The Securities and Exchange Board of India (SEBI) has released a consultation paper proposing measures to strengthen the governance and operational framework of Market Infrastructure Institutions (MIIs) like stock exchanges and depositories. This initiative is in response to the significant growth in MIIs’ investor base, volumes, revenue, and profitability, emphasizing their critical role as first-line regulators and public utilities. The proposals focus on three key areas: mandating the appointment of two Executive Directors (EDs) to the Governing Board, one for “Critical Operations” and another for “Regulatory, Compliance, Risk Management, and Investor Grievances”; clearly defining the roles and responsibilities of the Managing Director (MD), the proposed EDs, and key management personnel such as the Chief Technology Officer (CTO) and Chief Information Security Officer (CISO); and establishing clear norms for directorships of MDs and EDs in other companies. These measures aim to ensure that MIIs prioritize public interest, technology, operations, and risk/compliance over commercial considerations, foster robust succession planning, and enhance the safety and reliability of the securities market. SEBI is inviting public comments on these proposals until July 15, 2025.

Securities and Exchange Board of India

Jun 24, 2025 | Reports : Reports for Public Comments

Consultation Paper: Strengthening Governance of Market Infrastructure Institutions (MIIs)

Executive Summary

1. In recent years, large MIIs such as Stock Exchanges, Clearing Corporations and Depositories have seen a rapid increase in investor base and volumes, and a growing network of intermediaries associated with them. Alongside, they have experienced significant growth in revenue and profitability, and they enjoy high profit margins. In this context, given the vital role MIIs play as first-line regulators and public utilities in the cause of capital formation, this consultation paper outlines proposals aimed at strengthening the operational and governance framework of MIIs. The proposed steps aim to further ensure that MIIs accord highest priority to public interest, technology and operations, and risk and compliance, over commercial considerations.

2. Our proposals focus on three key areas:

2.1. Appointment of Two Executive Directors (EDs) to the Governing Board: Mandating the appointment of two EDs, each heading “Vertical 1: Critical Operations” and “Vertical 2: Regulatory, Compliance, Risk Management, and Investor Grievances,” as Key Management Personnel (KMPs) and will serve on the MII’s Governing Board.

2.2. Defining Roles and Responsibilities: Clearly outlining the broad roles and responsibilities of the Managing Director (MD), the proposed EDs, and specific KMPs such as the Chief Technology Officer (CTO) and Chief Information Security Officer (CISO) and

2.3. Norms on Directorships: Establishing clear norms for the directorships of MDs and the proposed EDs of an MII in other companies.

3. These measures are designed to instil a culture that prioritizes regulatory and operational excellence at both the Governing Board and operating levels of MIIs. They will also ensure robust succession planning and adept governance structures to reflect the increasing complexity and significance of MIIs. Further, this approach not only enhances the safety and reliability of the securities market but also fosters an environment conducive to innovation.

Part A: Appointment of Two EDs of Appropriate Stature and Independence as Heads of Vertical 1 and Vertical 2 and also on the Governing Board of MIIs

4. Objective

4.1. The significant growth observed in MIIs, highlighted by increased revenues, profits, an expanding network of intermediaries, and a rapidly growing investor base, necessitates a heightened focus on their role as first-line regulators. To ensure the orderly functioning and development of the securities market, it is crucial that MIIs give priority to, and are seen to give priority to, public interest (represented by Vertical 1 – Critical Operations, and Vertical 2 – Regulatory, Compliance, Risk Management, and Investor Grievances) over commercial interests and business development (Vertical 3).

5. Background

5.1. MIIs serve as the backbone of the capital market, providing essential infrastructure for trading, clearing & settlement, and holding of securities. Their unique operating model empowers them to regulate their paying members and listed companies. While they operate as efficient and competitive commercial entities, their primary mandate is to serve as crucial public utilities and first-line regulators for capital markets.

5.2. The Governing Board of an MII, comprising of the MD, Non-Independent Directors (NIDs), and Public Interest Directors (PIDs), plays a vital role in ensuring that public interest is prioritized in all MII operations. Currently, SEBI mandates an equal or higher number of PIDs on the governing board to ensure primacy of public interest.

5.3. Regulatory oversight of MIIs is primarily governed by various Acts and Regulations, including the Securities Contracts (Regulation) Act, 1956, the SEBI Act, 1992, and the Depositories Act, 1996, along with specific regulations like Securities Contracts (Regulation) (Stock Exchanges and Clearing Corporations) Regulations, 2018 (hereinafter referred to as “SECC Regulations, 2018”), SEBI (Depositories and Participants) Regulations, 2018 (hereinafter referred to as “D&P Regulations, 2018”). SEBI approves the appointment of PIDs and the MD based on Governing Board recommendations, and the Governing Board approves the appointment, re-appointment, termination, and resignation of specific KMPs like the Compliance Officer (CO), Chief Risk Officer (CRiO), CTO, and CISO.

5.4. MIIs are mandated to segregate their functions into three verticals:

5.4.1. Vertical 1: Critical Operations (e.g., trading, clearing & settlement, securities holding).

5.4.2. Vertical 2: Regulatory, Compliance, Risk Management, and Investor Grievances.

5.4.3. Vertical 3: Other functions, including business development.

5.5. Functions under Verticals 1 and 2 must be given higher priority in resource allocation, with MIIs periodically assessing their adequacy. While regulatory frameworks are regularly reviewed, changes are introduced calibrately to foster innovation and overall economic growth. Therefore, governance norms must be carefully tailored to ensure market safety and reliability while preserving the MIIs’ ability to innovate.

6. Need for Review

6.1. The phenomenal growth in the securities market over recent years, driven by increased market capitalization, trading volumes, technology adoption, investor base, and market intermediaries has significantly amplified the role of MIIs as first-line regulators. Any failure or mis-governance in these critical institutions could have an adverse impact on the securities market and the broader economy.

6.2. Evidence of this growth is clearly visible in various parameters

6.2.1. Financials of MIIs: As shown in Table 1 (all tables are enclosed at Annexure-1), certain MIIs have demonstrated substantial growth in revenue and profit after tax (PAT) over the financial years 2022-23 to 2024-25.

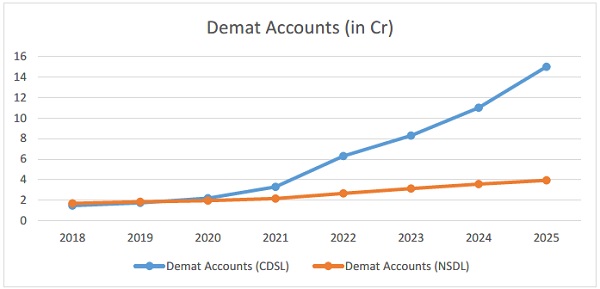

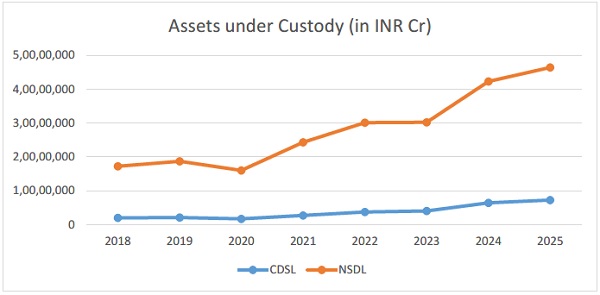

6.2.2. Growth in Demat Accounts and Assets under Custody:

Source – CDSL, NSDL websites and Annual Reports

Source – CDSL, NSDL websites and Annual Reports

6.2.3. Growth in Total Funds Pay-in: Tables 2 and 3 illustrate the significant increase in funds pay-in for both cash and derivatives markets (including commodity derivatives), across various clearing corporations from FY 2021-22 to FY 202425.

6.2.4. Significant Increase in Derivatives Turnover: Tables 4, 5, and 6 highlight the substantial notional turnover growth in equity and commodity derivatives segments across major exchanges over the past few financial years.

6.2.5. Increase in Resource Mobilization by Issuers in Primary Market (Equity): Table 7 demonstrates the significant increase in the number of companies listed and the value of total issues through IPOs on NSE and BSE.

6.2.6. Significant Increase in Technology-related Expenses: Table 8 shows a consistent increase in computer technology and IT-related expenses for various MIIs, reflecting the growing reliance on robust technology infrastructure.

6.2.7. Data on Dividend Paid to Shareholders: Table 9 indicates substantial dividends paid to shareholders by some MIIs, underscoring their commercial success.

6.3. This growth unequivocally demonstrates that the role of MIIs as first-line regulators has become more critical, making the prioritization of public interest (Vertical 1 and Vertical 2) over commercial interests (Vertical 3) even more imperative for market integrity.

6.4. Currently, the MD holds overall authority for all three Verticals. Further, there is often a significant gap in authority, stature, and compensation between the MD and other KMPs, with only the MD currently serving on the Governing Board of MIIs.

6.5. To ensure adequate resource allocation to Verticals 1 and 2, and to ensure that these critical functions are not constrained by commercial considerations, capable and empowered KMPs of stature are needed to head these verticals. These KMPs are vital for maintaining appropriate compliance, risk management, technology infrastructure, and information security.

6.6. Having these senior executives on the Governing Board will ensure timely addressing of concerns related to Verticals 1 and 2, facilitating timely communication to the Governing Board, Statutory Committees, and SEBI for corrective actions. Furthermore, their presence on the Board will aid in effective succession planning. This practice of including senior executives beyond the MD on the Governing Board is also prevalent in many top 100 listed companies.

7. Proposals

Based on the foregoing, we propose the following measures to strengthen MII governance:

7.1. Appointment of EDs:

7.1.1. In addition to the MD, MIIs shall appoint two KMPs, designated as EDs (or equivalent), to head Vertical 1 and Vertical 2, respectively. These EDs shall be members of the MII’s Governing Board.

7.1.2. MIIs may, at their discretion, appoint an ED for Vertical 3.

7.1.3. While the MD will continue to oversee the overall MII, the appointed EDs must be of comparable stature to the MD.

7.1.4. The appointment and re-appointment process for these EDs will be similar to that of the MD, requiring prior SEBI approval and as specified by SEBI from time to time.

7.2. Reporting Structure for EDs:

7.2.1. For administrative purposes, EDs will continue to report to the MD.

7.2.2. The Standing Committee on Technology (SCOT) shall hold separate quarterly meetings with the ED of Vertical 1, without the MD’s presence. The SCOT shall independently assess the ED, and the Nomination and Remuneration Committee (NRC) shall consider inputs of both the SCOT and the MD in finalising the appraisal of the ED of Vertical 1.

7.2.3. The Regulatory Oversight Committee (ROC) and Risk Management Committee (RMC) shall hold separate quarterly meetings with the ED of Vertical 2, without the MD’s presence. The ROC and RMC shall independently assess the ED, and the NRC shall consider inputs of the ROC, RMC and the MD in finalising the appraisal of the ED of Vertical 2.

7.2.4. EDs are required to report to the Governing Board and SEBI quarterly on matters concerning their respective verticals. As and when necessary, the EDs shall directly raise issues to the Governing Board and SEBI.

7.3. Reporting to EDs:

7.3.1. All Heads of Department within Vertical 1, including the CTO and CISO, shall report to the ED of Vertical 1. Similarly, all Heads of Department within Vertical 2, including the CO and CRiO, shall report to the ED of Vertical 2.

7.4. Recognizing the heterogeneous nature of MIIs (size, financial health, growth stage), MIIs facing practical difficulties in complying with these provisions may seek exemptions from SEBI, which will be evaluated on a case-by-case basis.

Part B: Roles and Responsibilities of MD, EDs, and Specific KMPs (CO, CRiO, CTO, and CISO)

8. Background

8.1. Current SECC Regulations, 2018, and D&P Regulations, 2018, define the MD and outline the definitions, roles, and responsibilities of CO and CRiO, as well as a Code of Conduct for Directors and KMPs. While specific circulars address the MD’s responsibilities in certain areas, there is no comprehensive provision in the Regulations covering the MD’s and KMPs’ overall roles and responsibilities. The definitions and roles of CTO and CISO are currently prescribed via circulars, not within the Regulations.

8.2. Industry Norms

8.2.1. SEBI (Mutual Funds) Regulations, 1996: The CEO of an Asset Management Company (AMC) is responsible for ensuring compliance, safeguarding unit holder interests in investments, and overseeing the overall risk management function. The CEO must also ensure adherence to the Code of Conduct for Fund Managers and Dealers, with any breaches reported to the Board and Trustees.

8.2.2. Banking Regulations Act, 1949: Section 10B (1) mandates that every banking company appoint a whole-time Chairman or MD to manage its entire affairs.

8.2.3. These industry norms demonstrate that the roles and responsibilities of the MD/CEO are broadly defined in other regulated sectors.

9. Need for Review

9.1. The existing Regulations lack clear definitions and broad roles for the MD and certain KMPs viz. CTO and CISO. It is imperative to embed these definitions and roles within the Regulations to ensure management’s unwavering focus on its core public interest mandate such as prioritizing technological resilience, market integrity, risk management and compliance over commercial considerations. Furthermore, the broad roles and responsibilities of the proposed EDs for Verticals 1 and 2 also need to be clearly prescribed. Discussions within the Secondary Market Advisory Committee (SMAC) have also recommended defining and segregating the roles and responsibilities of the MD and these four KMPs within the regulations.

10. Proposals

Based on the above, the broad roles and responsibilities of the MD, ED and specific KMPs shall include the following:

10.1. Roles and Responsibilities of the MD:

10.1.1. The MD shall be entrusted with the overall management of the MII’s affairs.

10.1.2. The MD shall ensure the MII’s compliance with all applicable Regulations (SECC Regulations, 2018 or D&P Regulations, 2018) and related guidelines/circulars.

10.1.3. The MD shall ensure that functions under Verticals 1 and 2 operate in the interest of the securities market and are responsible for the MII’s overall risk management, and

10.1.4. The MD shall at all times ensure the MII has adequate infrastructure and systems for efficient functioning.

10.2. Roles and Responsibilities of the EDs:

10.2.1. The EDs shall be responsible for the overall affairs of their respective Verticals.

10.2.2. The EDs shall ensure that functions under their respective Vertical operate in the interest of the securities market, guided by public interest, and without revenue-oriented objectives, and

10.2.3. The ED of Vertical 2 shall also be responsible for the MII’s overall risk management.

10.3. Roles and Responsibilities of the CISO:

10.3.1. Assess, identify, and reduce cybersecurity risks; respond to incidents; establish appropriate standards and controls; and direct the establishment and implementation of processes and procedures as per the cybersecurity and cyber resilience policy approved by the governing board.

10.4. Roles and Responsibilities of the CTO:

10.4.1. Oversee and manage overall technology-related system design, infrastructure, and operations.

10.4.2. Be accountable for managing risks in all IT-related functions.

10.4.3. Responsible for IT policy and the IT Risk Management Framework.

Part C: Directorships of MD and EDs of an MII in Companies other than Subsidiaries

11. Background

11.1. Regulation 25, clause 4 of the SECC Regulations, 2018, restricts the MD of a recognized stock exchange or recognized clearing corporation from being a shareholder or associate of a shareholder, a trading or clearing member or their associate/agent, or holding concurrent positions in a subsidiary or any other associated entity, with a proviso allowing directorship (but not as MD) in a subsidiary. Similar provisions exist for MDs of depositories under D&P Regulations, 2018.

11.2. The Banking Regulations Act, 1949, specifically Sections 10B (2) and (4), place significant restrictions on the directorships of a whole-time Chairman or MD of a banking company in other companies, firms, or commercial concerns, with an exception for directorships in subsidiaries or Section 25 (now Section 8) companies. Section 8 of the Companies Act, 2013, pertains to companies formed with charitable objects, where profits are applied to promote these objects, and no dividends are paid to members.

12. Need for Review

12.1. Currently, there are no clear norms on external directorships of MDs (in companies other than subsidiaries) creating potential governance risks. Given the MD’s full-time role and the significant growth of the securities market, the MD’s role as a first-line regulator has become increasingly critical. The absence of clear provisions in this regard could lead to various risks, including conflicts of interest, divided focus, and reputational risk. Similar restrictions on directorships are observed in the banking industry.

12.2. The Secondary Market Advisory Committee (SMAC) has recommended that, in addition to a subsidiary company, the MD of an MII should be permitted to serve as a non-executive director of a company registered under Section 8 of the Companies Act, 2013, and an unlisted State/Central Government Company not engaged in any commercial activity. Furthermore, norms for the directorships of the EDs of Verticals 1 and 2 also need to be prescribed.

13. Proposals

In view of the above, the following are proposed:

13.1. The MD may be permitted to be appointed as a non-executive director on the board of:

13.1.1. A company registered under Section 8 of the Companies Act, 2013, and 13.1.2. An unlisted State/Central Government Company that is not involved in any commercial activity.

13.2. The EDs of an MII shall not serve on the board of any other company, except for a subsidiary of the MII.

14. Indicative Amendments (Based on the proposals at Part A, B and C)

14.1. In light of the proposals outlined in Parts A, B, and C, indicative amendments to both SECC Regulations, 2018, and D&P Regulations, 2018, are provided in Annexure-2.

********

Public Comments on this Consultation Paper

We invite public comments on these three proposals for Strengthening Governance of Market Infrastructure Institutions (MIIs).

Please submit your comments/suggestions by July 15, 2025, through the following link:

https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPubl icComments=yes

Should you encounter any technical issues with the web-based public comments form, you may send your comments via email to aditya@sebi.gov.in, yerasiv@sebi.gov.in, and mrd_pod3@sebi.gov.in.

Please use the subject line: “Strengthening Governance of Market Infrastructure Institutions (MIIs)” and refer to the proposals in paragraphs above.

Issued on: June 24, 2025