A. FAQs on Electronic Credit Ledger under GST

Q.1 What is an Electronic Credit Ledger?

Ans: In the Electronic Credit Ledger, all credits accrued on account of inward supplies made by a taxpayer within a tax period are accumulated. The ledger is maintained Major Head-wise, i.e., IGST, CGST, SGST, and CESS.

Q.2 Who maintains the Electronic Credit Ledger?

Ans: The Electronic Credit Ledger is maintained by the GST System.

Q.3 Where can the taxpayers view their Electronic Credit Ledger?

Ans: Taxpayers can view their Electronic Credit Ledger in the post login mode by logging on to the GST Portal. Path: Services > Ledgers > Electronic Credit Ledger

Q.4 Can a taxpayer view the Electronic Credit Ledger of another taxpayer?

Ans: No. An Electronic Credit Ledger can be viewed only by the taxpayers themselves or by the concerned Jurisdictional Officer (JO).

Q.5 How can the credit available in the Electronic Credit Ledger be utilized? Can a taxpayer utilize the credit available in one major head to pay tax liability under any other major head?

Ans: The amount available in the Electronic Credit Ledger can be utilized for paying of tax liabilities as per the following rules:

(a) IGST input tax credit shall first be utilized towards payment of IGST liability and the amount remaining, if any, may be utilized towards the payment of CGST, SGST/UTGST liabilities, in any order before utilizing the CGST, SGST/UTGST credit.

(b) CGST input tax credit shall first be utilized towards payment of CGST liability and the amount remaining, if any, may be utilized towards the payment of IGST liability. CGST credit shall be utilized only if IGST credit is not available.

(c) SGST/UTGST input tax credit shall first be utilized towards payment of SGST/UTGST liability and the amount remaining, if any, may be utilized towards payment of IGST liability (if no CGST credit is available). SGST/UTGST credit shall be utilized only if IGST credit is not available.

(d) CGST input tax credit cannot be utilized towards payment of SGST/UTGST liabilities and

(e) SGST/UTGST input taxed credit cannot be utilized towards payment of CGST liabilities.

Q.6 How can a taxpayer check the available balance in the Electronic Credit Ledger?

Ans: A taxpayer can login to the GST Portal and check the available balance on the landing page of the Electronic Credit Ledger.

Path: Services > Ledgers > Electronic Credit Ledger

Q.7 Can a taxpayer make debit entry in advance for the future liability in the Electronic Credit Ledger?

Ans: No, the Electronic Credit Ledger can be debited only against an existing tax liability.

Q.8 Can the amount available in the Electronic Credit Ledger be deemed as payment for any liability?

Ans: No, unless the taxpayer makes a debit entry from the Electronic Credit Ledger against a specific liability, the amount available in the Electronic Credit Ledger cannot be assigned to any liability.

Q.9 Can a Departmental Officer debit the Electronic Credit Ledger in case of outstanding dues?

Ans: Yes, in exceptional circumstances as permitted in the Act and rules, especially when the amount of additional demand is not stayed by the Appellate Authority, Tribunal, or Court, the credit can be debited to the extent of the demand by the proper officer.

Q.10 Is it necessary to claim refund of the excess amount available in the Electronic Credit Ledger?

Ans: No, the amount may continue to remain in the Electronic Credit Ledger and can be utilised for any future liability. Refund can only be claimed if ITC has been accumulated due to export of goods and/or services and/or due to rate of tax on outward supplies being lower than inward supplies.

Q.11 Can a taxpayer utilise the credit available in the Electronic Credit Ledger for purposes other than return liability?

Ans: Yes. Taxpayer can utilize the credit against other than return related liabilities as well. However, credit can be adjusted only against tax liability.

Q.12 Can I download the Credit Ledger?

Ans: Yes. You can download and save the Credit ledger from your dashboard in PDF and CSV format on your local machine.

Q.13 Where can I see my transitional credit?

Ans: You can see your transitional credit in the Electronic Credit Ledger. This is identified with a different description and reference.

Q.14 Where can I see the credit on transition from composition to normal taxpayer?

Ans: You can see your credit on transition from composition to normal taxpayer in the Electronic Credit Ledger.

Q.15 Electronic Credit Ledger is not maintained for which taxpayers?

Ans: Electronic Credit Ledger is not maintained for composition taxpayer, ISD taxpayer and Tax Deductor & E-commerce operator.

Q.16 Can I edit the Electronic Credit Ledger?

Ans: No, you cannot edit the Electronic Credit Ledger. You can ONLY view the details in the Electronic Credit Ledger.

Q.17 What is provisional credit table? What does it show?

Ans: Provisional credit tables display the balance of provisional and mismatch credit, tax period wise. Navigate to Services > Ledgers > Electronic Credit Ledger > Provisional Credit Balance link to view it.

Q.18 How a taxpayer can utilize credit available in Electronic Credit Ledger?

Ans: The credit available can be utilized to pay off the tax liabilities as per the utilization rules. Balance in credit ledger cannot be utilized for payment of fees, Penalty and interest.

Q.19 Can a GST Practitioner view my Credit ledger? Can I allow or deny access to my GST Practitioner to view my Credit ledger?

Ans: Yes, a GST Practitioner can view your Credit ledger who has been authorized by you. You can allow or deny GST practitioner to view your credit ledger by online engaging/disengaging a GST practitioner.

Q.20 Electronic Credit Ledger can be viewed for which period?

Ans: You can view the Electronic Credit Ledger for a maximum period of 6 months.

Q.21 Can cess be used to make payment of IGST/ CGST/ SGST/ UTGST?

Ans: No, Credit availed on CESS will be available for setoff against any output tax liability of CESS only. There is no Inter head adjustment for CESS Input Tax Credit.

Q.22 What is blocking or unblocking of ITC in Electronic Credit Ledger?

Ans: Jurisdiction Officer may scrutinize the amount of ITC claimed by a taxpayer, through GST TRAN-1 and GST TRAN-2 etc. for its authentication. The concerned Jurisdiction Officer may decide to temporarily block the ITC available to a taxpayer, wherever it is felt that further investigation is required, in the interest of the revenue. The Jurisdictional Officer may block CGST, SGST, IGST & Cess balance in whole or in part.

The Jurisdictional Officer after investigation may unblock the ITC that was previously blocked.

An email and SMS is sent to the taxpayer for blocking or unblocking of ITC

Q.23 Where can I view blocked credit balance?

Ans: Navigate to Services > Ledgers > Electronic Credit Ledger > Blocked Credit Balance to view the blocked credit balance.

Q.24 Can I perform intra-head or inter-head transfer of amount available in Electronic Cash Ledger?

Ans: Yes, you can perform intra-head or inter-head transfer of amount, as available in Electronic Cash Ledger, using Form GST PMT-09. Form GST PMT-09 enables any registered taxpayer to perform, intra-head or inter-head transfer of amount, as available in Electronic Cash Ledger. Thus, a registered taxpayer can now file Form GST PMT-09 for transfer of any amount of tax, interest, penalty, fee or others, under one (major or minor) head to another (major or minor) head, as available in the Electronic Cash Ledger.

Navigate to Services > Ledgers > Electronic Cash Ledger > File GST PMT-09 For Transfer of Amount option to file Form GST PMT-09.

Q. No. 25 is FAQ related to Creation of new UT of Ladakh and consequent changes on GST Portal for taxpayers

Q.25 I have received an intimation that a new GSTIN has been assigned to me for UT of Ladakh. What will happen to the Input Tax Credit left in my old GSTIN?

Ans: You may transfer the balance ITC available in old GSTIN, to the new GSTIN.

This can be done by reversing the ITC in Table 4(B)(2), of the last Form GSTR-3B filed for the old GSTIN and availing the same ITC in Table 4(A)(5) of the Form GSTR-3B filed for the new GSTIN.

Q. No. 26 is FAQ related to Merger of UT of Daman & Diu with UT of Dadra and Nagar Haveli and consequent changes on GST Portal for taxpayers

26. I have received an intimation that a new GSTIN has been assigned to me for UT of Dadra and Nagar Haveli and Daman and Diu. What will happen to the Input Tax Credit left in my old GSTIN?

Ans: You may transfer the balance ITC available in old GSTIN, to the new GSTIN.

This can be done by reversing the ITC in Table 4(B)(2), of the last Form GSTR-3B filed for the old GSTIN and availing the same ITC in Table 4(A)(5) of the Form GSTR-3B filed for the new GSTIN.

B. Manual on Electronic Credit Ledger under GST

1. How can I view the Electronic Credit Ledger?

The Electronic Credit Ledger enables the taxpayer to view the credit balance as on date and ledger details.

To view the Electronic Credit Ledger, perform the following steps:

1. Access the https://www.gst.gov.in/ URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials.

3. Click the Services > Ledgers > Electronic Credit Ledger command.

The Electronic Credit Ledger page is displayed. The credit balance as on today’s date is displayed.

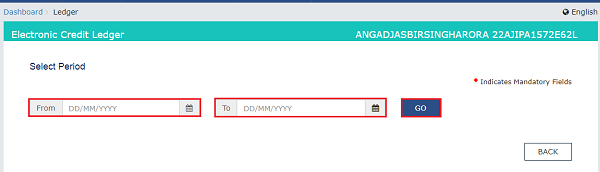

Electronic Credit Ledger:

4. Click the Electronic Credit Ledger link.

5. Select the From and To date using the calendar to select the period for which you want to view the transactions of Electronic Credit Ledger.

6. Click the GO button.

The Electronic Credit Ledger details are displayed.

Note: Click the SAVE AS PDF and SAVE AS EXCEL button to save the Electronic Credit Ledger in the pdf and excel format.

Provisional Credit Balance:

4. Click the Provisional Credit Balance link.

The Provisional Credit Balance details are displayed.

Note: Click the SAVE AS PDF and SAVE AS EXCEL button to save the Provisional Credit Balance in the pdf and excel format.

Blocked Credit Balance:

4. Click the Blocked Credit Balance link.

The blocked Credit Balance details are displayed.

Note: Click the SAVE AS PDF and SAVE AS EXCEL button to save the Provisional Credit Balance in the pdf and excel format.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

We are facing problem with GST Audit. We reversed the wrongly taken credit in 2018. and GST audit demanding for interest for utilization of wrongly taken ITC CGST. But fact is that we intend to keep the balance but at that time portal not allow to keep the CGST balance and zeroing the CGST Only then portal allow to go ahead to file the return. Hence after zeroing CGST amount the Total ITC reflected in SGST amount. Now Audit is asking for interest.

if we have only purchases for one company past 10 month and that ITC showing in credit ledger, now how long we can adjust this ITC against future sales

Hi,

how can I transfer CREDIT ledger balance from CGST/SGST to IGST Credit ledger. Please note that the question is about CREDIT ledger and NOT cash ledger

MY CGST INPUT BALANCE IS SO HIGH WHEREAS IN OFFSET OF GSTR 3B MY LIABILITIES COMES IN MY SIDE AS ABOUT 46000/- CAN I UTILIGED MY CGST BALANCE ( APP 500000/- ) WHERE IGST & SGST BALNCE IS NIL

Sir, please advise how to reconcile the refund claim and the balance ITC with books and portal as we are EOU and we go for refund after exports so now i want to reconcile with books and portal.

When amount of GST refund claimed will be deducted from electronic credit ledger ?

the balance available in the credit ledger electronic,

used by another GST No or account?

WE HAVE BALANCE OF PAID CA FEES IN CREDIT LEDGER & WE R APPLYING FOR CANCALLATION OF GST NO. WHAT WOULD BE MY STATUS OF CREDIT BALANCE AT THE TIME OF CANCALLATION ?

Thanx sir

it’s really useful information . Thanku so much for providing this knowledge .

Very useful FAQa

Sir, there is a mismatch of Opening amounts in the accounts and GST Electronic Credit Ledger. Can you please guide as to what entry can I pass in the current year so that my balance in books and portal match