I. Setting the Context: Why This Development Matters

On February 21, 2026, the Goods and Services Tax Network activated a long-awaited facility on the GST Portal, allowing taxpayers registered under Rule 14A of the Central Goods and Services Tax Rules, 2017 to formally opt out of that registration category. The mechanism operates through Form GST REG-32 — a new form that brings the exit process for Rule 14A registrants into a structured, portal-driven framework.

To appreciate the significance of this update, one must look at the origins of Rule 14A. The rule was introduced through Notification No. 18/2025-Central Tax dated October 31, 2025, and became operative from November 1, 2025. Its purpose was straightforward: to extend a simplified Aadhaar-authenticated registration route to small suppliers who predominantly cater to registered businesses, and whose monthly output tax liability on such supplies remains within Rs. 2,50,000.

Having provided a convenient entry path under Rule 14A, the GSTN has now followed through with a correspondingly structured exit path by completing what may be described as the full registration lifecycle management for this category of taxpayers.

II. Understanding Rule 14A: A Brief Recap

Before examining the withdrawal process, it is worth recapping the core features of Rule 14A, since an understanding of the entry conditions directly informs the exit conditions.

- Eligibility Threshold: Only those applicants whose total monthly output tax liability spanning Central Tax, State/UT Tax, Integrated Tax and Compensation Cess on supplies made to registered persons does not exceed Rs. 2,50,000 qualify for registration under this rule.

- Aadhaar as a Gateway: Registration under Rule 14A is permissible only for those who have successfully authenticated their Aadhaar. Persons who have opted out of Aadhaar authentication are ineligible for this route.

- One-State, One-PAN & One Registration: A taxpayer cannot hold two Rule 14A registrations within the same State or Union Territory against the same Permanent Account Number.

- Expedited Registration: The portal grants registration electronically within three working days of a successful Aadhaar authentication significantly faster than the standard seven-working-day window under Rule 9. Practically, many applicants have got registration on the very same day of submitting application.

| Author’s Commentary — Who Actually Uses Rule 14A?

In practice, Rule 14A is best suited for job workers, small manufacturers supplying to large original equipment manufacturers, and professional service providers whose clientele is predominantly GST-registered. The Rs. 2.5 lakh per month cap translates to an annual outward liability of approximately Rs. 30 lakh. Businesses that experience seasonal spikes such as those in the textile or agro-processing sector may find themselves periodically exceeding this threshold and will need to evaluate whether Rule 14A registration remains appropriate. This makes familiarity with the exit procedure especially critical for such taxpayers and their advisors. |

III. Who Is Eligible to Apply for Withdrawal?

Not every registered person can file Form GST REG-32. The facility is restricted to a well-defined category, and the portal itself enforces this restriction by making the navigation link visible only to eligible taxpayers. The conditions are:

- Active Registration Status: The taxpayer must hold an active GSTIN at the time of filing. Suspended or cancelled registrations are outside the scope of this facility.

- Registration Specifically Under Rule 14A: Only taxpayers who entered the GST framework through the Rule 14A route and not through the standard Rule 8/Rule 9 mechanism are eligible. The portal navigation path for this application will not appear for other registrants.

- No Active Cancellation Proceedings: The proper officer must not have initiated proceedings for cancellation of registration under Section 29 of the CGST Act against the applicant. The rule further provides that even if cancellation proceedings commence after the filing of REG-32 but before its disposal, the withdrawal application shall be rejected.

- Amendment Pre-condition: If any particulars in the original Form GST REG-01 have changed, the taxpayer must first carry out the amendment under Rule 19 before filing the withdrawal application.

| Author’s Commentary — The Cancellation Proceedings Bar — A Critical Watch-Point

Sub-rule (13) of Rule 14A introduces an important restriction: if the proper officer initiates cancellation proceedings after REG-32 has been filed, the withdrawal application shall be rejected — and crucially, the deemed approval provision under Rule 9(5) will not apply. This is a significant departure from the usual safeguard that protects taxpayers against administrative delay. In the author’s assessment, this provision is designed to prevent taxpayers from using the withdrawal route as a tactical manoeuvre to pre-empt enforcement action. Advisors should check whether any show-cause notice for cancellation has been issued or is likely before recommending the REG-32 route. |

IV. Return Filing Pre-Conditions: The Non-Negotiable Gateway

The law treats return compliance as a foundational pre-condition to filing REG-32. A taxpayer who has pending returns cannot access this facility. The specific requirements vary based on when the application is filed:

| Timing of Application | Minimum Return Filing Requirement |

| Filed before April 1, 2026 | Returns for a minimum of three consecutive months must be furnished |

| Filed on or after April 1, 2026 | Returns for a minimum of one complete tax period must be furnished |

| Applicable in all cases | Every return due from the effective date of Rule 14A registration up to the date of filing REG-32 must be cleared without any pendency |

The three-pronged compliance check i.e. minimum period requirement, period-specific minimum, and a clean slate from the date of registration ensures that the withdrawal mechanism cannot be misused to avoid retrospective return obligations.

| ✎ Author’s Commentary — The April 2026 Inflection Point — Transitional Relief or Long-Term Design?

The differential threshold i.e. three months before April 1, 2026 versus one tax period thereafter — raises an interesting interpretive question. Is this a transitional concession for early filers, acknowledging that Rule 14A registrations are still relatively new, or is the one-period requirement intended to become the permanent standard? The author’s reading of the provision suggests this is likely a transitional design: early applicants are expected to demonstrate a slightly longer compliance track record given the novelty of the rule, while the post-April 2026 standard eases the requirement once the rule has had adequate time to bed in. Taxpayers who are on the threshold of filing should consider whether deferring to post-April 2026 would reduce their return compliance burden, while being mindful that any deferral must not result in continued non-compliance with the Rs. 2.5 lakh output tax cap. |

V. Step-by-Step Application Process on the GST Portal

The entire withdrawal application process is digital. Taxpayers should follow these steps after logging into the GST Portal:

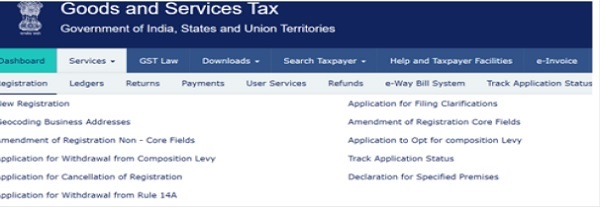

| Step 1 | Navigate to: Services → Registration → Application for Withdrawal from Rule 14A. This link will only appear for eligible Rule 14A registrants. |

| Step 2 | The field ‘Option for registration under Rule 14A’ will default to ‘No’. No change is required here. |

| Step 3 | Enter a clear, factually accurate reason for withdrawal in the designated field. Avoid vague entries — the proper officer will rely on this while verifying the application. |

| Step 4 | Proceed to the Aadhaar Authentication tab and complete the authentication for the prescribed persons. |

| Step 5 | Submit the application. An Application Reference Number (ARN) will be generated only upon successful authentication. |

| Author’s Commentary — Drafting the Reason for Withdrawal — More Important Than It Appears

The ‘reason for withdrawal’ field in the application form deserves more attention than most applicants give it. Under Rule 14A(9), the proper officer is required to verify the application in accordance with Rule 9, which involves examining the application on merits. A vague or inadequate reason such as simply stating ‘business requirements’ may invite unnecessary queries or delays. In the author’s recommendation, the reason should briefly mention the factual trigger: for instance, whether output tax liability has grown beyond the Rs. 2.5 lakh threshold, or whether the business model has changed to include supplies to unregistered persons. A well-articulated reason not only speeds up approval but also creates a defensible record. |

VI. Aadhaar Authentication: The Mandatory Verification Gateway

Authentication of Aadhaar is not an optional step in the withdrawal process. It is a hard prerequisite for ARN generation. The portal determines the mode of authentication based on data analysis and risk profiling:

- OTP-Based Authentication: A one-time password is sent to the mobile number registered with Aadhaar. This is the standard mode for most applicants.

- Biometric-Based Authentication: For higher-risk profiles identified through the portal’s data analysis parameters, biometric verification at a designated facilitation centre is required, along with physical verification of original documents.

The following persons must complete Aadhaar authentication:

- Primary Authorised Signatory — Authentication is mandatory in all cases.

- At Least One Promoter or Partner — Required where such persons exist in the organisational structure.

| Author’s Commentary — Biometric Authentication: Planning Ahead to Avoid Time-Loss

Biometric-based authentication requires a physical visit to a notified GST Suvidha Kendra or facilitation centre. The identity of such centres varies by state, and availability of appointment slots can sometimes be limited. Considering that the authentication must be completed within 15 days of submission, taxpayers who are flagged for biometric verification are effectively working against a tight operational clock. The author advises practitioners to check whether their client is likely to be flagged, particularly where the registration is for a new entity, or where there have been prior instances of discrepancies and to begin the facilitation centre process immediately after submission rather than waiting. |

VII. Non-Negotiable Timelines: The 15-Day Windows

Two strict time limits govern the application process, and missing either one means the application lapses without an ARN:

| Action | Prescribed Deadline |

| Submission of draft application | Within 15 days of creation of the draft on the portal |

| Completion of Aadhaar / Biometric Authentication | Within 15 days of submission of the application |

| Consequence of missing either deadline | ARN will not be generated; the application is treated as not filed |

–

| Important: The 15-day clock begins running from the date the draft is created not from the date the taxpayer last edited it. Taxpayers who create a draft and then delay finalising it may find the application has already lapsed before submission. |

VIII. Portal Restrictions While the Application Is Pending

From the moment Form GST REG-32 is submitted and remains under the proper officer’s consideration, certain other portal activities are temporarily suspended. The taxpayer cannot file:

- Core Amendment Applications — Covering changes to the principal place of business, business name, constitution, or addition/deletion of partners or directors.

- Non-Core Amendment Applications — Covering changes to bank account details, authorised signatories, HSN/SAC codes, and similar details.

- Self-Cancellation Applications — Under Section 29(1) of the CGST Act, where the registered person wishes to surrender the registration.

| Author’s Commentary — Pre-Filing Housekeeping Is Essential

The processing freeze makes pre-filing compliance housekeeping non-negotiable. If a taxpayer needs to change their bank account, update an authorised signatory, or correct the principal place of business details, all such amendments must be completed before filing REG-32 not after. The author recommends a structured pre-filing checklist that includes: (a) verification of all registration particulars in REG-01 against current business reality; (b) confirmation that the Aadhaar-linked mobile numbers of signatories are active; (c) clearance of all pending GST returns; and (d) confirmation that no SCN for cancellation has been issued. Only after clearing this checklist should the taxpayer proceed to file. |

IX. After Approval: Legal Consequences of the Withdrawal Order

Where the proper officer, upon verification, issues an order in Form GST REG-33 allowing the withdrawal, the following legal consequences follow:

A. Prospective Transition to Normal Reporting

The withdrawal takes effect from the first day of the month that follows the month in which Form GST REG-33 is issued. From that date, the taxpayer is permitted to report and pay output tax liability on supplies to registered persons that exceeds the Rs. 2.5 lakh threshold in the normal course.

B. Retrospective Restriction on Amending Past Returns

The taxpayer is expressly barred from going back and amending returns for any period prior to the effective date of withdrawal so as to cross the Rs. 2.5 lakh output tax threshold. The logic here is straightforward: any period governed by Rule 14A must reflect a liability within the rule’s prescribed cap. This retrospective bar preserves the legal integrity of the taxpayer’s historical compliance record under the special registration.

C. Consequences of Rejection

If the proper officer finds the application non-compliant or the grounds insufficient, a rejection order in Form GST REG-05 is issued. In such a case, the taxpayer continues to be governed by Rule 14A. The rejection should be reviewed carefully for the stated grounds, and a fresh application may be filed after remedying the deficiency.

| Author’s Commentary — The Prospective Effect Clause — Planning the Transition Month

The prospective operation of the withdrawal order has an important practical dimension that is often overlooked. Consider a taxpayer whose REG-33 order is issued on March 15, 2026. The withdrawal takes effect from April 1, 2026 i.e. the first day of the succeeding month. This means that for the entirety of March 2026, the taxpayer remains under Rule 14A and must ensure that the output tax liability on supplies to registered persons does not cross Rs. 2.5 lakh in that month. Businesses with growing order books must plan their billing for the transition month with particular care. Exceeding the cap in the pre-effective-date period while REG-33 is already in hand could create an inadvertent compliance breach. |

X. Advisory Checklist for Tax Practitioners

Tax professionals managing clients registered under Rule 14A should consider the following structured advisory framework:

1. Threshold Monitoring: Implement a monthly output tax liability tracker for all Rule 14A clients. Any month where the liability approaches Rs. 2 lakh should trigger a formal review of whether withdrawal is warranted.

2. Return Pendency Audit: Before recommending REG-32, run a complete return pendency check from the date of Rule 14A registration. Even a single unfiled return will block the application at the portal level.

3. Aadhaar Mobile Verification: Confirm that the Aadhaar-linked mobile numbers of the Primary Authorised Signatory and at least one Promoter/Partner are active and accessible. This step is routinely missed and causes last-minute application failures.

4. Pre-Amendment Completion: Audit the details in REG-01 against current business reality. Carry out all necessary core and non-core amendments under Rule 19 before filing, since the portal freeze will prevent amendments during pendency.

5. Cancellation Proceedings Check: Verify that no SCN under Section 29 has been issued or is imminent. Filing REG-32 in the shadow of pending cancellation proceedings is likely to result in rejection without the deemed-approval safety net.

6. Transition Month Billing Plan: Once REG-33 is anticipated, advise the client to plan billing for the transition month carefully to ensure the Rule 14A threshold is not breached before the effective date of withdrawal.

| Author’s Commentary — The Bigger Picture: When Is Rule 14A Registration Still Worth Retaining?

Before advising withdrawal, practitioners should pause to consider whether the client should remain under Rule 14A. The rule provides significant compliance benefits: expedited registration, simplified Aadhaar-based processing, and a lower administrative burden. For taxpayers whose output tax liability fluctuates around the Rs. 2.5 lakh mark, a month of excess does not automatically require withdrawal, it requires an assessment of whether the excess is structural or seasonal. Only when the liability has consistently and materially exceeded the threshold or when the client’s business model has fundamentally changed should withdrawal be recommended. An unnecessarily early opt-out surrenders the benefits of Rule 14A without any regulatory compulsion to do so. |

XI. Quick Reference Summary

| Parameter | Details |

| GSTN Advisory Date | February 21, 2026 |

| Form to Be Filed | Form GST REG-32 |

| Governing Rule | Rule 14A, CGST Rules, 2017 |

| Enabling Notification | No. 18/2025-CT dated 31.10.2025 (w.e.f. 01.11.2025) |

| Who Can Apply | Active taxpayers registered under Rule 14A with no pending Section 29 proceedings |

| Pre-condition (Before 01.04.2026) | Minimum 3 months’ returns filed + all returns from reg. date cleared |

| Pre-condition (On/After 01.04.2026) | Minimum 1 tax period’s returns filed + all returns from reg. date cleared |

| Draft Submission Deadline | Within 15 days of draft creation |

| Authentication Deadline | Within 15 days of application submission |

| Authentication Mode | Aadhaar OTP or Biometric (risk-based) |

| Persons to Authenticate | Primary Authorised Signatory (mandatory) + at least one Promoter/Partner |

| Restrictions While Pending | No core/non-core amendments; no self-cancellation filing |

| Approval Order Form | Form GST REG-33 |

| Rejection Order Form | Form GST REG-05 |

| Effective Date of Withdrawal | First day of the month succeeding the month of REG-33 order |

| Retrospective Amendment Bar | Cannot amend past returns to exceed Rs. 2.5 lakh threshold for pre-effective periods |

XII. Conclusion

The operationalisation of Form GST REG-32 on the GST Portal completes a critical missing piece in the Rule 14A framework. From November 2025, when the rule was introduced, to February 2026, when the withdrawal facility went live, taxpayers registered under Rule 14A had no structured mechanism to transition back to the mainstream registration framework. That gap has now been addressed.

What distinguishes this facility from a routine portal update is its careful architecture: mandatory return compliance, Aadhaar-linked authentication, strict timelines, and a prospective transition mechanism together ensure that the exit route cannot be exploited for compliance arbitrage. At the same time, the procedural symmetry with the registration process mirroring Aadhaar requirements and officer verification provides a predictable, rule-bound pathway that taxpayers and advisors can plan around.

For the practitioner community, this development reinforces a broader lesson: special compliance regimes under GST require not just entry-level attention but ongoing monitoring. A client who entered the GST register through Rule 14A in November 2025 may well need to exit it by mid-2026 and that exit, as this article has detailed, carries its own set of conditions, timelines, and strategic considerations.

| Author’s Commentary — Final Thought: Regulatory Signals Worth Watching

The introduction of Rule 14A and its withdrawal mechanism together represent an experiment in risk-stratified GST administration the idea that taxpayers at different scales of operation can be governed by different compliance architectures. If this model proves effective, there is reason to expect further differentiation in GST compliance requirements in the future. Tax professionals who stay ahead of such structural changes rather than reacting to them will be better positioned to advise clients proactively. The key takeaway from this update is not just the mechanics of REG-32, but the recognition that GST law is evolving toward a more nuanced, taxpayer-profile-sensitive design. |

5 FAQs on Withdrawal from GST Rule 14A Registration Using Form GST REG-32

Q.1 Who is eligible to apply for withdrawal from Rule 14A registration?

Ans. Only taxpayers holding an active GST registration obtained under Rule 14A can apply through Form GST REG-32. The facility is unavailable if cancellation proceedings under Section 29 have been initiated or if the registration is suspended or cancelled.

Q.2 What conditions must be fulfilled before filing Form GST REG-32?

Ans. The taxpayer must file all pending GST returns from the effective date of Rule 14A registration up to the application date. Depending on the filing date, a minimum return filing requirement also applies. Any changes in registration particulars must first be updated through the prescribed amendment process.

Q.3 How can a taxpayer file Form GST REG-32?

Ans. The application is filed online through the GST Portal by navigating to Services → Registration → Application for Withdrawal from Rule 14A, providing the reason for withdrawal, completing Aadhaar authentication, and submitting the application to generate an ARN.

Q.4 What happens after the withdrawal application is approved?

Ans. Upon approval, the proper officer issues Form GST REG-33, and the withdrawal becomes effective from the first day of the month following the month in which the order is issued. Thereafter, the taxpayer transitions to the normal GST reporting framework.

Q.5 Are there any restrictions while the withdrawal application is pending?

Ans. Yes. During the pendency of Form GST REG-32, the taxpayer cannot file core or non-core registration amendment applications or apply for self-cancellation of GST registration until the withdrawal application is disposed of.

*******

Disclaimer: This article is written for educational and informational purposes only and does not constitute legal or tax advice. All readers are advised to verify the applicable provisions independently and consult a qualified GST professional for guidance specific to their situation. The author’s commentary sections reflect the author’s personal analytical views and do not represent official guidance.

Author Bio