Case Law Details

ACIT Vs Hariom Mobile Private Limited (ITAT Delhi)

Price Drop Losses Allowed Because Distributor Bore Unreimbursed Margin Loss; ITAT Deletes AMP Disallowance Because Advertisement Expenses Were for Distributor’s Own Business; Section 37 Deduction Allowed Because AMP Expenses Were Not Reimbursed by Brand Owner; ITAT Upholds Deletion of Price Drop Disallowance Because Commercial Loss Was Genuine.

The Income Tax Appellate Tribunal (ITAT), Delhi, dismissed the Revenue’s appeals for Assessment Years 2019-20 and 2020-21 and upheld the orders of the Commissioner of Income Tax (Appeals) [CIT(A)] deleting disallowances relating to advertisement, marketing and brand promotion (AMP) expenses and price drop expenses claimed by the assessee, a Super Authorised Distributor (SAD) of OPPO mobile phones. The assessee’s cross-objections were dismissed as not pressed.

For AY 2019-20, the Assessing Officer (AO) had disallowed ₹11,55,11,349 towards AMP expenses under Section 37(1), holding that the expenditure was either reimbursed by OPPO Mobile India Pvt. Ltd. (OMIPL) or incurred for the exclusive benefit of the brand owner. The AO also disallowed ₹8,43,23,780 towards price drop expenses on the ground that such losses had already been reimbursed by OMIPL through credit notes.

The CIT(A) examined the distributorship agreement and found that the assessee was responsible for distribution, market development, territory management, and regional brand promotion. The agreement permitted the assessee to use the OPPO brand for advertising and promotional campaigns but did not impose any obligation on OMIPL to reimburse AMP expenses. The CIT(A) accepted the assessee’s explanation that OMIPL compensated distributors by offering a lower selling price instead of reimbursing advertisement expenses. This position was corroborated by the statement of OMIPL’s Finance Head, who confirmed that there was no policy for reimbursement of advertisement expenses and that such costs were embedded in the pricing structure. The assessee also produced advertisement invoices, promotional materials, vendor payments, and newspaper advertisements demonstrating that the expenditure had been incurred independently for its own regional business. The CIT(A) noted that the AO had not disputed the genuineness of the expenditure and had based the disallowance solely on a presumption of reimbursement. Accordingly, the disallowance of AMP expenses was deleted.

Regarding the price drop expenses, the CIT(A) observed that the assessee purchased mobile phones from OMIPL and sold them to distributors and retailers. Whenever OMIPL announced price reductions, the assessee became commercially obliged to issue credit notes to downstream dealers. While OMIPL reimbursed the assessee only for unsold inventory lying with the SAD or sub-dealers based on inactive IMEI data and only up to the invoice price charged by OMIPL, the assessee had to compensate its dealers based on its own selling price, which included its margin.

The unreimbursed margin reversal constituted the claimed expenditure of ₹8.43 crore. The assessee supported its claim with credit notes, IMEI reconciliation, ledger extracts, and other records. The CIT(A) found that the AO had neither disputed the computation nor established that the expenditure was fictitious or inflated, and therefore deleted the disallowance.

The Tribunal upheld the CIT(A)’s findings. It held that the AO’s disallowance of AMP expenses rested only on the presumption that the expenditure had been reimbursed. The Tribunal noted that the contractual terms, factual evidence, industry practice, third-party confirmation, and absence of reimbursement established that the AMP expenditure was genuine, necessary, and incurred wholly for the assessee’s own business, making it allowable under Section 37(1).

The Tribunal also upheld the deletion of the disallowance of price drop expenses. It observed that the assessee had demonstrated that OMIPL reimbursed only the base purchase price of unsold inventory and not the distributor’s margin lost while issuing credit notes to downstream dealers. Since the claimed expenditure represented an actual and verifiable commercial loss and the AO had not disproved its genuineness or necessity, the disallowance was held to be unsustainable. The Tribunal applied the same reasoning to AY 2020-21, dismissed both Revenue appeals, and dismissed the assessee’s cross-objections as not pressed.

FULL TEXT OF THE ORDER OF ITAT DELHI

These two appeals by the Revenue and Cross objections by the assessee are preferred against the respective orders of the Ld. Commissioner of Income Tax (Appeals)-30, New Delhi [in short “the Ld. CIT(A)] relevant to assessment years 2019-20 & 2020-21. Since common grounds have been taken in both the Revenue’s appeals, hence, appeals were heard together and disposed of by this common order for the sake of convenience, by dealing with the facts of ITA no. 4501/Del/2025 (AY 2019-20) wherein, the following grounds have been raised:-

1. Whether on the facts and in the circumstances of the case and in the provisions of the law, the Ld. CIT(AJ is correct in allowing the appeal of the assessee without appreciating the facts of the case.

2. Whether on the facts and in the circumstances of the case and in the provisions of the law, the Ld. CIT(Aj is correct in not considering the line of the Article 3 of the Distributorship Agreement that “all other expenses including but not limited to transportation, logistics, loading/unloading, Shipping, Supply/product recall/ return, warehousing, storage, insurance etc., shall be born by the Distributor only.

3. Whether on the facts and in the circumstances of the case and in the provisions of the law, the Ld. CIT(A) is correct in not considering the statement of Sh. Rahul Pujara that 100% reimbursement have been claimed from M/s 0M1PL and the same are given by M/s OMIPL.

4. Whether on the facts and in the circumstances of the case and in the provisions of the law, the Ld. CIT(A) is correct in not considering the fact that unsold inventory identified through inactive IMEIs is revalued at costs below the original purchases price resulting into losses of the SADs. For this, Price Drop Notifications were issued by M/s OMIPL. The Cost of price drop was availed by SADs and Dealers.

5. Whether on the facts and in the circumstances of the case and in the provisions of the law, the Ld. CIT(A) is correct in not considering the statement of Sh. Rahil Pujara (Q. 43 to Q 49) wherein he has admitted that all the price drop expenses have been reimbursed by M/s OMIPL.

6. The grounds of appeal are without prejudice to each other. 2

7. The appellant craves to add, alter, or amend any/all of the grounds of appeal before or during the course of hearing of appeal.

2. Both the cross objections of the assessee were not pressed by the Ld. AR for the asssessee, hence, the cross objections of the assessee, are dismissed, as not pressed.

3. The brief facts of the case are that the assessee has filed original return of income on 31.10.2019 declaring income of Rs. 6,53,50,690/-. Subsequently, ITS is processed u/s. 143(1) at total income of Rs. 6,53,55,690/- on 28.4.2020. A search and seizure operation u/s. 132 of the Act was conducted on 21.12.2021 in the case of assessee alongwith the other cases of Oppo Mobile India Group at various residential and business premises. Notice u//s. 148 of the Act was issued on 21.2.2023. In response to this, the assessee filed his return of income on 20.3.2023 declaring total income of Rs. 65350690/-. Notice u/s. 143(2) of the Act was issued on 21.6.2023 which was duly served on the assessee and questionnaire alongwith notices u/s. 142(1) of the Act were issued on various dates and show cause notice was issued on 9.3.2024. In response, assessee submitted its replies and documents. After considering the replies and documents, AO made the addition of Rs. 11,55,11,349/- on account of advertisement, marketing and brand promotion expenses by noting that after considering the Article 3 of the Distributorship agreement and the fact that the assessee has claimed certain expenses from the supplier, booking advertisement and brand promotion expenses on behalf of owner of brand “Oppo” , in its profit and loss account is not an allowable expenses in view of Section 37(1) of the Income Tax Act, 1961, hence, Further, AO made addition of Rs. 8,43,23,780/- on account of disallowance of price drop expenses not claimed by the assessee from M/s OMIPL, addition on account of price drop expenses u/s. 37 by noting that the expenses borne by the assessee company in its books of accounts towards Price Drop expenses of Rs. 8,43,23,780/- debited to its profit and loss account under the price drop expenses head of other expenses in financial statements of relevant FY 2018-19 are not allowed as these expenses are directly related with the assessee company and has been made on behalf of the other company, hence, addition of Rs. 8,43,23,780/- was added in the hands of the assessee. Aggrieved the action of the AO, assessee preferred appeal before the Ld. CIT(A), who vide order dated 31-3-2025 deleted both the additions made by the AO by observing as under:-

“..10. Ground No. 12: Disallowance of Advertisement and Brand Promotion (AMP) Expenses Rs. 11,55,11,349/-: The core issue under this ground relates to the disallowance of advertisement and brand promotion expenses incurred by the assessee in the sum of Rs. 11,55,11,349. The AO’s basis for disallowance is the presumption that these expenses were reimbursed by OMIPL or incurred for the exclusive benefit of the brand owner, and not for the business of the assessee. The AO refers to Article 3 of the Distributorship Agreement and draws an analogy with after-sales service reimbursements to conclude that the AMP expenses were either reimbursed or not allowable under Section 37(1) of the Act.

10.1 The assessee is a Super Authorised Distributor (SAD) of OPPO mobile phones in the entire state of Gujarat. Under the terms of the Distributorship Agreement dated 14.06.2019 with OMIPL, the assessee undertakes the responsibility not only of distribution and logistics but also of market development, territory management, and regional brand promotion.

10.2…………………………. Clause 2.03 of the Agreement specifically empowers the assessee to use the OPPO trademark, brand, and materials for the purpose of advertising and promotional campaigns in its assigned region. Clause 2.01 and 2.02 place responsibility on the SAD to actively engage in product promotion and coordinate with OMIPL for visibility strategies. In contrast, Clause 3, relied upon by the AO, merely states that save as provided above for reimbursement of branding and advertisement cost. This clause is permissive in nature and does not create any obligation on OMIPL to reimburse promotional expenditure.

10.3 Despite this, the AO concluded—without any direct evidence—that these expenses were reimbursed or were not wholly and exclusively for the assessee’s business. This conclusion appears to be based primarily on conjecture and a misreading of contractual terms.

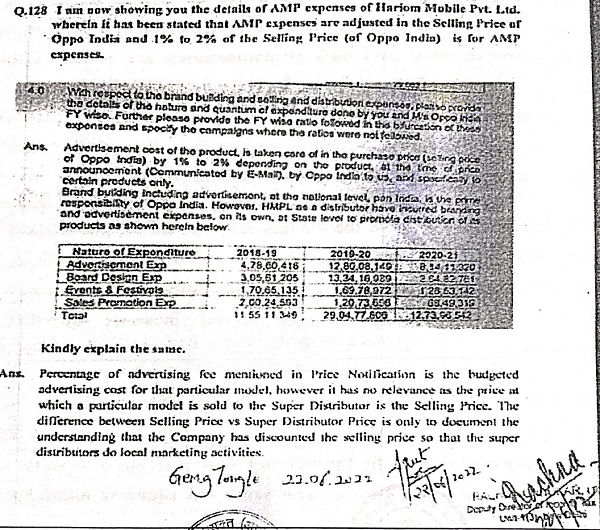

10.4 The assessee has explained that AMP expenses were never reimbursed by OMIPL. Instead, OMIPL provides a lower “Selling Price” (SP) to the SAD as against a notional “SAD Price.” This margin differential is provided to allow the SAD to independently undertake marketing and brand-building expenses in its region. This commercial understanding is consistently reflected in the price notifications issued by OMIPL and has also been corroborated by OMIPL itself.

10.5 In this context, the statement of Shri Geng Tongle, Finance Head of OMIPL, assumes significant relevance. In his deposition recorded under section 131(1A), he categorically stated that is no specific policy for reimbursement of advertisement expenses by OMIPL. The SADs are responsible for local advertisement and are compensated only by offering them favourable selling prices.

10.6 He also explained that AMP expenses are not reimbursed. The same are embedded in the price structure offered to the SAD. Relevant part of statement is reproduced below :

10.7 This statement directly and conclusively contradicts the AO’s presumption. The assessee, for its part, submitted sample AMP invoices, advertisement creatives, vendor payments, and newspaper clippings showing that it had independently incurred expenses for dealer-level brand awareness, store-level branding, print advertisements, and trade event promotion.

10.8 Moreover, these promotional materials bear the name of <!HOC” (Hari Om Communication) the trade name of the assessee—alongside OPPO branding, thereby reinforcing the fact that these campaigns were not merely for the benefit of the principal’s brand, but directly enhanced the visibility and goodwill of the assessee in its regional network.

10.9 The AO’s analogy with after-sales service reimbursements is also misplaced. Clause 4 of the agreement mandates 100% reimbursement of authorised service costs, and such reimbursements are evidenced through specific credit notes. There is no such evidence for AMP expenses. Unlike service support, which is centrally handled and reimbursed, AMP in this distribution model is the independent responsibility of the SAD, funded from its own resources, with compensation factored into pricing.

10.10 It is also significant that the AO has not disputed the genuineness of the AMP expenditure. There is no finding that the expenses are fictitious, inflated, or not incurred. The only ground for disallowance is the presumption of reimbursement an assumption now proven incorrect by third-party confirmation.

10.11 Based on the contractual framework, factual evidence, industrypractice, third-party statements, and the clear absence of reimbursement, it is held that the AMP expenses incurred by the assessee were genuine, necessary, and for the purposes of its own business. The same are squarely allowable under Section 37(1) of the Act. The disallowance of Rs. 11,35,11,349/- is deleted. Ground No. 12 is allowed.

11. Ground No. 13: Disallowance of Price Drop Expenses – Rs. 8,43,23,780: The AO disallowed the claim of Rs. 8,43,23,780 made by the assessee under the head “Price Drop Expenses,” holding that OMIPL had reimbursed such losses based on the IMEI-linked inventory validation process and the terms of Clauses 3.06 and 3.07 of the Agreement. The AO concluded that since the assessee was compensated by OMIPL via credit notes for price drops, no further deduction was allowable under Section 37(1).

11.1 The assessee, as a SAD, purchases products from OMIPL and sells them onward to distributors and retailers at a markup. When OMIPL announces a 7 price drop common in the mobile handset industry due to short product cycles the assessee becomes commercially obligated to issue credit notes to its dealers to maintain pricing parity across the distribution chain.

11.2 OMIPL compensates the SAD only for unsold inventory lying at the SAD or sub-dealer level, identified using inactive IMEI data. However, this compensation is limited to the base price at which OMIPL sold the product to the SAD. On the other hand, the SAD must issue credits to its downstream dealers based on its own sale price to them, which includes its margin. This difference, or margin reversal, is not reimbursed and is absorbed by the assessee.

11.3 To substantiate this, the assessee submitted a working for the F 9 4GB model, where OMIPL issued a price drop notification on 09.10.2018 reducing the customer price from Rs. 11,187 to Rs. 10,598. The following was demonstrated:

| Particulars | Original Price | Price drop |

Reduce price |

| Purchase price of SAD for F9 4GB Model | 11,187 | 589 | 10,598 |

| Purchase price of Distributor No. 1 | 12,748 | 1,256 | 11,492 |

| Purchase price ofDistributor No. 2 | 12,943 | 1,274 | 11,669 |

| So on to its other distributors / dealers/ RDS |

11.4 The total expense of Rs. 8.43 crores claimed by the assessee represents this net margin loss arising on stock already sold to dealers. The assessee submitted credit notes, IMEI reconciliation, ledger extracts, and supporting documentation to substantiate the claim. The AO did not challenge the computation, nor did he point to any fictitious or inflated entries.

11.5 Further, this business model and pricing mechanism were confirmed by Mr. Geng Tongle, Finance Head of OMIPL. In his deposition he affirmed OMIPL reimburses price drop only for stock with inactive IMEIs and only up to the invoice price charged to SAD. He clearly mentioned that we do not track or reimburse what SADs pay to their downstream distributors or retailers. This statement, from the principal company itself, nullifies the AO’s assumption that OMIPL bore the entire cost of price drops.

11.6 In a competitive and price-sensitive industry like mobile distribution, price drops are a frequent and commercial necessity. The distributor must adjust pricing across the supply chain to avoid returns, disputes, and to maintain dealer trust. The cost incurred is neither optional nor unrelated to business it is directly linked revenue expenditure necessary for smooth operations.

11.7 The AO’s finding that the assessee was fully compensated is based on a misunderstanding of pricing mechanics. There is a clear commercial distinction between base price reimbursement by OMIPL and margin reversal by the SAD. The latter is a legitimate cost arising out of a business compulsion.

11.8 In light of the above, the assessee’s claim of price drop expenses represents an actual and verifiable commercial loss. The AO has not disproved the genuineness or necessity of the expense. The disallowance is therefore not sustainable either on facts or in law. The disallowance of Rs. 8,43,23,780/- is deleted. Ground No. 13 is allowed.”

4. Aggrieved, the aforesaid findings of the Ld. CIT(A), Revenue preferred appeal before us.

5. The Ld. DR vehemently supported the order of the AO.

6. AR of the assessee submitted that Ld.CIT(A) has rightly deleted the additions, thus the same may be upheld.

7. We have heard the rival contentions and perused the records. With regard to disallowance of advertisement and brand promotion expenses amounting to Rs. 11,55,11,349/- is concerned, the AO’s basis for disallowance is the presumption that these expenses were reimbursed by OMIPL or incurred for the exclusive benefit of the brand owner, and not for the business of the assessee. The AO refers to Article 3 of the Distributorship Agreement and draws an analogy with after-sales service reimbursements to conclude that the AMP expenses were either reimbursed or not allowable under Section 37(1) of the Act. The assessee has explained that AMP expenses were never reimbursed by OMIPL. Instead, OMIPL provides a lower “Selling Price” (SP) to the SAD as against a notional “SAD Price.” This margin differential is provided to allow the SAD to independently undertake marketing and brand-building expenses in its region. This commercial understanding is consistently reflected in the price notifications issued by OMIPL and has also been corroborated by OMIPL itself. It is also significant that the AO has not disputed the genuineness of the AMP expenditure. Even there is no finding that the expenses are fictitious, inflated, or not incurred. The only ground for disallowance is the presumption of reimbursement an assumption now proven incorrect by third-party confirmation. Based on the contractual framework, factual evidence, industry practice, third-party statements, and the clear absence of reimbursement, Ld. CIT(A) has rightly held that the AMP expenses incurred by the assessee were genuine, necessary, and for the purposes of its own business, the hence, the same are squarely allowable under Section 37(1) of the Act. Therefore, the disallowance of Rs. 11,35,11,349/- was rightly deleted by the Ld. CIT(A), which does not need any interference, thus, we uphold the same and reject the ground raised by the Revenue.

7.1 As regards disallowance of Price Drop Expenses amounting to Rs. 8,43,23,780/- is concerned, we note that the AO disallowed the claim of Rs. 8,43,23,780 made by the assessee under the head “Price Drop Expenses,” holding that OMIPL had reimbursed such losses based on the IMEI-linked inventory validation process and the terms of Clauses 3.06 and 3.07 of the Agreement. The AO concluded that since the assessee was compensated by OMIPL via credit notes for price drops, no further deduction was allowable under Section 37(1). The assessee, as a SAD, purchases products from OMIPL and sells them onward to distributors and retailers at a markup. When OMIPL announces a price drop common in the mobile handset industry due to short product cycles the assessee becomes commercially obligated to issue credit notes to its dealers to maintain pricing parity across the distribution chain. OMIPL compensates the SAD only for unsold inventory lying at the SAD or sub-dealer level, identified using inactive IMEI data. However, this compensation is limited to the base price at which OMIPL sold the product to the SAD. On the other hand, the SAD must issue credits to its downstream dealers based on its own sale price to them, which includes its margin. This difference, or margin reversal, is not reimbursed and is absorbed by the assessee. The total expense of Rs. 8.43 crores claimed by the assessee represents this net margin loss arising on stock already sold to dealers. The assessee submitted credit notes, IMEI reconciliation, ledger extracts, and supporting documentation to substantiate the claim. The AO did not challenge the computation, nor did he point to any fictitious or inflated entries. The assessee’s claim of price drop expenses represents an actual and verifiable commercial loss. The AO has not disproved the genuineness or necessity of the expense. The disallowance is therefore not sustainable either on facts or in law, therefore, the disallowance of Rs. 8,43,23,780/- was rightly deleted by the Ld. CIT(A), which does not need any interference, thus, we uphold the same and reject the ground raised by the Revenue. Resultantly, the revenue’s appeal for assessment year 2019-20 stand dismissed.

8. As regards revenue’s appeal for assessment year 2020-21 is concerned, our decision taken for AY 2019-20, as aforesaid, will apply mutatis mutandis to the appeal relevant to assessment year 2020-21, thus, this appeal also stands dismissed on the similar lines, as aforesaid.

9. In the result, both the revenue’s appeals as well as assessee’s cross objections are dismissed in the aforesaid manner.

Order pronounced in the open court on 17-6-2026.

Author Bio