Day: December 16, 2017

13 articlesGoods and Services Tax

Goods and Services Tax

Inter-State e-way Bill to be compulsory from 1st February, 2018

Income Tax

Income Tax

CIT cannot treat AO’s order as erroneous and prejudicial to interest of revenue without conducting an enquiry and recording a finding

Income Tax

Income Tax

TNGST Act, 1959: Matter covered by certificate of settlement shall cannot be re-opened

Finance

Finance

MDR charges on transactions of value less than Rs. 2000 to be subsidised

Goods and Services Tax

Goods and Services Tax

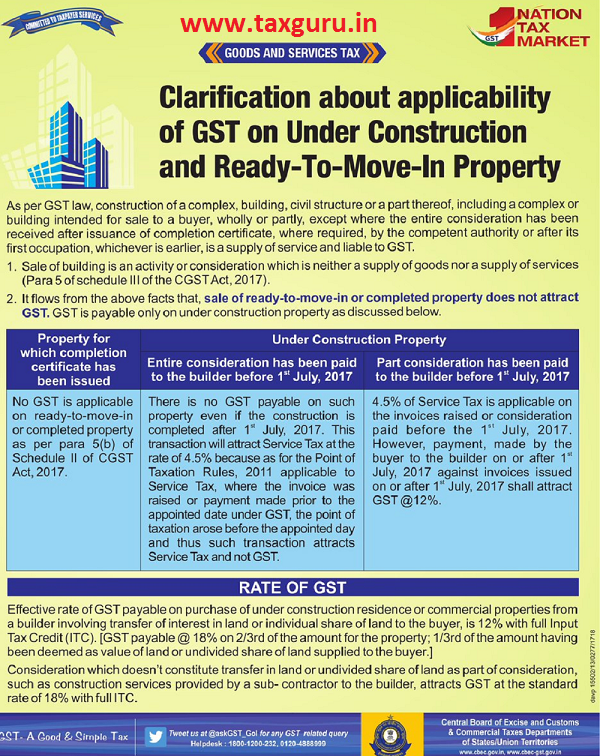

GST on Under Construction and Ready-To-Move-In Property

Goods and Services Tax

Goods and Services Tax

TNVAT: Assessees entitled to avail benefit of input tax credit, once turnover exceeds Rs. 50,00,000/- limit from Beginning of year: HC

Income Tax

Income Tax

Capital gain chargeable only on transferor and not on transferee: No Tax on firm on crediting Revaluation Surplus to Retiring Partners A/c

Income Tax

Income Tax

Section 13(3) : ITAT upheld exemption to trust who received grant from ABN AMRO Foundation & RBS Bank India

Income Tax

Income Tax

Order of AO not become erroneous merely because PCIT feels that further inquiry should have been made

Corporate Law

Corporate Law