Clarification about applicability of GST on Under Construction and Ready-To-Move-In Property

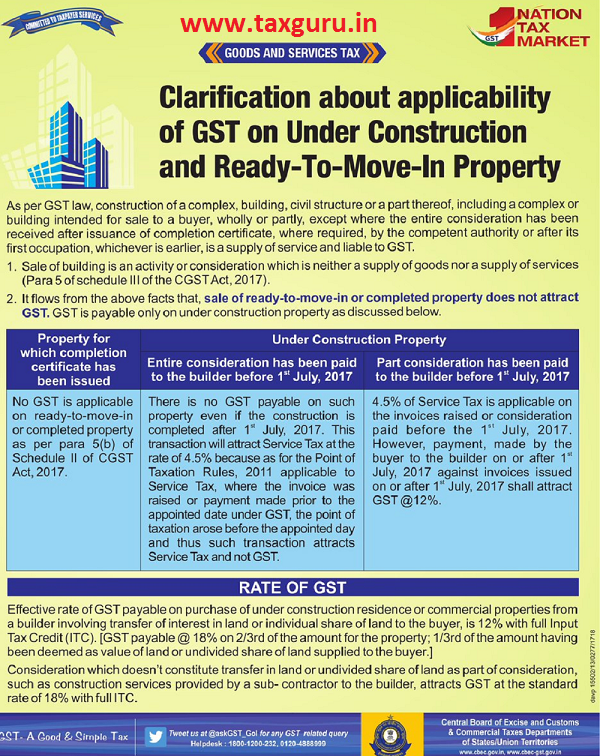

As per GST law, construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier, is a supply of service and liable to GST.

1. Sale of building is an activity or consideration which is neither a supply of goods nor a supply of services (Para 5 of schedule III of the CGST Act, 2017).

2. It flows from the above facts that, sale of ready-to-move-in or completed property does not attract GST. GST is payable only on under construction property as discussed below.

| Property for which completion certificate has been issued |

Under Construction Property |

|

| Entire consideration has been paid to the builder before 1st July, 2017 | Part consideration has been paid to the builder before 1st July, 2017 | |

| No GST is applicable on ready-to-move-in or completed property as per para 5(b) of Schedule II of CGST Act, 2017 | There is no GST payable on such property even if the construction is completed after 1st July, 2017. This attraction will attract Service Tax at the rate of 4.5% because as for the Point of Taxation Rules, 2011 applicable to Service Tax, where the invoice was raised or payment made prior to the appointed date under GST, the point of taxation arose before the appointed day and thus such transaction attracts Service Tax and not GST. | 4.5% of Service Tax is applicable on the paid before the 1st July, 2017. However, payment, made by the buyer to the builder on or after 1st July, 2017 against invoices issued on or after 1st July, 2017 shall attract GST @ 12% |

RATE OF GST

Effective rate of GST payable on purchase of under construction residence or commercial properties from a builder involving transfer of interest in land or individual share of land to the buyer, is 12% with full Input Tax Credit (ITC). [GST payable @ 18% on 2/3rd of the amount for the property; 1/3rd of the amount having been deemed as value of land or undivided share of land supplied to the buyer.]

Consideration which doesn’t constitute transfer in land or undivided share of land as part of consideration, such as construction services provided by a sub- contractor to the builder, attracts GST at the standard rate of 18% with full ITC.

Get More Information on GST under construction property here

Sir,

on 03.12.2024 we have booked a flat in gated community by paying token advance. Occupancy certificate was issued by competent authority on 31.12.2024. We have got the flat registered on 12.02.2025 by paying entire sale consideration. The seller charged 5% GST separately. Please clarify whether GST is applicable for our flat

Sir,

We have booked a flat in gated community on 03.12.2024 by paying token advance. Occupancy certificate was issued by competent authority on 31.03.2024. we have got registered the flat by paying entire sale consideration on 12.02.2025 in which the seller included 5% GST. Please clarify whether GST is applicable for my flat

I have purchase under construction flat for 45 lakhs the builder is asking to pay gst on registration value of 20 lakhs & work order value of 25 lakhs separately with GST of 5 percent I have to pay both or on only registration value only

Dear Sir, I have recently purchased office with 12% GST rate. I would like to pay Rs.15 Lakh at the time of possession and after B.U Permission. So after B.U Permission GST will be applicable on Rs.15 Lakh or not applicable as per GST rules.

Dear Sir,

I have booked under construction Flat Rs-17,60,550.00 (726 sqft*2425) +Extra development charges Rs- 50,820/-(726 sqft * 70) +Club Charges Rs- 21,780 (726sqft *30)+Documentation Charges -Rs-21500/-

Now there is two part respect to GST (8% & 18%)

Part A-8%

Total Rs-17,60,550.00 (726 sqft*2425)

Part B-18%

Total Rs-94,100 (50820+21780+21500)

If he demand Booking Amount 50000 & 4000 GST-No tax invoice given about RS – 4000/- GST

If he demand 10% within 30 days and he is calculation 8% GST of overall amount and then 10% is calculated.Is it ri8??

sir,

I have purchased a plot measuring 1200 sq.ft from a builder, who is developing gated community.

Now I have given contract for constructing a independent house at the rate of 1800/- per sq.ft. to the said developer. Please clarify whether i need to pay GST at 12%.

2. As per GST rules, it is only sale of

under -construction of building or flat , where completion certificate has not been issued by the authority, attracts GST .

3. I am under the impression that since there is only agreement to construct a house has been executed , no GST is payable by me.

4. Further there is no mention about GST in the agreement between me and developer.

5. Please advise me in this regard at an early date.

Thanking you Yours sincerely.

H.N.Divakaran

I PURCHASE A COMMERCIAL PROPERTY READY OFFICE FROM DIRECT BUILDER, GST LIABILITIES IS ON READY OFFICE OR GST FREE.

I am purchasing an under construction property from a party who is first party. The first party has paid the full payment with GST to builder.

Now whether again GST is applicable on resale of under construction flat of a building.???

I had booked an under construction flat sale agreement value 25lakhs affordable sector and had paid 25% agreement value plus 8% GST on 25%, and had applied for 75% hsg loan on sale agreement value, now the builder is asking me to pay full 75% GST on housing loan, The pocession is Dec’2021.

I want to pay gst as per demand letter as when the builder raise depending upon the construction work. Please guide me am i right i doing so

In an under construction project where the builder is registering the agreement on 10% is it right that he can demand 100% gst of total consideration even only 25% work is completed

I have made agreement in the year 2012 ,

and i have paid the vat amount to bullder before 1.07.17 but i have not paid service tax amount to him and he is giving position in as on 1.08.18 asking for GST 18% on my remaining consideration (i.e consideration includes MSEB & Society formation).please guide me in this situation wether i am liable to pay gst,Service amount during agreement?wheather i will get any rebate for my vat amount paid to builder

A flat including the building block had already been constructed by a builder before 1.7.2010 i.e. when Service tax on residential buidlings has not come into effect. But due to some or other reason, the flats could not be sold, but physical possession of which was given to the buyers of some other unconstructed flats(which were originally booked but had to be shifted to the unsold flats of this old building., under mutual agreement, by adjusting the advance payments made towards original unconstructed flats in other semi constructed blocks- as being towards these flats of this old pre-ST.GST building block which has recently been registered as phase-1 of the project by obtaining completion certificate from the competent authority..Some buyers had made full payments towards orginally allotted unconstructed flats before 1.7.2010 when ST has come into effect & in some cases ST was also recovered being originally made towards underconstruction flats/blocks. But with shifting to the old pre-ST constructed flats in the blocks, whether registration is now made after residual payments, if any left towards shifted readytomove flats of the pre-ST block, whether any GST is payable if transferred/registered now?

i am purchasing a flat in a building , this building was completed in 2016 but only one flat was left for sale which i am purchasing now.. so wil gst be applicable on it?

And builder is not asking for any GSTs ..can registry office ask for gst to be paid?

I want to buy a new flat which is ready to occupy. What would be GST rate applicable?

In 12th June 2017 i am book row house of Rs.2400000 and apply the loan at the time of disbursement. Row house stage of construction is 80 % so am excuted Reigester Agreement to Sale with builder on 27th June 2017 and got that am paid 147000 for service tax and 20000 Registration fees but now I want do sale deed with builder so he demanding GST do property and it’s is complete property so please suggest it’s applicable to me or not

i would like to know in this regards

If a Tenant receives flat from builder after redevelopment of building, Sales his flat before receipt of Part OC via sale agreement to third party for consideration

Will this transaction attract GST?

If Yes, then How much?

Under new GST reform, an under-construction property is being levied at the rate of 18%. However, it is not applied to the whole amount (value) of the property but it is applied only to the two-thirds value of the property.

GST Tax Rate on Booking Amount of Flat

As per the explanation provided for entire considered received before 1.7.2017 and on which ST is paid then no GST is applicable though construction not completed as on 1.7.17, then why the proviso 142(11)(C) is provide as supply is after 1.7.17. Pls. explain.

Please clarify what does mean first occupant …

Also i need some clarification …. I registered a flat in chennai on 14th July 2017…For this 90% of construction is completed before July 1st… only Bath room fittings and tile finishes are balance …is this condition the flat is considered as ready to occupy ???… whether i have to pay any GST for this ??… please expecting your suggestion i am very confused ….

the original allot-tee wants to sale his unit in a apartment and i want to purchase it. the apartment was completed in the year 2014 .the consideration with service tax was paid by the original allottee to builder,but registration was not taken place,now i want to purchase/transfer the above flat to his name after paying the consideration to the builder but the builder demanded G.S.T on the said matter ?

Sir,

We 2 partners have setup a business wherein we sell individual plots (purchased a large chunk of land, divided it into small plots, made roads, boundaries for individual plots, main gate, playing area, etc). Once full payment is realized the individual plot is registered in the name of the party by paying Stamp Duty & Registration charges as applicable

Is GST applicable on such a setup?

How much if YES?

Thanks

In the case of sale of an under construction flat the final sale price includes all the input taxes paid by the Builder.As GST is claimed to be a tax on Value Additiion what is the Taxable Value of the transaction as per section15 of the CGST Act.The FM may give a clarification on this point early.

To Admn.

This once again gives rise to the same point of grave doubt – repeatedly shared, through this website itself, in several instances, so also elsewhere. That is, whether as reported by the Print media not long ago, such a levy of GST on under-construction contracts had been a matter till then under consideration, with no final decision taken. Despite inquiries made independently, there has been no information available or forthcoming about any further developments.

You will do a favor to your readers in case have in possession any authentic information in that respect, clarifying whether or not any final decision has since been taken by the FM, and openly pronounced for the public having a vested interest- both promoters and buyers alike,

Thank for GST information which i look for many days..So third case still be applicable in below case-

Under construction Flat booked by paying initial amt + Service tax in Jan’2016 and completed registration and stamp duty payment in month of March-2016.(FY2015-16).

2017 Dec , till date 70% Construction completed.

Should builder be demanding GST from Flat purchaser as purchaser has already made payment of Service Tax in FY.2015-16 ?

In case of ready to move in property you says that there is no gst levied, than what about the Cenvat of Service tax w.r.t to builders

Whether ration of decision of Hon’ble Supreme Court of India in L & T Case (2013) has any impact under GST law? In case of property under construction, whether GST liable on the portion of the property already constructed by the builder at the time of entering of the buyer?