Introduction

The classification of liabilities as current or non-current under Ind AS 1 has long been a source of interpretive ambiguity and practical difficulty. With the Ministry of Corporate Affairs (MCA) notifying the Companies (Indian Accounting Standards) Second Amendment Rules, 2025 — effective for financial years beginning on or after 1 April 2025 — India aligns more closely with the global IFRS framework, particularly the amendments to IAS 1 issued by the IASB in 2020 and 2022. This article critically examines the revised principles, their rationale, illustrative scenarios, and practical implications for preparers, auditors, and stakeholders.

1. Background: The Pre-Amendment Framework

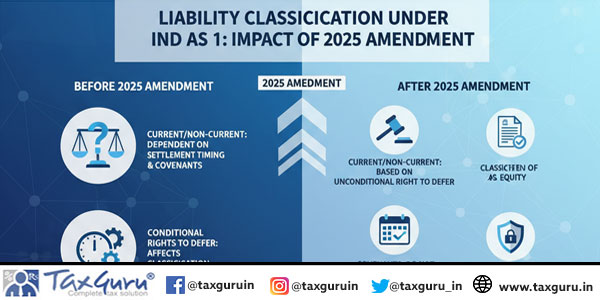

Under the earlier version of Ind AS 1 (para 69–76), a liability was classified as current if the entity did not possess an unconditional right to defer settlement for at least 12 months after the reporting date. This rigid formulation led to interpretive challenges, particularly in the context of:

- Loan covenant breaches and waivers

- Grace periods and refinancing arrangements

- Timing of covenant testing

- Settlement via equity instruments

Entities often relied on post-balance-sheet waivers or refinancing agreements to justify non-current classification, leading to inconsistent practices and reduced comparability.

2. Core Changes Introduced by the Amendment

The 2025 amendment introduces several key changes, summarized below:

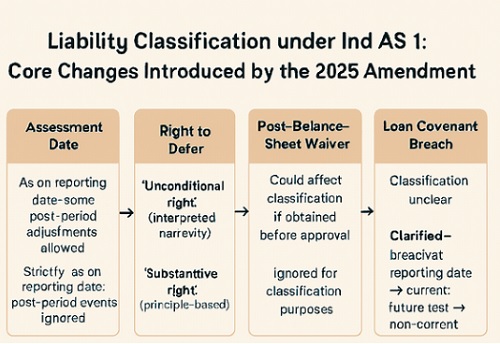

| Parameter | Old Ind AS 1 (till FY 2023–24) | Amended Ind AS 1 (from FY 2024–25) |

| Assessment date | As on reporting date; some post-period adjustments allowed | Strictly as on reporting date; post-period events ignored |

| Right to defer | “Unconditional right” (interpreted narrowly) | “Substantive right” (principle-based) |

| Post-balance-sheet waiver | Could affect classification if obtained before approval | Ignored for classification purposes |

| Loan covenant breach | Classification unclear | Clarified — breach at reporting date → current; future test → non-current |

| Settlement concept | Limited to repayment | Broadened to include equity, goods, or services |

| Refinancing after date | Could justify non-current classification | Not permitted |

These changes are codified in revised paragraphs such as 72A, 72B, 75A, and 76A–76B of Ind AS 1, as proposed in ICAI’s Exposure Draft and finalized via MCA’s notification dated 13 August 2025.

3. Rationale Behind the Amendment

The amendment addresses several long-standing issues:

- Inconsistent interpretation: Entities varied in their treatment of post-year-end waivers and refinancing arrangements, undermining comparability.

- Ambiguity in covenant testing: Confusion prevailed over whether covenants tested after the reporting date (e.g., DSCR or interest coverage ratios) should influence classification.

- Global convergence: The changes align Ind AS 1 with IAS 1, promoting consistency across jurisdictions.

- Improved transparency: The revised standard ensures that classification reflects the entity’s position as of the reporting date, not management’s expectations or subsequent events.

4. Illustrative Examples

Example 1: Breach of Covenant Before Year-End

Facts:

- Loan repayable after 3 years

- Covenant: Current ratio ≥ 1.2, tested at 31 March 2025

- Actual ratio = 1.1 → breach

- Waiver obtained in April 2025

Classification:

- Before Amendment: Some entities classified the loan as non-current if the waiver was obtained before financial statement approval.

- After Amendment: Classified as current, since the entity lacked a substantive right to defer settlement as of 31 March 2025. The waiver is a non-adjusting event.

Example 2: Covenant Tested After Reporting Date

Facts:

- Loan repayable in 3 years

- Covenant: Interest coverage ratio ≥ 2.0, tested on 30 June 2025

- Actual ratio = 1.1 → breach

- Waiver obtained in April 2025

Classification:

- As of 31 March 2025, the covenant is not yet tested. The entity retains a substantive right to defer settlement → non-current classification.

Example 3: Refinancing Agreement Signed After Year-End

Facts:

- Short-term loan maturing on 31 December 2025

- Refinancing agreement signed on 15 January 2026

Classification:

- Before Amendment: Entities often classified such loans as non-current if refinancing was virtually certain.

- After Amendment: Must be classified as current, since the refinancing right did not exist as of 31 December 2025.

Example 3: Refinancing Agreement Signed After Reporting Date

Facts:

- An entity has a short-term loan of ₹10 crore maturing on 30 June 2025.

- As of the reporting date 31 March 2025, the loan is classified as current.

- On 10 April 2025, the entity signs a refinancing agreement with the same lender to convert the loan into a 3-year term facility.

Position under Old Ind AS 1:

- Many entities would classify the loan as non-current if the refinancing was virtually certain and signed before the financial statements were approved.

- The rationale was that management’s intent and post-period arrangements could influence classification.

Position under Amended Ind AS 1 (Effective FY 2024–25):

- The loan must be classified as current as of 31 March 2025.

- The refinancing agreement signed on 10 April 2025 is a non-adjusting event under Ind AS 10.

- Since the entity did not have a substantive right to defer settlement as of the reporting date, the liability remains current.

Key Takeaway:

Under the amended standard, only rights existing at the reporting date determine classification. Post-period refinancing, even if contractually binding, cannot reclassify a current liability as non-current.

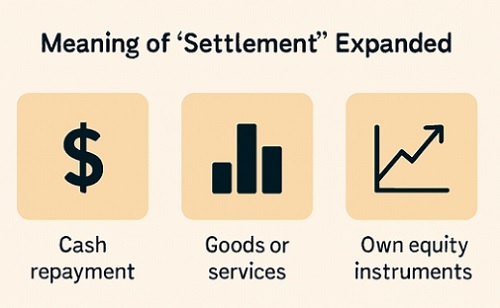

5. Expanded Definition of “Settlement”

A notable change is the broadened definition of “settlement.” Previously, settlement was interpreted narrowly as repayment in cash. The amendment expands this to include:

- Transfer of cash

- Delivery of goods or services

- Issuance of own equity instruments (e.g., conversion of debentures into shares)

This has implications for instruments like convertible debentures, where mandatory conversion within 12 months may trigger current classification.

6. Ambiguities and Interpretive Challenges

Despite the clarifications, certain areas remain judgmental:

a. Meaning of “Substantive Right”

The term “substantive” is not explicitly defined. Entities must assess whether the right to defer settlement is enforceable and not subject to unilateral withdrawal by the lender. For instance, a clause allowing the lender to revoke the deferral right at will may not constitute a substantive right.

b. Grace Period Clauses

If a loan agreement includes a contractual grace period extending beyond 12 months, classification hinges on whether the entity had the right to defer settlement within that period as of the reporting date.

C. Linked Covenants and Multi-Stage Testing

C. Linked Covenants and Multi-Stage Testing

Where multiple covenants are tested at different times (e.g., quarterly DSCR and annual interest coverage), determining which covenant affects classification requires careful analysis.

D. Interaction with Ind AS 10

Post-balance-sheet waivers and refinancing agreements are non-adjusting events under Ind AS 10. While they do not affect classification, they must be disclosed. Practices vary on the level of detail and prominence given to such disclosures.

7. Practical Implications

The amendment has far-reaching consequences:

a. Reclassification of Borrowings

More borrowings may now be classified as current, especially where covenant breaches exist or refinancing is post-period. This increases current liabilities and may affect liquidity assessments.

b. Impact on Financial Ratios

Ratios such as current ratio, debt-equity ratio, and working capital may be adversely affected. This could trigger secondary covenant breaches or affect credit ratings.

c. Disclosure Requirements

Entities must enhance disclosures around:

-

- Covenant terms and testing dates

- Breaches and waivers

- Management’s assessment of rights to defer settlement

d. Audit and Review Considerations

Auditors must scrutinize loan agreements, covenant clauses, and waiver letters to ensure accurate classification. Management representations alone may not suffice.

8. Regulatory Timeline and Notifications

| No. | Document & Issuing Body | Scope / Highlights | Status | Relevance to Liability Classification |

| 1 | Exposure Draft by ICAI (ASB) – “Classification of Liabilities as Current or Non-current and Non-current Liabilities with Covenants – Amendments to Ind AS 1” | Proposed alignment with IAS 1 (Jan 2020 & Oct 2022). Introduced revised paras 72A, 72B, 75A, 76A–76B, 76ZA etc. | Draft – Circulated 30 Dec 2022; comment deadline extended to 28 Feb 2023 | Primary draft proposing the full liability classification framework. Basis for final amendment. |

| 2 | MCA Notification – Companies (Indian Accounting Standards) Amendment Rules, 2023 (G.S.R. … dated 31 March 2023) | Amended several Ind AS including Ind AS 1, but focused on accounting policy disclosures (e.g., para 117) and other topics. | Final – Effective 1 Apr 2023 (for covered aspects) | Did not include the liability classification amendment. Often misunderstood as covering it. |

| 3 | MCA Notification – Companies (Indian Accounting Standards) Second Amendment Rules, 2025 (G.S.R. 549(E) dated 13 August 2025) | Explicitly amended Ind AS 1 to incorporate liability classification changes and supplier finance disclosures (Ind AS 7/107). Includes transitional provisions. | Final – Effective from 13 Aug 2025 for FYs starting 1 Apr 2025 | Operative notification enacting the liability classification amendment. Codifies revised principles. |

The 2025 notification is the operative amendment for liability classification, incorporating the revised principles and transitional provisions.

9. Strategic Considerations for Stakeholders

For Preparers:

- Review all loan agreements and covenant clauses before year-end.

- Engage with lenders early to renegotiate terms or obtain waivers before the reporting date.

- Ensure internal controls capture covenant testing timelines and breach risks.

For Auditors:

- Evaluate whether rights to defer settlement are substantive.

- Assess the timing and enforceability of waivers and refinancing arrangements.

- Verify disclosures under Ind AS 10 for post-period events.

For Analysts and Investors:

- Reassess liquidity and solvency metrics in light of reclassified liabilities.

- Scrutinize disclosures for covenant risks and management’s mitigation strategies.

10. Conclusion

The amendment to Ind AS 1 reinforces that liability classification must reflect rights and conditions existing as of the reporting date, not management’s expectations or post-period developments. It reduces subjectivity, aligns Indian standards with global IFRS practice, and enhances transparency and comparability.

Entities must now adopt a more document-driven, covenant-aware, and timing-sensitive approach to liability classification. This demands early engagement with lenders, precise drafting of loan agreements, and robust internal controls around covenant monitoring.

In a financial landscape shaped by covenant complexity and disclosure scrutiny, the amended Ind AS 1 shifts the spotlight from managerial intent to legal enforceability. Classification is no longer a matter of hindsight — it is a test of foresight, documentation, and discipline.