This is premium content. Please become a Premium member. If you are already a member, login here to access the full content.

Deduction u/s. 54 / 54EC cannot be denied for investment in joint names

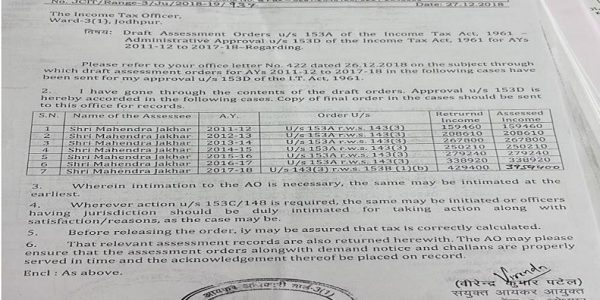

Case Law Details

- Case Name

- Director of Income-tax, International Taxation, Bangalore Vs Mrs. Jennifer Bhide (Karnataka High Court)

- Appeal Number

- Only available for paid members

- Date of Judgement/Order

- Only available for paid members

- Courts

- All High Courts, Karnataka High Court

Upgrade to Basic or Premium to download.

Already Upgraded? Log in.

A careful reading of section 54 as well as section 54EC makes it clear that when capital gains arise from the transfer of long term capital asset to an assessee and the assessee has, within the period of one year before or two years after the date on which the transfer took place purchase or has, within the period of three years after the date of transfer, construct residential house, then instead of capital gain being charged to income-tax as income of the previous year in which the transfer took place, it shall be dealt with in accordance with the provisions made under the section which gran...

Dear Sir,

My Father is thinking of selling his house which he is holding since 1957. He wishes to purchase a new residential property using the entire value/amount he is getting from selling his old house. He wishes to buy the new property in the joint name with his daughter-in-law. His daughter-in-law is not contributing a single penny for acquiring the new property. By reading the above case it seems that there will not be any Long Term Capital Gains Tax will applicable to him & he will be able to get full exemption from it.

Kindly confirm

Regards

Vijay Kapur

Dear Sir,

My Father is thinking of selling his house which he is holding since 1957. He wishes to purchase a new residential property using the entire value/amount he is getting from selling his old house. He wishes to buy the new property in the joint name with his daughter-in-law. His daughter-in-law is not contributing a single penny for acquiring the new property. By reading the above case it seems that there will not be any Long Term Capital Gains Tax will applicable to him & he will be able to get full exemption from it.

THANKS FOR SENDING IMPORTANT DECISION, IT WILL BENEFICIAL FOR THE CASES OF MY CLIENTS.

Thanks. This ruling makes clear that purchase of new property in joint name will not deprive the assessee benefit u/s 54 irrespective of the fact that old property was in the name of the assessee alone.