Tax Loss Harvesting in Indian Equity Markets (Strategic Realisation of Capital Losses to Optimise Tax Liability)

1. Introduction

This article is a note on tax harvesting, which is a legitimate and effective strategy under Indian tax laws that enables investors to:

-

Realise capital losses by selling underperforming shares

-

Offset those losses against capital gains

-

Potentially repurchase the same shares thereafter

-

Maintain the original investment thesis while optimising tax efficiency

This note outlines how tax harvesting works in the Indian listed equity shares and mutual fund context, with particular emphasis on matching:

Short-Term Capital Loss (STCL) with Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG)

Long-Term Capital Loss (LTCL) with Long-Term Capital Gains (LTCG)

2. Few points to be noted:

| Holding period | Tax Rate | Exemption (apart from basic exemption) | Set off | |

| Short-Term Capital Gains (STCG)/ Short Term Capital Losses (STCL) | 12 months or less | 20% (plus surcharge and cess) | Nil | STCL can be set off against STCG and LTCG |

| Long-Term Capital Gains (LTCG)/ Long Term Capital Losses (LTCL) | More than 12 months

|

12.5% (plus surcharge and cess) | Rs. 1,25,000/- (Rs. One Lakh Twenty-Five Thousand only) | LTCL can be set off only against LTCG |

3. Process of Tax Loss Harvesting:

| No | Steps | Checkmark |

| i. | Quantifying Gains of present financial till date and classifying as STCG/ LTCG | |

| ii. | Identifying shares with unrealised losses | |

| iii. | Selling those shares before 31 March | |

| iv. | Realising the capital loss | |

| v. | Using the realised loss to offset taxable gains | |

| vi. | Optionally buying back the same shares (often on the next trading day) | |

| vii. | Transactions must be genuine and executed at market price. |

4. Examples:

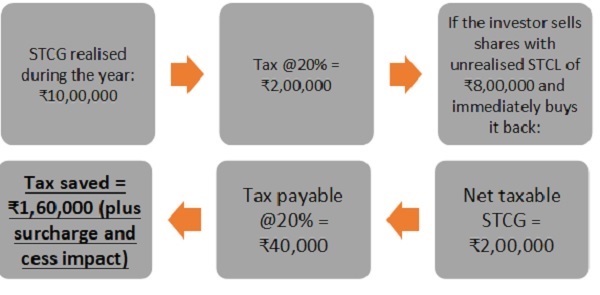

Example 1:

This is the most effective form of harvesting, especially for active traders or investors who have booked profits during volatile markets.

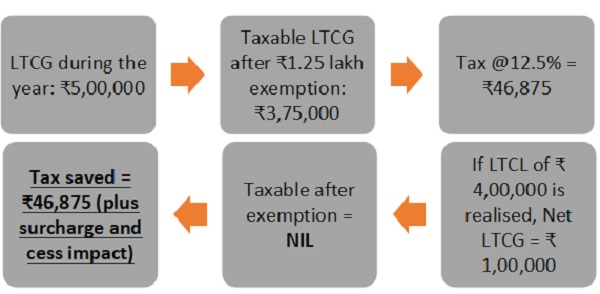

Example 2:

Utilising the annual exemption for LTCG:

Strategic realisation of LTCL can significantly reduce long-term capital gains tax exposure.

5. Important things to consider:

5.1. Properly select stocks to be sold and bought – aligning with portfolio requirements. If the long-term investment thesis remains intact, selling and repurchasing may be appropriate.

5.2. It’s most important to note that the First In First Out (FIFO) method applies. Shares bought first will be counted as Shares sold first. Hence calculation has to be careful to ensure correct match of losses with gains.

5.3. Ensure the loss category matches the gain category you intend to offset

5.4. Prioritise positions where losses are substantial enough to meaningfully reduce tax liability

5.5. Timing of selling and buying: Stocks should be sold near closing hours of Day 1 and bought immediately on opening of Day 2. This will prevent sharp price fluctuations and impact costs.

5.6. Tax considerations should not override sound portfolio construction. Avoid selling strategic core holdings purely for tax optics if re-entry risk is significant.

5.7. If capital losses exceed current year gains, they can be carried forward for 8 assessment years but timely filing of income tax returns is essential

5.8. Tax harvesting can be integrated with portfolio re-arrangement and exit from structurally weak positions

6. Conclusion

Tax loss harvesting is a prudent and legally permissible strategy within the Indian tax framework. When implemented thoughtfully, it can result in tangible savings. Tax efficiency should support — not override — investment discipline.

******

Disclaimer: This note is for informational purposes only and does not constitute investment advice. Tax positions should be evaluated in light of individual circumstances. We invite you to write at info@entrecap.in or call +71-7627872987 for particular advise on all income tax matters and corporate matters.

Author Bio