Article explains Meaning of Input Tax Credit, What is Input Tax Credit under GST, Example of Input Tax Credit in GST, Relevance of the concept of the Input Tax Credit in the business parlance, Input Tax Credit Rules under GST, Amendment Notification in regards to the provisions of Input Tax.

Page Contents

- I. What is Input Tax Credit under GST (Introduction & Meaning)

- II. Example of Input Tax Credit under GST

- III. Relevance of Input Tax Credit under GST

- IV. How Input tax Credit can be availed?

- i. Rule 36- Documents and conditions for claiming Input Tax Credit

- ii. Rule 37-Reversal of Input Tax Credit in the case of non payment of consideration

- iii. Rule 38- Claim of credit by a banking company or a financial institution

- iv. Rule 39- Input Tax Credit by Input Service Distributor

- v. Rule 40 & 43-Manner of Claiming credit in special circumstances

- vi. Rule 41-Transfer of credit on sale, merger, amalgamation, lease or transfer of a business

- vii. Rule 42- Manner of determination of input tax credit in respect of inputs or input services and reversal thereof

- viii. Rule 44- Manner of reversal of credit under special circumstances

- ix. Rule 45- Conditions and restrictions in respect of inputs and capital goods sent to the job worker

- V. Amendment Notification in regards to the provisions of Input Tax

I. What is Input Tax Credit under GST (Introduction & Meaning)

Sec 2(63) of the CGST Act 2017 explains that Input Tax Credit means the credit of input tax wherein “input tax” in relation to a registered person, means the central tax, State tax, integrated tax or Union territory tax charged on any supply of goods or services or both made to him and includes—

(a) the integrated goods and services tax charged on import of goods;

(b) the tax payable under the provisions of sub-sections (3) and (4) of section 9;

(c) the tax payable under the provisions of sub-sections (3) and (4) of section 5(Levy and Collection) of the Integrated Goods and Services Tax Act;

(d) the tax payable under the provisions of sub-sections (3) and (4) of section 9(Levy and Collection) of the respective State Goods and Services Tax Act; or

(e) the tax payable under the provisions of sub-sections (3) and (4) of section 7(levy and collection) of the Union Territory Goods and Services Tax Act, but does not include the tax paid under the composition levy;

In simple terms, Input Tax means the amount of tax charged on supply of goods/ services which are intended to be used for the furtherance of business.

As per Sec 16 of the CGST Act 2017, every registered person shall subject to such conditions and restrictions as may be prescribed and in the manner specified and will be entitled to the credit of input tax charged on the supply of goods and/ or services which are used or intended to be used in the course or furtherance of his business.

Various provisions and applicable rules to the concept of Input Tax Credit are mentioned below

| Section no | Description of provisions |

| 16 | Eligibility and conditions for taking input tax credit

There are certain conditions mentioned in the law which are treated as the valid conditions for availing credit under GST and hence those items attribute to the eligible ITC under GST |

| 17 | Apportionment of credit and blocked credits

As per subsection 5 of the Sec 17 of the CGST Act 2017, the Input tax Credit cannot be availed for a certain class of supply of goods and services. In other words it can be interpreted that Sec 17(5) of the CGST Act 2017 deals with the items on which credit is not allowed under GST. |

| 18 | Availability of credit in special circumstances |

| 19 | Taking input tax Credit in respect of inputs and capital goods sent for job work |

| 20 | Manner of distribution of credit by Input Service Distributor |

| 21 | Manner of recovery of credit distributed in excess |

- II. Example of Input Tax Credit under GST

- III. Relevance of Input Tax Credit under GST

- IV. How Input tax Credit can be availed?

- i. Rule 36- Documents and conditions for claiming Input Tax Credit

- ii. Rule 37-Reversal of Input Tax Credit in the case of non payment of consideration

- iii. Rule 38- Claim of credit by a banking company or a financial institution

- iv. Rule 39- Input Tax Credit by Input Service Distributor

- v. Rule 40 & 43-Manner of Claiming credit in special circumstances

- vi. Rule 41-Transfer of credit on sale, merger, amalgamation, lease or transfer of a business

- vii. Rule 42- Manner of determination of input tax credit in respect of inputs or input services and reversal thereof

- viii. Rule 44- Manner of reversal of credit under special circumstances

- ix. Rule 45- Conditions and restrictions in respect of inputs and capital goods sent to the job worker

- V. Amendment Notification in regards to the provisions of Input Tax

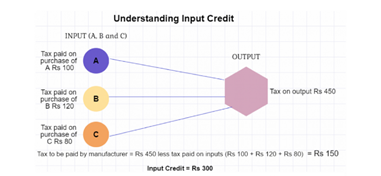

II. Example of Input Tax Credit under GST

III. Relevance of Input Tax Credit under GST

Input Tax Credit helps the businesses to determine their accurate amount of Working Capital at any given point of time. Needless to say that this is one of the most critical information from Business point of view, as it will actually determine the liquidity position of an entity at the time of evaluation.

Input Tax Credit Rules under Goods and Services Tax

| Rule no | Description of provisions |

| 36 | Documents and conditions for claiming Input Tax Credit |

| 37 | Reversal of Input Tax Credit in the case of non payment of consideration |

| 38 | Claim of credit by a banking company or a financial institution |

| 39 | Procedure of distribution of Input Tax Credit by Input service Distributor |

| 40 | Manner of Claiming credit under Special circumstances |

| 41 | Transfer of credit on sale , merger, amalgamation, lease, or transfer of a business |

| 42 | Manner of determination of input tax credit in respect of inputs or input services and reversal thereof |

| 43 | Manner of determination of input tax credit of capital goods and reversal thereof |

| 44 | Manner of reversal of credit under special circumstances |

| 45 | Conditions and restrictions in respect of inputs and capital goods sent to the job worker |

IV. How Input tax Credit can be availed?

i. Rule 36- Documents and conditions for claiming Input Tax Credit

For claiming Input Tax Credit under GST, a certain set of conditions has to be fulfilled by an assesee which comprise of the following-

1) Documentation requirement-On the basis – tax invoice/ debit note issued by a registered supplier, or other prescribed taxpaying document

Documents

|

2) Receipt status-Goods and/or services have been received*

3) Payment of Tax-Tax actually paid by the supplier to the credit of the appropriate Government, either in cash or by utilization of ITC

4) Furnishing of return-He has furnished the monthly return under Section 39

*Note: It shall be deemed that the registered person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such registered person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise.

Proviso to Sec 16(2) : If the recipient of services fails to pay (value + tax) within 180days from date of invoice, (ITC availed + interest) shall be added to his output tax liability

Other conditions for claiming Input tax Credit

– All the applicable particulars should be mentioned in the documents prescribed above

– All the relevant information is furnished in FORM GSTR2

– ITC can be availed if such payment has not been made as per the demand raised on account of any fraud, willful misstatement or suppression of facts etc

ii. Rule 37-Reversal of Input Tax Credit in the case of non payment of consideration

Applicability

For the assesee who has availed Input Tax Credit on the inward supply of goods or/ and services but has not paid the value of such supply to the supplier

Non payment on account of

Value of supply + amount of tax thereon

Time limit

As per the second proviso of Sec 16(2) i.e. 180 days

Action to be taken by such assesse

Furnishing of details in Form GSTR 2 , which will include the following-

– Supply details

– Amount of value not paid

– Amount of input tax credit availed of proportionate to such amount not paid to the supplier

When is to be submitted

In the Form GSTR 2 for the month immediately following the period of 180 days from the date of issue of invoice

iii. Rule 38- Claim of credit by a banking company or a financial institution

Applicability

For the Banking company, Financial Institutions including Non Banking Financial Companies engaged in the supply of services by way of accepting deposits or extending loans or advances.

Non availment of credit on account of

– Tax paid on inputs and input services that are used for non business purposes

– The credit on account of supplies specified in sec 17(5) of the CGST Act i.e Blocked Credits

iv. Rule 39- Input Tax Credit by Input Service Distributor

Rule 39 provides for the detailed requirements and conditions to be fulfilled by the Input Service Distributors for availing the Input Tax Credit, the manner is prescribed as follows-

– To be distributed in the same month of to which the credit belongs

– The details to be furnished in the Form GSTR 6

– Separate distribution for the eligible and ineligible Input Tax Credit

– Separate distribution of the Input tax Credit on account of Central, State, Union territory and Integrated Tax

– The input Tax credit on account of Integrated Tax shall be distributed as input tax credit of integrated tax to every recipient

– An Input Service Distributor Service Note shall be issued by the Input Service Distributor

– The invoice issued should clearly mentioned that it is issued only for distribution of Input Tax Credit

– Formula for distribution of Input Tax Credit in terms of provisions of law

v. Rule 40 & 43-Manner of Claiming credit in special circumstances

Applicability

On the inputs held in stock or inputs contained in semi finished or finished goods held in stock , credit claimed on capital goods

Input Tax credit on Capital Goods

There can be four different scenarios for availing Input tax Credit on Capital Goods namely-

1.Capital Goods used only for personal use

1.Capital Goods used only for personal use

2. Capital Goods only for exempted sales

Input Tax Credit is not available for personal purchases or for capital goods used in exempted sales. The same will be included in the form GSTR 2 and will not be credited to the Electronic Credit Ledger

3. Capital Goods used for normal sales

The Input tax credit on such sales will be available and the same will be reflected in GSTR 2 and will be credited in the electronic credit ledger.

4. Capital Goods used partly for personal/ exempted and partly for normal sales

The amount of Input tax Credit on account of Exempt Supplies will be calculated as follows

The remaining amount after reducing the credit on account of exempt supplies will be allowed as Input Tax Credit

vi. Rule 41-Transfer of credit on sale, merger, amalgamation, lease or transfer of a business

Applicability

– Sale

– Demerger

– Amalgamation

– Demerger

– Lease

– Transfer or change in the ownership of business or any other reasons

Action by assesee

The details of any of the above activity which has taken place will be submitted in Form GST ITC 02

Mode of Submission

Electronically on the common portal along with the request for transfer of untilised input tax credit lying in his electronic credit ledger to the transferee

vii. Rule 42- Manner of determination of input tax credit in respect of inputs or input services and reversal thereof

The detailed calculation along with the requisite formula has been explained in the relevant provisions of Rule 42 of the CGST rules.

viii. Rule 44- Manner of reversal of credit under special circumstances

Applicability

a. On the inputs held in stock or inputs contained in semi finished or finished goods held in stock ,

b. credit claimed on capital goods

Availment of Input Tax Credit

a. ITC to be calculated proportionately on the basis of eth corresponding invoices

b. The useful life will be taken as 5 years for the capital goods – 5 years to be taken from the date of Purchase and the total ITC will be distributed over the useful life of the asset

ix. Rule 45- Conditions and restrictions in respect of inputs and capital goods sent to the job worker

Applicability

Will be allowed to the Principal Manufacturer if a capital asset ahs been sent to a job worker for job work

Condition

– The goods sent must be received back within 3 years of being sent

– The goods must have been sent from the principal place of business or directly from the place of supply of the supplier of such goods

– The input goods must be received back within one year

– In case the goods are not received back within the stipulated time as mentioned above, then such goods will be treated as deemed supply and accordingly the provisions of the law will be applicable.

V. Amendment Notification in regards to the provisions of Input Tax

Cross-utilisation of ITC rationalized

Central Goods and Services Tax (Amendment) Rules, 2019 Notification No. 03/2019 – Central Tax 29/01/2019

| Prior 01/02/2019 | W.e.f 01/02/2019 | |

| Mode | – | The credit of state tax/union territory tax can be utilised for payment of integrated tax only when the balance of input tax credit on account of central tax is not available for payment of integrated tax. |

| New Section 49 A | – | A new section has been inserted to provide that the input tax credit on account

of central tax and state tax/union territory tax can be utilised towards the payment of integrated tax, central tax and state tax/union territory tax only after the input tax credit available on account of integrated tax has been first utilised fully towards such payment. |

| New Section 49 B | – | A new section has been inserted to allow the government, on the recommendation of the GST Council, to provide a specific order in which a registered person can utilise input tax credit, viz. integrated tax, central tax and state tax or union territory, for the settlement of the tax liability. |

I have purchase gold for personal use. But shown in GSTR 2A by supplier 3% GST . So how to shown in GSTR 3b and GSTR 9 if itc not claim

1.”A” HAS A BUSINESS SELLING LUBRICANT AS WELL AS TRACTOR PARTS.

2. “A” WISH TO WIND UP HIS BUSINESS,

3. “B” IS DEALING IN SAME BUSINESS . “A” SOLD HIS WHOLE BUSINESS SET UP TO ” B” . HOW AND HOW MUCH” ITC” WILL BE CLAIMED BY “B” ON THE CAPITAL GOODS PURCHASED FROM “A”.

day to day you publised the amendments thro web site in the matter how solve the GST R 9 AND GST R 9A IN THIS VIEW SOME SUPPLIERS NOT PROPERLY UPLOADED THRO GST R 1 AND ALSO ONE ISSUED THEY ARE BILLING WITH OUT GST IN MOBLIENUMBER AND ALSO ADHAR CARD BUT IT WAS UPLOADED REGECTED THE GST PORTAL WHEN UPLOADED SOME ERROR BUT AT THE SAME TIME RECEIVER BILLS CLAIMED ITC THEIR DEFF.IN PORTAL WITH ITC VARIATIION COMES THEIR IS LAST DATE OF RECTFICAITION BUT THE PORTAL NOT PROPERLY WORKING SOME TIME ERROR ANOTHER TIME POWER BLOCKED

AS REGARDS THE ABOVE DETAILS VOR THE YEAR JULY 2017 TO MARCH 2018 PLEASE HELP ME HOW TO RECTFY THE GSTR 9 AND GST R 9A TO DO NEEDFULL

Very well written but you have not explained rule 42 & 43 in detail as these rules are crux of itc.