#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

Penalty U/s. 271(1)(c) cannot be imposed for non deduction of TDS

Income Tax

Income Tax

Deduction U/s. 80-IA allowable on amount disallowed U/s. 43B

Income Tax

Income Tax

Exemption u/s. 54 is available even in respect of two house property / flats

Income Tax

Income Tax

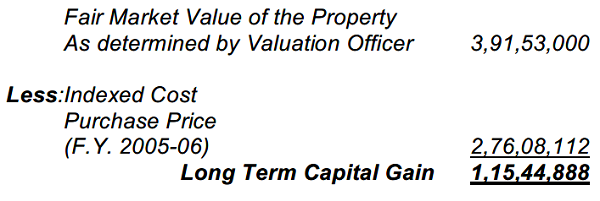

Section 50C not applicable on Right to Purchase a Building

Income Tax

Income Tax

ITAT show follow view favouring assesse in case of Two Conflicting views of Non-Jurisdictional HCs

Income Tax

Income Tax

Cessation of liability U/s. 41(1) cannot be presumed, merely because liability remained unpaid for a period of 3 years

Income Tax

Income Tax

Interest on bank deposits when project is being setup is a capital receipt: POSCO India case

Income Tax

Income Tax

Penalty U/s. 271(1)(c) not sustainable on failure of AO to strike off inappropriate words in show-cause notice U/s. 274

Income Tax

Income Tax

Expense of Corporate Membership of Director is allowable Expenditure

Income Tax

Income Tax