#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

Compensation/damage for settlement of dispute is capital receipt

Income Tax

Income Tax

Computation of Turnover in case of business of accommodation entries and applicability of Tax Audit

Income Tax

Income Tax

No Penalty U/s. 271AAA on Income surrendered during Assessment

Income Tax

Income Tax

Inclusion of Notional interest on interest-free security deposit in computation of annual value u/s 23(1)(b)

Income Tax

Income Tax

Treatment of interest income for deduction u/s 10B of Income Tax Act, 1961

Income Tax

Income Tax

Information given by DIT (Inv) can only be a reason to suspect not reason to believe

Income Tax

Income Tax

Assessment reopened merely based on details already on record is invalid

Income Tax

Income Tax

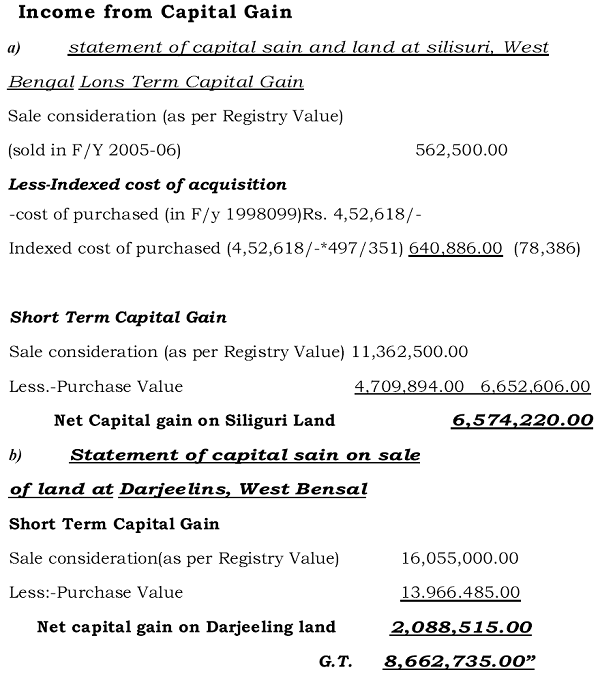

Addition justified for unexplained deposits in undeclared bank account

Income Tax

Income Tax

Travel expenses for seminar conducted abroad for medical practitioners with financial aid of Pharmaceuticals Company allowable

Income Tax

Income Tax