under consideration, sold land jointly with other co-owners to. M/s. Microsoft Corporation Ltd. This sale was made vide Registered Sale Deed No.14652/2021, with a total sale consideration of Rs.158,28,82,500/-. Mr. A. Ravi Kumar’s share in this sale amounted to Rs.127,47,09,413, which was the source for his additional capital introduction into the appellant firm. The appellant firm submitted copies of the registered sale deed and bank statements. AO has not questioned or doubted the transaction’s genuineness during the assessment proceedings. However, AO has identified bank transfer entries by the partner total amounting to Rs.5,21,36,000/- as genuine and noted that the remaining capital introduction amounts were not reflected in the bank account, hence, treated the balance amount as unexplained cash credit under Section 68 of Act.

5.7. From the perusal of documents available on record, it is apparent that Mr. A. Ravi Kumar partner of the firm had transferred funds directly to the accounts of the land owners on behalf of the appellant firm to expedite the transaction in respect of purchase of land. This fact was also brought to the notice of the AO during assessment proceedings in response to the query raised by the AO that partner Sri A. Ravi Kumar made payments totaling Rs.54,10,12,725/- on behalf of the appellant firm to the land vendors, hence, this amount is treated as his capital contribution to the firm. All the remittances stated above have been verified against the bank account statements provided by the appellant firm and it is found that partner Sri A. Ravi Kumar has made a total capital investment of Rs.65,97,14,725/- in the appellant firm during the previous year under consideration, as under:

| Bank transfers to Vendors on behalf of the appellant. | Rs.54,10,12,725 |

| Bank transfers directly to the appellant | Rs.11,87,02,000 |

| Total transfers made by the partner Sri A. Ravi Kumar as his capital | Rs.65,97,14,725 |

Hence, appellant firm has duly explained the source of total remittance made by partner Sri A. Ravi Kumar for his capital introduction during the previous year under consideration during the assessment proceedings as well as appellate proceedings supported by verifiable evidence in the form of copies of registered sale deeds. Therefore, the addition made under Section 68 of the Act as unexplained cash credit amounting to Rs.63,89,79,336/- is not sustainable.

5.8. The primary condition for invoking the provisions of section 68 of the Act is that there is a credit entry in the books of account of the assessee during the year and assessee offers no explanation or if the explanation offered by the assessee is not found satisfactory in the opinion of the AO in respect of identity, credit worthiness and genuineness of that transaction i.e. the credit entry found in the books of the assessee. Hence, assessee has to discharge the primary onus envisaged in section 68 to prove the nature, identity of lender, source of cash deposits i.e. credit worthiness of lender as well as genuineness of transactions in respect of credit entry found in the books of accounts of the assessee. The burden of proof lies upon the assessee to furnish the details/documentary evidences to support its contention and to offer the best possible explanation and after submission of the explanations, the onus cast by virtue of this section is shifted to the department to make rebuttals of the contentions made by the assessee in his explanations offered in the situation of making any adverse opinion in the case of the assessee or if he is not satisfied with the explanation offered by the assessee. In the present case, appellant has successfully discharged the primary onus cast upon by virtue of Section 68 of the Act and demonstrated the nature and source of credit entry found in the books of the appellant firm during the year under consideration, which is actually the capital introduced by the partner in the books of the firm. Further, the source of capital introduced by the partner Sri A. Ravi Kumar was also explained by the appellant during the assessment proceedings that Mr. A. Ravi Kumar, in the previous year under consideration had sold land jointly with other co-owners to M/s. Microsoft Corporation Ltd. This sale was made vide Registered Sale Deed No. 14652/2021, with a total sale consideration of Rs.158,28,82,500/-. Mr. A. Ravi Kumar’s share in this sale amounted to Rs.127,47,09,413/-, which was the source for his additional capital introduction into the appellant firm during the year under consideration. The appellant firm had also submitted copies of the registered sale deed and AO did not question or doubted the genuineness of transaction during the assessment proceedings. Further, in this case the source of funds introduced stands owned and accepted by its partner Sh. A. Ravi Kumar. He is an individual and in such capacity assessed to tax independently. The source of funds from which the partner had advanced the money to the appellant firm by way of capital introduction was from consideration received from sale of land. In such facts and circumstances as far as this appellant Firm is concerned, no adverse view can be taken. Stretching the AO’s reasoning hypothetically to scenario where a person, a partner in such cases, owns/confirms the transaction but the source of his funds is dubious; can an adverse view be taken against the Firm as long as the partner is owning the transaction/money advanced to the Firm? In my view action will still lie against the partner of the Firm and not the Firm. Therefore, without prejudice to the fact of the case discussed in the preceding para, the action of AO in the present case is unsustainable in view of the transaction’s confirmation by the partner.

5.9. In view of the above discussion, AO is directed to delete the addition of Rs.68,75,39,255/- made u/s 68 of the Act and Ground no. 3 of the appeal raised by the appellant on this issue is allowed.”

8.4. The facts as recorded by the learned CIT(A) in the impugned order are not in dispute and nothing has been brought before us by the department to controvert these facts otherwise evident from the record. Accordingly, we do not find any error or illegality in the impugned order of the learned CIT(A).

9. In the result, appeal ITA.No.9/Hyd./2025 of the Revenue is dismissed.

ITA.No.907/Hyd./2025 – A.Y. 2022-2023 [Assessee’s Appeal]

10. Though the assessee has filed a cross-appeal, however, as it is apparent from the impugned order of the learned CIT(A) that there is no grievance of the assessee against the impugned order when the appeal of the assessee was allowed and the addition made by the Assessing Officer was deleted. Therefore, the learned Authorised Representative for the Assessee has submitted that instead of filing the cross objection, the assessee has inadvertently filed the cross appeal, and he has pleaded that the assessee does not want to press the appeal and the same may be dismissed as withdrawn. He has filed an application dated 13.05.2026 for withdrawal of the appeal which reads as under:

Date: 13.05.2026

To :

The Hon’ble Bench,

The Hon’ble Income Tax Appellate Tribunal,

Bench “A”, Hyderabad.

Respected Sir,

Sub: Withdrawal of appeal in the case of Sai Balaji Developers for the Asst. Year 2022-23.

Ref:

1. PAN: ACZFS1334C

2. Assessee Appeal No: ITA 907/Hyd/2025 – “A” Bench.

3. Department Appeal No: 9/Hyd/2025 – “A” Bench.

It is humbly submitted before the Hon’ble ITAT Bench that the case of the Appellant M/s Sai Balaji Developers completed the arguments on 13.05.2026. During the course of hearing the Honorable JM find out that the appeal number ITA 907/Hyd/2025 filed by the appellant is as normal Appeal, not as a Cross objection. It is further submitted that there is no further grievance in the order passed by the Ld. CIT(A), the Appellant has paid the Court fee and filed the appeal inadvertently as normal Appeal instead of cross objections.

In this regard, it submitted that the counsel for the Appellant wishes to withdraw the appeal filed vide ITA No. 907/Hyd/2025. Hence the same maybe considered and dispose of by the Hon’ble Bench.

Thanking you,

Yours Sincerely,

(Signature)

(CA C. Maheshwar Reddy)

Authorized Representative

For the Appellant

11. On the other hand, the learned DR has raised no objection if the appeal of the assessee is dismissed as withdrawn.

12. Accordingly, in view of the facts and circumstances when no grievance of the assessee is raised against the impugned order, the present appeal of the assessee is allowed to be withdrawn and the same is dismissed being withdrawn.

13. In the result, appeal ITA.No.907/Hyd./2025 of the Assessee is dismissed as withdrawn.

14. To sum-up, appeal of the Revenue is dismissed and appeal of the Assessee is dismissed as withdrawn. A copy of this common order is placed in the respective case files.

Order pronounced in the open Court on 03.06.2026

Author Bio