Chartered Accountants Association, Ahmedabad

28th May, 2019

To,

The Chief Commissioner Gujarat State Goods and Service Tax

Rajyakar Bhavan,

Ahmedabad,

Gujarat.

Respected Sir,

Re: Representations for various matters under Goods and Service Tax

We are members of the Chartered Accountants’ Association Ahmedabad and currently we have a strength of 1500 active members. We are organising various knowledge enrichment programmes and also conducting Seminars,workshops and events with sole purpose of knowledge enhancement. In this era of GST we have trained around 1000 plus chartered Accountants and are also carrying out various GST seminars to upkeep with the changes. As we are a part of society building and we wish to work hand in hand with your department so that we can enrich and help in developing and smooth functioning on both the sides we are hereby sharing some observations which we feel needs to be represented so that errors in the forms or law can be made for removal of difficulty faced by the assessees’ at large.

Page Contents

- 1. The period mentioned in GSTR 9 needs to be changed from Sept 2018 to March 2019

- 2. IGST paid on Import in the year 2017-18 but claimed in 2018-19 Current:

- 3. Erroneous Auto Population in column 8A of GSTR-9

- 4. Error faced by assessee migrated from regular tax scheme to composition scheme

- 5. Excessive details called for in Column 16A of GSTR 9

- 6. Excessive details called for in Column 7A of GSTR 9

- 7. Profit & Loss Bifurcation as needed in GSTR 9C in column 14

- 8. Disclaimer Notes & Comments in GSTR 9C in Certification Part B

- 9. SMS sent for GSTR 1 and 3B and GSTR 2A and 3B Difference

- 10. No place to show RCM of 2017-18 paid in 2018-19

- 11. Amount of Reversal done not considered while making comparison with 2A

- 12. Interest charged as per Reversal under 42 or 43

1. The period mentioned in GSTR 9 needs to be changed from Sept 2018 to March 2019

Current: As we are aware that in the present case in column 8C the information is furnished for data that is ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018.

Suggestion: The same needs amendment to extend itself to ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to March, 2019.

Impact: The Government on 31St December 2018 had issued Order No. 2/2018 – Central Tax. Where in sec 16(4) was amended “Provided that the registered person shall be entitled to take input tax credit after the due date of furnishing of the return under section 39 for the month of September, 2018 till the due date of furnishing of the return under the said section for the month of March, 2019 in respect of any invoice or invoice relating to such debit note for supply of goods or services or both made during the financial year 2017-18, the details of which have been uploaded by the supplier under sub-section (1) of section 37 till the due date for furnishing the details under sub-section (1) of said section for the month of March, 2019.” The same change needs to be made in GSTR-9 to make it in line with the Order issued by the Central Board of Indirect Taxes and Customs

2. IGST paid on Import in the year 2017-18 but claimed in 2018-19 Current:

Suggestion: We hereby suggest that there needs to be an addition of a column after 8J in line with 8C in order to report credit for Import done in 2017-18 but availed in 2018-19 Or the council may issue a clarification in nature that only credit which has been availed in 2017-18 with regards to IGST paid on Imports including supplies from SEZ is required to be reported.

Impact: There is a fear that credit availed in succeeding year in respect to IGST paid on Imports including supplies from SEZ in preceding year shall lapse as there is no column to declare in GSTR -9. In this regards if our suggestion is accepted then major relief will be made available to Importers and DTA Purchasers at large.

3. Erroneous Auto Population in column 8A of GSTR-9

Current: It is observed that while preparing GSTR-9, the ITC s reflected in 2A is auto populated in Column 8A of GSTR-9. However on verification of the same it is observed that the cumulative figure as auto populated in Column 8A of GSTR 9 does not match with the cumulative Credit as reflected in GSTR 2A.

Cumulative credit as per Form 2A IGST 206742.57 CGST and SGST each 205989.50/-

Suggestion: We hereby suggest that the assesses shall be allowed to manually rectify the auto-populated incorrect figure as reflected in column 8A of GSTR 9.

Or

The GSTN system need to troubleshoot the error and address the same.

Impact: Due to mismatch in Column 8A and GSTR 2A, the assessee at large are unable to provide true and correct input in regards to ITC availed during the period.

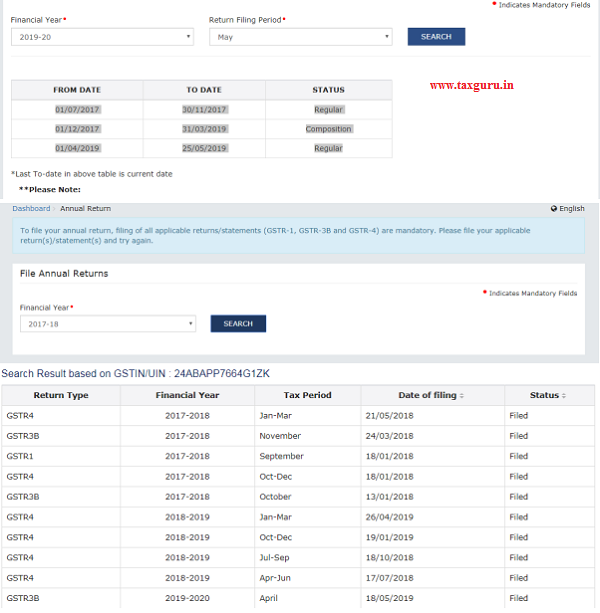

4. Error faced by assessee migrated from regular tax scheme to composition scheme

Current: The assessee who have migrated from the regular tax option to composition scheme during the year in 2017-18 Are unable to file form GSTR9 and GSTR9A for the period as the system is requiring the assessee to file GSTR 3B for the composition period as well.

Screenshot for the error faced is hereunder:

Suggestion: The GSTN system should allow the assessee to file the necessary returns. However in case of inability to update the system, a order needs to be passed allowing such assessee’s to manually file the annual return before the proper officer.

Impact: the system error has incapacitated regular and compliant assessee’s from filing the annual return. The proposed suggestion, if accepted, may bring respite to all the small tax assessee’s.

5. Excessive details called for in Column 16A of GSTR 9

Current: in Column 16A of GSTR 9 the assessee is required to report the supplies received by the assessee from composition tax payers. The assessee are facing real hardship in identifying the composition suppliers from whom the supplies are procured and further it is difficult to maintain books of accounts in which composition dealers are separated bifurcated. The said exercise requires unnecessary man power and increases compliance cost to the assessee.

Suggestion: The fact that composition dealers are small tax payers, supplies received from them normally would form a very minuscule part of the total supplies receivedby the assessee. The suggestion is being provided that like Column 18 wherein HSN wise summary of inward supply constituting of 10% or more supply of turnover is required to be reported, a suitable base limit in this regard may be provided for reporting of a transaction.

Impact: The excessive detail called for in Column 16A is extremely difficult to provide especially for MSME assessee’s and if the said details asked for are simplified it shall encourage assessee to file the returns in time, reduce compliance cost and thus facilitating ease of doing business.

6. Excessive details called for in Column 7A of GSTR 9

Current: in Column 7A and 7B of GSTR 9 the assessee is required to separately report the inward supplies received from registered and unregistered person liable for reverse charge. The assessee are facing real hardship in identifying the suppliers whether they are registered or not as the assessee was required to discharge the tax on reverse charge mechanism and hence no separate record was needed.

Suggestion: The fact that assessee was required to discharge the tax on reverse charge mechanism and hence there was no need for the assessee to bifurcate the supplies received liable under reverse charge into registered and unregistered suppliers. Further Section 9(4) has been omitted and hence there is no need to call for bifurcation anymore. It is thus suggested that column 7A and 7B be merged and single details of Inward supplies liable to reverse charge may be called for in Column 7.

Impact: The excessive detail called for in Column 7A and 7B is extremely difficult to provide especially for MSME assessee’s as the providing same will requiring verification of each and every invoice. Further the said details shall not have any tax impact. The suggestion if accepted shall simplify the compliance exercise and thus increase the ease of business.

7. Profit & Loss Bifurcation as needed in GSTR 9C in column 14

Current: In the current GSTR 9C there are illustrative list given and then a column of other is given to report the Amount of ITC available and ITC Availed. Only 5 row items can be added in other and the word other is not alterable

Suggestion: Such details are tedious in nature. Either such column for the year 2017-18 must be relaxed and not to be provided for or the details must only be asked for the ITC which is availed rather than Total ITC available. Further the row of expense type must be flexible and the assessee must be allowed to use the words and details as he wants rather than being a rigid field

Impact: The excessive detail called for in Column 14 of GSTR 9C is extremely difficult to provide especially for MSME assessee’s as the providing same will requiring verification of each and every invoice. Further the said details shall not have any tax impact. The suggestion if accepted shall simplify the compliance exercise and thus increase the ease of business.

8. Disclaimer Notes & Comments in GSTR 9C in Certification Part B

Current: In the offline tool provided there are static field that has been provided in Qualification as sr no 2 and 4 as qualification type. It cannot be edited.

Suggestion: The type of Qualification must be editable field

Impact: It will allow the Auditor to freely comment and address the report

9. SMS sent for GSTR 1 and 3B and GSTR 2A and 3B Difference

Current: The assessee is receiving SMS as to such differences as per the data filled by them in 3B.

Suggestion: We accept that it is a good initiative so we can timely take note of the errors and rectify them. However the data picked from GSTR 1 should be taken after deducting the details of 2017-18 shown in 2018-19 so as in order to make sure that the details of 3B and GSTR 1 are actually matching.

As far as matching of 2A and 3B is considered it is statistical in nature and having no impact. We also want to bring to your notice that such difference if any is right now being forced upon the assessee to pay vide DRC 03 or to reverse such value of ITC. This is injustice done to the honest assessee who will have to pay tax twice and incur loss due to the negligent seller. Even in refund such amounts are not allowed and credit is reduced to that extent. Sir in such cases the buyer if can prove that he has genuine purchases then the seller must be pressurised to pay the tax rather than ITC of genuine buyer being reduced. Further at time of refund such amount must not be deducted but if at time of final assessment if genuineness is not proved then maybe such ITC may be taxed with interest.

Impact: The genuine buyer will not be scared of making purchases and there would be ease of doing Business

10. No place to show RCM of 2017-18 paid in 2018-19

Current: In the current GSTR 9 any transactions pertaining to 2017-18 paid or disclosed in 18-19 needs to be reflected in column 10 to 13. If we add liability in column 10 the problem is it increases my taxable sale also

Suggestion: There needs to be a separate column for disclosing such liability or there needs to be a clarification issued in this regards

Impact: This will help in filling the GSTR 9 in correct manner.

11. Amount of Reversal done not considered while making comparison with 2A

Current: In Gstr 9, table 6 talks about ITC availed through 3B and we shall bifurcate the amounts in form of inputs capital goods & services. Table 7 talks about reversals and Table 8 comparison between 2A & table 6B (ITC availed). Nowhere in the form amount of reversal is considered while doing the comparison between 2A and table 6B

Meaning thereby, the assesse has availed credit under Rs 1.5 lakhs each in CGST and SGST, later on the assesseee came to know 0.5 lakhs is wrongly availed henceforth reversed such credit in table 4B of 3B.

So table 6 of Gstr 9 will indicate 1.5 lakhs and same in taken for consideration between 2A and 6B in table 8. In 2A only actual invoice having credit of 1 lakhs each under CGST and SGST will come. So there shall be difference on account of such reversals.

Suggestion: Clarification as to how to make the comparison effective or the formula must include such reversal while computing the differences

Impact: This will help in filling the GSTR 9 in correct manner.

12. Interest charged as per Reversal under 42 or 43

Current: As per the Act the assessee is right now required to reverse credit u/s 42 or 43 on monthly basis and then recalculate it on yearly bass. If he finds that the credit reversed is less than he is required to pay interest on such difference

Suggestion: It is impossible to know before the year end whether such amount is less or more and such excess reversal needed must be done but no interest on the same should be charged as it is not possible to reverse credit of the whole year in the beginning of the year. Thus waiver of such interest is a need of the hour

Impact: The genuine assessee wouldn’t be forced to pay unnecessary interest as he has not done anything wrong. This will help the assessee to be more compliant and increase ease of doing business

Conclusion

We, the members of the CA Association Ahmedabad thus would like to bring to you some important changes or clarifications required from the department side. We thus in our earnest effort to build the bridge and keeping in mind the revenue and client needs have put forth some suggestions. It would be of great help that such issues be resolved and trader and Tax fraternity also can file the return in simplified manner so that accurate and correct information can be collected.

Thanking you

Yours faithfully

For, Chartered Accountants Association, Ahmedabad

CA.Monish S.Shah

Chairman

legal Representation Committee

(Indirect Tax)

CA. Anand S.Sharma

President

C.A. Association, Ahmedabad

CC

Secretary of Ministry of Finance

office of the GST Council Secretariat

Download Representation by Chartered Accountants Association, Ahmedabad in PDF

Not 12 …… There are thousands of errors … Worst GST system on Earth India.

It is designed by bullheads

In B2b invoices in gst1 for the month of july 2017 i mistakely uplode bill but amdment of gstr1 due date is alreday over i need to change it there is no option coorect my mistake..But recipent ask you pay lability amt.But actually i pay tax in gstr3b govt pls extend due date..Or realse gstr2 in invoices accept or reject or uploded by recipent..Seeious issue

Pls extend due to date amendee gstrl

w.r.t to the point no.9 the policy of harassing the genuine buyer for supllier’s default who has not uploaded the sales made by him is not acceptable. If the buyer is in a position to substantiate his claim ie., having the bill and making the payment by cheque etc the govt should action against the supplier. General saying is “even if ten culprits are escaped the punishment , not even one innocent should be punished.” Where as it seems to be reverse in this case. The govt should take some genuine steps to safeguard the interest of honest dealers.

Dear Sir,

while thanking you for your efforts and suggestions for simplifying the GSTR-9, I request you to represent on one more issue as detailed below:

we are dealer in automobiles. As per supplier norms, we have to maintain stock equivalent to 45 days sale value , which resulted in purchase value is always more than sale value and input tax credit in electronic ledger is accumulating month by month which is lakhs.

this is causing undue strain on working capital.

I request you to take up the issue with govt. to at least allow the tax payer to seek refund of excess credit after certain limit, say any amount above Rs.500000/- five lakhs.

thanking you sir,

regards

A.Rangaswamy

9392790744

Sir, Government Customers are deducting GST TDS from the payment of bill amount. Such TDS can be utilized for payment of future GST liability. We do not have as much GST liability as much the amount of TDS deducted by govt.customers. Hence we applied for Refund of Excess Balance in March 2019 which is not approved as yet. Central Tax officers are saying this is a new type of claim and they are not aware of the procedure to settle this claim. How can we get the refund of excess cash balance.

If any registered person wrongly upload B2B tax invoice with GSTIN of A instead of B in GSTR1 then A is wrongly received it in GSTR2A, in next month registered person amend such invoice in GSTR1 and correct GSTIN of B then after B is received tax invoice in GSTR2A but error is that A is not received any intimation of amendment of such invoice in GSTR2A for the month of amended GSTR1 by registered person and also same invoice available in GSTR2A for the month of original GSTR1 uploaded month.

much much needed!

Why dont the governement dont understand the practical issues before implementing?

there are changes made again 15 days before, then they extend the form date at last week or last moment, which leads to non quality work!

This issue needs urgent attention!

CALCULATION OF INPUT REVERSAL IN CASE OF FINISHED GOODS – DATE EXPIRED FOR SALE AND FINISHED GOODS DRAINED