Chartered Accountants Association, Surat (CAAS), has written to the Finance Minister expressing significant concerns about the current Goods and Services Tax (GST) regime. The letter highlights a range of issues, including alleged unauthorized access and sale of taxpayer data, prolonged GST registration processes due to arbitrary “high-risk” profiling, and substantial delays in GST refunds, with claims of unofficial “packages” for expedited processing. CAAS also points to the misuse of power by officers in bank account attachments, the lack of coordination between Central and State GST authorities, and flaws in the GST amnesty scheme where circulars override legal provisions. Furthermore, the Association notes staff shortages and a perceived lack of diligence among GST officers, leading to inefficiencies and unnecessary penalties. Other grievances include the inconsistent application of Document Identification Numbers (DINs) and the use of unofficial email for communications, alongside severe backlogs in the appellate process due to the absence of a functional GST Tribunal. To address these systemic problems, CAAS proposes a “GSTCoin” system, a blockchain-based digital token for GST transactions, aiming to improve real-time tax remittance, ensure verified Input Tax Credit, and streamline reconciliation, ultimately fostering a more transparent and efficient tax environment.

Chartered Accountants Association, Surat

Ref: CAAS/Representations/2024-25/05 Date: 31-05-2025

To,

The Finance Minister,

Ministry of Finance,

North Block,

New Delhi – 110001

Respected Madam,

Subject: Alms and Apathy under GST Regime

The Chartered Accountants Association Surat (CAAS), an organisation steadfastly committed to upholding ethical practices and fostering a conducive environment for trade and compliance, is compelled, yet again, to address your esteemed office. This communication is a reluctant extension of our previous representations, notably our letters dated January 20, 2024 (Ref: CAAS/Representations/2023-24/04)and August 21, 2024 (Ref: CAAS/Representations/2024-25/02). These earlier pleas, detailing the unscrupulous practices and systemic inertia plaguing the GST framework, particularly within the State machinery, appear to have been met with the customary bureaucratic indifference, as many of the maladies not only persist but have, in fact, metastasized, courtesy the flawed policies with no connection with ground realities.

We reiterate that CAAS has always championed the cause of a transparent and efficient tax system. However, the ground reality, as experienced by taxpayers and professionals alike, paints a grim picture of a system held hostage by a culture of delay, opacity, and an insatiable appetite for “Alms.” This letter, therefore, must be read in its entirety, as a holistic indictment of a failing system, rather than a disjointed list of grievances, lest the overarching narrative of distress be vitiated.

We present below, with a profound sense of concern and a sharper pen, the pressing issues that demand your immediate and decisive intervention, including amendment to the existing GST Law and rules, before the “Good and Simple Tax” becomes a national epitaph for failed reform.

1. The Great GST Data Bazaar: Your Privacy, Our Commodity!

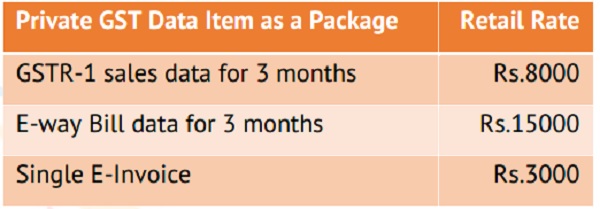

It appears the only thing growing faster than GST revenues is the audacity with which taxpayer confidentiality is being auctioned. We are aghast to learn of reports that GST transactional data, the lifeblood of businesses, is allegedly available in the open market.

This isn’t just a data breach; it’s the death knell for business privacy, enabling effortless profiling of sourcing and supply chains by anyone with a few thousand rupees to spare. The very notion of “Holier than Thou” GST Officers and the GSTN fortress of data security has crumbled, revealing a marketplace where trust is the cheapest commodity. This is not mere corruption of money, but a far more insidious corruption of data and faith. If this digital striptease of business vitals continues, the GST system will not just fall apart; it will implode under the weight of colossal distrust.

Our Demands:

- Implement mandatory, on-the-fly AES-256 encryption for all data uploaded to GSTN – be it returns, invoices, or e-way bills. Let’s at least pretend our data is valuable.

- Drastically shrink the circle of individuals with access to raw downloadable data. Adjudicating officers, should be stripped from any access to data in its downloadable form. In their sacred duties of refund or assessment, data should be made available for viewing only and not for download.

- If GSTR-1, GSTR-2B, and GSTR-3B are truly “linked” (as the prophecy foretold), perhaps the redundant, mind-numbing queries from DGARM about mismatches could be eliminated, saving paper, time, and taxpayer sanity.

- A small matter of rounding off: Section 170 of the CGST Act permits rounding of tax to the nearest rupee. Why, then, are taxpayers allowed, even, encouraged, to upload invoices with decimal paisa, creating a delightful playground for mismatches? Forbid decimal uploads for tax amounts and watch a species of mismatch vanish.

2. The Registration Gauntlet: Welcome to the “High Risk” Club (Everyone’s a Member!)

The CBIC policy paints a rosy picture of GST registration within 7 days emanating from the GST Law – an absolute fairy tale indeed. The reality? A journey prolonged up to 30 agonizing days, because, almost every applicant is profiled as “high risk.” This “risk,” a nebulous concept whose parameters are guarded more fiercely than state secrets, becomes the perfect pretext for lethargy culminating in queries magnanimously issued on the 30th day. One wonders if starting a business is now a suspicious activity requiring an inquisition worthy of a medieval witch hunt. The Income Tax Department issues PANs out of sheer trust; companies are also incorporated with trust, but a GST number? That requires extraordinary scrutiny. This invasive, almost hostile approach to entrepreneurs who are the supposed engines of growth is baffling. They should be welcomed with open arms, not treated like potential fraudsters before they’ve even made their first sale. And amendments? Another golden opportunity to seek “Alms.”

Our Demands:

- Issue GST registrations and amendments based on trust, much like opening a Gmail account. Keep the friction for post-registration misdemeanours, where the entire arsenal of penalties and prosecution awaits for the newcomer who, then, should not be spared.

- To inject an ounce of transparency and perhaps shame the idlers, display a regular, public ageing report of pending registration applications on the portal. Let the numbers speak for themselves.

3. The Refund Mirage: Your Capital, Our Leverage, Their “Packages.”

A taxpayer dutifully pays 18% (or more) GST, a sum that can make or break a business’s going concern. For export-oriented units, those under inverted duty structures, or new businesses, this GST accumulation becomes a deadweight. Businesses obsess over debtor cycles, but the GST department has become the ultimate non-performing debtor, comfortably sitting on taxpayer funds for the full statutory 60 days, only to issue refunds at the last possible moment – a masterclass in loophole exploitation. And the “packages” – Regular, Max, Pro, Ultra-Pro, Ultra-Max-Pro – offered by officials for prioritized refunds? It’s an entire cottage industry thriving on desperation. It’s also tragically amusing that banks, don’t officially finance this GST credit, a massive chunk of working capital. Perhaps they know something we don’t about the department’s payment reliability.

Our Demands:

- Make GST refunds faceless, akin to the Income Tax system. No names, no faces, no contact information exchanged.

- All documents to be processed exclusively through GSTN, with applications randomly assigned to officers in different cities each time. Break the jurisdictional nexus.

- Crucially, delink the visibility of taxpayer contact information from jurisdictional and other offices. No more direct calls, no more “facilitation.” Let the tax marketers find other prey.

4. Misuse of Power: The Attachment Autocrats and the Art of the Freeze.

Section 79(1)(c)(i) of the CGST Act empowers officers to recover dues from third parties, including banks, to the extent sufficient to pay the amount due. A simple, logical provision. Yet, in practice, it translates to a total freeze of bank accounts, regardless of whether the account holds multiples of the demanded sum. This isn’t recovery; it’s financial strangulation, creating immense hardship. And, of course, the taxpayer must then wag their tails, while serving “Alms” for an early defrosting of their own funds. It’s a masterstroke of coercive negotiation.

Our Demands:

With great power comes the urgent need for great responsibility – or, failing that, stringent rationalisation. The “blind bull” approach of officers needs to be curbed, not just for attachments but for every discretionary power under the Act they wield with such devastating effect. Clear, unambiguous guidelines and severe penalties for overreach are essential.

5. The Two Fathers Syndrome: CGST & SGST – A Tale of Discordant Harmony.

In our culture, the government is often referred to as ‘Mai-Baap’ (parents). Under GST, taxpayers seem to have been blessed with two fathers – CGST and SGST – both equally eager to bombard them with notices on the same issue for the same period. It’s a unique form of parental attention. Even the sauce at a pizza franchise maintains consistency across all outlets; why then, do the standards, practices, and interpretations of CGST and SGST officers diverge so wildly? The tax, interest, and penalties flow into a common pool, administered without bias by the jurisdictional principal. So why this chaotic multiplicity of agencies – CGST, SGST, and their various offspring like Preventive Wing, DGARM, DGGI, Enforcement, Audit, and the regular adjudicating officer? When the benefits are shared, why does one parent (Centre) wash its hands when the other’s (State) child misbehaves, claiming “not our employee”? This deep-seated distrust within the governmental structure itself, leading to an organizational model found nowhere else, is perhaps the most telling feature of GST’s “success.”

Our Demands:

- The Central Government must either invest in rigorously training its SGST brethren to sing from the same hymn sheet.

- Or, summon the courage to take over the entire GST administration, perhaps by absorbing SGST officials (if they are deemed trainable).

- Alternatively, and perhaps most simply, denounce its own position and dissolve the CGST Department, letting the States manage their own show, however chaotic. At least the taxpayer will know which father towould have seen a commensurate increase. Unfortunately, reality, as always, has a sarcastic twist.

6. The GST Amnesty Scheme (Section 128A): A Masterclass in Bait-and-Switch.

Though the amnesty scheme form SPL-01 was launch quite late. But the Taxpayers were lured, with officers even making personal calls encouraging applications. Trusting souls withdrew appeals, waived legal remedies, and jumped through hoops to become eligible. And then? The rug pull. Show Cause Notices in SPL-03 were issued contending to reject applications, citing Item 4 of Table in Para 4 of Circular No.238/32/2024-GST dated 15th October 2024. This item audaciously excludes interest on delayed return filing/reporting from the waiver, claiming it’s “self-assessed liability” interest. The moot question, which seems to have escaped the intellectual giants drafting these circulars, is: how can a mere CBIC circular introduce a condition that brazenly overrides the clear, unambiguous provisions of Section 128A of the Act itself? The said section clearly applies to demands raised under Section 73, which inherently includes tax and, by extension, related interest. This is not interpretation; it’s legislative overreach by a body not empowered to legislate. Any override by the circular over the Act, is bad in law and illegal.

Our Demands:

- Amend this absurd circular immediately and put an end to the illegality. An executive fiat cannot nullify a legislative act.

- Stop the piling up of illegal demands by both Centre and State. Neither stakeholders nor the already overburdened judiciary have surplus time for such manufactured litigation.

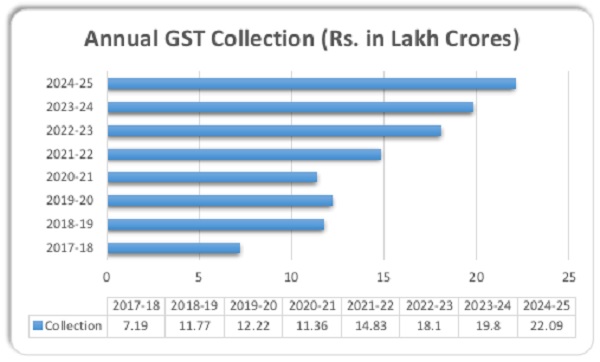

7. The Curious Case of the Disappearing Staff and the Expanding Lunch Breaks.

Since GST’s grand arrival in July 2017, collections have, by official accounts, more than tripled. One would imagine the workforce managing this windfall such manufactured litigation.

would have seen a commensurate increase. Unfortunately, reality, as always, has a sarcastic twist.

As the collections soar, the staff count stagnates, if not dwindles. The CBIC’s own Citizen’s Charter, with its lofty benchmarks, remains a distant dream, partly because there simply aren’t enough (willing) hands on deck. Our earlier plea to SGST Gujarat to consider outsourced manpower fell on deaf ears – perhaps the existing staff feared competition in efficiency.

But it’s not just about numbers. It’s about the will to work. Officers walking in at 11:30 AM or even noon (for SGST, punctuality is clearly a foreign concept, best disregarded). The legendary “SBI-styled” hour-long lunch break. And then, the its remarkable feature: a profound reluctance to move a muscle without the sacred offering of “Alms.” Work is held hostage, ransomed by these “brothers in Alms.” Registrations, spot visits, refunds, assessments, appeals – all languish, not just due to staff shortage, but a shortage of sincere, willing manpower. Even ruling party spokespersons have lamented on national television about insubordinate officers who listen to neither superiors nor Ministers. The employee-to-taxpayer ratio is plummeting to alarming levels.

Our Demands:

- Firstly, tighten personnel policies. Monitor attendance and work hours. Fingerprint machines at CGST are a good start; perhaps extend this “revolutionary” technology to SGST.

- Secondly, the colonial 11:00 AM to 6:00 PM timing needs an overhaul. For national growth and perhaps even a blip in the happiness index of the personnel, why not 8:00 AM to 5:00 PM, with a crisp 12:00 PM to 1:00 PM lunch? Eight hours of actual work might just achieve miracles.

- Thirdly, those who have clearly demonstrated their unwillingness to work and an aptitude for spoiling the environment should be relieved of their duties – respectfully if they choose, or with the necessary disgrace if their dither.

- Fourthly, appoint more staff. There are legions of genuinely needy, qualified candidates desperate for these jobs. Give them a chance to serve, rather than be server ”Alms.”

8. The Penalty Bazaar: When in Doubt, Slap on Section 125!

The GST law has become a fertile ground for levying penalties with the creativity of a surrealist painter. A taxpayer misses the return filing date by a few days? SGST issues a Show Cause Notice under Section 125 (General Penalty) for Rs. 25,000 CGST + Rs. 25,000 SGST for contravening “any of the provisions.” This, when late fees, themselves penal in nature, are already applicable. It’s like being fined for speeding, and then fined again for “using the road improperly.” Similarly, an innocent mistake under Section 73, self-corrected with tax and interest paid. Here comes a mechanical penalty under Section 73(9) r.w.s 73(11) of Rs. 10,000 CGST + Rs. 10,000 SGST. It seems a GST registration is not a license to do business, but a subscription to a white elephant that thrives on a diet of penalties.

Our Demand:

Penalties are often a function of officer’s discretion. Discretion, as we know, is the fertile soil where bias and the quest for “Alms” blossom. We demand to rationalize all penalty provisions. Implement safeguards against the blind, almost gleeful, invocation of residuary penalties like Section 125 or the mechanical application of Section 73(9). Let the punishment fit the crime, not the officer’s mood or monthly target.

9. The DIN Deception and the Gmail Gambit: Official Communications, Unofficial Channels. The mandate for Document Identification Number (DIN) via Circular contemptuous disregard by both Central and State officers. Blank DINs are allegedly generated, only to be conveniently slapped onto back-dated communications. State officers sometimes argue CBIC circulars don’t bind them, preferring their own Reference Numbers (RFNs), if at all, which offer dubious authentication as to whom it is addressed. And then there’s the shabby, unprofessional, and frankly insecure practice of using Gmail IDs for official communication, despite clear instructions to use ‘.gov.in’ domains. We’ve seen instances in South Gujarat where fraudsters, masquerading as GST officials, have solicited information via Gmail, and competitors have allegedly used similar tactics for data extraction. This is in direct contravention of MHA Office Memorandum No.14/4/2001-T, dated 17-07-2007, regarding data transaction on servers outside India.

Our Demands:

- If GSTN provides a common IT infrastructure, then common circulars onprocedural integrity (like DIN) must apply universally. No excuses.

- Issue stringent guidelines to prevent the misuse of DINs, perhaps by making blank DIN generation impossible or immediately flaggable.

- Enable DIN tracking on the GST portal itself, so officers (and taxpayers) can verify authenticity and prevent duplicate notices for the same period.

- The mandatory use of ‘.gov.in’ email IDs needs teeth. Issue a clear circular stating that any communication regarding GST matters emanating from third-party email IDs (Gmail, Yahoo, etc.) should be officially ignored by taxpayers and will hold no legal validity.

10. The Appellate Labyrinth & The Elusive Tribunal: Justice Delayed is Justice Denied (and Compounded).

The progress in GST appeals is so slow. SGST departments, in a “meaningless pursuit” to clear backlogs, recently rejected a swathe of appeals by refusing to condone delays beyond the statutory 120 days (90 days + 30 days). This hasn’t solved the problem; it has merely shifted the litigation burden to already overwhelmed High Courts, especially since the GST Tribunal, despite EIGHT long years of GST, remains a mythical creature, a distant dream. The disposal rate at the first appellate level is abysmal, while departmental “artists” continue to generate fresh truckloads of litigation with their creative interpretations.

Our Demands:

- Allocate more officers (competent ones, preferably) to clear the appeal backlog. Amend the provisions of Section 107 so as to confer more powers upon the Commissioner (Appeal), by allowing condonation of delay, in the interest of justice, where genuine reasons exist, especially when the primary fault lies with a non-existent Tribunal.

- The sight of High Courts adjudicating petty GSTR-1 vs GSTR-3B mismatches is, frankly, shameful. It demeans the stature of these institutions. To avoid such situations, adequate staffing is required to entertain and dispose of the first appeals in a timely manner.

- Materialize the GST Tribunal without any delay. Failure to do so will cement GST’s reputation as the biggest con job of our times.

11. The CGST-SGST-IGST Charade: Why Make the Public Privy to Your Internal Squabbles? Businesses across India don’t inherently mind paying taxes. What they vehemently mind is the farcical exercise of dissecting their payments into piecemeal chunks for Centre and State, and then being interrogated if one chunk was inadvertently larger than the other. When partners in a business earn, they don’t bill their clients based on their internal profit-sharing ratio. The world doesn’t care about their internal arithmetic; it cares about the final invoice. Making the entire nation a party to this meaningless CGST/SGST/IGST bifurcation from a public perspective is an utter debacle, adding layers of complexity with no discernible public benefit.

12. A Concluding Suggestion: The GSTCoin Proposition – A Glimmer of Hope?

We had previously floated an idea – GSTCoin – which, if implemented with sincerity, could potentially address some of the foundational issues of transparency, fraud, and efficiency. We would like to present the core concept in more concrete financial terms for your consideration during an official interaction in person on the said subject. The central idea involves a blockchain-based, non-tradable digital token exclusively for GST transactions.

As Suggestion:

- Issuance & Management: To be handled by an independent subsidiary operating under the aegis of the GSTN.

- Mechanism:

1. A supplier (Taxpayer ‘A’) needing to pay GST would purchase GST Coins from the GSTN subsidiary (e.g., via NEFT/RTGS into a designated treasury account). 1 GST Coin = 1 Rupee. These coins would be credited to Taxpayer A’s GST Coin wallet, linked to their GSTIN.

2. When Taxpayer A issues an invoice to a recipient (Taxpayer ‘B’), the GST amount on the invoice would be simultaneously transferred as GST Coins from A’s wallet. This transfer could be to B’s GST Coin wallet (representing Input Tax Credit – ITC) and/or directly to the Government’s GST Coin treasury wallet (as tax paid).

3. Taxpayer B could then use the GST Coins received as ITC to offset their output tax liability, by transferring them to the Government’s treasury wallet.

- Translated Benefits:

- Real-time Tax Remittance: Tax payment would be intrinsically linked to invoicing, ensuring that tax is remitted when an invoice is “validated” by a GSTCoin transfer. This would directly address fraudulent billing where tax is collected but not deposited.

- Verified Input Tax Credit: The recipient (Taxpayer B) would have assurance that their ITC is genuine, as it would be backed by an actual GSTCoin transfer from the supplier, thus minimizing disputes over fake invoicing for ITC.

- Assurance on Passing of Credit: For CAs, while certifying and attesting under the CGST Act, 2017, as to whether any credit has been passed on to the other party or not, it requires substantial inquisition at present. With GST Coin, the trail of cryptographic transaction would be substantive evidence to facilitate such certification.

- Automated Reconciliation: The blockchain ledger would provide an immutable, real-time record of all transactions and tax payments, largely automating and expediting GSTR-1, 2A/2B, and 3B reconciliation.

- Transparent Refunds: For exports or inverted duty structures, refunds could be processed more swiftly based on verified GSTCoin transactions, minimizing officer discretion and the scope for demanding “Alms.”

- Reduced Compliance Burden: The system would simplify return filing as most data would be captured transactionally.

- Enhanced Data Security: While blockchain offers transparency, cryptographic methods can be employed to ensure taxpayer privacy. The focus would shift from collated return data to secure transactional verification.

-

- Release of Working Capital: If at the eleventh hour, any business is not able to arrange funds for payment of GST due to limited banking hours, GSTCoins from friends, associate entities can be borrowed to pay the GST output liability. This can help entities lending GST Coins, to earn interest on that blocked working capital, which at present is not transferable, but with GST Coins it can be transferred to third parties using GSTIN as their wallet address.

This proposal is not presented as a panacea, but as a constructive direction worth exploring if the intent is to genuinely reform the GST system.

We trust that this representation, stemming from genuine concern and considerable businesses of this nation deserve a GST regime that is truly efficient and fair, not one characterized by bureaucratic inertia and opportunities for malfeasance. We await tangible action and meaningful reforms.

Regards,

For Chartered Accountants Association, Surat.

President | Chairman – Indirect Tax Committee

Copy to: –

(1) The Chairman

– for information and appropriate action

Central Board of Indirect Taxes & Customs (CBIC),

Ministry of Finance,

North Block, New Delhi – 110001

(2) The Hon’ble Cabinet Minister,

– for information and appropriate action

Ministry of Personnel, Public Grievances and Pensions,

Through PG Portal

(3) The Commissioner of State Tax

– for information and appropriate action

Rajya Kar Bhawan, Ashram Road, Ahmedabad – 380009, Gujarat

(4) The Finance Minister

– for information and appropriate action

Finance Department, Government of Gujarat,

Swarnim Sankul-1, Sachivalaya,

Gandhinagar – 382010