#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

Addition cannot be made just because share premium is abnormally high as per test of human probabilities

Income Tax

Income Tax

Exemption U/s 54F eligible if delay in investment was beyond control of Assessee

Income Tax

Income Tax

Loss on Sale of Shares of Subsidiary Company is a Business Loss

Income Tax

Income Tax

Penalty not leviable for cash loan taken/paid to comply re-settlement scheme of BIFR

Income Tax

Income Tax

Foreign travel expenses by law firm for pleasure tour by counsels & family not allowable

Income Tax

Income Tax

Deduction U/s 80IB not allowable on lease rent of industrial undertaking

Income Tax

Income Tax

No addition can be made for mere non-production of directors of shareholder companies

Income Tax

Income Tax

Reassessment based on usurpation of jurisdiction on non-existing jurisdiction is invalid

Income Tax

Income Tax

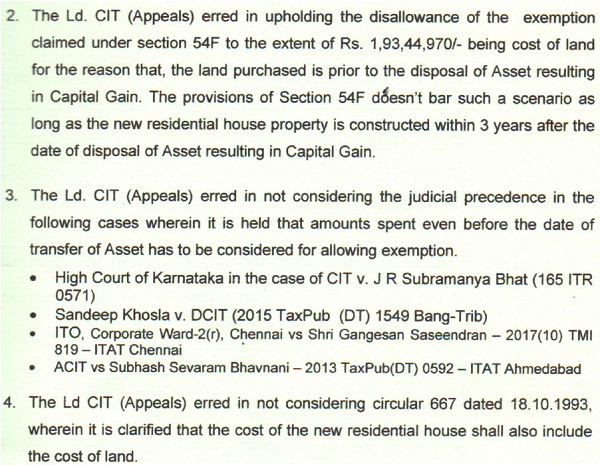

No exemption U/s 54F for purchase of land prior to period of one year from sale of capital asset

Income Tax

Income Tax