#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

Addition for Cash deposit in Bank explained without supporting documents justified

Income Tax

Income Tax

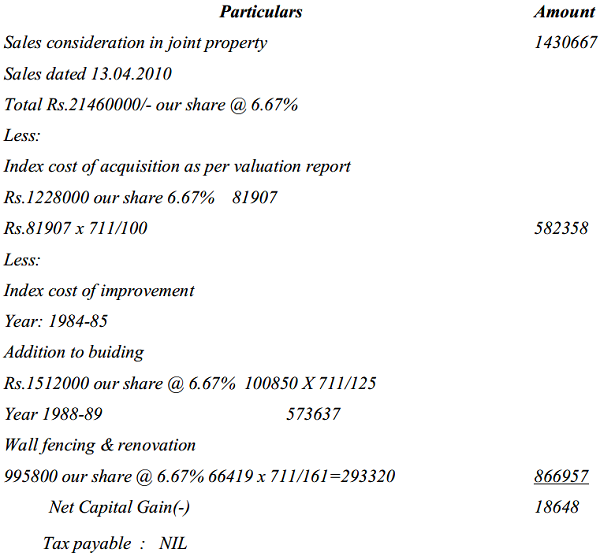

Deduction U/s. 54F can be claimed against Gain on Multiple Assets in Multiple Years

Income Tax

Income Tax

S. 68 Cash Receipt from Debtors: Addition justified on failure to prove

Income Tax

Income Tax

Bank passbook cannot be treated as books of accounts

Income Tax

Income Tax

Subsidy based on reimbursement of sales tax – revenue or capital receipt?

Income Tax

Income Tax

Addition U/s. 68 for Alleged unaccounted stock merely based on value of closing stock declared to banks is not sustainable

Income Tax

Income Tax

Discount cannot be treated as bogus merely because some parties denied it

Income Tax

Income Tax

ITAT allows Finance Charges paid to NBFCs without TDS deduction as NBFCs included the same in their Income

Income Tax

Income Tax

ITAT confirms addition for Bogus LTCG

Income Tax

Income Tax