Case Law Details

Sterling Holiday Resorts Limited Vs DCIT (ITAT Mumbai)

Conclusion: Disallowance of assessee’s claim was upheld for set-off of brought forward unabsorbed depreciation and carry forward of business losses and unabsorbed depreciation of the demerged company under section 72A(4), holding that failure to satisfy the mandatory condition of issuing shares to the demerged company disentitled the assessee from claiming the statutory benefit. A holding company cannot issue shares on behalf of its subsidiary to satisfy the conditions for claiming tax benefits arising from a demerger.

Held: Assessee claimed the benefit of set-off and carry forward of the brought forward business losses and unabsorbed depreciation of a demerged company under section 72A(4) of the Income-tax Act following a corporate restructuring. AO disallowed the claim on the ground that the statutory conditions prescribed under section 72A(4) were not fulfilled, particularly because the resulting subsidiary company did not issue shares to the demerged company as mandated by law. CIT(A) upheld the disallowance, following which the assessee appealed before the Tribunal. Assessee contended that it was entitled to succeed to the losses and unabsorbed depreciation of the demerged undertaking notwithstanding the manner in which the restructuring was implemented. It argued that the transaction substantially complied with the statutory scheme governing demergers. Revenue submitted that section 72A(4) prescribes mandatory conditions for availing the benefit of carry forward and set-off of losses in a demerger. Since the resulting company had not issued shares to the demerged company, an essential statutory requirement remained unfulfilled. It was further argued that a holding company and its subsidiary were separate legal entities and the holding company could not perform or satisfy statutory obligations on behalf of its subsidiary. Tribunal held that the conditions prescribed under section 72A(4) were mandatory and must be strictly complied with before the benefit of carry forward and set-off of losses and unabsorbed depreciation can be claimed. Since assessee admittedly did not issue shares to the demerged company, the statutory requirement stood violated. Tribunal observed that a holding company and its subsidiary possess distinct legal identities, and the holding company could not discharge obligations that the law specifically casts upon the subsidiary. In the absence of compliance with the statutory conditions, assessee was not entitled to claim the benefit of set-off or carry forward of the demerged company’s losses and unabsorbed depreciation.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

The present appeal preferred by the assessee and cross appeal by the Revenue emanate from the appellate order dated 29.12.2023 passed by the Learned Commissioner of Income-tax (Appeals)/National Faceless Appeal Centre, Delhi [hereinafter referred to as “CIT(A)”] pertaining to the assessment order passed u/s. 143(3) of the Income-tax Act, 1961 [hereinafter referred to as “Act”] dated 27.12.2017 for the Assessment Year [A.Y.] 2015-16.

2. ITA No. 843/MUM/2024

The grounds of appeal are as under:

“1. Ground No.1-General

The Ld. CIT(A) has erred in confirming the actions of the Learned Assessing Officer (Ld. AO’) and sustain the following additions or disallowance made in the impugned assessment order:

a. Disallowance of Prior Period Expenses of Rs. 3,11,55,478/-

b. Disallowance of Employee Stock Option Plan expense aggregating to Rs. 3,19,61,289/-

c. Disallowance of carry forward and set off of accumulated business loss and unabsorbed depreciation aggregating to Rs. 2,40,15,01,124/-

2. Ground No. 2 – Disallowance of Prior Period Expenses of Rs. 3,11,55,478/-

2.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of Ld. AO in disallowing prior period expenses of Rs. 3,11,55,478/-.

2.2. On the facts and in the circumstance of the case and in law, the Ld. CIT(A) erred in not considering the facts and explanation presented by the appellant company in its written submission that the expense incurred by the appellant company was deductible expense under section 36(1) (iii) and 37(1) of the Act.

2.3. Without prejudice to the above, prior period expenses of Rs.3,11,55,478/-should be allowed in the relevant previous year.

3. Ground No. 3-Disallowance of Employee Stock Option Plan expense aggregating to Rs. 3,19,61,289/-

3.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of the Ld. AO in disallowing the employee stock option plan expense of Rs. 3,19,61,289 debited to profit and loss account.

3.2. The Ld. CIT(A) / Ld. AO erred in not in not appreciating that the ESOP discount has been recognized over the vesting period of the ESOP in accordance with the guidelines and accounting principles.

3.3. The Ld. CIT(A) / Ld. AO erred in not following the decision of the Hon’ble Mumbai ITAT dated 20 November 2019 in the appellant company’s own case.

3.4. Further, the Ld. CIT(A) / Ld. AO has erred in not appreciating the fact that the ESOP discount is a part of the remuneration of the employees and the same is wholly and exclusively Incurred for the purpose of the business of the appellant company.

3.5. The Ld. CIT(A) / Ld. AD erred in relying on circular 09/2007 without appreciating that the ESOP granted in the appellant’s case were of the holding company i.e. Thomas Cook (India) Limited.

3.6. On the facts and in the circumstances of the case and in law, the appellant company prays that impugned action of the Ld. AD of disallowance of ESOP expense ought to be deleted.

Ground No. 4- Disallowance of carry forward and set off of accumulated business loss and unabsorbed depreciation aggregating to Rs.2,40,15,01,124/-

4.1. Based on the facts and circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of the Ld. AO of disallowing the set off of brought forward unabsorbed depreciation of Rs.5,19,10,313/- against income of assessment year 2015-16. 2015 Further, the learned AO erred in disallowing carry forward of business loss of Rs.121,66,74,982/- and unabsorbed depreciation of Rs.113,29,15,829/- under section 72A (4) of the Act;

4.2. On the facts and in the circumstance of the case and in law, the Ld. CIT(A) erred in not understanding the facts of the case and appreciating that appellant company (company to which the demerged undertaking has been transferred) as well as its parent (TCIL, CIL, a wholly owned subsidiary of which has received the demerged undertaking) falls within the definition of ‘resulting company’ as per section 2(41A) of the Act.

4.3. Further, the Ld. the Ld. CIT(A)/Ld. AO has erred in not appreciating that condition under section 2(19AA) (iv) of the Act has been complied with as the resulting company TCIL has issued shares to the shareholders of the demerged company.

4.4. The Ld. CIT(A) / Ld. AO also erred in not appreciating that issue of shares by resulting company TCIL results in fulfilment of condition prescribed under clause (v) of section 2(19AA) of the Act which is to be read in conjunction with clause (iv) to the said section.

3. The assessee company formerly known as Thomas Cook Insurance Services India Ltd(‘TCISL’) is engaged in selling vacation home and leisure hospitality services etc. It filed loss return. The AO made certain additions and upheld by the appellate authority which are being contested in the instant appeal.

4. Ground no.1- This ground is general in nature and doesn‘t need any adjudication.

5. In ground no.2, the assessee has disputed the disallowance of Prior period expenses of Rs.3,11,55,478/-. The AO made the disallowance on the reasoning that they did not pertain to the relevant assessment year and also they did not crystallize during the year.In the subsequent appeal, the ld.CIT(A) upheld the addition with the observations that though the main contention of the assessee was that the expenditure were made during the period relevant to AY 2015-16 and therefore, the same should be allowed, it had not produced any document in support of such claim. In absence of the documentary evidence to prove that the expenditure was incurred in AY 2015-16, the same could not be allowed. The assessee was free to claim the expenditure the said year after producing the relevant documents to prove the genuineness and year of expenditure made. The addition made was confirmed.

6. Before us, the ld.AR has furnished the details of such expenses claimed as Prior period expenses as per Paper Book page nos.117-118.It is contended that both the authorities did not appreciate the details filed by the assessee in correct perspective and based on TAR and the ground that the expenses pertaining to earlier years could not be allowed, made the disallowance. In respect of interest in Securitization, it was submitted that the assessee had securitized certain debtors against which interest expenses were incurred which are allowable u/s 36(1)(iii) of the Act. Such expenses were never claimed in the earlier years. In respect of statutory dues falling under the purview of section 43B of the Act, it was submitted that the impugned amounts are allowable once paid during the subsequent year as well. He has also made a request to remand the entire issue for de novo consideration by the AO. The ld.DR did not dispute such proposition though he claimed that the expenses did not crystalize during the relevant year.

7. On careful consideration, we find that both the lower authorities have brushed aside the claim without due application of mind. Accordingly, the addition is set aside with a direction to the AO for due verification and decision. The assessee would also bring on necessary evidence that though the expenses pertained to previous years, they were ascertained and got crystallized during the relevant itself. Therefore, the ground is allowed for statistical purposes.

7. Ground no.3 pertains to the addition of Rs.3,19,61,289/- made by the AO on the expenditure towards Employee Stock Option Plan(ESOP) discount. The assessee contented that the ESOP cost was incurred wholly and exclusively for the purpose of the business. It also quoted decision in case of Biocon Limited Vs DCIT 35(2013) 35 taxman passed by ITAT, Bangalore Bench. The AO on the other hand, relied on the decision of the Hon‘ble Supreme Court in the case of Punjab State Industrial Development Corp Ltd (1997) 225 ITR 792 (SC) and Brooke Bond India ltd (1997) 225 ITR 798 (SC) and inter alia observed that the nature of ESOP was that of issue of shares to employees at a predetermined rate on a discounted rate and there is no specific provision in the Act which provides deduction on the discount given to the employees in ESOP. The ld.CIT(A) held that the assessee had not made out a case for allowing deduction of discount on ESOP as expenditure u/s 37 of the Act. Accordingly, this ground of appeal was dismissed and the addition made by the AO was confirmed.

9. Before us, the ld.AR has claimed that the issue under consideration is no longer res integra and in a plethora of judicial decisions, such claims are consistently being allowed in favour of the assesses. The ld.DR on the other hand relied on the lower authorities.

10. We have carefully considered the relevant facts of the case and we find that the impugned issue has been consistently decided in favour of the taxpayers by the appellate authorities including the coordinate bench of ITAT, Mumbai. The Mumbai ITAT in the case of IPCA Laboratories Ltd 161 com 511 (Mumbai – Trib.), following the decision of Karnataka High Court held that ESOP compensation expenditure incurred by assessee is an allowable deduction under section 37(1)of the Act. The ITAT Hyderabad in the case of Nagarjuna Construction Co. Ltd 159 taxmann.com 538 (Hyd – Trib.) again decided this issue in favour of the assessee by holding that discount on issue of ESOPs i.e., difference between grant price and market price on shares as on date of grant of options was allowable deduction under Section 37(1) of the Act. In the case of Fortune Park Hotels Ltd. 159 taxmann.com 1217 (Delhi),the Delhi ITAT held that ESOP expenses are allowable as per ESOP scheme and further, such expenses had been duly taxed in hands of employees as “perquisites” and included in Form-16 of employees and due TDS was deducted by assessee treating them as salary.

10.1 Therefore, we find that the law on the subject, therefore, is unanimous as various tribunals by following the decision of Biocon Ltd, Karnataka High Court have decided the issue in favour of the assessee. Secondly, we observe that the ESOP scheme under consideration was part of the Annual Report of the assessee and further the specific details of ESOP benefit granted to its employees had been duly disclosed to the AO during the course of assessment proceedings, being the difference between the market price of shares at the time of grant of option to these employees and the market price of such shares as on the date of exercise by employees of the assessee company. Therefore, even from this perspective, the expenses so claimed were not contingent in nature, since the assessee had claimed the ESOP expenses at the time of actual exercise of option by its employees, during the year under consideration. Accordingly, in view of the judicial precedents on the subject as on date, which have consistently taken the view that ESOP expenses are allowable in the hands of assessee under section 37 of the Act and looking into the facts of the assessee’s case, we are of the considered view that both the lower authorities have erred on facts and in law in deciding this issue against of the assessee. Accordingly, we set aside the appellate order and direct the AO to allow the deduction. The ground of the assessee is, therefore, allowed.

11. Ground No. 4 pertains to the disallowance of carry forward and set off of accumulated business loss and unabsorbed depreciation aggregating to Rs.2,40,15,01,124/-by the AO and affirmed by the ld.CIT(A).It is claimed that both the authorities erred in disallowing the set off of brought forward unabsorbed depreciation of Rs.5,19,10,313/- against income of the impugned year. Further, the AO erred in disallowing carry forward of business loss of Rs.121,66,74,982/- and unabsorbed depreciation of Rs.113,29,15,829/- under section 72A (4) of the Act.

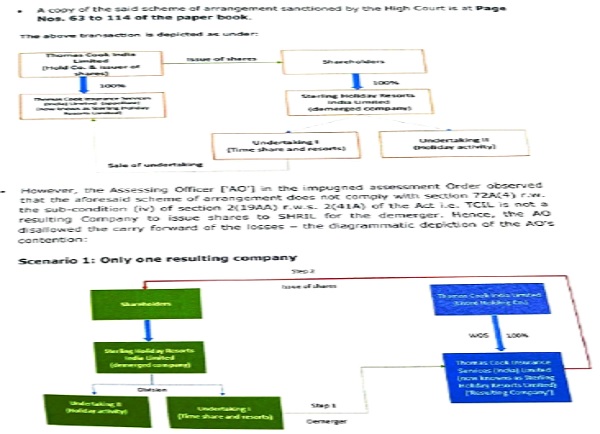

11.1 Facts emanating from the records reveal that in this case, three entities which entered into a court-approved scheme of arrangement, sanctioned by the Hon’ble Bombay High Court involvingi. e. Sterling Holiday Resorts India Ltd. (‘SHRIL’ / ‘Demerged or Transferor Company’) a listed company, Thomas Cook (India) Ltd. (‘TCIL’/’Transferee Company’ / ‘Resulting Company’),a listed Company; and the assessee (formerly known as ‘Thomas Cook Insurance Services Ltd.’) [‘TCISL’ /‘Resulting Company’] wholly owned subsidiary [‘WOS’] of TCIL. The scheme of arrangement involved:(i)demerger of the resorts and time-share undertaking of SHRIL into the assessee company on a Going-concern basis and;(ii)amalgamation of the residual business of SHRIL into TCIL, pursuant to which SHRIL ceased to exist.

12. According to the AO as the shares were allotted by the Holding company of the TCISIL and ‘not by TCISIL‘ or its wholly owned subsidiary, there was violation of the provisions of Sec.2(19AA)(iv) r.w.s 2(41A) of the Act and due to this violation, he disallowed the carry forward and set off of accumulated loss and unabsorbed depreciation. The AO further reasoned that Section 72A of the Act talks only about loss under the head Profits and gains of business or profession and not Long term capital loss and therefore, he disallowed the carry forward of long term capital loss. The assessee contended before the lower authorities that even the shares allotted by the Holding company would also come under the purview of sec.2(19AA) of the Act and would lead to proper compliance of the conditions contained therein. The ld.CIT(A) rejected the contention by observing that the Act is very clear on the conditions which have to be complied with for claiming the carry forward and set off of accumulated loss and unabsorbed depreciation. The assessee had not complied with the conditions as contained in Sec 2(19AA) and 2(41A)of the Act and the demerger scheme of the assessee was not in tandem with the provisions of the Act as provided in Sec 72A(4) and Sec 2(19AA) and 2(41A) of the Act. A clear reading of the provisions would show that the ‘Resulting company‘ is one or more companies to which the undertaking of the demerged company is transferred which includes its subsidiary company and does not include its holding company. Therefore, the Resulting company which was obliged to issue shares as a consideration for the undertaking are the company that had received the undertaking and its wholly owned subsidiary thereof. In the present case, the Resulting company would be TCISIL or its wholly owned subsidiary. As TCISIL or its wholly owned subsidiary had not issued shares to the shareholders of SHRIL, the conditions provided in Sec.2(19AA)(iv) r.w.s 2(41A) of the Act were not fulfilled and hence, the addition made was confirmed.

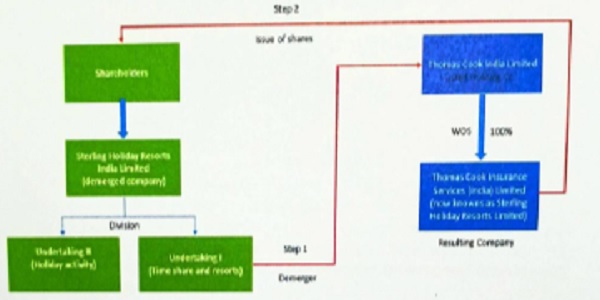

13. Before us, the ld.AR has made detailed argument which was followed with a brief written submission. It is submitted the lower authorities erred in not understanding the facts of the case and appreciating that assessee company to which the demerged undertaking had been transferred as well as its parent i.e. TCIL, a wholly owned subsidiary of which had received the demerged undertaking, falls within the definition of ‘Resulting company’ as per section 2(41A) of the Act. The conditions under section 2(19AA) (iv) of the Act have been complied with as the resulting company TCIL had issued shares to the shareholders of the demerged company. The issue of shares by resulting company TCIL results in fulfilment of condition prescribed under clause (v) of section 2(19AA) of the Act which is to be read in conjunction with clause (iv) to the said section.

13.1 A flow chart of the transactions as entered into amongst the three entities has been reproduced as below:

–

13.2 It was submitted further that the aforesaid restructuring was undertaken to consolidate complementary businesses, ensure focused management, and unlock long-term value. Post-demerger, the assessee company received the demerged undertaking, while TCIL issued shares to the shareholders of SHRIL in accordance with the scheme. It was submitted that the entire issue is just on the interpretation of the word “resulting company” defined under Section 2(41A).Even at the time of approval of the demerger by High Court, this issue was raised but the High Court observed that whether the transaction satisfied the definition of demerger under section 2(19AA) r.w.s. 2(41A) of the Act may be left to be examined by the tax department. Issue under consideration is whether on demerger the shares have to be issued by TCISL or TCIL i.e. who is Resulting company as per section 2(41A) r.w.s 2(19AA) of the Act. It was argued that when the shares upon demerger are being issued by TCIL, it is submitted that the conditions of “demerger” under section 2(19AA) of the Act, including clause (iv), are duly complied with by the assessee. Section 2(19AA) of the Act defines the term ‘demerger’ to mean transfer by a demerged company of its one or more undertakings to any resulting company and enlists certain manners. Reliance in this regard is placed on the following illustrative list of decision(s) wherein the word “any” has been explained. He relied on the decisions of the Hon’ble Supreme Court of India in the case of Shri Balaganesan Metals v/s. M. N. Shanmugham Chetty and Ors. reported in (1987) 2 SCC 707and Shri Illuri Subbayya Chetty & Sons. vs. State of Andhra reported in [1963] 50 ITR 93 (SC)in this regard. It was further pleaded that certain binding principles are directly relevant to the interpretation of sections 2(19AA) and 2(41A) of the Act as held by the hon‘ble Supreme Court i.e. Provisions granting deductions or relief must be construed liberally and in favour of the assessee as held in CIT v/s. Gwalior Rayon Silk Mfg. Co. Ltd. [1992] 196 ITR 149 (SC).Also the provisions granting incentives for economic growth must be interpreted liberally; restrictive conditions must be construed so as to advance, not frustrate, the statutory objective as held in Bajaj Tempo Ltd. v/S. CIT [1992] 196 ITR 188 (SC).It is argued further where a taxing provision is capable of two reasonable constructions, the construction favouring the assessee must be adopted as held in CIT v. Vegetable Products Ltd. [1973] 88 ITR 192 (SC).

13.3 It is argued that sub-section (iv) to section 2(19AA) states that ‘resulting company’ should issue its shares to the shareholders of the demerged company on a proportionate basis in consideration of the demerged undertaking. As per the section 2(41A) expressly defines “resulting company” to include one or more companies, including a wholly owned subsidiary, to which the undertaking is transferred. The issue for consideration now is the meaning of the phrase “one or more companies (including wholly owned subsidiary thereof)”. The inclusion of the phrase “including wholly owned subsidiary thereof” cannot be for the purpose of including the category of wholly owned subsidiaries as a resultant company. The starting phase “one or more companies” would include all companies including a company which is a wholly owned subsidiary of another company or for that matter a company which is a holding company of another subsidiary. It is not necessary to state separately that a wholly owned subsidiary can be a Resultant company. Both the companies can be interchangeably considered as a ‘Resultant Company’. Further, the Act considers a combination of holding company together with subsidiary, interchangeably as a resulting company because the very purpose for providing for demerger is for the reconstruction of business of Companies, into various other companies and the transactions should be cashless and the shareholders of the demerged company should be allotted shares in a company which will take into account the value of the demerged undertaking. Such cases would be considered as a valid demerger u/s 2(19AA) read with section 2(41).

13.4 It further pleaded that from the perusal of definition of the Resultant Company u/s. 2(41A) of the Act , it would not matter whether an undertaking is transferred to the Holding Company or its wholly owned subsidiary and also which company allots shares on account of demerger, because either company would fall within the definition of Resultant company. If section 2(19AA) has to be interpreted as to mean that only the company to which the undertaking was demerged should allot shares, then the bracketed phrase ‘(including a wholly owned subsidiary thereof)’ in the definition of ‘Resultant Company’ under Section 2(41A) would become wholly redundant and purposeless. An interpretation that renders a part of the statute redundant must therefore be rejected in favour of an interpretation that gives the bracketed phrase a distinct and operative meaning. Applying this principle, the bracketed phrase “including a wholly owned subsidiary thereof” in section 2(41A) must be given independent operative content, which it can only acquire under the Appellant’s construction. If the undertaking is to be transferred to holding company whereas the shares were to be allotted by the wholly owned subsidiary, then it would defeat the purpose of demerger since the wholly owned subsidiary will cease to be the wholly owned subsidiary of the holding company due to this allotment; and the shares of the subsidiary company allotted to the shareholders of the demerged company could not reflect and include the value of the transferred undertaking, inasmuch as the undertaking was transferred to the holding company. Therefore, the transaction between SHRIL and TCISL should be considered as a valid demerger and hence, TCISL can claim the carried forward of the losses of the demerged undertaking under section 72A(4) of the Act. In view of the above, the demerger into the Appellant and the discharge of consideration by issuing of shares of TCIL is in compliance with the provisions of 2(19AA) r.w.s. 2(41A) of the Act i, e. in case of more than one resulting company, the conditions to section 2(19AA) is complied with even if either of the resulting company discharges consideration.

14. The ld.DR on the other hand relied on the order of the lower authorities contending that the claim of the assessee is not in accordance with the express provisions of law.

15. We have carefully considered the facts of the case, rival submission. In the case before us, the only issue is whether the assessee company has complied with the requirements of section 2(19AA) and 2(41A) or not while demerged company merged into it, being a Resultant Company. The Department has gone by the strict meaning of the provisions laid therein which inter alia provider that the Resultant company is required to issue shares to the shareholders of the merged company while the assesses contention is that even when the holding company i.e. TCIL issued such shares, there was sufficient compliance making the assessee company eligible for the set of brought forward business losses and unabsorbed depreciation.

15.1 Before proceeding further in the matter, it would be important to examine the provisions of the Act relating to the matter in hand. Section 2(19AA) defines the term Demerger. According to this section:

- A demerger refers to the transfer of an undertaking, unit, or business division from one company (the demerged company) to another company (the resulting company).

- Such a transfer must be pursuant to a scheme of arrangement under the Companies Act, 2013.

- The shareholders of the demerged company must receive shares in the resulting company in the same proportion as their existing holdings.

- The transfer should be on a going concern basis (i.e., the business continues to operate).

15.2 This provision ensures that a transfer of an undertaking from one company to another as part of a genuine restructuring process is not considered a taxable event. “The section lays down certain important conditions:

1. Tax Neutrality – The transfer of assets & liabilities during demerger does not attract immediate capital gains tax.

2. Shareholder Continuity – Shareholders of the demerged company must get shares in the resulting company in proportion to their holdings.

3. All Assets & Liabilities Transfer – The entire undertaking, including assets, debts, and obligations, must be transferred to the resulting company.

4. Resulting Company – The company receiving the undertaking must be an Indian company.

15.3 As per clause (iv) section 2(19AA)(iv) in the Act, the resulting company issues, in consideration of the demerger, its shares to the shareholders of the demerged company on a proportionate basis except where the resulting company itself is a shareholder of the demerged company.

15.4 Section 2(41A) the Act provides for the meaning of ‘Resulting company‘ as below:

2(41A)”resulting company” means one or more companies (including a wholly owned subsidiary thereof) to which the undertaking of the demerged company is transferred in a demerger and, the resulting company in consideration of such transfer of undertaking, issues shares to the shareholders of the demerged company and includes any authority or body or local authority or public sector company or a company established, constituted or formed as a result of demerger.

15.5 The term ‘resulting company‘ finds significance from the term ‘demerger‘ which is defined u/s 2(19AA) of the Act, wherein one of the conditions for tax neutrality of demerger stipulates that the resulting company must issue its shares to the shareholders of the demerged company, in consideration of the demerger scheme. Accordingly, as per Section 2(41A) of the Act, unless the context otherwise requires, the term ―resulting company‖ means one or more companies (including a wholly owned subsidiary thereof) to which the undertaking of the demerged company is transferred in a demerger and, the resulting company in consideration of such transfer of undertaking, issues shares to the shareholders of the demerged company and includes any authority or body or local authority or public sector company or a company established, constituted or formed as a result of demerger.

15.6 Therefore, the Act inter alia provides that a demerger must satisfy all the conditions: i. All the properties and liabilities of the undertaking being transferred by the demerged company, immediately before the demerger, become the property or liability of the resulting company by virtue of the demerger. ii. The properties and liabilities must be transferred at their book value immediately before the demerger (excluding increase in value due to revaluation). iii. In consideration of the demerger, the resulting company must issue its shares to the shareholders of the demerged company on a proportionate basis (except where the resulting company itself is a shareholder of the demerged company).iv. Shareholders holding at least 3/4th in value of shares in the demerged company become shareholders of the resulting company by virtue of the demerger. Shares in the demerged company already held by the resulting company or its nominee or subsidiary are not considered in calculating 3/4th in value. v. The transfer of the undertaking must be on a ‘going concern‘ basis. vi. The demerger must be in accordance with additional conditions, if any, as notified by the Central Government under Section 72A (5) of the Act. It is only when a demerger satisfies all the above conditions, that it will be considered a ‘demerger‘ for purposes of the Act.

15.7 Section 72A of the Act lays down the provisions relating to carry forward and set off of accumulated loss and unabsorbed depreciation allowance in amalgamation or demerger as under:

(1) Where there has been an amalgamation of—(a)a company owning an industrial undertaking or a ship or a hotel with another company; or(b)a banking company referred to in clause (c) of section 5 of the Banking Regulation Act, 1949 (10 of 1949) with a specified bank; or(c)one or more public sector company or companies with one or more public sector company or companies; or(d)an erstwhile public sector company with one or more company or companies, if the share purchase agreement entered into under strategic disinvestment restricted immediate amalgamation of the said public sector company and the amalgamation is carried out within five years from the end of the previous year in which the restriction on amalgamation in the share purchase agreement ends,]then, notwithstanding anything contained in any other provision of this Act, the accumulated loss and the unabsorbed depreciation of the amalgamating company shall be deemed to be the loss or, as the case may be, allowance for unabsorbed depreciation of the amalgamated company for the previous year in which the amalgamation was effected, and other provisions of this Act relating to set off and carry forward of loss and allowance for depreciation shall apply accordingly:[Provided that the accumulated loss and the unabsorbed depreciation of the amalgamating company, in case of an amalgamation referred to in clause (d), which is deemed to be the loss or, as the case may be, the allowance for unabsorbed depreciation of the amalgamated company, shall not be more than the accumulated loss and unabsorbed depreciation of the public sector company as on the date on which the public sector company ceases to be a public sector company as a result of strategic disinvestment.

15.8 Therefore, section 72A(4) of the Act provides that in case of a demerger, the accumulated losses and unabsorbed depreciation directly relatable to the undertaking that is being transferred under the demerger, shall be allowed to be carried forward in the hands of the resulting company. If the loss or unabsorbed depreciation cannot be directly attributed to the said undertaking, the same shall be apportioned between the demerged and resulting company in the same ratio in which the assets of the undertaking have been retained by the demerging company and transferred to the resulting company and shall be allowed to be carried forward and set off in the hands of the demerged company and the resulting company, as the case may be. Also, the accumulated losses and unabsorbed depreciation in case of demerger are available irrespective of whether an industrial undertaking is owned by the demerging company or not.

15.9 In the light of above provisions, the matter in hand is required to be adjudicated. While the claim of the Department is that the being no ambiguity in the aforesaid provisions, it was incumbent on the assessee company to satisfy the requirement of Demerger and Resulting company as it did not issue any corresponding shares to the shareholders of the demerged company i.e. Sterling Holiday Resorts India Ltd. (‘SHRIL’).On the other hand, the assessee has claimed that even transfer of shares by the Holding company would be sufficient compliance. We note that the ld.AR apart from harping on such a preposition has not been able to support his contentions from the plain reading and interpretations of the provisions which to our mind also is unambiguously worded leaving no room for any other interepretation. The contention is also not supported by any judicial precedent ruling of higher courts of law as none have been cited or relied upon. The mere claim that there can be two interpretations possible has no substance at all. Accepting his arguments would amount to a different interpretation altogether and against the rationale behind introduction of such provisions by the legislature. His reliance on the cited decision in the case of Vegetable Products and other cited decisions of hon‘ble Supreme Court on liberal interpretation of the Act is misplaced and not relevant to the facts of the case.

15.10 It is a settled law that the taxation statutes need to be interpreted strictly going by its literal meaning. In the case of Commnr. Of Customs (Import), Mumbai vs M/S. Dilip Kumar and Company dated 30 July, 2018 in AIR 2018 SUPREME COURT 3606, 2018 (5) ABR 802, AIRONLINE 2018 SC 73, the hon’ble Apex reiterated this principle by observing strict interpretation of a statute certainly involves literal or plain meaning test. The other tools of interpretation, namely contextual that or purposive interpretation cannot be applied nor any resort be made to look to other supporting material, especially in taxation statutes. Indeed, it is well settled that in a taxation statute, there is no room for any intendment; that regard must be had to the clear meaning of the words and that the matter should be governed wholly by the language of the notification. Equity has no place in interpretation of a tax statute. Strictly one has to look to the language used and there is no room for searching intendment nor drawing any presumption. Furthermore, nothing has to be read into nor should anything be implied other than essential inferences while considering a taxation statute.

15.11 In the ruling while deciding civil appeals filed by the Director of Income Tax (IT)-I, Mumbai, concerning the interpretation of Section 44C of the Act, the respondents being M/s American Express Bank Ltd and M/s Oman International Bank dated 06.02.2026, the hon‘ble Supreme Court has reiterated that taxation statutes must be interpreted strictly and that where the statutory language is plain and unambiguous, courts are bound to give effect to its plain meaning. A Bench of Justices J. B. Pardiwala and K. V. Vishwanathan observed that it is impermissible for courts to add or read words into a statute on the assumption that such additions may better advance legislative intent, particularly when the language used by Parliament is clear.

15.12 Similarly, in the case of Britania Industries Ltd. vs. CIT (2005) 278 ITR 546-547 (SC)it was reiterated that when the language of a statute is clear and unambiguous, the courts are to interpret the same in its literal sense and not to give a meaning which would cause violence to the provisions of the statute.

15.13 It is a well settled principle of law that the court cannot read anything into a statutory provision or a stipulated condition which is plain and unambiguous. A statute is an edict of the Legislature. The language employed in a statute is the determinative factor of legislative intention. While interpreting a provision the court only interprets the law and cannot legislate it. If a provision of law is misused and subjected to the abuse of process of law, it is for the Legislature to amend, modify or repeal it, if deemed necessary. Legislative casus omissus cannot be supplied by judicial interpretative process. A casus omissus ought not to be created by interpretation, save in some case of strong necessity‖ as held in Union of India vs. Dharmendra Textiles Processors and Others (2008) 306 ITR 277 (SC). If the construction of a statutory provision on its plain reading leads to a clear meaning, such a construction has to be adopted without any external aid as held in CIT vs. Rajasthan Financial Corporation (2007) 295 ITR 195 (Raj F.B.).

15.14 In Ajmera Housing Corporation and Another vs. CIT (2010) 326 ITR 642 (SC), it was held that the taxing statute is to be construed strictly : in a taxing statute one has to look merely at what is said in the relevant provision. There is no presumption as to a tax. Nothing is to be read in, nothing is to be implied. There is no room for any intendment. There is no equity about a tax. In interpreting a taxing statute the court must look squarely at the words of the statute and interpret them.

15.15 In State of Jharkhand v. Ambay Cements (2005) 1 SCC 368, it was held as follows:

(a) Provision of exemption should be strictly construed. It is not open to Court to ignore the conditions prescribed in the exemption notification; (b) Mandatory rule must be strictly followed, while substantial compliance might suffice in a directory rule; (c) Whenever the statute prescribed that a particular act is to be done in a particular manner and also lays down that failure to comply with the said requirement leads to severe consequences, such requirement is mandatory;(d) It is the cardinal rule of the interpretation that where a statute provides that a particular thing should be done, it should be done in the manner prescribed and not in any other way; and (e) Where a statute is penal in character, it must be strictly construed and followed.‖

16. Considering the above discussion and in the light of the cited decisions, we are of the considered opinion that there being no ambiguity in the aforesaid provisions and in the absence of any other interpretation by any court of law, there is absolutely no basis for any other interpretation. The fact remains that in this case, the assessee did not issue shares to the demerged company, thus failing to satisfy the conditions laid therein. There is no dispute that there is substantial difference between a Holding company and a subsidiary thereof having their own independent legal existence vested with relevant rules and regulations. The Holding company cannot issue shares on behalf of the subsidiary and its obligations are restricted to its own legal liabilities and obligation under the law. Therefore, the ld.CIT(A) was justified in confirming the action of the AO of disallowing the set off of brought forward unabsorbed depreciation of Rs.5,19,10,313/- against income of assessment year 2015-16 and also in disallowing carry forward of business loss of Rs.121,66,74,982/- and unabsorbed depreciation of Rs.113,29,15,829/- under section 72A (4) of the Act. Therefore, we find no infirmity in the conclusion drawn by the lower authorities in denying the assessee, the benefit of set of carry forward losses and depreciation of the demerged company. Accordingly, the above ground is dismissed.

17. In the result, appeal of the assessee is partly allowed.

18. ITA No. 843/MUM/2024

“The ld.CIT erred in holding that 40% of of income is to be deferred for 33 year when there is no such concept of Deferred income in the Act.

He erred in concluding that 40% of receipts did not accrue to the assessee during the year ignoring that the fact that there is no provision for refund of even part of the collection.

He erred in holding that 40% is to be deferred for maintenance of property in future years when assessing is collecting Annual Maintenance Charges separate from all the members for each year and whether the order of Tribunal is perverse over the years.

He is not correct in allowing the claim relying on AS-9 even when such Accounting standards stipulated for recognition of income when the sale take place”

19. The assessee has disputed the addition of Rs.44,69,42,000/- made on account of Deferred income. It was submitted that as per the method of accounting regularly followed by it, the income was recognised in part basis and was distributed over the period of entitlement. The assessee heavily relied on the favourable order passed by the ITAT in its own case for several assessment years. The AO has not considered the order of the ITAT by stating that the appeal of the revenue is pending before Hon‘ble High Court, Madras. The ld.CIT(A) observed that the order of the ITAT will remain valid till the same is overturned by a higher court or its operation is stayed by a higher court. In the case, there was nothing on the record which can show that the said decision of ITAT was overturned or stayed by a higher court. Therefore, following the judgement of the ITAT the ground of the appeal was allowed and the addition made on deferred income deleted.

20. The ld. AR has relied on the appellate order while the ld.DR did not controvert such facts. Accordingly, we do not find any infirmity in the appellate order which is therefore upheld and the ground of appeal of the Revenue is dismissed.

21. In the result, appeal of the Revenue is dismissed.

22. In the final summing up, the appeal filed by the assessee is partly allowed while the Cross appeal of the Revenue is dismissed.

Order pronounced in the open court on 25/06/2026.