#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

45% profit from educational activities establishes profit motive of trust and exemption U/s. 11 cannot be allowed

Income Tax

Income Tax

TDS U/s. 195 not deductible if Commission Income of Foreign Agent not Taxable in India

Income Tax

Income Tax

AO cannot pass assessment order U/s. 143(3) against dissolved Company

Income Tax

Income Tax

Provision of Section 2(22)(e) cannot be attracted to current account transactions

Income Tax

Income Tax

No exemption for one SOP U/s. 23(2)(a) if property was not occupied by the owner

Income Tax

Income Tax

CIT(A) has no power to travel beyond subject-matter of assessment

Income Tax

Income Tax

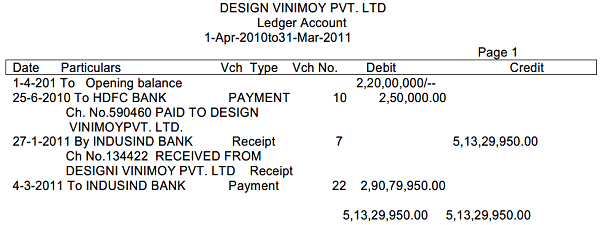

Addition deleted as money deposited in the bank account was received from son

Income Tax

Income Tax

No wealth tax on land used for business purpose by construction / set up of office and service centre

Income Tax

Income Tax

Mere allegation by investigation dept not sufficient to prove Bogus Capital gains from penny stocks

Income Tax

Income Tax