In this article, the author explains why ITC is allowable on electricity infrastructural expenditure and capital services expenditure incurred by a manufacturer, outside the factory premises, for taking thee electricity produced to the Sub-station of the State electricity undertaking. He has touched upon the recent Ruling of the GAAR in this regard.

GST ITC on Electricity Infrastructure Outside Factory Premises

1. Introduction

One of the key questions surrounding the minds of GST practitioners is about the eligibility of ITC on capital goods and services used to install electricity infrastructure outside the factory premises. When a manufacturer embarks on such exercise, he has to incur heavy cots on infrastructural , especially when high-tension (HT) connections are required from state electricity boards. He has to also avail services in this regard, after obtaining permission from the regulatory bodies.

To the relief of the manufacturers, two important Ruling—Elixir Industries Pvt. Ltd. (2024) and Alleima India Pvt. Ltd. (2025)—have clarified the position under Sections 16 and 17(5) of the CGST Act, 2017. CBIC Circular No. 219/13/2024-GST is also relevant in this context. These Rulings and the aforesaid circular, play a strong role in favour of the taxpayers on the impugned issue.

Let us go through the CBIC Circular and the Rulings above.

2. Factual Background: Elixir and Alleima

2.1 Elixir Industries Pvt. Ltd. – GAAR Order No. GUJ/GAAR/R/2024/18, dated 02.07.2024

The applicant was in need of a 1000 KVA HT connection at 66KV. When the applicant sought necessary permission from the GETCO, it mandated the installation of a feeder bay and underground cables from its substation to the factory. Under the supervision of GETCO, the applicant carried out the same, incurring costs therefor (equipment as well as services). The applicant claimed ITC on cables, electrical equipment, and installation services. The applicant sought an Advance Ruling on the correctness of the claim.

2.2 Alleima India Pvt. Ltd. – GAAR Order No. GUJ/GAAR/R/2025/44, dated 16.10.2025

In this case, the applicant expanded its Mehsana plant and required 4500 KVA connection at 66KV. The distance of the GETCO’s substation to the factory switchyard. Was around 2.8 kms. It had to lay underground cables for this distance.

GETCO had provided two options for the execution of the cable laying work:-

(a) Execution by GETCO: GETCO may undertake the work directly through its vendors.

(b) Supervised Installation: The applicant may conduct the work under the supervision of GETCO.

The applicant chose the second option, which involved carrying out the cable laying work on their own cost under the supervision of GETCO. The applicant selected, M/s Rajesh Power Services Pvt. Ltd (the vendor), from the approved authorised vendors of GETCO, to execute the installation of the underground cable line and supply the requisite materials.

the books of the applicant, were capitalised as enabling assets; depreciation was claimed on taxable value. It may be noted that the Ownership remained with the applicant, subject to future transfer.

3. Statutory Framework

We can now need to look into the relevant sections under the CGST Act, 2017, which are relevant to the discussion.

Section 16 – Eligibility for ITC

- ITC is allowed on goods/services used in the course or furtherance of business.

- The required conditions under Section 16(2) must be fulfilled: possession of invoice, receipt of goods/services, tax paid to Government, GST return must be filed.

Section 17(5)(c) and (d) – Blocked Credits

- ITC is disallowed for:

- Works contract services for construction of immovable property (other than plant and machinery).

- Goods/services used for construction of immovable property on own account.

Explanation to Section 17

- “Plant and machinery” includes equipment fixed to earth by foundation or structural support, used for making outward supply.

- Excludes:

- Land, building, or any other civil structures

- Telecommunication towers

- Pipelines laid outside factory premises

4. Key Issues

In the case cited in 2.2 (supra), the process of laying of cables has been explained by the appellant, as under :-

- The transmission of electricity from the power station to the factory premises requires the excavation of a trench that will extend the entire distance from the power station to the manufacturing site.

- The high voltage cables are laid out through ducts with adequate spacing

- In areas, where the cables cross under roads, the applicant will implement additional safety measures by utilising double-wall corrugated (DWC)/Hume pipes within the trench.

- This comprehensive approach to cable installation not only guarantees the safety and reliability of the electric transmission system but also aligns with industry best practices and regulatory standards.

All these activities associated with the laying of cables and installation of equipment will be executed under the careful supervision of GETCO.

The applicant has submitted that they would be eligible for ITC, for the reasons stated as under:

- They fulfil all the conditions of Section 16(2) of the CGST Act, 2017;

- The ITC to be availed is not hit by the exclusions mentioned in Section 17(5);

- Laying of cables from GETCO substation outside the factory premises to the applicant’s switchyard within the factory premises does not qualify as works contract;

- that u/s 2(119), works contract is limited to immovable property; that the components involved in the project ie cables, wires, switchyards, aluminium corrugated sheaths are movable property; that they can be easily transported from one location to another; that they can be coiled and relocated without significant effort; that their modular nature allows them to be connected or disconnected as need facilitating movement between various operational sites or configurations;

- that the transmission is facilitated through an underground cable carefully laid to ensure minimal disruption & optimal performance;

- that the cables and wires can be removed from ducts & manholes when necessary & replaced with new ones demonstrating their movable nature;

- that in terms of explanation to section 17(5), cables/wires & equipment falls within the ambit of ‘plant and machinery’;

- that the phrase ‘any other civil structure’ as appearing in explanation to 17(5) is to be read ejusdem generis to the preceding words land and building; that the phrase ‘any other civil structure’ is to be restricted to immovable property in the nature of land and building; that the structure used as an apparatus in the manufacturing activity will not be ‘any other civil structure’ & will be plant and machinery;

- that the ITC is eligible on ducts and manholes; that they would like to rely on Circular no. 219/13/2024-GST dated 26.6.2024, which provides clarification on the availability of ITC for ducts and manholes used in the network of optic fibre cables.

- that they would also like to rely on the GAAR ruling in the case of M/s Elixir Industries Pvt. Ltd [GUJ/GAAR/R/2024/18] which is entirely on the same facts.

The following key issues need to be looked into in this context:

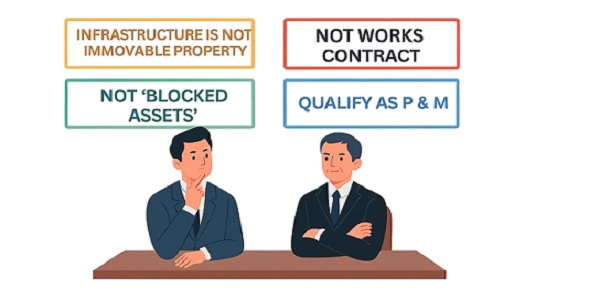

i. Can the infrastructure be regarded as “immovable property”?

In both instances, the applicants argued that the cables, wires, and switchyards were modular and movable. They could be dismantled, coiled, and relocated. Therefore, they cannot be regarded as “immovable property”.

The authorities accepted this. In this context, Movability was the decisive factor.

ii. Is it a “works contract”?

Under Section 2(119), a works contract relate to immovable property falls in blocked credit. Since the assets were movable, the impugned transaction is not to be treated as a works contract.

iii. Are they “blocked” assets?

The answer is in the negative. The exclusions apply only to construction of immovable property. Since the infrastructure and amount expended were towards movable assets and used for business, ITC was not blocked on the same.

iv. Does it qualify as “plant and machinery”?

Yes. The assets were utilised for outward supply. They were fixed to earth; however, they were not excluded under the Explanation. Hence, they qualified as “plant and machinery”.

Author’s Note: The eligibility of Input Tax Credit (ITC) on cables laid from the factory to the EB sub-office may be supported by the Supreme Court’s ruling in Jawahar Mills Ltd. v. CCE [(1999) 108 ELT 47 (SC)]. In this case, the Apex Court held that capital goods— welding electrodes, wires, and cables — used in or in relation to the manufacture of final products — even indirectly — qualify for credit. This precedent strengthens the argument that such cables, being essential to power transmission for manufacturing, may be treated as part of plant and machinery. Further, the decision in CCE v. Grasim Industries Ltd. [2014] 41 taxmann.com 66 (MP) dated 13-12-2013 confirms that panel boards and PVC cables used for electrical purposes are eligible for credit as capital goods. f these items are capitalized and used for business operations, they qualify for ITC under GST — unless blocked by Section 17(5), which this case helps to navigate.

5. CBIC Circular No. 219/13/2024-GST – Ducts and Manholes in OFC Networks

The relevant portion of the Circular reads as under:

| Issue | Clarification |

| Whether the input tax credit on the ducts and manholes used in network of optical fiber cables (OFCs) for providing telecommunication services is barred in terms of clauses (c) and (d) of sub-section (5) of section 17 of the CGST Act, read with Explanation to section 17 of CGST Act? | 1. Sub-section (5) to Section 17 of the CGST Act provides that input tax credit shall not be available, inter alia, in respect of the following:

i. works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service; or ii. goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business. 2. Explanation in section 17 of CGST Act provides that the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes land, building or any other civil structures; telecommunication towers; and pipelines laid outside the factory premises. 3. Ducts and manholes are basic components for the optical fiber cable (OFC) network used in providing telecommunication services. The OFC network is generally laid with the use of PVC ducts/sheaths in which OFCs are housed and service/connectivity manholes, which serve as nodes of the network, and are necessary for not only laying of optical fiber cable but also their upkeep and maintenance. In view of the Explanation in section 17 of the CGST Act, it appears that ducts and manholes are covered under the definition of “plant and machinery” as they are used as part of the OFC network for making outward supply of transmission of telecommunication signals from one point to another. Moreover, ducts and manholes used in network of optical fiber cables (OFCs) have not been specifically excluded from the definition of “plant and machinery” in the Explanation to section 17 of CGST Act, as they are neither in nature of land, building or civil structures nor are in nature of telecommunication towers or pipelines laid outside the factory premises. 4. Accordingly, it is clarified that availment of input tax credit is not restricted in respect of such ducts and manhole used in network of optical fiber cables (OFCs). either under clause (c) or under clause (d) of sub-section (5) of section 17 of CGST Act. |

It may be seen that this circular clarifies that ducts and manholes used in optical fiber cable (OFC) networks are not civil structures and qualify as “plant and machinery”.

The circular was relied upon in both rulings to support the argument that underground infrastructure used for transmission is eligible for ITC.

6. Reasoning of the AAR

GAAR in Elixir Industries

- Accepted that cables and equipment were movable.

- Held that ITC was admissible under Section 16.

- Section 17(5) did not apply to the facts of the case.

- Ownership transfer to GETCO did not affect eligibility.

- The AAR opined that, nevertheless, Section 18(6) would apply for reversal if assets were transferred.

GAAAR in Elixir Industries – Appeal No. GUJ/GAAAR/APPEAL/2025/16, dated 22.09.2025

The Department appealed against the aforesaid GAAR ruling. The GAAAR dismissed the appeal and upheld the ruling. The GAAR was of the emphatic view hat ITC is available on movable infrastructure used for electricity transmission.

GAAR in Alleima India

The GAAR held in favour of the applicant, followed Elixir Industries (supra). It accepted movability and modularity of cables and switchyards. Reliance was placed on CBIC Circular discussed supra. GAAR held that ITC was admissible and upheld the claim of the applicant. It was however made clear that section 18(6) would apply if assets were transferred to GETCO.

Comparative Table

| Aspect | Elixir Industries | Alleima India |

| Voltage | 66KV | 66KV |

| Cable Length | ~1 km | 2.78 km |

| Ownership | Transferred to GETCO | Retained (subject to future transfer) |

| Execution | Under GETCO supervision | Under GETCO supervision |

| Capitalisation | Yes | Yes |

| Depreciation | On taxable value | On taxable value |

| ITC Allowed | Yes | Yes |

| Section 18(6) | Applicable on transfer | Applicable on transfer |

| Appeal Outcome | Upheld by GAAAR | Not appealed |

7. Key Takeaways

For the readers and professionals, these rulings offer several doctrinal lessons:

(i) More than the location, movability is more important;

(ii) A Modular infrastructure can be regarded as plant and machinery;

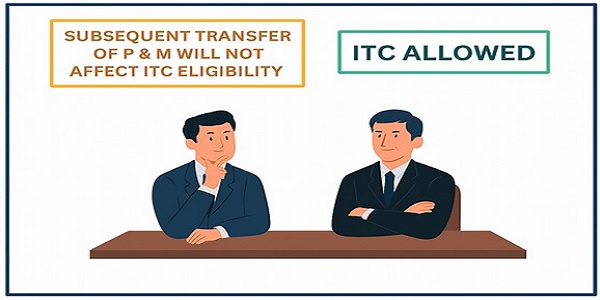

(iii) The transfer of the assets in question on a late date, will not affect the eligibility. It will only end in reversal at such point of time, of the sum to be computed as per the ACT and the Rules applicable;

(iv) Taxpayers must capitalise the amount in question properly in the books and claim depreciation thereon. The treatment in books of account plays a pivotal role in this context.

Theme Extension: ITC for Business Infrastructure Outside Factory

This article shows one key idea. ITC is allowed if the asset is used for business. Even if it is outside the factory. Even if it is not fixed to the ground. Even if it is transferred later. What matters is the purpose.

This idea helps in other cases too.

Example: Underground cables from EB to factory

> Used to bring electricity for production.

> Cables are movable.

> Used in business.

> So, ITC is allowed.

Example: Office setup in rented space

> Movable partitions and wiring.

> Used for business.

> Not part of building.

> So, ITC may be allowed.

Example: Temporary project site

♦ Mobile cabins and equipment.

♦ Used only for business.

♦ Not for personal use.

♦ So, ITC may be allowed.

Practical Implications for stakeholders

When manufacturers expand operations and require HT connections, they often install infrastructure outside the factory. These Rulings confirm that:

- ITC is available if the assets are movable and used for the purposes of business.

- Attention must be paid for proper drafting of the Agreements with the requisite authorities and regulators.

- Capitalisation in books and depreciation on taxable value must be clearly and properly documented by the taxpayer.

- If ownership is transferred at a later daye, reversal under Section 18(6) must be planned.

8. Judicial Endorsement of Doctrinal Clarity

The GAAAR’s affirmation in Elixir Industries is particularly important. It confirms that movable infrastructure used for electricity transmission is not hit by Section 17(5). This sets a precedent for similar cases across India. Such installation may be outside the factory premises also. Transfer of the assets at a subsequent point of time may result in reversal of the proportionate ITC, but will not affect the eligibility for ITC.

9. Taxguru Posts on Alleima India Pvt. Ltd.

| Title | Date | Summary (as per author) |

| ITC Allowed on Power Transmission Equipment Installed Outside Factory: AAR Gujarat | 29 Oct 2025 | Covers the GAAR ruling in Alleima India Pvt. Ltd. (GUJ/GAAR/R/2025/44), confirming ITC eligibility on underground cables and electrical equipment installed outside the factory premises. |

| No GST on Employee Canteen Charges: Alleima India Pvt Ltd (AAR Gujarat) | 17 Jul 2024 | Discusses a separate AAR ruling involving Alleima on GST applicability for nominal canteen charges recovered from employees. Not directly related to infrastructure ITC. |

10. Linking Prior Commentary: ITC for Electricity in Townships vs. Manufacturing

In an earlier article published on TaxGuru (“GST ITC on electricity consumed for maintenance of township is not admissible”, 18 August 2025), the author had explained why ITC is not allowed when electricity is used for residential or welfare purposes. This article covers the CBiC circular also, and whether it is prospective or retrospective. That case involved power supplied to employee townships, which is not considered part of business activity under Section 16 of the CGST Act. In contrast, the Alleima India Pvt. Ltd. Ruling deals with electricity infrastructure used directly for manufacturing. The cables and equipment were installed to bring power to the factory. They were movable, capitalised, and used in business. So, ITC was rightly allowed. The key difference is the purpose—business use versus welfare use.

11. Concluding remarks

The Rulings in Elixir Industries and Alleima India have clarified a critical area of GST law. They affirm that ITC is available on capital goods and services used for electricity transmission, even if installed outside the factory premises. The amounts expended on them, either by the taxpayer or through an approved vendor, would be regarded as one spent towards movable property and not an immovable property.

These decisions are doctrinally sound. They are also commercially relevant, and pedagogically rich. They offer clarity to manufacturers, tax professionals, and students alike.

Author Bio