Manual on Refund of ITC accumulated due to Inverted Tax Structure (RFD-01A)

What are the steps to file for refund of ITC accumulated due to Inverted Tax Structure, on the GST Portal?

To file for refund of ITC accumulated on account of Inverted Tax Structure, perform following steps on the GST Portal:

1. Access the https://www.gst.gov.in/ URL. The GST Home page is displayed.

2. Click the Services > Refunds > Application for Refund command.

3. The Select the refund type page is displayed. Select the Refund on account of ITC accumulated due to Inverted Tax Structure option.

4. Select the Financial Year for which application has to be filed from the drop-down list.

5. Select the Tax Period for which application has to be filed from the drop-down list.

6. Click the CREATE button.

7 (a). Select Yes if you want to file a nil refund. Or else, select No.

In case of Yes:

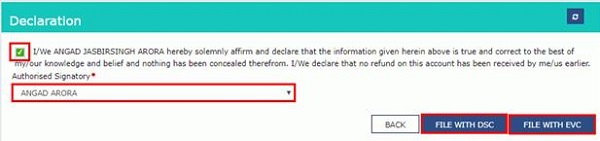

8. Select the Declaration checkbox.

9. In the Name of Authorized Signatory drop-down list, select the name of authorized signatory.

10. Click the FILE WITH DSC or FILE WITH EVC button.

In Case of DSC:

a. Click the PROCEED button.

b. Select the certificate and click the SIGN button.

In Case of EVC:

a. Enter the OTP sent to email and mobile number of the Authorized Signatory registered at the GST Portal and click the VERIFY button.

7 (b). In case of No:

8. The Refund on account of ITC accumulated due to Inverted Tax Structurepage is displayed.

First you need to download the offline utility, upload details of invoices for inward and outward supplies and then file refund on account of ITC accumulated due to Inverted Tax Structure.

Click the hyperlink below to know more about them.

Download Offline Utility – To download offline utility for statement 1A and enter details for invoices for which refund has to be claimed

Upload details of invoices for inward and outward supplies – To upload the details of invoices for inward and outward supplies

Refund on account of ITC accumulated due to Inverted Tax Structure – To enter details for refund of ITC on account of Inverted Tax Structure on the GST Portal

Download Offline Utility

9. Click the Download Offline Utility link.

10. Click the PROCEED button.

11. The zip file is downloaded. Right click on the zip file and select Extract All to unzip the downloaded file.

12. Statement 1A template would be downloaded. Open the excel sheet.

13. Once the template is downloaded, you need to enter the invoice details for which refund has to be claimed. Enter the GSTIN and “From Return Period” and “To Return Period” in mmyyyy format for which refund has to be claimed.

14. Enter the Sr. No., details of invoices of inwards supplies received, tax paid on inward supplies, details of invoices of outward supplies issued and tax paid on outward supplies.

15. Click the Validate & Calculate button.

16. The total number of records in the sheet is displayed. Click the OK button.

In case of Error:

17.1. Error is displayed in the Error column. Rectify the error.

17.2. Click the Validate & Calculate button.

17.3. Notice that the Error column is blank now after rectification.

18. Click the Create File To Upload button.

19. Browse the location where you want to save the file. Enter the name of the file and click the SAVE button.

20. A success message is displayed that file is created and you can now proceed to upload the file on the GST Portal. Click the OK button.

Upload details of invoices for inward and outward supplies

21. Click the link Click to fill the details of invoices for inward and outward supplies.

22. Click the CLICK HERE TO UPLOAD button.

23. Browse the location where you saved the JSON file. Select the file and click the Open button.

24.1. A success message is displayed that Statement has been uploaded successfully. You can click the Download Unique Invoices link to view the invoices that has been uploaded successfully.

24.2. Unique invoices that has been uploaded successfully are displayed.

25. Select the Declaration checkbox.

26. Click the PROCEED button.

27. Click the VALIDATE STATEMENT button.

28.1. In case any statement is validated with error, click the Download Invalid Invoice link.

28.2 Invalid invoice excel sheet is downloaded on your machine. Open the invalid invoice excel sheet. Error details are displayed.

28.3 (a). If your statement has been uploaded/validated with error, rectify the error in the JSON file and upload these invoices on the GST Portal again, as per process described above.

Note: You need to upload only the error invoices again by clicking the CLICK HERE TO UPLOAD button.

28.3 (b). If you don’t have any error and statement has been validated, and then you want to update/delete the statement, then you would have to first delete the whole statement and upload a new statement of invoices again if needed.

29. Once the statement is validated, you will get a confirmation message on screen that the statement has been submitted successfully for validation. Click the BACK button.

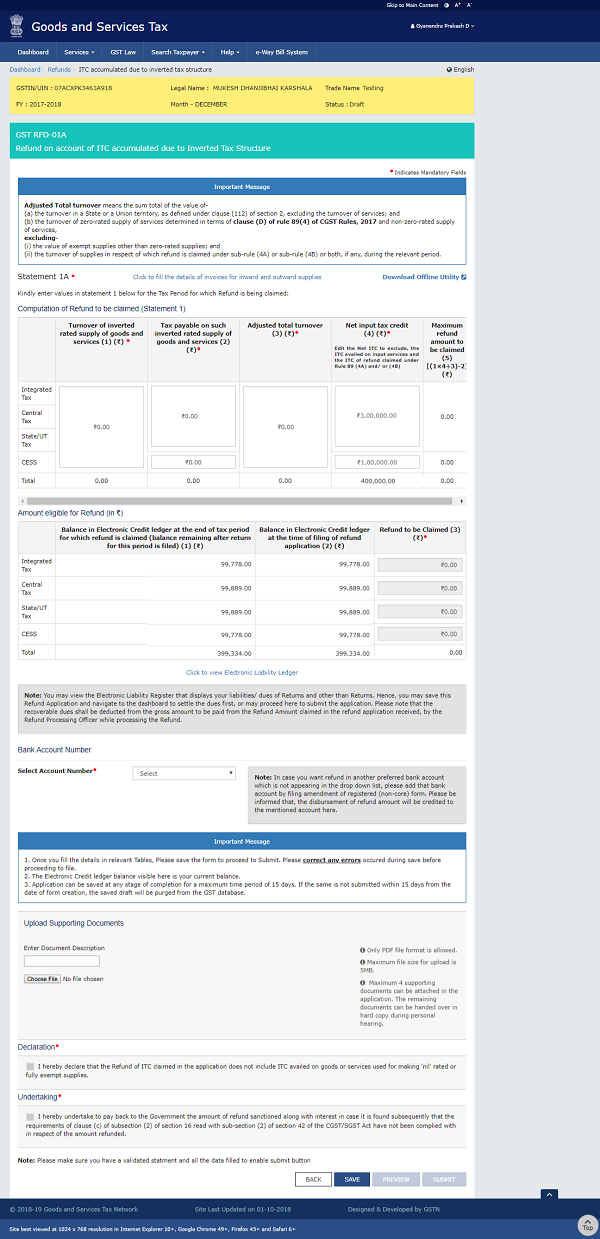

Refund on account of ITC accumulated due to Inverted Tax Structure

30. In the Table Computation of refund to be Claimed (Statement 1), perform following steps:

a. In column-1 (Turnover of inverted rated supply of goods and services), enter the turnover of inverted rated supply of goods and services by referring to column-3.1(a) of the Form GSTR-3B. The figure in column-1 is not pre-populated.

b. In column-2 (Tax payable on such inverted rated supply of goods and services), enter the tax payable on such inverted rated supply of goods and services. Taxpayer shall enter the sum of Integrated Tax, Central Tax and State/UT Tax in merged tax column and enter cess amount separately.

c. In column-3 (Adjusted total turnover), enter the amount of adjusted total turnover.

d. In column-4 (Net input tax credit), The figures of Net Input Tax Credit (ITC) in column-4 may be taken from column-4(C) of the Form GSTR-3B respectively. Net Input Tax Credit shall be auto-populated from the Electronic Credit Ledger of the taxpayer and taxpayer can edit the Net ITC, if required to exclude, the ITC availed on input services and the ITC of refund claimed under Rule 89 (4A) and/ or (4B). Sum of Integrated Tax ITC, Central Tax ITC and State/UT Tax ITC would be populated on aggregation basis. And Cess ITC amount would be auto-populated separately.

31. After filling the appropriate figures in table for Computation of Refund to be claimed (Statement 1), enter the amount of refund to be claimed in the “Amount Eligible for Refund” Table.

32. You can click the hyperlink Click to view Electronic Liability Ledger to view details of Electronic Liability Ledgerthat displays your liabilities/ dues of Returns and other than Returns.

33. Click the GO BACK TO REFUND FORM to return to the refund application page.

34. Select the Bank Account Number from the drop-down list.

35. Under section upload Supporting Documents, you can upload supporting documents (if any).

36. Click the Delete button, in case you want to delete any document.

Note: To view your saved application, navigate to Services > Refunds > My Saved/Filed Application command.

Application can be saved at any stage of completion for a maximum time period of 15 days from the date of creation of refund application. If the same is not filed within 15 days, the saved draft will be purged from the GST database.

37. Click the PREVIEW button to download the form in PDF format.

38. Form is downloaded in the PDF format.

39. Select the Declaration and Undertaking checkbox.

40. Click the SUBMIT button.

41. A confirmation message is displayed that “Statement submitted successfully.” Click the PROCEED button.

42. Select the Declaration checkbox.

43. In the Name of Authorized Signatory drop-down list, select the name of authorized signatory.

44. Click the FILE WITH DSC or FILE WITH EVC button.

In Case of DSC:

a. Click the PROCEED button.

b. Select the certificate and click the SIGN button.

In Case of EVC:

a. Enter the OTP sent to email and mobile number of the Authorized Signatory registered at the GST Portal and click the VERIFY button.

45. The success message is displayed and status is changed to Submitted.Application Reference Number (ARN)receipt is downloaded and ARN is sent on your e-mail address and mobile phone number. Click the PDF to open the receipt.

Notes:

- The system generates an ARN and displays it in a confirmation message, indicating that the refund application has been successfully filed.

- GST Portal sends the ARN to registered e-mail ID and mobile number of the registered taxpayer.

- Filed applications (ARNs) can be downloaded as PDF documents using the My Applications option under Services.

- Filed applications can be tracked using the Track Application Status option under Refunds.

- Once the ARN is generated on filing of form RFD-01A, refund application shall be assigned to refund processing officer for processing. The application will be processed and refund status shall be updated.

- The disbursement is made once the concerned Tax Official processes the refund application.

46. ARN receipt is displayed.

Also Read-

As on 12-10-2018, I opened my refund application and found that now we have to upload details of our inward and out ward supplies under STATEMENT 1A, a tool is available which can has to be used to create Json file to upload invoice details inward and out ward, this tool is not accepting all details and is regularly showing error even after a number of attempts. Kindly give solutions.

As on 03-010-2017, I opened my refund application and found that now we have to upload details of our inward and out ward supplies under STATEMENT 1A, a tool is available which can has to be used to create Json file to upload invoice details inward and out ward, this tool is not accepting all details and is regularly showing error even after a number of attempts. Kindly give solutions.

sir i need a help for refund the electronic credit ledger in my gst portal

Sir,

How to claim the credit carry forwarded from pre gst – VAT input tax credit balance availed through TRAN-1 Application. There is no taxable turnover details available. the carry forwarded has been duly credited to credit ledger in GST portal. Till now the balance credit available in gst portal. kindly advise to claim the refund of excess credit.