Page Contents

- Refund on account of Refund by Recipient of Deemed Export (FAQS)

- 1. What are the preconditions for filing a refund application as recipient of deemed exports supplies?

- 2. Which amounts are eligible for refund as a recipient of deemed export?

- 3. Can I file multiple refund applications during a single tax period?

- 4. When / how will the refund form RFD-01A be processed?

- How can I file for refund as a recipient of deemed export?

Refund on account of Refund by Recipient of Deemed Export (FAQS)

1. What are the preconditions for filing a refund application as recipient of deemed exports supplies?

The following conditions must be met for being eligible to file form RFD-01A, for refund by recipient of deemed exports:

- The Taxpayer is registered with GST Portal and holds an active GSTIN during the refund application period.

- Balance in the Electronic Credit Ledger must be greater than or equal to the amount of refund to be claimed, since the same is required to be debited in case of Refund of ITC by recipient of deemed exports.

- GSTR-3B must have been filed for the relevant tax period.

2. Which amounts are eligible for refund as a recipient of deemed export?

While filing form RFD-01A (Recipient of deemed exports), Taxpayers need to enter the amount that they want to get as refund. The lowest of the following three categories are eligible for refund:

- Balance in Electronic Credit Ledger

- ITC availed for the particular tax period

- Amount entered by Taxpayer in Refund Claim Matrix.

3. Can I file multiple refund applications during a single tax period?

Only one Refund application (form RFD-01A) can be filed for each Refund type in a given Return period. For example, a Taxpayer may choose to file the refund against supplies received on account of deemed exports, as well as refund of excess balance in Electronic Cash Ledger, which is not related to any tax period. However, the Taxpayer cannot file two refund applications as recipient of deemed exports during a single tax period.

4. When / how will the refund form RFD-01A be processed?

Once the ARN is generated on submission of form RFD-01A, the Taxpayer needs to take prints of the filed application and the Refund ARN Receipt generated at the portal, and submit the same along with supporting documents to the jurisdictional authority. The application will be processed and refund will be disbursed manually.

How can I file for refund as a recipient of deemed export?

Refund by Recipient of Deemed Export (RFD-01A)

Taxpayers can file for refund of IGST / CGST / SGST / UTGST / Cess if any amount is due to them from the tax administration.

Filing for refunds is a post-login functionality, which means that the Taxpayer must login to the GST Portal with their valid login credentials before filing a refund application.

Recipients of Deemed Exports can file for refund by performing the following steps:

1. Access the GST Portal. The GST Home page is displayed.

2. Using your valid credentials, login to the GST Portal.

3. The Taxpayer’s Dashboard is displayed.

4. Open the Services menu, click the Refunds category, and select the Application for Refund option.

5. Select the tax period (year and month) for which the refund application needs to be filed.

6. Select the Recipient of Deemed Exports refund type radio button.

7. Click the corresponding Create button.

Notes:

- Form GST-RFD-01 A opens, which is meant for filing refund of taxes as a recipient of deemed exports.

- The header area displays the Taxpayer’s GSTIN, Legal name of Business, Trade Name, selected tax period, and status of current application.

- In the section Amount Eligible for Refund, the Taxpayer needs to enter the amount of Refund that he / she wants to claim. In subsequent columns, following are displayed against all the four major heads – IGST, CGST, SGST, and Cess:

> Balance in Electronic Credit Ledger (column 2)

> Tax Credit Availed during the period (column 3)

- The eligible refund amount in the last column must be lowest of the three figures displayed against each major head.

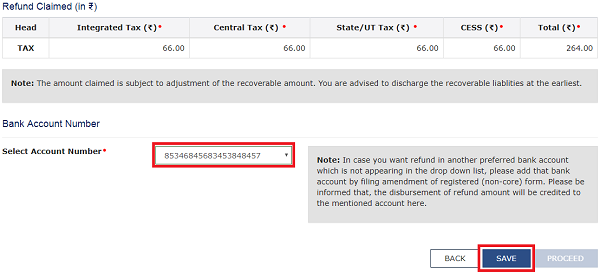

8. Enter the refund amount that you want to claim against each major head under column 1.

Note: The eligible amounts for each major head will reflect under the Refund Claimed section / table.

9. Select the bank account where you wish to receive the refund.

Notes:

- The bank accounts displayed in the drop-down are those accounts that were provided during GST registration.

- The Taxpayer must select a bank account from the drop-down list in order to receive refund.

10. Click Save to upload your entered refund details to the GST Portal.

Notes:

- The refund application must be saved before filing.

- The system will flash a confirmation message when saving the application for the first time.

- The system displays a confirmation message upon saving the application.

- Application can be saved at any stage and can be retrieved using the My Saved / Submitted Applications option under Refunds.

- Saved applications are stored in the system for 15 days, after which they get deleted automatically.

- Saving the application activates the Proceed button.

11. Click Proceed.

12. Check the declaration box.

13. Select an Authorized Signatory from the list of registered names in drop-down.

14. Click either Submit with DSC or Submit with EVC option:

- Submit with DSC: Sign the application using the registered Digital Signature Certificate of the selected authorized signatory.

- Submit with DSC: If the EVC option is selected, the system will trigger an OTP to the registered mobile phone number and e-mail address of the authorized signatory. Enter that OTP in the pop-up to sign the application.

Notes:

- The system generates an ARN and displays it in a confirmation message, indicating that the refund application has been successfully filed.

- GST Portal sends the ARN to the Taxpayer by e-mail and SMS.

- GST Portal makes a Debit entry in the Electronic Credit Ledger for the amount claimed as refund.

- Filed applications (ARNs) can be downloaded as PDF documents using the My Saved / Submitted Applications option under Refunds.

- Filed applications can be tracked using the Track Application Status option under Refunds.

- Once the ARN is generated on submission of form RFD-01A, the Taxpayer needs to take prints of the filed application and the Refund ARN Receipt generated at the portal, and submit the same along with supporting documents to the jurisdictional authority. The application will be processed and refund will be disbursed manually.

- The disbursement is made once the concerned Tax Official processes the refund application.