UNION BUDGET 2018 – AN ANALYSIS OF PROPOSED CHANGES IN PROVISIONS RELATING TO TAXATION OF LONG TERM CAPITAL GAIN ON EQUITY SHARES ETC.

UNION BUDGET 2018 – AN ANALYSIS OF PROPOSED CHANGES IN PROVISIONS RELATING TO TAXATION OF LONG TERM CAPITAL GAIN ON EQUITY SHARES ETC.

INTRODUCTION : Presently, the long term capital gain on sale / other transfers of (a) equity shares in a company (b) unit of an equity oriented fund and (c) a unit of business trust (where such transaction is chargeable to securities transaction tax) is completely exempt from tax under section 10(38) of the Income Tax Act, 1961.

The Finance Bill, 2018 has proposed a new regime for taxation of above gain wherein the above exemption under section 10(38) is to be withdrawn and a new section 112A is to be introduced for taxing the above gains.

POSITION OF TAX ON LONG TERM CAPITAL GAIN UP TO 31ST MARCH, 2018 : These amendments are proposed to be applicable w.e.f. 1st April, 2019 i.e., to the Assessment Year 2019-20 and subsequent assessment years. Therefore, any such gain on sale / other transfer up to 31st March, 2018 shall be still exempt under section 10(38). Only the gains earned on sale etc. made from 1st April, 2018 and onwards shall be subject to taxation under the new regime.

POSITION OF TAX ON LONG TERM CAPITAL GAIN AFTER 31ST MARCH, 2018 : After 31st March, 2018 there may be two type of such gains i.e., firstly, those which will be taxable under new section 112A and secondly, those which will not be eligible for being taxed under section 112A and as such will be taxable under other sections i.e., under an existing section 112 (general section for taxing long term capital gains applicable to resident individuals & HUFs, domestic companies, other residents, non-resident (not being a company) and a foreign company ) / under other sections applicable in specific cases.

The gains covered under section 112A shall be taxable at the concessional rate with threshold limit. In case of individuals and HUFs (only resident), the benefit of unutilized basic tax exemption limit shall also be available. Further, the Long Term Capital gains which will be realized in future, on existing holding (i.e., shares etc. acquired up to 31st January, 2018) to the extent of fair market value as on 31st January, 2018 shall also not be chargeable to tax even if the shares etc. are sold etc. after 31st March, 2018. Thus, to some extent, the benefit of section 10(38) shall also be available indirectly in respect of LT capital gains on existing holdings realized in future(termed as benefit of “grandfathering” ).

All other such LTCG on sale etc. of shares etc. that will not be eligible for benefit of section 112A will be taxable under existing section 112 at the rate of 20% (with indexation benefit) (in some cases restricted to 10% of gain without indexation) / under other applicable sections. In case of resident individuals and HUFs the benefit of unutilized basic tax exemption limit e.g., shall also be available in such cases.

THRESHOLD LIMIT OF LONG TERM CAPITAL GAIN EXEMPTION UNDER NEW REGIME : The threshold limit of Rs. 1 lakhs in a year shall be available only in respect of gains chargeable under section 112A e.g., If a gain in a year is Rs. 1,20,000/- than tax will be payable only on the amount of Rs. 20,000/-. No such threshold limit is available in respect of gains chargeable under existing section 112.

TAX RATE ON LONG TERM CAPITAL GAIN UNDER NEW REGIME : The LTCG covered under section 112A shall be taxed at a concessional rate of 10% (as against general tax rate of 20% under section 112 -restricted to 10% of gain without indexation in some cases).

TYPE OF ASSESSEE TO WHOM NEW REGIME IS APPLICABLE: It is applicable to all type of assesses e.g., individual, HUF, Firm, Company etc.

CONDITIONS FOR APPLICABILITY OF SECTION 112A : The benefit of section 112A shall be available only if Securities Transaction Tax has been paid (a) in respect of equity shares, both on acquisition and transfer thereof ; and (b) in respect of units of equity oriented fund, on transfer thereof ; and (c) in respect of a unit of a business trust, on transfer thereof.

It is important to note here that for eligibility for exemption under section 10(38) in respect of equity shares, the payment of STT was necessary only in respect of sale of shares whereas for claiming benefit of concessional rate of tax in respect of shares the payment of STT both on acquisition and transfer is a necessary condition. However, the compulsion of payment of STT on acquisition is not there in respect of units of equity oriented funds and of a business trust.

IMPORTANT ISSUE : In cases where the shares have been acquired without payment of STT (e.g., old shares when there was no STT at the time of purchase etc.) the biggest benefit of Section 112A i.e., no taxing of long term capital gain up to the extent of fair market value up to 31st January, 2018 may not be available and the gain may be taxable under other section 112 etc.

NO INDEXATION BENEFIT UNDER SECTION 112A: The benefit of indexation as provided under second proviso of section 48 is not available in respect of gains chargeable under section 112A. However, such benefit will be available in respect of other such gains chargeable under section 112 @ 20%. Similarly, benefit of computation of capital gain in foreign as prescribed in first proviso of section 48 shall also not be available in respect of gains chargeable under section 112A.

NO DEDUCTION UNDER CHAPTER VI-A & REBATE UNDER SECTION 87A: The deduction under chapter VI-A as well as rebate under section 87A are not available in respect of gains chargeable under section 112A as well as under existing section 112.

AVAILABILITY OF UNUTILIZED BASIC TAX EXEMPTION LIMIT: The same is available in the case of individuals and HUFs (only resident) in respect of the gains chargeable under both the section 112A and 112.

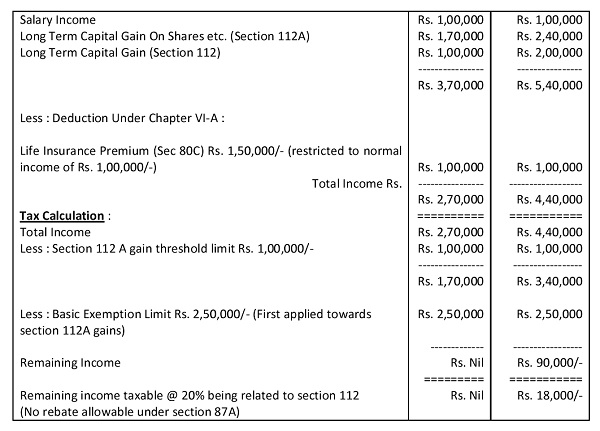

AVAILABILITY OF UNUTILIZED BASIC EXEMPTION LIMIT FIRSTLY IN RESPECT OF SECTION 112A OR 112: The benefit of unutilized normal tax exemption limit for resident individuals and HUFs is available in respect of income taxable under both section 112A and 112. There is no specific mention of this fact that whether the benefit will be firstly available in respect of section 112 or 112A. If the assessee has both type of gains i.e., taxable under section 112 as well as section 112A then the availability of benefit towards gain related to section 112 gain will give benefit of 20% whereas in respect of gain related to section 112A it will give benefit of only 10%. However, the author is of the opinion that the benefit may be firstly applicable towards gain related to section 112A because the provisions of section 112A starts with the wordings “notwithstanding anything contained in the section 112”. Thus, in this regard the position may be favorable to revenue.

HYPOTHETICAL EXAMPLE : The above provisions are explained with the help of hypothetical example :

MANNER OF CALCULATION OF LTCG UNDER SECTION 112A :

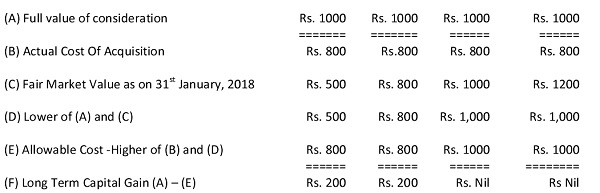

(a) In respect of shares etc. acquired after 31.01.2018 : – The LT capital gain shall be computed by deducting cost of acquisition from the full value of consideration.

(b) In respect of Existing Holding i.e., shares etc. acquired up to 31.01.2018 : – The LT capital gain shall be computed by deducting from full value of consideration the higher of the :-

(i) actual cost of acquisition ; and

(ii) lower of :-

(a) fair market value ; and

(b) full value of consideration.

HYPOTHETICAL EXAMPLE : The above provisions are explained with the help of hypothetical example :

Thus, it is clear from the above example that in respect of the existing holdings, only the gain arising due to the sale price over fair market value as on 31st January, 2018 will be chargeable to tax under section 112A.

HOW TO DETERMINE FAIR MARKET VALUE OF EXISTING HOLDING : The following shall be taken as fair market value –

(a) Where the capital asset is listed on any recognized stock exchange :- The highest price thereof as quoted on such exchange on the 31st day of January, 2018 ;

(b) Where there is no trading in such asset on such exchange on 31st day of January, 2018 :- The highest price of such asset on such exchange on a date immediately preceding the 31st day of January, 2018 when such asset was traded on such exchange ;

(c) Where the capital asset is a unit and is not listed on a recognised stock exchange :- The net asset value of such asset as on the 31st day of January, 2018;

TDS ON LONG TERM CAPITAL GAIN TAXABLE UNDER SECTION 112A : According to Point No. II. Rates for deduction of income-tax at source during the financial year 2018-19 from certain incomes other than “Salaries” in Part A.-“Rates of Income Tax” in section “Direct Taxes” of the budget memorandum and also in the Finance Bill, it is mentioned that in case of long-term capital gain referred to in section 112A of the Act, tax shall now be deducted at source at the rate of 10 per cent.

OTHER CONSIDERABLE POINTS : (a) With introduction of tax on LTCG, the Securities Transaction Tax has not been abolished or reduced . (b) There is no change in provisions relating to the Short Term Capital Gains on shares. They will be taxable at the present rate of 15% (on meeting conditions otherwise will be taxable at the general rate applicable to the assessee). (c) The major impact of non eligibility for section 112A will be that the benefit of grandfathering will not be available in all such cases. Similarly, the benefit of threshold limit of Rs. 1,00,000/- will not be available in such cases. However, the impact of taxability of higher rate of 20% may not be there in all cases as in many cases the tax payable will be restricted to the 10% of gain without indexation (which is equivalent to the mode of calculation of tax under section 112A also). (d) The amendment is also made in section 115AD to provide that such long term capital gain in excess of Rs. 1 lakh are also taxable @ 10% in the hands of Foreign Institutional Investors.

Author Bio

Hi,

I got some shares from my previous company(it’s US based company). If i sell them how much tax i need to pay for it.

Information provided by you was worth reading.

I got a complete understanding of the amended LTCG in finance act 2018

Who will deduct Tds and in which section?

Thanks sir for your sharing