CA Satish Sarda

After the roll out of GST on 1st July 2017, there have been more then 200 amendments in just 133 days. Most of the changes were made to cover the software lapses and some were related to accommodate the valid demands of rationalization in tariff rates from businessmen from across the nation

Though many of the changes were much needed but indefinite postponement of GSTR 2 and GSTR 3 relating to matching of input credit and monthly final return ( which forms the basis of whole GST system) is very disappointing and exposes the government’s ill preparedness in roll out of GST.

Lacks of businessmen/professionals have wasted their time and energy in complying with the inefficient system. Culprit for the same must be identified and punished.

I have compiled the changes which have been announced by the the GST Council in its 23rd meeting held on 10th November 2017 at Guwahati headed by Finance Minister Mr. Arun Jaitley (Source-Press Release):

1. Registration : Exemption from registration to service provider providing service through E-commerce platform if annual turnover is below INR 20 Lakhs (INR 10 Lakhs for Special Category States) even if involved in interstate supplies

Return reschedulement:

GST Return

| Period / Month | GSTR-3B along with payment | GSTR-1 | GSTR-2 | GSTR-3 | |

| Taxpayers with annual aggregate turnover upto Rs. 1.5 crore | Taxpayers with annual aggregate turnover more than Rs. 1.5 crore | ||||

| July 2017 | 25-Aug-2017 | 31-Dec-2017 | 31-Dec-2017 | The time period for filing GSTR-2 and GSTR-3 for the months of July 2017 to March 2018 would be worked out by a committee of officers | |

| August 2017 | 20-Sep-2017 | 31-Dec-2017 | |||

| September 2017 | 20-Oct-2017 | 31-Dec-2017 | |||

| October 2017 | 20-Nov-2017 | 15-Feb-2018 | 31-Dec-2017 | ||

| November 2017 | 20-Dec-2017 | 10-Jan-2018 | |||

| December 2017 | 20-Jan-2018 | 10-Feb-2018 | |||

| January 2018 | 20-Feb-2018 | 30- Apr-2018 | 10-Mar-2018 | ||

| February 2018 | 20-Mar-2018 | 10-Apr-2018 | |||

| March 2018 | 20-Apr-2018 | 10-May-2018 | |||

Note : Late fee is waived in all cases where return in FORM GSTR-3B is not filed within due date for the months of Jul, Aug & Sep 2017. Where such late fees was paid, it will be re-credited to their Electronic Cash Ledger under “Tax” head instead of “Fee” head so as to enable them to use that amount for discharge of their future tax liabilities.

Other GST Return

| Form / Period | Particulars | Due Date |

| GSTR-4 July to Sept 2017 | Quarterly return for registered person opting for composition levy | 24-Dec-2017 |

| GSTR-5 July 2017 | Return for Non-resident taxable person | 11-Dec-2017 |

| GSTR-5A July 2017 | Details of supplies of online information and database access or retrieval services by a person located outside India made to non-taxable person in India | 15-Dec-2017 |

| GSTR-6 July 2017 | Return for Input Service Distributor | 31-Dec-2017 |

Other Forms and Statements

| Form / Period | Particulars | Due Date |

| TRAN-1 | Transitional ITC/Stock Statement | 31-Dec-2017 |

| ITC-01 | Declaration for claim of Input Tax Credit under sub-section (1) of Section 18 | 30-Nov-2017 |

| ITC-04

July to Sept 2017 |

Details of goods/capital goods sent to job workers and received back | 31-Dec-2017 |

| It is proposed to issue notifications [giving effect to these recommendations of the Council] on 14th/15th November, 2017, to be effective from 00hrs on 15th of November, 2017. |

3. Changes recommended in Composition Scheme

i. Uniform rate of tax @ 1% under composition scheme for manufacturers and traders (for traders, turnover will be counted only for supply of Taxable goods only instead of earlier Aggregate Turnover ). No change for composition scheme for restaurant.

ii. Supply of services by taxpayer upto Rs 5 lakh per annum will not debar the taxpayer to opt for composition scheme. ( earlier a taxpayer providing any services in addition to trading / manufacturing could not opt for composition scheme.)

iii. Annual turnover eligibility for composition scheme will be increased to Rs 2 crore from the present limit of Rupees 1 crore under the law. Thereafter, eligibility for composition will be increased to Rs. 1.5 Crore per annum.

iv. The changes recommended by GST Council at (ii) and (iii) above will be implemented only after the necessary amendment of the CGST Act and SGST Acts.

4. Recommendations for rate changes made by the GST Council :

a. As per these recommendations, the list of 28% GST rated goods is recommended to be pruned substantially, from 224 tariff headings [about 18.5% of total tariff headings at 4-digit] to only 50 tariff headings including 4 headings which have been partially reduced to 18% [about 4% of total tariff headings at 4-digit].

b. Further, the Council has recommended changes in GST rates on a number of goods, so as to rationalize the rate structure with a view to minimize classification disputes.

c. The Council has also recommended issuance of certain clarifications to address the grievance of trade on issues relating to GST rates and taxability of certain goods and services.

d. On the services side also, the Council recommended changes in GST rates to provide relief to aviation & handicraft sectors and restaurants.

Major recommendations of the Council in this regard are summarized below.

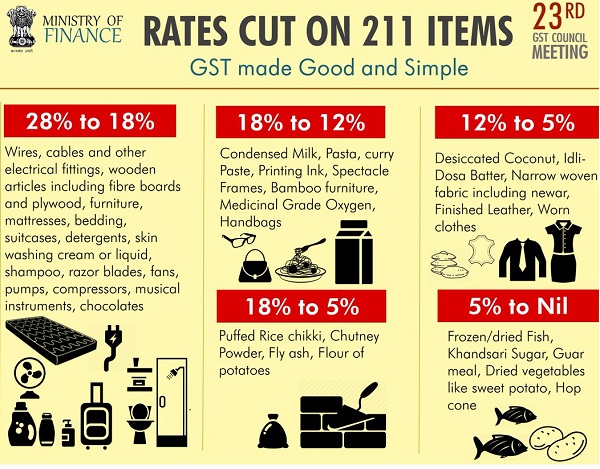

a) Goods on which the Council has recommended reduction in GST rate from 28% to 18% include:

- Wire, cables, insulated conductors, electrical insulators, electrical plugs, switches, sockets, fuses, relays, electrical connectors

- Electrical boards, panels, consoles, cabinets etc for electric control or distribution

- Particle/fiber boards and ply wood. Article of wood, wooden frame, paving block

- Furniture, mattress, bedding and similar furnishing

- Trunk, suitcase, vanity cases, brief cases, traveling bags and other hand bags, cases

- Detergents, washing and cleaning preparations

- Liquid or cream for washing the skin

- Shampoos; Hair cream, Hair dyes (natural, herbal or synthetic) and similar other goods; henna powder or paste, not mixed with any other ingredient; Pre- shave, shaving or after-shave preparations, personal deodorants, bath preparations, perfumery, cosmetic or toilet preparations, room deodorizers

- Perfumes and toilet waters

- Beauty or make-up preparations

- Fans, pumps, compressors

- Lamp and light fitting

- Primary cell and primary batteries

- Sanitary ware and parts thereof of all kind

- Articles of plastic, floor covering, baths, shower, sinks, washbasins, seats, sanitary ware of plastic

- Slabs of marbles and granite

- Goods of marble and granite such as tiles

- Ceramic tiles of all kinds

- Miscellaneous articles such as vacuum flasks, lighters,

- Wrist watches, clocks, watch movement, watch cases, straps, parts

- Article of apparel & clothing accessories of leather, guts, fur skin, artificial fur and other articles such as saddlery and harness for any animal

- Articles of cutlery, stoves, cookers and similar non electric domestic appliances

- Razor and razor blades

- Multi-functional printers, cartridges

- Office or desk equipment

- Door, windows and frames of aluminum.

- Articles of plaster such as board, sheet,

- Articles of cement or concrete or stone and artificial stone,

- Articles of asphalt or slate,

- Articles of mica

- Ceramic flooring blocks, pipes, conduit, pipe fitting

- Wall paper and wall covering

- Glass of all kinds and articles thereof such as mirror, safety glass, sheets, glassware

- Electrical, electronic weighing machinery

- Fire extinguishers and fire extinguishing charge

- Fork lifts, lifting and handling equipment,

- Bull dozers, excavators, loaders, road rollers,

- Earth moving and leveling machinery,

- Escalators,

- Cooling towers, pressure vessels, reactors

- Crankshaft for sewing machine, tailor’s dummies, bearing housings, gears and gearing; ball or roller screws; gaskets

- Electrical apparatus for radio and television broadcasting

- Sound recording or reproducing apparatus

- Signalling, safety or traffic control equipment for transports

- Physical exercise equipment, festival and carnival equipment, swings, shooting galleries, roundabouts, gymnastic and athletic equipment

- All musical instruments and their parts

- Artificial flowers, foliage and artificial fruits

- Explosive, anti-knocking preparation, fireworks

- Cocoa butter, fat, oil powder,

- Extract, essence ad concentrates of coffee, miscellaneous food preparation

- Chocolates, Chewing gum / bubble gum

- Malt extract and food preparations of flour, groats, meal, starch or malt extract

- Waffles and wafers coated with chocolate or containing chocolate

- Rubber tubes and miscellaneous articles of rubber

- Goggles, binoculars, telescope,

- Cinematographic cameras and projectors, image projector,

- Microscope, specified laboratory equipment, specified scientific equipment such as for meteorology, hydrology, oceanography, geology

- Solvent, thinners, hydraulic fluids, anti-freezing preparation

b) Goods on which the Council has recommended reduction in GST rate from 28% to 12% are:

- Wet grinders consisting of stone as grinder

- Tanks and other armoured fighting vehicles

c) 18% to 12%

1. Condensed milk

2. Refined sugar and sugar cubes

3. Pasta

4. Curry paste, mayonnaise and salad dressings, mixed condiments and mixed seasoning

5. Diabetic food

6. Medicinal grade oxygen

7. Printing ink

8. Hand bags and shopping bags of jute and cotton

9. Hats (knitted or crocheted)

10. Parts of specified agricultural, horticultural, forestry, harvesting or threshing machinery

11. Specified parts of sewing machine

12. Spectacles frames

13. Furniture wholly made of bamboo or cane

d) 18% to 5%

i. Puffed rice chikki, peanut chikki, sesame chikki, revdi, tilrevdi, khaza, kazuali, groundnut sweets gatta, kuliya

ii. Flour of potatoes put up in unit container bearing a brand name

iii. Chutney powder

iv. Fly ash

v. Sulphur recovered in refining of crude

vi. Fly ash aggregate with 90% or more fly ash content

e) 12% to 5%

a. Desiccated coconut

b. Narrow woven fabric including cotton newar [with no refund of unutilised input tax credit]

c. Idli, dosa batter

d. Finished leather, chamois and composition leather

e. Coir cordage and ropes, jute twine, coir products

f. Fishing net and fishing hooks

g. Worn clothing

h. Fly ash brick

f) 5% to Nil

i. Guar meal

ii. Hop cone (other than grounded, powdered or in pellet form)

iii. Certain dried vegetables such as sweet potatoes, maniac

iv. Unworked coconut shell

v. Fish frozen or dried (not put up in unit container bearing a brand name)

vi. Khandsari sugar

g) Miscellaneous

1. GST rates on aircraft engines from 28%/18% to 5%, aircraft tyres from 28% to 5% and aircraft seats from 28% to 5%.

2. GST rate on bangles of lac/shellac from 3% GST rate to Nil.

h) Exemption from IGST/GST in certain specified cases:

i. Exemption from IGST on imports of lifesaving medicine supplied free of cost by overseas supplier for patients, subject to certification by DGHS of Center or State and certain other conditions

ii. Exemption from IGST on imports of goods (other than motor vehicles) under a lease agreement if IGST is paid on the lease amount.

iii. To extend IGST exemption presently applicable to skimmed milk powder or concentrated milk, when supplied to distinct person under section 25(4) for use in production of milk for distribution through dairy cooperatives to where such milk is distributed through companies registered under the Companies Act.

iv. Exemption from IGST on imports of specified goods by a sports person of outstanding eminence, subject to specified conditions

v. Exemption from GST on specified goods, such as scientific or technical instruments, software, prototype supplied to public funded research institution or a university or IISc, or IITs or NIT.

vi. Coverage of more items, such as temporary import of professional equipment by accredited press persons visiting India to cover certain events, broadcasting equipments, sports items, testing equipment, under ATA carnet system. These goods are to be re-exported after the specified use is over.

i) Other changes for simplification and harmonization or clarification of issues

i. To clarify that inter-state movement of goods like rigs, tools, spares and goods on wheel like cranes, not being in the course of furtherance of supply of such goods, does not constitute a supply. This clarification gives major compliance relief to industry as there are frequent inter-state movement of such kind in the course of providing services to customers or for the purposes of getting such goods repaired or refurbished or for any self-use. Service provided using such goods would in any case attract applicable tax.

ii. To prescribe that GST on supply of raw cotton by agriculturist will be liable to be paid by the recipient of such supply under reverse charge.

iii. Supply of e-waste attracts 5% GST rate. Concerned notification to be amended to make it amply clear that this rate applies only to e-waste discarded as waste by the consumer or bulk consumer.

j) Changes relating to GST rates on certain services

(A) Exemptions / Changes in GST Rates / ITC Eligibility Criteria

a. All stand-alone restaurants irrespective of air conditioned or otherwise, will attract 5% without ITC. Food parcels (or takeaways) will also attract 5% GST without ITC.

b. Restaurants in hotel premises having room tariff of less than Rs 7500 per unit per day will attract GST of 5% without ITC.

c. Restaurants in hotel premises having room tariff of Rs 7500 and above per unit per day (even for a single room) will attract GST of 18% with full ITC.

d. Outdoor catering will continue to be at 18% with full ITC.

e. GST on services by way of admission to “protected monuments” to be exempted.

f. GST rate on job work services in relation to manufacture of those handicraft goods in respect of which the casual taxable person has been exempted from obtaining registration, to be reduced to 5% with full input tax credit.

(B) Rationalization of certain exemption entries

i. The existing exemption entries with respect to services provided by Fair Price Shops to the Central Government, State Governments or Union Territories by way of sale of food grains, kerosene, sugar, edible oil, etc. under Public Distribution System (PDS) against consideration in the form of commission or margin, is being rationalized so as to remove ambiguity regarding list of items and the category of recipients to whom the exemption is available.

ii. In order to maintain consistency, entry at item (vi) of Sr. No.3 of Notification No. 11/2017-CT(R) will be aligned with the entries at items (ii), (iii), (iv) and (v) of SI.No.3. [The word “services” in entry (vi) will be replaced with “Composite supply of Works contract as defined in clause 119 of Section 2 of CGST Act, 2017“].

iii. In order to obviate dispute and litigation, it is proposed that irrespective of whether permanent transfer of Intellectual Property is a supply of goods or service.-

(i) permanent transfer of Intellectual Property other than Information Technology software attracts GST at the rate of 12%; and

(ii) permanent transfer of Intellectual Property in respect of Information Technology software attracts GST at the rate of 18%.

(C) Clarifications

i. It is being clarified that credit of GST paid on aircraft engines, parts & accessories will be available for discharging GST on inter–state supply of such aircraft engines, parts & accessories by way of inter-state stock transfers between distinct persons as specified in section 25 of the CGST Act.

ii. A Circular will be issued clarifying that processed products such as tea (i.e. black tea, white tea etc.), processed coffee beans or powder, pulses (de-husked or split), jaggery, processed spices, processed dry fruits & cashew nuts etc. fall outside the definition of agricultural produce given in Notification No. 11/2017-CT(R) and 12/2017-CT(R) and therefore the exemption from GST is not available to their loading, packing, warehousing etc.

iii. A suitable clarification will be issued that (i) services provided to the Central Government, State Government, Union territory under any insurance scheme for which total premium is paid by the Central Government, State Government, Union territory are exempt from GST under Sl. No. 40 of Notification No. 12/2017-Central Tax (Rate); (ii) services provided by State Government by way of general insurance (managed by government) to employees of the State government/ Police personnel, employees of Electricity Department or students are exempt vide entry 6 of Notification No. 12/2017-CT(R) which exempts Services by Central Government, State Government, Union territory or local authority to individuals.

Trade and Industry were expecting cut in the rate of Cement , Paints and some domestic utility items also. We hope GST council once again considers the valid demands and recommend the required changes. Rate cut on Cement and Paints is very much needed as they constitute a major portion in Construction cost without ITC benefit. So to give impetus to Housing and Infrastructural sector a rate cut is much needed.

An overhauling and dry run of the system is extremely necessary to save the taxpayers from further harassments. It will be a “Good and Simple Tax” only if people in general ratify it and not because Government thinks so.

Disclaimer : Please refer to Notifications which will be issued in due course for accurate information.

(Author is a Practicing Chartered Accountant and Past Chairman of Nagpur Branch Of ICAI and can be reached at satishsardanagpur@gmail.com)

Author Bio