#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

Assessment U/s. 153C in absence of incriminating material is bad in law

Income Tax

Income Tax

Payment for Acquiring Mining Rights is Capital Expenditure

Income Tax

Income Tax

In absence of principal agent relationship section 194H not applicable

Income Tax

Income Tax

Wealth Tax: Non striking irrelevant column in notice issued u/s 18(1)(c) renders notice invalid

Income Tax

Income Tax

JCIT cannot give Approval U/s. 153D in a mechanical way

Income Tax

Income Tax

Income from sale of Agricultural Land after plotting is business Income

Income Tax

Income Tax

Expenditure on issue of FCCB allowable as revenue expense

Income Tax

Income Tax

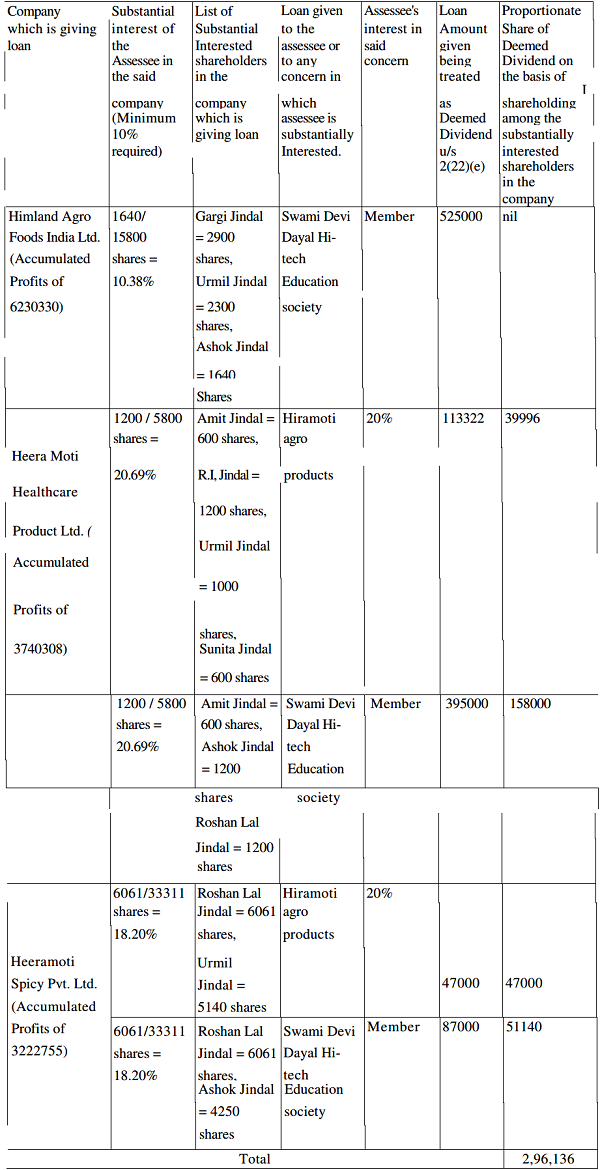

Advance cannot be treated as deemed dividend if Assessee do not have substantial interest

Income Tax

Income Tax

Section 56(2)(vii) HUF can’t be treated as a ‘Donor’ of Gift

Income Tax

Income Tax