Case Law Details

Phantom Studios India Private Limited Vs EROS International Media Limited (NCLT Mumbai)

The National Company Law Tribunal (NCLT), Mumbai Bench, dismissed a petition filed under Section 9 of the Insolvency and Bankruptcy Code, 2016 (IBC) seeking initiation of the Corporate Insolvency Resolution Process (CIRP) against Eros International Media Limited for an alleged operational debt of ₹1,48,28,902. The Tribunal held that the claim did not qualify as an “operational debt” under Section 5(21) of the IBC because it arose from a joint venture and profit-sharing arrangement rather than from the provision of goods or services.

The dispute arose from a Term Sheet dated 11.02.2013 and a Film Co-Production Agreement dated 17.12.2013 for the co-production of the Hindi film NH-10. Under the agreement, the Corporate Debtor was responsible for funding, distributing, exploiting, and marketing the film, while the producer was responsible for production-related activities. The parties also agreed to jointly bear the lead artist’s fee of ₹1.25 crore, contributing ₹62.50 lakh each, with the amount to be recouped from film revenues under the agreed recoupment mechanism. The producer’s rights were subsequently assigned to the petitioner through consent terms, a deed of novation, and related agreements.

The petitioner relied on a letter dated 14.03.2024, signed by both parties, recording that a net amount of ₹1,25,66,866, comprising ₹62.50 lakh towards principal and ₹63,16,866 towards agreed interest, was payable from revenues generated by the film and was to be paid on or before 30.06.2024. After repeated reminders seeking payment of the admitted dues, applicable GST, and a debit note, the petitioner issued a demand notice upon non-payment and contended that there was no pre-existing dispute because the liability had been expressly acknowledged.

The Corporate Debtor opposed the petition on multiple grounds. It argued that the claim did not arise from the supply of goods or services and therefore fell outside the scope of operational debt under Section 5(21). It also contended that a portion of the claim was barred by limitation, as certain amounts had become due between 2016 and 2018. Additionally, it claimed a right of set-off against an alleged debt recoverable from Supernova Entertainment Private Limited, asserting that both entities were under the same management.

After examining the Term Sheet, Film Co-Production Agreement, and related documents, the Tribunal found that the parties had undertaken a common commercial venture for producing the film. The agreement required the producer to carry out production activities while the Corporate Debtor financed, marketed, distributed, and exploited the film. Both parties jointly contributed towards the lead artist’s fee, agreed upon a structured recoupment mechanism, shared intellectual property rights, and were entitled to share profits equally after recoupment of production costs. The Tribunal observed that these features demonstrated a joint venture arrangement involving shared investment, common commercial objectives, reciprocal rights and obligations, joint control over significant aspects of the project, and profit-sharing.

Relying on the decision of the National Company Law Appellate Tribunal (NCLAT) in Prashant Shekara Shetty v. Alcuris Healthcare Private Limited, the Tribunal held that claims arising from profit-sharing or joint venture agreements do not constitute operational debt under the IBC. It also referred to its earlier decision in Gutz Feel Film Production LLP v. Eros International Media Limited, where a similar revenue-sharing arrangement in the film industry had been held not to give rise to an operational debt. The Tribunal distinguished the judgments relied upon by the petitioner on the ground that the facts of those cases were different.

The Tribunal concluded that although money may be payable by one party to another, the contractual relationship between the parties determines whether the claim qualifies as an operational debt. Since the relationship in the present case was that of a joint venture rather than that of an operational creditor and corporate debtor, the claim did not fall within Section 5(21) of the IBC. Having reached this conclusion, the Tribunal found it unnecessary to examine the issues of limitation or set-off and dismissed the Section 9 petition. It further observed that the IBC cannot be used as a mechanism for recovery of money or to compel payment.

FULL TEXT OF THE NCLAT JUDGMENT/ORDER

1. This Petition has been filed by Phantom Studios India Private Limited (‘Petitioner/ Operational Creditor’) to initiate Corporate Insolvency Resolution Process (‘CIRP’) against EROS International Media Limited (‘Respondent/Corporate Debtor’) under Section 9 of the Insolvency and Bankruptcy Code, 2016 (‘the Code’) read with Rule 6 of the Insolvency and Bankruptcy (Application to Adjudicating Authority) Rules, 2016 for a default of 1,48,28,902/- (Rupees One Crore, Forty Eight Lakhs, Twenty Eight Thousand, Nine Hundred and Two only) as on 01.07.2024.

2. Brief Facts

2.1 A term sheet was executed between the Eclatant Films Private Limited (earlier known as Phantom Films Production Private Limited) and Corporate debtor on 11.02.2013, wherein the parties agreed to co-produce four full length cinematography films on terms and conditions set out therein.

2.2 Pursuant thereto, the Corporate Debtor entered into a Film Co-Production Agreement dated 17.12.2013 (‘Film Co-Production Agreement’), with Eclatant Films Private Limited (Phantom Films Production Private Limited), for the co-production of the cinematography film in Hindi titled as NH-10 (‘Film’), under which the Corporate Debtor was to exploit the Film and the revenues therefrom were to be divided as per the Film Co-Production Agreement.

2.3 An Addendum Letter dated 15.01.2014 was executed between the Corporate Debtor and Eclatant Films Private Limited (Phantom Films Production Private Limited) by which Eclatant Films Private Limited was entitled to assign half of its share in the rights of the Film to Clean Slate Films Private Limited.

2.4 Thereafter, an addendum agreement dated 05.03.2015 was entered between the Corporate Debtor and Eclatant Films Private Limited (Phantom Films Production Private Limited) entered by which the budget of the Film was revised from Rs. 9,40,00,000/- to Rs. 10,03,77,071/-.

2.5 By an order dated 08.12.2021, the Hon’ble High Court of Bombay, took on record the consent terms dated 06.12.2021 in Execution Application No. 27808 of 2021 wherein the Eclatant Films Private Limited, inter- alia, assigned all rights in the film to Mad Man Films Ventures Private Limited now known as Phantom Studios India Private Limited (‘Petitioner’).

2.6 Eclatant Films Private Limited (Phantom Films Production Private Limited) under a Deed of Novation Cum Amendment dated 27.01.2022 irrevocably, absolutely and unconditionally assigned, transferred all its rights and obligations in the Film under the Film Co-Production Agreement and the Addendum Agreement dated 05.03.2013 to the Petitioner.

3. Submissions by the Petitioner

3.1 It is submitted that on 14.03.2024, the Petitioner issued a letter to the Corporate Debtor, stating that an amount payable by the Corporate Debtor for the amount generated by the Corporate Debtor, from the revenues generated from the exploitation of the Film is Rs.1,25,66,866/-, The said letter was signed and executed by the Petitioner as well the Corporate Debtor.

3.2 Mr. Kamlakar Kesarkar, director of the Petitioner vide email dated 17.04.2024, requested the Corporate Debtor to clear the GST payments amounting to Rs. 22,22,768/- on or before 19.04.2024. By the said email, the Petitioner also requested the Corporate Debtor to clear the admitted dues i.e. a sum of Rs. 1,25,66,866/ – on or before 30.06.2024.

3.3 The Petitioner once again vide email dated 25.06.2024 requested the Corporate Debtor, to clear GST payment of Rs. 22,22,768/- pending since 20.04.2024. The Petitioner also requested the Corporate Debtor to clear the admitted dues of Rs.1,25,66,866/- as per the letter dated 14.03.2024 prior to 30.06.2024.

3.4 The Corporate Debtor vide letter dated 28.06.2024 requested the Petitioner and Supernova Entertainment Private Limited (earlier known as Mojostar Brand Management Merchandising), to set off the amount of Rs. 1,25,66,866/- admittedly owed by the Corporate Debtor to the Petitioner, against the alleged debt of Rs. 1,40,00,000/- of September 2018, claimed to be due and payable from Supernova Entertainment Private Limited to the Corporate Debtor in a completely independent transaction.

3.5 The Petitioner vide its letter dated 29.06.2024 unequivocally rejected the request of the Corporate Debtor and once again reiterated that the Corporate Debtor is bound to pay the amount of Rs.1,25,66,866/- along with applicable GST of Rs. 22,22,768/- on or before 30.06.2024.

3.6 Further, vide letter dated 30.06.2024 Supernova Entertainment Private Limited, also rejected the request of setoff made by the Corporate Debtor vide letter dated 23.06.2024.

3.7 The Petitioner on 30.06.2024 issued a debit note bearing no. DN/2024-25/001 for Rs. 2,57,418/-. Despite sending multiple reminders the Corporate Debtor failed to make payment hence the Petitioner issued a Demand Notice dated 01.07.2024.

3.8 It is submitted that the Corporate Debtor has never disputed its liability rather has admitted its liability vide letter dated 14.03.2024 and 25.06.2024 therefore there is no pre-existing dispute.

4. Submission by the Corporate Debtor:

4.1 The Petitioner has not supplied any goods or services to Corporate Debtor, and therefore the amount claimed by the Petitioner is beyond the scope of Operational Debt as defined in Section 5(21) of the Code.

4.2 Out of the principal amount of Rs. 62,50,000/-, a claim for Rs. 33,27,639/- and corresponding interest thereon amounting to Rs. 36,12,084/- is barred by limitation.

4.3 As required under Clause 17 of the Film Co-production Agreement dated 17.12.2013, Corporate Debtor had sent quarterly business statement to Petitioner vide emails, the amounts payable and due date thereon reflects as follows:

| Business

Statement as on |

Amount reflected payable (₹) | Due date of payment by Corporate Debtor |

| 30.09.2016 | 33,27,639/- | 30.09.2016 |

| 31.03.2017 | 07,91,145/- | 31.03.2017 |

| 31.12.2017 | 10,13,728/- | 31.12.2017 |

| 31.03.2018 | 11,17,488/- | 31.03.2018 |

| Total | 62,50,000/- |

4.4 Each of the payments became due on the dates mentioned in the above table, therefore Petitioner is claiming interest of Rs.63,16,866/- from the due date till 30.06.2024 @14% per annum.

| Amount | Interest from | Interest till | No. of

days |

Interest @14% p.a |

| 30.09.2016 | 30.09.16 | 30.06.24 | 2830 | 36,12,084/- |

| 31.03.2017 | 31.03.17 | 30.06.24 | 2648 | 8,03,543/- |

| 31.12.2017 | 31.12.17 | 30.06.24 | 2373 | 9,22,687/- |

| 31.03.2018 | 31.03.18 | 30.06.24 | 2283 | 9,78,552/- |

| 62,50,000/- | Total | 63,16,866/- | ||

4.5 It is further submitted that principal payment of Rs. 33,27,639/- for quarter ending 30.09.2016, became due on 30.09.2016 and therefore Petitioner had to claim said payment within the period of limitation i.e. by 30.09.2019. The present Petition is filed on 12.07.2024.

4.6 The Petitioner’s limitation for seeking recovery of aforesaid amount of Rs.33,27,639/- was never extended under Section 18 or Section 19 of the Limitation Act as the Corporate Debtor has never acknowledged the liability to pay the said amount during the period of limitation nor has made any part payment or acknowledged the liability.

4.7 The Corporate Debtor had advanced a sum of Rs. 1,40,00,000/- to Supernova Entertainment Private Limited (formerly known as Mozostar Brand Management & Private Limited) through Cheque No.916269 dated 31.07.2018 for Rs.70,00,000/- drawn on Indian Overseas Bank and Cheque No.560840 dated 06.09.2018 for Rs. 70,00,000/- drawn on IDBI Bank towards refundable/adjustable advance.

4.8 It is submitted that Mr. Madhu Mantena is the Ultimate Beneficial Owner of Supernova Entertainment Private Limited as well as the Petitioner. The relevant details in this regard are reproduced here in under: –

| Name of

Company |

Name of Directors | Name of shareholder | Shareholding % |

| Supernova Entertainment Private Limited | Suresh Shankar Mandapeli,

Kamlakar Babu Kesarkar |

Kwan Media Ventures Pvt. Ltd.

Madhu Mantena (nominee of Kwan Media) |

98.79%

1.21% |

| Kwan Media Ventures Private Limited | Suresh Shankar Mandapeli,

Kamlakar Babu Kesarkar

|

Kwan Celebrity Advisory Services Pvt. Ltd.

Madhu Mantena (nominee of Kwan Celebrity) |

97%

3% |

| Kwan Celebrity Advisory Services Private Limited | Suresh Shankar Mandapeli,

Kamlakar Babu Kesarkar |

Kwan Securities Private Limited

Bimal Parekh Vijay Subramaniam Dhruv Chitgopekar |

90%

2% 4% 4% |

| Kwan Securities Private Limited | Suresh Shankar Mandapeli, Kamlakar Babu Kesarkar | Big Bang Media Ventures Pvt. Ltd

Madhu Mantena (nominee of Big Bang) |

51%

49% |

| Phantom Studios India Private Limited | Kamlakar Babu Kesarkar, Sushil Kamalakar Garud | Big Bang Media Ventures Pvt. Ltd.

Kamlakar Babu Kesarkar. WSG Entertainment LLP Purab Entertainment LLP Vistaar Investment Holdings Limited |

93.93%

0% (1 share) 2.55% 0.22% 3.29% |

| Big Bang Media Ventures Pvt.Ltd. | Madhu Mantena, Ashwatha Aaron Naik, Ravneet Singh Gill, Manmohan Ramanna Shetty. | Madhu Mantena Ashwatha Aaron Naik Ravneet Singh Gill | 98.99%

1% 0.1% |

4.9 It is submitted that Corporate Debtor is entitled to set-off the amount payable to Petitioner from the amount recoverable from Company under same Management i.e. Supernova Entertainment Private Limited. The Corporate Debtor has also filed a separate application before this Tribunal for commencement of Corporate Insolvency Resolution Process against Supernova Entertainment Private Limited for its default in payment of above-mentioned amount of Rs.1,40,00,000/-.

5. Rejoinder on behalf of the Petitioner:

5.1 It is submitted that the present petition arises from the letter dated 14.03.2024 which is in furtherance of film production agreement dated 17.12.2013, whereby the Corporate Debtor promised to pay a sum of Rs.1,25,66,866/- to the Petitioner. Thus, the question being barred by limitation does not arise in light of Section 25 of the Indian Contract Act 1872.

5.2 Section 25(3) of Contract act makes it clear that an agreement without consideration is not void if it is a promise made in writing and signed by a person to pay whole or a part of debt which the creditor might have enforced payment for the law for limitation.

5.3 The amount claimed by the Petitioner is within the scope of Operational Debt as defined in Section 5(21) of the Code.

5.4 The present matter does not pertain to cross-recoveries between two Corporate Groups and Mr. Madhu Mantena doesnot exercise complete control over the Petitioner. The Petitioner is a separate legal entity and its claim arising from letter dated 14.03.2024 cannot be set off against the alleged claim of the Corporate Debtor against Supernova Entertainment Private Limited. There is no case made out for piercing of the corporate veil the corporate debtor is free to exercise its remedies against Supernova Entertainment Private Limited.

5.5 The Petitioner states that it is neither privity to the agreement nor is aware about the disputes between the Corporate Debtor and Supernova Entertainment Private Limited. Nonetheless, assuming without admitting that there is sum due and payable by Supernova Entertainment Private Limited does not have any bearing on the present petition.

FINDINGS AND OBSERVATIONS

6. Heard Ld. Counsel for the parties and perused the material placed on record.

7. It is the case of the Petitioner that:

i. The operational debt of Rs. 1,48,28,902/- arises from the services provided by the Petitioner under the Film Co-Production Agreement dated 17.12.2023 read with the letter dated 14.03.2023 recording the payment of dues on or before 30.06.2024.

ii. The amount claimed by the Petitioner falls within the ambit of operational debt.

iii. The present petition is not barred by limitation.

iv. The Corporate Debtor is not entitled to set off the operational debt owed to the Petitioner.

8. Refuting the submissions made by the Petitioner the Corporate Debtor has submitted that: –

i. The amount claimed by the Petitioner is outside the scope of operational debt under Section 5(21) of the Code.

ii. The Petition, claim of Rs. 33,27,639/- with interest thereon amounting to Rs. 36,12,084/- is barred by Limitation.

iii. The Corporate Debtor is entitled to set off the Operational debt owed to the Corporate Debtor against the alleged dues recoverable by it from an alleged group company of the Petitioner.

9. Taking into consideration the submissions made by the parties the points arising for determination are:

i. Whether the amount claimed by the Petitioner falls within definition of operational debt under Section 5(21) of the Code?

ii. If yes then, whether the Petition is barred by Limitation?

iii. Whether the Corporate Debtor is entitled to set off the operational debt?

I. Whether the amount claimed by the Petitioner falls within the definition of operational debt?

10. The Petitioner has submitted that it was agreed between the parties that, only after complete recoupment of the production costs (as per clause 5.3 of film production Agreement), the net profits arising from the exploitation of the Film would be shared between the parties in the ratio of 50:50. Further, it was submitted that as per clause 3.1 and 2.1 of the Film Co-Production Agreement that the Corporate Debtor was merely a financial investor and the Petitioner was a service provider and that the profit-sharing arrangement, if any, could be triggered only after the production costs are recouped. Until that point, there was no question of ‘profit share’. It was also submitted that the Corporate debtor vide order email dated 14.03.2024 had acknowledged to pay the said debt out of the revenues generated therefore the present debt was an operational debt. The Petitioner to contend that present debt is an operational debt has further relied on the following case laws: –

i. Consolidated Construction Consortium Ltd vs Hitro Energy Solutions Pvt. Ltd; 2022 SCC online SC 142 wherein the Hon’ble Supreme Court allowed the appeal and held that that Advance payments made for the supply of goods or services constitute “operational debt” and observed that for a claim to be considered as an operational debt under Section 5(21) of IBC, it ought to have some nexus with provision of goods or services.

ii. Manoj Stone Infra Pvt. Ltd v. Railways Engineers, Company Appeal (AT) (Insolvency) No. 763 of 2023 wherein the Hon’ble NCLAT considered whether debt arising from profit sharing agreement could qualify as an operational debt and held that for a claim to qualify as operational debt, it must arise out of the provision of goods or services between the parties.

iii. Somesh Choudhary v. Knight Riders Sports Pvt. Ltd, Company Appeal (AT) (Insolvency) No. 501 of 2021 wherein the Hon’ble NCLAT considered whether nonpayment of minimum guaranteed royalties under licensing agreement would fall within the meaning of operational debt.

iv. Kotak Mahindra Bank Ltd v. Kew Precision Parts (P) Ltd; (2022) 9 SCC 364 wherein the Hon’ble Supreme Court held that a one-time settlement proposal does not revive a time-barred debt unless it contains a clear written promise to pay, as required under Section 25(3) of the Contract Act and that any agreement to pay a time barred debt would be enforceable in law, within three years from the due date of payment.

11. The Corporate Debtor to contend that the present debt is not an operational debt has placed reliance on Film Co-production agreement dated 17.12.2023 and has stated that the Agreement is nothing but a profit-sharing agreement as the Petitioner has not supplied any goods and services to the Corporate debtor but has merely raised invoices for recoupment which is different from cost of goods and services.

12. The Corporate Debtor in support has placed reliance on the following case laws wherein it was held that investment in joint venture and revenue sharing cannot be an operational debt:

i.B4U Broadband (India) Private Limited vs Kyta Productions Private Limited CP (IB) 637/MB/2020 wherein NCLT held that investment in a joint venture for film production with revenue sharing is not a claim arising from supply of goods or services, and therefore cannot be treated as operational debt under Section 5(21) of the IBC. The NCLT Mumbai Bench dismissed the petition, holding that the claim does not constitute operational debt.

ii. Prashant Shekara Shetty vs Alcuris Healthcare Private Limited, Company Appeal (AT) (Ins) No. 359 of 2022 & I.A. No. 1321 of 2022, the Hon’ble NCLAT allowed the appeal and set aside the NCLT order admitting the Section 9 petition and initiating CIRP holding that a claim arising from breach of a profit-sharing or joint venture agreement cannot be treated as operational debt under the IBC.

13. Other case laws submitted by the Corporate Debtor in its compilation of case laws:

i. Global Credit Capital Limited vs Sach Marketing Private Limited (2024) 9 SCC 482;

ii. Parul vs Vora vs Kavya Buildcon Pvt Ltd, CP (IB) 2832/MB/2019;

iii. Bharti Airtel Ltd & Anr Vs. Vijaykumar V.Iyer & Anr (2024) 4 SCC 668.

iv. Vidhyasagar Prasad vs UCO 2024 SCC Online SC 2993.

14. In order to establish whether the said debt is operational debt or not it would be important to peruse the clauses of the Term Sheet dated 11.02.2013 and Film Co-Production agreement dated 17.12.2013. We note that as per term sheet dated 11.02.2013 and Clause 3.1 and 2.1 of the Film Co-Production Agreement dated 17.12.2013, the Petitioner was to produce and deliver the film and the Corporate Debtor was to finance, exploit and distribute the film. The Role of the Petitioner (‘Producer’) and Corporate Debtor as per the term sheet dated 11.02.2013 is reproduced as follows:

i. First Copy of the Films to be delivered to Eros by Producer All costs till such date shall be spent on behalf of Eros by the Producer as per the cash flow facilitated by Eros to the Producer.

ii. The Producer shall be responsible for all the production related activities but not limited to Music, Post production upto First Copy, engagement of cast etc.

iii. Producer will be responsible for execution of all agreements including but not limited to all production/artist/crew cast director/ music director and other agreements. The lead cast and director agreements will be tripartite between Eros Producer and the individual.

(Emphasis Provided)

15. Further the role of the Corporate Debtor was as follows:

i. Eros will fund the cost of production.

ii. Eros will distribute, market and exploit the film.

16. Further, Clause 2.1 and 3.1 of the film production agreement are reproduced below:

2.1 All Rights in the said Film as stated in clause 1.1.23 throughout the world shall be exclusively distributed, exploited and dealt with and by EROS.

3.1 The Budget of the said film shall be defrayed and disbursed by Eros by cheques in suitable installments and tranches to PFPPL in accordance with approved Budget, Production Reports, Production Schedule and progress of the said Film Cash Flow Schedule for funding the production and Completion of the said Film including all disbursals and payments to third parties, performers, artists, suppliers, vendors and other persons connected with the Production and Completion of the said Film.

17. We note that Clause 1.1.2 and 1.1.3 elucidated budget in the Film Co-production Agreement dated 17.12.2013. Further under Clause 1.1.3 (a) and 1.1.3 (A) i.e. the budget excluded the fees of Rs. 1.25 crores of the Lead Artist, Anushka Sharma. The said fees were to be equally borne and funded by Eclatant (earlier known as Phantom Films Production Private Limited who later assigned all rights in the film to the Petitioner) and the Corporate Debtor. The said contribution was to be later recouped by the parties from the revenues generated in accordance with the recoupment mechanism set out in clause 5.3 of the Agreement. The Clause 1.1.3(a) and 1.1.3(A) are reproduced as under:

1.1.3 The Budget for cost of production of the said Film in Clause 1.1.2 shall include but shall not be limited to the following:

a) the fees to be paid to all Artists excluding the Artist Fee of Ms. Anushka Sharma but including the fees of other Lead Artists of the said Film and all payments to performers, contributors and all other persons connected with the production and development of the said Film including Director’s Fee & Writer’s Fee.

1.1.3 A. The Budget of the said Film in Clauses 1.1.2/1.1.3 above shall exclude the Artist Fee of one of the Lead Artists of the said Film, Ms. Anushka Sharma @ a maximum of Rs.1.25 Crore which shall jointly and equally be borne, paid and funded by the Parties hereto i.e. Rs.62.50 Lakh by Eros and Rs.62.50 Lakh by PFPPL (hereinafter referred to as Eros share of Artist Fee and PFPPL Share of Artist Fee respectively) and which shall be recouped by the Parties as per Clause 5.3 hereto.

(Emphasis Provided)

18. We note that, Clause 5 of the Film Co-production Agreement 17.12.2013 stipulated recoupment mechanism by the Corporate Debtor. It was agreed that after complete recoupment of the production costs, the net profits arising from the exploitation of the Film would be shared between the parties in the ratio of 50:50. Clause 5 of the Film Co-production Agreement is reproduced herein under:

“5. Recoupment: EROS shall, from all revenues in Clause 1.4.22 accrued from exploitation of all copyright and all other Rights of the said Film as stated in Clause 1.1.23 be entitled to recoup the following in the following order:

5.1 Firstly, EROS shall recoup all taxes, costs, charges, insurance premium on policy on Agreement for distribution and loss of profit, and all expenses for exhibition exploitation and distribution of all said rights in the said Film throughout the world, including but not limited to expenses towards prints, publicity, marketing, advertising and freight and transportation expenses and all other expenses including stamp duty incurred by EROS in respect of the said Film.

5.2 Secondly, EROS shall recoup the entire Budget and/or such amounts actually expended by EROS in respect of the said Film.

5.3 Thirdly, Eros and PFFPL shall recoup their respective share of the Artist Fee as stated in Clause in 1.1.3 A hereof.

5.4 Fourthly, PFPPL shall recoup the Loss stated in Clause 1.1.25A in the manner set out therein.

5.5 Fifthly, EROS shall recoup 15% distribution commission on all Gross Revenues from exploitation of all the Rights in the Said Film excluding satellite Rights for India on which commission shall be @10%.

5.6 Sixthly, Eros shall recoup interest @ 14% p.a. to be calculated on the entire Budget from the date of disbursement of all amounts till the date of release of the said Film and PFPPL shall, recoup 10% PFPPL Production Fee in Clause 1.1 .4.

5.7 After recoupment and appropriation of the amounts mentioned from Clause 5.1 to 5.6 above for the said, Film thereafter all monies, revenues, income, recoveries and realizations receivable (“Profits”) shall be shared between EROS and PFPPL in the ratio of 50:50 i.e. 50% by EROS and 50% by PFPPL.

(Emphasis Provided)

19. We note that the Petitioner has relied upon letter dated 14.03.2024 and has stated that it was mutually agreed that the Corporate Debtor would pay a net sum of Rs. 1,25,66,866/- on or before 30.06.2024. The relevant extracts of the letter dated 14.03.2024 are reproduced as under:

We confirm that as per the business statements submitted by Eros in relation to the Film upto 31st March 2023 and duly accepted by us, a net amount of INR 1,25,66,866/- (Indian Rupees One Crore Twenty Five Lakhs Sixty Six Thousand Eight Hundred and Sixty Six Only) [consisting of INR 62,50,000/- principal amount and the agreed interest of INR 63,16,866/-], is payable by Eros to us from the revenues generated out of the Film (“Amount Payable”), which shall be paid by Eros to us on or before 30th June 2024 (“Due Date”). It is agreed that all applicable taxes on the principal amount will be payable additionally by Eros and the payment of the Amount Payable will be subject to deduction of TDS. Eros agrees and confirms to make the payment of the Amount Payable to us on or before the Due Date.

You are requested to kindly confirm the above by appending your signature hereto.

Yours Truly,

For, Phantom Studios India Private Limited

We agree, accept and confirm the above

For, Eros International Media Limited

Name: Kamlakar Kesarkar

Designation: Director

Name: Vijay Thaker

Designation Director

20. We note that pursuant to letter dated 14.03.2024, the Petitioner has raised invoices and Debit Note for recoupment of NH-10 Film. The relevant extracts of the invoice and debit note are reproduced below:

–

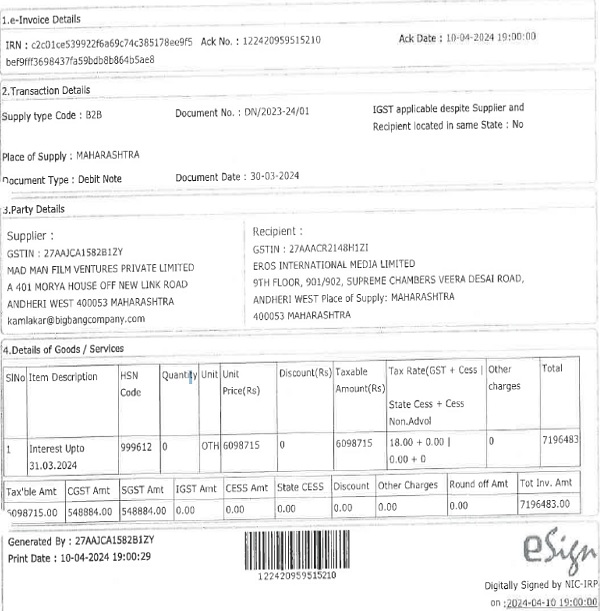

21. It is evident that the Petitioner issued an Invoice dated 30.03.2024 bearing no. 2023/2024 for a total amount of Rs. 73,75,000/- which included principal amount of Rs.62,50,000/- and GST amounting to Rs.11,25,000/- whereas Debit Note dated 30.03.2024 was raised for a total amount of Rs.71,96,483/- which included Interest upto 31.03.2024 amounting to Rs.60,98,715/- along with GST amounting to Rs. 10,97,768/- upon the Corporate Debtor.

22. Further, a plain reading of Film Co-production Agreement clearly shows that after recoupment of Production Cost, the parties had agreed to share profits arising from the exploitation of cinematographic rights in the ratio of 50:50. However, artist fees paid to Lead Artist Ms. Anushka Sharma were to be jointly and equally borne by both the parties and then recouped from the revenues generated. The Petitioner has submitted that the Corporate Debtor appropriated and paid itself its share of Rs. 62.50 lakhs from the revenues generated but has defaulted in paying share of Rs.62.50 lakhs to the Petitioner.

23. In order to see whether expenses incurred by the Petitioner towards artist fees constitutes operational debt or not, it would be relevant to refer to the definition of Operational debt.

24. We note that Section 5(21) of the Code defines “operational debt” by reference to a claim in respect of the provision of goods or services including employment or debt in respect of repayment of the dues arising under any law for the time being in force and payable to the Central Government, any state government or any local authority. For determining whether a particular claim constitutes an operational debt, what is material is the nature of the transaction giving rise to such a claim.

25. From the perusal of invoices, it is evident that the Petitioner has raised invoices claiming recoupment from the revenue generated from the exploitation of the cinematographic rights. It was clearly stated in Clause 1.1.3 A of the film production agreement that the parties will bear Artist fees 50:50 i.e. Rs.62.50 Lakh by the Petitioner and Rs.62.50 Lakh by the Corporate Debtor.Therefore, it is necessary to determine whether sharing of Artist fees 50:50 i.e. in equal proportion tantamount to Joint Venture between the Parties.

26. According to Black’s Law Dictionary, Tenth Edition, a joint venture is defined as:

“A business undertaking by two or more persons engaged in a single defined project. The necessary elements are: (1) an express or implied agreement, (2) a common purpose that the group intends to carry out, (3) shared profits and losses (4) each member’s voice in controlling the project.”

27. As noted earlier, the Petitioner and Corporate Debtor entered into agreement for production of movie NH-10. The term Sheet dated 11.02.2013 and Film Co-Production Agreement dated 17.12.2013 were executed which defined roles and responsibilities of both the parties. It was agreed that only after complete recoupment of the production costs, the net profits arising from the exploitation of the Film would be shared between the parties in the ratio of 50:50. Further, Clause 1.1.3 (a) and 1.1.3 (A) i.e. budget excluded the fees of the Lead Artist (Ms. Anushka Sharma) of Rs.1.25 crores. The said fees were to be equally borne by both the parties and recouped later from the revenue generated.

28. A perusal of the aforesaid arrangement demonstrates that the nature of the transactions entered into between the parties were not that of a Vendor and Vendee. The parties were bound by the Term sheet dated 11.02.2013 and Film Production Agreement dated 17.12.2013. The parties pursued a common commercial objective of producing the Film NH-10, and exercised effective joint control on factors like production cost, Production period, release date etc, which were to be mutually decided by both the parties. The parties had defined scope of work and were to contribute in the ratio of 50:50 towards lead artist’s fees in the. Moreover, it was also agreed between the parties that after complete recoupment of the production costs, the net profits arising from the exploitation of the Film would be shared between the parties in the ratio of 50:50 and IPR of the films werealso to be equally shared by both the parties in ratio of 50:50. These features are indicative of a joint venture arrangement between the parties.

29. As the nature of relationship between the parties is that of joint venture, the debt even if owed by the Corporate Debtor to the Petitioner the same cannot be considered as an ‘operational debt’ within the meaning of 5(21) of the Code.

30. In the case of Prashant Shekara Shetty vs Alcuris Healthcare Private Limited, Company Appeal (AT) (Ins) No. 359 of 2022 & I.A. No. 1321 of 2022, the Hon’ble NCLAT has held that claim arising from breach of a profit-sharing or joint venture agreement cannot be treated as operational debt under the IBC. The relevant extracts of the order are reproduced below:

“28. In the present matter, the clauses of the agreement entered between the two parties, who are described as “general profit-sharing partners” therein, furnish the key to the minds of the makers of this agreement. The clauses of the agreement disclose an intent that both parties shall exercise joint control over the SRV Heart Centre and will be accountable to each other for their respective acts with reference to the functioning of the Cathlab. We also note that both the parties also combined their investments, property, efforts, resources, skill and knowledge in this unit. There are unmistakeable signs of reciprocal rights and obligations contained in the agreement besides evidence of common participation/joint control in the management as well as sharing of profits and losses. When shared control of interest or enterprise and shared liability for profit and losses is so clearly manifested, it cannot be denied that both parties are implicit partners and co-adventurers in the Cathlab venture rather than one being a consumer and the other a service provider. From the material on record, facts and circumstances there arises no clear or unambiguous jural relationship between the two parties as one of Corporate Debtor and Operational Creditor. Rather both the Corporate Debtor and Respondent No. 1 are like the principal as well as the agent of the other party. This spirit is not only captured in the body of the agreement but also demonstrated in the actions and conduct of both parties in their role as “general profit-sharing partners”. Thus, for the above reasons, we are not inclined to agree with the contention of the Respondent No. 1 that the outstanding amount so claimed constitutes an operational debt under the IBC. As we hold that the claim is not in the nature of Operational debt, we need not go further to examine whether there was any default in respect of a debt which had become due and payable and whether it was laced with pre-existing dispute.

29. With the aforesaid discussion, we are of the considered view that the Adjudicating Authority has erroneously admitted the application under Section 9 of the IBC. We therefore set aside the impugned order. The orders passed by the Adjudicating Authority initiating CIRP against the Corporate Debtor and appointing Interim Resolution Professional and all other orders pursuant to impugned order are declared illegal and set aside. The Corporate Debtor company is released from the rigours of CIRP and is allowed to function independently through its board of directors with immediate effect. The appeal is allowed with the aforesaid observations. With this IA No. 1321 of 2022 also stands disposed of. No order as to costs.

31. We also note that in the matter of Gutz Feel Flim Production LLP vs Eros International Media Limited CP No.670 of 2024 dated 08.04.2026 the NCLT Mumbai Bench II in similar facts and circumstances has held that joint venture agreement cannot constitute Operational Debt under Section 5(21) of the Code. The relevant extracts of order dated 08.04.2026 is reproduced as under:

15. Thus, the profit from the revenue-sharing arrangement cannot be equated with an operational debt, and the agreement is essentially in the nature of a joint venture cannot be construed as service or goods supplied to the Respondent by any stretch of imagination. At best, it can be termed as recoverable amount, which can be agitated before the Civil Court leading document and evidence etc.

32. Further, the judgements submitted by the Petitioner do not aid the case of the Petitioner as the facts and circumstances in those cases are distinguishable from the facts of the present case. The Petitioner via this petition is seeking recovery of amount in default. IBC cannot be used as a tool for recovery or as a lever to coerce payment. Accordingly Issue No.1 is answered in negative.

Conclusion

33. Even if money is owed by one party to another the nature of the relationship between the parties, based on the contract between them, plays a significant role in determining whether a debt can be considered as an operational debt.

34. As in the facts and circumstances of present case the dues claimed by Petitioner do not constitute an operational debt within the meaning of Section 5(21) of the Code, as discussed above, this Tribunal does not deem it necessary to examine other aspects of this case.

35. Accordingly, C.P. No. (IB) 598/MB/C-III/2024 is dismissed.

Author Bio